AIサーバー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

AI Server Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 320 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801945

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

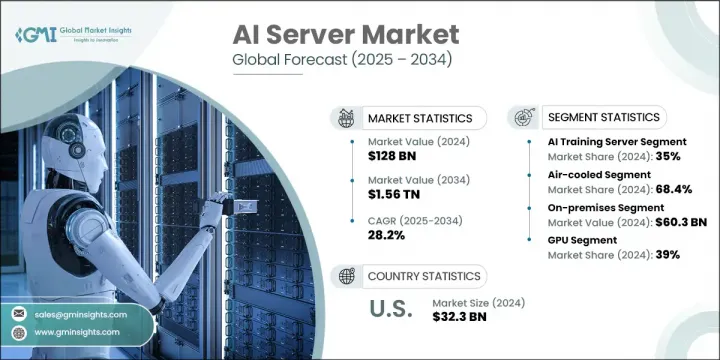

AIサーバーの世界市場規模は、2024年に1,280億米ドルとなり、CAGR 28.2%で成長し、2034年には1兆5,600億米ドルに達すると推定されています。

この急成長の背景には、さまざまな業界でAI技術が急速に採用され、複雑化するAI主導のワークロードをサポートする堅牢なサーバーへの要求が高まっていることがあります。AIが製造、金融、ヘルスケアなどの分野を変革し続ける中、ハイパフォーマンス・コンピューティング・インフラに対する需要が急増しています。ハイブリッド環境、エッジ展開、リアルタイムデータ処理の台頭は、AIサーバーの需要の上昇をさらに後押ししています。企業運用における生成AI、予測分析、自動化への注目の高まりは、AIに最適化されたインフラへの巨額投資を企業に促し、この分野の収益と技術革新の両方を促進しています。

北米は、クラウドプロバイダーとAI半導体企業の確立されたエコシステムに支えられ、AIサーバー導入のトップランナーであり続けています。同地域は、強力な機関投資と政府支援のAIイニシアチブの恩恵を受けており、持続的なイノベーションを可能にしています。エッジAIコンピューティングは、特にヘルスケア、スマート産業、自動化システムなどのデータ集約的な垂直市場において、市場を変革するトレンドとして浮上しています。こうした使用事例では、現場でのデータ処理に特化したAIアクセラレーターを搭載したコンパクトで電力効率の高いサーバーが必要とされ、集中型のクラウドネットワークに大きく依存する必要がなくなります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,280億米ドル |

| 予測金額 | 1兆5,600億米ドル |

| CAGR | 28.2% |

AIトレーニングサーバー分野は2024年に35%のシェアを占め、2025年から2034年にかけてCAGR 26%で成長すると予測されています。このセグメントは、より多くの組織が高度な機械学習、コンピュータビジョン、生成AIシステムを採用するにつれて勢いを増しています。AIに特化したプロセッサやGPUを搭載したこれらの高性能サーバは、大規模なデータセットや複雑な学習モデルを処理するために不可欠です。企業や研究機関による支出の増加は、AIトレーニングがイノベーションと競合戦略に不可欠となるため、このセグメントの成長を強化しています。

空冷AIサーバーセグメントは2024年に68.4%のシェアを占め、2034年まで27%のCAGRで成長すると予測されています。これらのシステムは、設置が簡単で、コストが低く、メンテナンス要件が単純であるため、引き続き優位を占めています。エアフロー管理、熱制御、シャーシ設計の技術的進歩により、これらのサーバーはより高密度なAIワークロードをサポートできるようになり、インフラリソースが限られたエッジ環境や企業施設への導入に理想的なものとなっています。

米国AIサーバー市場は2024年に323億米ドルを生み出し、80%のシェアを占めました。成長は、製造環境におけるAI主導のロボット工学と自動化の統合に強く影響されています。次世代サーバーの生産がますます複雑化する中、メーカーは自動化を活用して業務を合理化し、精度を向上させ、人件費を削減しています。スケーラブルで高効率なAIインフラの推進は、工場フロアを再構築し、AIを推進するシステム構築におけるインテリジェントマシンの役割を強調しています。

世界のAIサーバー市場を形成している主要企業には、マイクロソフト、デル、富士通、Nvidia、IBM、Super Micro Computer、Hewlett Packard Enterpriseなどがあります。AIサーバー分野の企業は、より強固な市場ポジションを確保するため、多方面にわたる戦略に注力しています。これには、AIサーバーポートフォリオを拡大し、トレーニングと推論の両方のアプリケーションに対応することや、エネルギー効率の高い冷却ソリューションの開発などが含まれます。大手企業はAIソフトウェアベンダーや半導体メーカーと協力し、完全に最適化されたシステムを提供しています。サプライチェーンリスクを低減しつつ、地域需要の高まりに対応するため、ローカライズされた製造と自動化への投資を増やしている企業もあります。クラウド統合、スケーラブルな設計、迅速な展開能力は、ヘルスケア、金融、自律システムなどの高成長垂直市場に参入するための戦略的提携とともに、製品イノベーション戦略の中心であり続けています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料供給者

- 部品供給業者

- ハードウェアプロバイダー

- 最終用途

- コスト構造

- 利益率

- 各段階での付加価値

- サプライチェーンに影響を与える要因

- 破壊者

- サプライヤーの情勢

- テクノロジーとイノベーションの情勢

- 現在の技術

- GPUとAIアクセラレータの進化

- 液体冷却システムと高度な熱管理

- 高帯域幅メモリ(HBM)と高度なメモリテクノロジー

- エッジAIと分散コンピューティングを強化

- 新興技術

- 量子コンピューティングの統合

- ニューロモルフィックコンピューティングと脳に着想を得たプロセッサ

- フォトニックコンピューティングと光インターコネクト

- AI専用シリコンとカスタムASIC

- イノベーションエコシステムとパートナーシップ

- テクノロジーパートナーシップ戦略

- イノベーション加速メカニズム

- 現在の技術

- 特許分析

- 価格分析

- コスト構造分析

- 主なニュースと取り組み

- 規制情勢

- AIサーバー動向, 2020-2024

- 冷却別のコスト構造の内訳

- AIサーバーの平均寿命

- CSPとOEMによるサーバー調達量, 2020-2024

- CSPとOEMによる地域的なAIサーバーの展開, 2020-2024

- AIサーバー製品統合:社内vsアウトソーシング, 2020-2024

- サーバーによる電力消費

- メンテナンスコスト:OEM vs.サードパーティ

- 部品別の故障率

- AIサーバー市場ケーススタディ

- マイクロソフトのAzure AIインフラストラクチャ変革

- GoogleのTPUベースのカスタムシリコン戦略

- テスラの完全自動運転向けAIトレーニングインフラ

- 今後の展望と提言

- 市場の変革と成長軌道

- 戦略的インフラの推奨事項

- 規制遵守と持続可能性の枠組み

- 長期的な成功戦略とエコシステム開発

- 影響要因

- 促進要因

- 爆発的な企業AI導入と実証済みの投資収益率

- 大規模なクラウドインフラの拡張と投資

- エッジコンピューティングの成長とリアルタイム処理の需要

- AIワークロードの高性能コンピューティング要件

- 業界の潜在的リスク&課題

- 天文学インフラのコストと電力消費

- 重要なスキルの不足と技術的な複雑さ

- 規制遵守とデータ主権の要件

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:サーバー別、2021年~2034年

- 主要動向

- AIデータ

- AIトレーニング

- AI推論

- その他

第6章 市場推計・予測:ハードウェア別、2021年~2034年

- 主要動向

- ASIC

- FPGA

- グラフィックプロセッサ

- その他

第7章 市場推計・予測:冷却技術別、2021年~2034年

- 主要動向

- 空冷式

- パッシブ空気冷却

- アクティブ空気冷却

- 精密空調

- 封じ込めソリューション

- 液冷式

- ダイレクト・トゥ・チップ

- 浸漬冷却

- 単相

- 二相

- ハイブリッド冷却システム

第8章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- オンプレミス

- クラウドベース

- ハイブリッド

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- IT・通信

- 輸送・自動車

- BFSI

- 小売業・eコマース

- ヘルスケア・医薬品

- 産業オートメーション

- その他

第10章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- OEM

- クラウドサービスプロバイダー(CSP)

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベルギー

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- シンガポール

- 韓国

- ベトナム

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- 世界企業

- Advanced Micro Devices

- Intel

- NVIDIA

- Cisco Systems

- サーバーシステム製造業

- Dell

- Hewlett Packard Enterprise

- Huawei

- Inspur

- International Business Machines

- Lenovo

- Super Micro Computer

- ハイパースケールおよびクラウドプロバイダー

- Amazon Web Services

- Microsoft

- Oracle

- 新興企業と地域企業

- Foxconn(Hon Hai)

- Fujitsu

- Inventec

- Quanta Computer

- Wistron

目次

The Global AI Server Market was valued at USD 128 billion in 2024 and is estimated to grow at a CAGR of 28.2% to reach USD 1.56 trillion by 2034. This surge is being fueled by the rapid adoption of AI technologies across various industries and the growing requirement for robust servers to support increasingly complex AI-driven workloads. As AI continues to transform sectors such as manufacturing, finance, and healthcare, demand for high-performance computing infrastructure is surging. The rise of hybrid environments, edge deployments, and real-time data processing further supports the upward trajectory of AI server demand. Enhanced focus on generative AI, predictive analytics, and automation in enterprise operations is pushing organizations to invest heavily in AI-optimized infrastructure, driving both revenue and technological innovation in this space.

North America remains the front runner in AI server deployment, supported by an established ecosystem of cloud providers and AI semiconductor firms. The region benefits from strong institutional investments and government-backed AI initiatives, enabling sustained innovation. Edge AI computing has emerged as a transformative trend in the market, especially in data-intensive verticals such as healthcare, smart industry, and automated systems. These use cases require compact, power-efficient servers with specialized AI accelerators for on-site data processing, eliminating the need to rely heavily on centralized cloud networks.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $128 Billion |

| Forecast Value | $1.56 Trillion |

| CAGR | 28.2% |

The AI training servers segment held 35% share in 2024 and is projected to grow at a CAGR of 26% between 2025 and 2034. The segment is gaining momentum as more organizations adopt advanced machine learning, computer vision, and generative AI systems. These high-performance servers, equipped with AI-specific processors and GPUs, are crucial for handling large datasets and complex training models. Increased spending from enterprises and research institutions is reinforcing the growth of this segment, as AI training becomes integral to innovation and competitive strategy.

The air-cooled AI servers segment held 68.4% share in 2024 and is expected to grow at a 27% CAGR through 2034. These systems continue to dominate due to their straightforward installation, lower costs, and simpler maintenance requirements. Technological advancements in airflow management, thermal control, and chassis design have allowed these servers to support more dense AI workloads, making them ideal for deployment in edge environments or enterprise facilities with limited infrastructure resources.

United States AI Server Market generated USD 32.3 billion in 2024 and held 80% share. Growth is strongly influenced by the integration of AI-driven robotics and automation in manufacturing environments. As production of next-generation servers becomes increasingly complex, manufacturers are leveraging automation to streamline operations, improve accuracy, and cut down on labor costs. The push for scalable, high-efficiency AI infrastructure is reshaping factory floors, emphasizing the role of intelligent machines in building the very systems that drive AI forward.

The major companies shaping the Global AI Server Market include Microsoft, Dell, Fujitsu, Nvidia, IBM, Super Micro Computer, and Hewlett Packard Enterprise. To secure stronger market positions, companies in the AI server space are focusing on multi-pronged strategies. This includes expanding their AI server portfolios to cater to both training and inference applications and developing energy-efficient cooling solutions. Leading firms are collaborating with AI software vendors and semiconductor producers to deliver fully optimized systems. Several players are increasing investments in localized manufacturing and automation to meet rising regional demand while reducing supply chain risk. Cloud integration, scalable design, and rapid deployment capabilities remain central to product innovation strategies, along with strategic alliances to penetrate high-growth verticals such as healthcare, finance, and autonomous systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Data mining sources

- 1.2.1 Global

- 1.2.2 Regional/Country

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Type

- 2.2.4 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Hardware providers

- 3.1.1.4 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.2.1 Current technologies

- 3.2.1.1 GPU and AI accelerator evolution

- 3.2.1.2 Liquid cooling system and advanced thermal management

- 3.2.1.3 High-bandwidth memory (HBM) and advanced memory technology

- 3.2.1.4 Power edge AI and distributed computing

- 3.2.2 Emerging technologies

- 3.2.2.1 Quantum computing integration

- 3.2.2.2 Neuromorphic computing and brain-inspired processor

- 3.2.2.3 Photonic computing and optical interconnects

- 3.2.2.4 AI-Specific Silicon and Custom ASICs

- 3.2.3 Innovation ecosystem and partnerships

- 3.2.3.1 Technology partnership strategy

- 3.2.3.2 Innovation acceleration mechanisms

- 3.2.1 Current technologies

- 3.3 Patent analysis

- 3.4 Pricing analysis

- 3.5 Cost structure analysis

- 3.6 Key news and initiatives

- 3.7 Regulatory landscape

- 3.8 AI server trends, 2020-2024

- 3.9 Cost structure breakdown by cooling

- 3.10 Average lifespan of AI servers

- 3.11 Server procurement volume by CSPs and OEMs, 2020-2024

- 3.12 Regional AI server deployment by CSPs and OEMs, 2020-2024

- 3.13 AI server product integration: In-house vs outsourced, 2020-2024

- 3.14 Power consumption by server

- 3.15 Maintenance cost: OEM vs. third party

- 3.16 Failure rate by component

- 3.17 AI server market case studies

- 3.17.1 Microsoft's Azure AI infrastructure transformation

- 3.17.2 Google's TPU-based custom silicon strategy

- 3.17.3 Tesla's AI training infrastructure for full self-driving

- 3.18 Future outlook and recommendations

- 3.18.1 Market transformation and growth trajectory

- 3.18.2 Strategic infrastructure recommendations

- 3.18.3 Regulatory compliance and sustainability framework

- 3.18.4 Long-term success strategies and ecosystem development

- 3.19 Impact forces

- 3.19.1 Growth drivers

- 3.19.1.1 Explosive enterprise AI adoption and proven return on investment

- 3.19.1.2 Massive cloud infrastructure expansion and investment

- 3.19.1.3 Edge computing growth and real-time processing demands

- 3.19.1.4 High-performance computing requirements for AI workloads

- 3.19.2 Industry pitfalls & challenges

- 3.19.2.1 Astronomical infrastructure costs and power consumption

- 3.19.2.2 Critical skills shortage and technical complexity

- 3.19.3 Regulatory compliance and data sovereignty requirements

- 3.19.1 Growth drivers

- 3.20 Growth potential analysis

- 3.21 Porter's analysis

- 3.22 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Server, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 AI data

- 5.3 AI training

- 5.4 AI inference

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Hardware, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 ASIC

- 6.3 FPGA

- 6.4 GPU

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Cooling Technology, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Air-cooled

- 7.2.1 Passive air cooling

- 7.2.2 Active air cooling

- 7.2.3 Precision air conditioning

- 7.2.4 Containment solutions

- 7.3 Liquid-cooled

- 7.3.1 Direct-to-chip

- 7.3.2 Immersion cooling

- 7.3.3 Single-phase

- 7.3.4 Two-phase

- 7.4 Hybrid cooling systems

Chapter 8 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 On-premises

- 8.3 Cloud-based

- 8.4 Hybrid

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 IT & telecommunications

- 9.3 Transportation and automotive

- 9.4 BFSI

- 9.5 Retail and e-commerce

- 9.6 Healthcare and Pharmaceutical

- 9.7 Industrial Automation

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Cloud Service Provider (CSP)

- 10.4 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 North America

- 11.1.1 US

- 11.1.2 Canada

- 11.2 Europe

- 11.2.1 UK

- 11.2.2 Germany

- 11.2.3 France

- 11.2.4 Italy

- 11.2.5 Spain

- 11.2.6 Belgium

- 11.2.7 Netherlands

- 11.2.8 Sweden

- 11.3 Asia Pacific

- 11.3.1 China

- 11.3.2 India

- 11.3.3 Japan

- 11.3.4 Australia

- 11.3.5 Singapore

- 11.3.6 South Korea

- 11.3.7 Vietnam

- 11.3.8 Indonesia

- 11.4 Latin America

- 11.4.1 Brazil

- 11.4.2 Mexico

- 11.4.3 Argentina

- 11.5 MEA

- 11.5.1 South Africa

- 11.5.2 Saudi Arabia

- 11.5.3 UAE

Chapter 12 Company Profiles

- 12.1 Global players

- 12.1.1 Advanced Micro Devices

- 12.1.2 Intel

- 12.1.3 NVIDIA

- 12.1.4 Cisco Systems

- 12.2 Server system manufacturers

- 12.2.1 Dell

- 12.2.2 Hewlett Packard Enterprise

- 12.2.3 Huawei

- 12.2.4 Inspur

- 12.2.5 International Business Machines

- 12.2.6 Lenovo

- 12.2.7 Super Micro Computer

- 12.3 Hyperscale and cloud providers

- 12.3.1 Amazon Web Services

- 12.3.2 Google

- 12.3.3 Microsoft

- 12.3.4 Oracle

- 12.4 Emerging and regional players

- 12.4.1 Foxconn (Hon Hai)

- 12.4.2 Fujitsu

- 12.4.3 Inventec

- 12.4.4 Quanta Computer

- 12.4.5 Wistron

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 320 Pages

- 納期

- 2~3営業日