パワースポーツアフターマーケット市場規模:車両別、推進別、用途別、販売チャネル別、コンポーネント別、2025年~2034年の成長予測

Powersports Aftermarket Size - By Vehicle, By Propulsion, By Application, By Sales Channel, By Component, Growth Forecast, 2025 - 2034

- 発行日

- ページ情報

- 英文 350 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801925

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

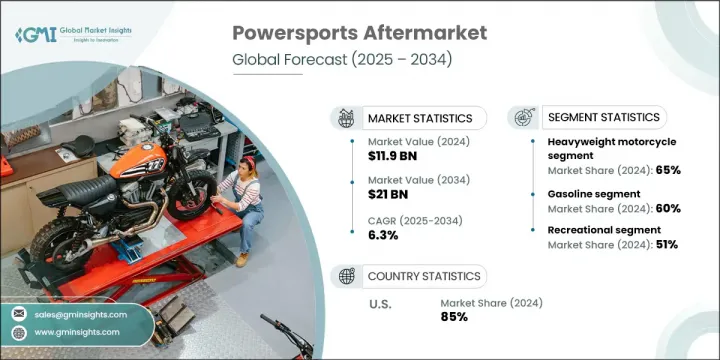

世界のパワースポーツアフターマーケットの2024年の市場規模は119億米ドルで、CAGR6.3%で成長し、2034年には210億米ドルに達すると推定されています。

この上昇動向は、アウトドアやレクリエーション活動への関心の高まりに加え、車両性能技術の進化や電気およびハイブリッドエンジン搭載モデルの存在感の高まりによって形成されています。冒険的なライフスタイルを取り入れる消費者が増えるにつれて、アフターマーケットの部品、アクセサリー、性能アップグレードの需要も増加の一途をたどっています。近年では、デジタル・プラットフォームが業界情勢の再構築に貢献しており、より多くのライダーがアップグレード、改造、修理キットをオンラインで購入しています。消費者行動の変化もeコマースの成長を後押ししており、特に自宅にいながらにしてカスタマイズされたソリューションを求めるユーザーが増えています。アウトドア体験にまつわるポスト・パンデミックの機運は、パワースポーツ車の普及に大きく貢献し、全体的な需要に拍車をかけています。市場各社は、顧客の利便性と満足度を高めるために、製品ラインナップの拡充やシームレスなデジタルサービスによって対応しています。

2024年には、重量級モーターサイクルのカテゴリーが65%のシェアを占め、2034年までCAGR 7%で成長すると予測されます。これらのモーターサイクルは通常750cc以上で、カスタマイズ、耐久ツーリング、長期的な所有価値を優先するライダーに支持されています。その堅牢な設計とツーリング性能により、アップグレードされたサスペンション、ラゲッジシステム、パフォーマンスエキゾースト、ライティング強化などのアフターマーケットパーツへの投資が増加することが多いです。このセグメントのライダーは、一般的に性能と個性化に熱心であるため、重量級バイクを取り巻くアフターマーケットのエコシステムは特に強力なままです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 119億米ドル |

| 予測金額 | 210億米ドル |

| CAGR | 6.3% |

2024年のガソリン車のシェアは60%で、2034年までのCAGRは7%の成長が見込まれます。ガソリンは、広く入手可能で、トルク出力が高く、航続距離も長いため、オフロードや遠隔地での使用に理想的な燃料として選ばれ続けています。このセグメントには、ATV、モーターサイクル、ユーティリティ・テレイン・ビークル、その他のパフォーマンス・マシンが含まれ、これらはしばしば大きな摩耗や損傷を経験するため、交換部品やアップグレード・キットに対する需要が持続しています。ガソリンエンジンの弾力性と信頼性により、ユーザーは改良と長期メンテナンスへの投資を続けています。

米国パワースポーツアフターマーケットのシェアは85%で、2024年には47億2,000万米ドルに達します。米国のパワースポーツアフターマーケットは、消費者の強い支持、確立された所有パターン、深く根付いたオフロード文化によって繁栄しています。小売チャネル、ディーラー、サービスセンターの強固なネットワークがアフターマーケット製品へのアクセスを容易にし、eコマースの普及が消費者への直接販売を支えています。BRP、ポラリス、ヤマハ、ホンダのような有名ブランドの存在と、RevZillaやRocky Mountain ATV/MCのようなデジタル先進プラットフォームが相まって、米国市場の地位と消費者の嗜好の変化への対応力を強化し続けています。

世界のパワースポーツアフターマーケットの主要企業には、バンス・アンド・ハインズ(VANCE &HINES)、BRP、K&Nエンジニアリング、ポラリス(Polaris)、アークティック・キャット(Arctic Cat)、デイコ・インコーポレイテッド(Dayco Incorporated)、S&Sサイクル(S&S Cycle)などがあります。パワースポーツアフターマーケットを展開する企業は、デジタルトランスフォーメーションに重点を置き、eコマースのリーチを拡大し、パーソナライズされた購買体験を提供しています。製品の多様化も中核戦略のひとつで、各ブランドは特定の車種やライダーの好みに合わせた革新的なパーツやアクセサリーを発表しています。OEMとの戦略的提携は、ブランドの認知度を高め、流通網を拡大するのに役立ちます。研究開発への投資は、製品の耐久性、性能、進化する排ガス規制への準拠の向上を目標としています。多くの企業がデータ分析とCRMプラットフォームを活用して、顧客の行動を理解し、ターゲットを絞ったマーケティングを展開しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 世界のアウトドアレクリエーションとアドベンチャーツーリズムの増加

- 若者のATV、UTV、スノーモービル、オートバイ所有が急増

- 車両カスタマイズの需要増加

- 北米と欧州における個人の可処分所得の増加

- 業界の潜在的リスク&課題

- 激しい価格競合を伴う細分化された市場

- 地域をまたぐ多様かつ複雑な規制遵守

- 市場機会

- 電動パワースポーツ車両アフターマーケットの拡大

- オンラインおよびモバイルカスタマイズサービスの成長

- 新興市場におけるパワースポーツの普及拡大

- スマート接続アクセサリの統合

- 促進要因

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許分析

- 流通チャネルの進化とオムニチャネル戦略

- 従来のディーラーネットワークの変革

- 独立系小売業者と専門店の動向

- オンラインマーケットプレースの統合と消費者直販モデル

- 倉庫と配送センターの最適化

- 消費者行動と購買パターン分析

- DIY vs.プロによる設置の好み

- ブランドロイヤルティとOEMとアフターマーケットの好み

- 季節的な購入パターンと在庫サイクル

- 価格感度と価値認識分析

- 価格戦略の進化と価値提案分析

- デジタル変革とeコマースの統合

- オンライン販売プラットフォームの開発と市場浸透

- デジタルカタログと製品構成システム

- モバイルコマースとアプリベースの注文ソリューション

- 拡張現実とバーチャルフィッティング技術

- 製品イノベーションとパフォーマンス向上の動向

- パフォーマンス向上技術と市場導入

- スマートテクノロジーの統合と接続アクセサリ

- 軽量素材と高度な製造技術

- カスタマイズとパーソナライゼーション技術の動向

- 価格動向

- 地域別

- 車両別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- サイドバイサイド車両

- 全地形対応車

- ヘビーウェイトバイク

- 水上バイク

- スノーモービル

第6章 市場推計・予測:推進別、2021年~2034年

- 主要動向

- ガソリン

- ディーゼル

- 電気

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- レクリエーション

- ユーティリティ

- 商業

- スポーツ

- 建設

- 防衛

第8章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- オンライン

- オフライン

第9章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- サスペンション&ブレーキパーツ

- 排気システム

- タイヤとホイール

- ボディパーツとフレーム

- バッテリーと電気製品

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- フィリピン

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 世界企業

- Akrapovic d.o.o.

- BRP

- Continental

- Fox Factory

- Honda Powersports

- Kawasaki Motors

- Magura GmbH

- Polaris

- Suzuki Motor

- Yamaha Motor

- 地域企業

- Acerbis S.p.A

- All Balls Racing

- Kimpex

- Mitas Tires

- Motovan

- Polisport Group

- ProX Racing Parts

- SBS Friction A/S

- TM Designworks

- Twin Air

- 新興企業

- Baja Designs

- Cycra Performance Plastics

- FMF Racing

- IMS Products

- Racetech Products

- Renegade Powersports

- Scorpion Exhausts

- Tusk Racing

- Vortex Racing

- ZETA USA

目次

The Global Powersports Aftermarket was valued at USD 11.9 billion in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 21 billion by 2034. This upward trend is shaped by rising interest in outdoor and recreational activities, alongside the evolution of vehicle performance technologies and the increasing presence of electric and hybrid-powered models. As more consumers embrace adventure lifestyles, the demand for aftermarket parts, accessories, and performance upgrades continues to rise. In recent years, digital platforms have helped reshape the industry landscape, with more riders purchasing upgrades, modifications, and repair kits online. Shifts in consumer behavior are also driving e-commerce growth, especially among users looking for customized solutions from the comfort of home. The post-pandemic momentum around outdoor experiences contributed significantly to the adoption of powersport vehicles, fueling demand across the board. Market players are adapting with expanded product offerings and seamless digital services that elevate customer convenience and satisfaction.

In 2024, the heavyweight motorcycle category held a 65% share and is projected to grow at a CAGR of 7% through 2034. These motorcycles-typically over 750cc-are favored by riders who prioritize customization, endurance touring, and long-term ownership value. Their robust design and touring capabilities often drive higher investment in aftermarket parts such as upgraded suspensions, luggage systems, performance exhausts, and lighting enhancements. Because riders of this segment are typically more enthusiastic about performance and personalization, the aftermarket ecosystem surrounding heavyweight bikes remains particularly strong.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.9 Billion |

| Forecast Value | $21 Billion |

| CAGR | 6.3% |

Gasoline-powered vehicles held 60% share in 2024, with growth anticipated at 7% CAGR through 2034. Gasoline continues to be the fuel of choice due to its widespread availability, high torque output, and extended range-factors that make these vehicles ideal for off-road and remote usage. This segment includes ATVs, motorcycles, utility terrain vehicles, and other performance machines, which often experience significant wear and tear, resulting in sustained demand for replacement components and upgrade kits. The resilience and reliability of gasoline engines ensure that users continue to invest in enhancements and long-term maintenance.

United States Powersports Aftermarket held 85% share and generated USD 4.72 billion in 2024. The US powersports aftermarket thrives on strong consumer adoption, established ownership patterns, and a deeply rooted off-road culture. Its robust network of retail channels, dealerships, and service centers makes aftermarket products easily accessible, while widespread adoption of e-commerce supports direct-to-consumer sales. The presence of notable brands like BRP, Polaris, Yamaha, and Honda, combined with digital-forward platforms such as RevZilla and Rocky Mountain ATV/MC, continues to strengthen the US market's position and responsiveness to shifting consumer preferences.

Leading companies in the Global Powersports Aftermarket include VANCE & HINES, BRP, K&N Engineering, Polaris, Arctic Cat, Dayco Incorporated, and S&S Cycle. Companies operating in the powersports aftermarket are focusing heavily on digital transformation, expanding their e-commerce reach, and offering personalized buying experiences. Product diversification is another core strategy, with brands introducing innovative parts and accessories tailored to specific vehicle types and rider preferences. Strategic collaborations with OEMs help boost brand visibility and expand distribution networks. Investments in R&D are targeted at improving product durability, performance, and compliance with evolving emission standards. Many players are leveraging data analytics and CRM platforms to understand customer behavior and deliver targeted marketing.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Application

- 2.2.5 Sales channel

- 2.2.6 Component

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in global outdoor recreation and adventure tourism

- 3.2.1.2 Surge in ATV, UTV, snowmobile, and motorcycle ownership among youth

- 3.2.1.3 Increase in demand for vehicle customization

- 3.2.1.4 Rising disposable income of individuals in North America and Europe

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fragmented market with intense price competition

- 3.2.2.2 Diverse and complex regulatory compliance across regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of electric powersports vehicles aftermarket

- 3.2.3.2 Growth in online and mobile customization services

- 3.2.3.3 Rising powersports adoption in emerging markets

- 3.2.3.4 Integration of smart connected accessories

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Distribution channel evolution and omnichannel strategies

- 3.8.1 Traditional dealer network transformation

- 3.8.2 Independent retailer and specialty shop dynamics

- 3.8.3 Online marketplace integration and direct-to-consumer models

- 3.8.4 Warehouse and distribution center optimization

- 3.9 Consumer behavior and purchase pattern analysis

- 3.9.1 DIY vs. Professional installation preferences

- 3.9.2 Brand loyalty and OEM vs. Aftermarket preferences

- 3.9.3 Seasonal purchase patterns and inventory cycles

- 3.9.4 Price sensitivity and value perception analysis

- 3.10 Pricing strategy evolution and value proposition analysis

- 3.11 Digital transformation and e-commerce integration

- 3.11.1 Online sales platform development and market penetration

- 3.11.2 Digital catalog and product configuration systems

- 3.11.3 Mobile commerce and app-based ordering solutions

- 3.11.4 Augmented reality and virtual fitting technologies

- 3.12 Product innovation and performance enhancement trends

- 3.12.1 Performance upgrade technologies and market adoption

- 3.12.2 Smart technology integration and connected accessories

- 3.12.3 Lightweight materials and advanced manufacturing

- 3.12.4 Customization and personalization technology trends

- 3.13 Price trends

- 3.13.1 By region

- 3.13.2 By Vehicle

- 3.14 Production statistics

- 3.14.1 Production hubs

- 3.14.2 Consumption hubs

- 3.14.3 Export and import

- 3.15 Cost breakdown analysis

- 3.16 Sustainability and environmental aspects

- 3.16.1 Sustainable practices

- 3.16.2 Waste reduction strategies

- 3.16.3 Energy efficiency in production

- 3.16.4 Eco-friendly Initiatives

- 3.16.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.1.1 Side by side vehicle

- 5.1.2 All-terrain vehicle

- 5.1.3 Heavyweight motorcycle

- 5.1.4 Personal watercrafts

- 5.1.5 Snowmobile

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 Electric

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Recreational

- 7.3 Utility

- 7.4 Commercial

- 7.5 Sports

- 7.6 Construction

- 7.7 Defense

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Online

- 8.3 Offline

Chapter 9 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Suspension & Brake Parts

- 9.3 Exhaust Systems

- 9.4 Tires & Wheels

- 9.5 Body Parts & Frames

- 9.6 Batteries & Electricals

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Akrapovic d.o.o.

- 11.1.2 BRP

- 11.1.3 Continental

- 11.1.4 Fox Factory

- 11.1.5 Honda Powersports

- 11.1.6 Kawasaki Motors

- 11.1.7 Magura GmbH

- 11.1.8 Polaris

- 11.1.9 Suzuki Motor

- 11.1.10 Yamaha Motor

- 11.2 Regional Players

- 11.2.1 Acerbis S.p.A

- 11.2.2 All Balls Racing

- 11.2.3 Kimpex

- 11.2.4 Mitas Tires

- 11.2.5 Motovan

- 11.2.6 Polisport Group

- 11.2.7 ProX Racing Parts

- 11.2.8 SBS Friction A/S

- 11.2.9 TM Designworks

- 11.2.10 Twin Air

- 11.3 Emerging Players

- 11.3.1 Baja Designs

- 11.3.2 Cycra Performance Plastics

- 11.3.3 FMF Racing

- 11.3.4 IMS Products

- 11.3.5 Racetech Products

- 11.3.6 Renegade Powersports

- 11.3.7 Scorpion Exhausts

- 11.3.8 Tusk Racing

- 11.3.9 Vortex Racing

- 11.3.10 ZETA USA

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 350 Pages

- 納期

- 2~3営業日