ハイパースケールデータセンター市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Hyperscale Data Center Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 310 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801918

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

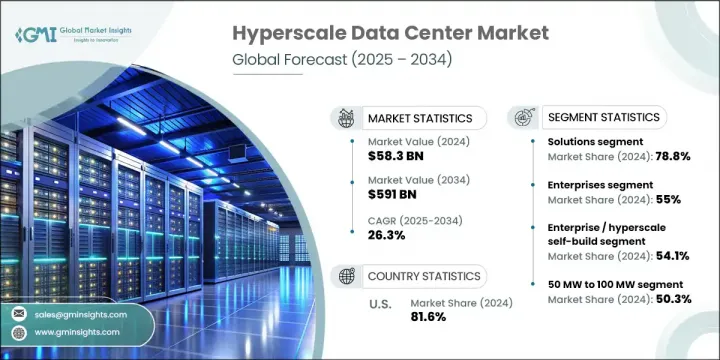

ハイパースケールデータセンターの世界市場規模は2024年に583億米ドルとなり、CAGR 26.3%で成長し、2034年には5,910億米ドルに達すると予測されています。

この拡大は、デジタルサービス、クラウドコンピューティング、人工知能(AI)、ビッグデータ分析に対する需要の急増によってもたらされます。大規模なスケーラビリティ、エネルギー効率、高性能コンピューティングのために設計されたハイパースケールデータセンターは、テクノロジープロバイダー、企業、政府機関にとって不可欠なものとなっています。ソーシャルメディア、IoTデバイス、企業アプリケーションなど、さまざまなソースからのデータ消費が増大するにつれ、こうした高度なデータセンターの必要性は世界各地で高まっています。

COVID-19の大流行は、市場の成長を加速させる上で極めて重要な役割を果たしました。2020年には当初、建設と設備供給に混乱が生じたが、2021年にはリモートワーク、eラーニング、オンラインサービスへの世界のシフトにより需要が急増しました。このため、ハイパースケールプロバイダーは、ネットワーク、エッジコンピューティング、ハイブリッドクラウドインフラの拡大に向けた投資を強化しました。さらに、労働力の課題の中で業務を維持するために、自動化やリモート管理ツールが採用されました。その結果、AIを活用したデータ管理プラットフォーム、エッジコロケーション、ワークロードオーケストレーションなどのサービスが、市場の差別化にとってますます重要になっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 583億米ドル |

| 予測金額 | 5,910億米ドル |

| CAGR | 26.3% |

2024年には、ソリューション分野のシェアが78.8%を占め、2034年までの成長率は27.1%と予測されます。この分野は、ハイパースケール環境に不可欠なサーバー、ストレージ、ネットワークハードウェア、電源・冷却ソリューションなど、スケーラブルで高性能なITインフラに対する需要の高まりにより、市場をリードしています。クラウドコンピューティング、AI、ビッグデータ分析、ストリーミングの分野が活況を呈していることから、より堅牢でエネルギー効率の高いシステムへのニーズが高まっており、企業はこれに投資しています。

企業向けセグメントは2024年に55%と最大のシェアを占め、2025年から2034年にかけてCAGR 24.8%で成長すると予測されています。この優位性は、ミッションクリティカルなワークロードのサポート、規制遵守、データ管理に不可欠なプライベートクラウドやハイブリッドクラウドインフラの採用が拡大していることを反映しています。銀行、ヘルスケア、通信、製造などの分野の企業は、ITフレームワークを近代化し、俊敏性を高め、サイバーセキュリティを強化するためにハイパースケールシステムを導入しています。

米国のハイパースケールデータセンター市場は2024年に81.6%のシェアを占め、175億米ドルを創出。同国の優位性は、強力なクラウド・コンピューティング・エコシステム、広範なデジタル・インフラ、大手テクノロジー企業による多額の投資による。米国は、ハイパースケールデータオペレーションの主要拠点であると同時に、クラウド導入と企業のデジタル変革の主要市場でもあります。

ハイパースケールデータセンター世界市場の主要企業には、マイクロソフト、IBM、アマゾンウェブサービス、ファーウェイ・テクノロジーズ、アルファベット、ブロードコム、エクイニクスなどがあります。ハイパースケールデータセンター分野の企業は、市場での存在感を高めるため、世界展開の拡大、革新的技術への投資、サービス内容の多様化に注力しています。クラウド・サービス・プロバイダーは、業務効率の向上と間接コストの削減のため、自動化とAI主導のデータ管理ソリューションを優先しています。また、データ処理速度の向上と顧客の待ち時間短縮のため、エッジコンピューティングにも多額の投資を行っています。さらに、柔軟性と拡張性に対する顧客の要求に応えるため、業界プレーヤーとの協業やハイブリッドクラウドアーキテクチャの導入が標準的な戦略となりつつあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 研究開発投資と製品イノベーションへの重点化

- 電動スポーツ車両の導入

- レクリエーション活動への傾向の高まり

- オフロードイベントの増加

- 業界の潜在的リスク&課題

- パワースポーツ車両の初期コストが高め

- 安全性と環境への影響に対する懸念の高まり

- 市場機会

- 電動スポーツカーセグメントの拡大

- 成長するアドベンチャーツーリズムとエコツーリズム

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- スキルギャップ分析と人材開発

- 現在のデータセンターのスキル不足の評価

- 将来の労働力要件

- スキルアップと再教育の取り組み

- 企業研修と個人認定

- 学術機関との提携

- 政府の研修プログラム

- データセンター管理におけるキャリアパス開発

- 価格分析とコストモデル

- インフラコスト構造分析

- ベンダーの価格戦略

- サブスクリプションモデルと消費ベースモデル

- コロケーション料金パッケージ

- 電力使用コストの内訳

- ハイパースケール投資のROI評価

- 地域間のコスト比較

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

- ユースケース

- 最良のシナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソリューション

- 冷却

- 電力

- ITラックとエンクロージャ

- LV/MV分布

- ネットワーク機器

- DCIM

- サービス

- インストールと展開

- メンテナンスとサポート

- 監視サービス

第6章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- クラウドプロバイダー

- コロケーションプロバイダー

- 企業

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- BFSI

- 小売・eコマース

- 政府

- ITおよび通信

- エンターテインメントとメディア

- その他

第8章 市場推計・予測:電力容量別、2021年~2034年

- 主要動向

- 20MW~50MW

- 50MW~100MW

第9章 市場推計・予測:データセンター別、2021年~2034年

- 主要動向

- エンタープライズ/ハイパースケールセルフビルド

- ハイパースケールコロケーション

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 世界プレーヤー

- ABB

- Alibaba Cloud

- Alphabet

- Amazon Web Services

- Broadcom

- Cisco Systems

- Dell

- Digital Realty Trust

- Equinix

- HPE

- Huawei

- IBM

- Inspur

- Intel

- Lenovo

- Marvell Technology

- Microsoft

- NVIDIA

- Oracle

- Schneider Electric

- Vertiv

- Western Digital

- 地域プレーヤー

- Colt

- Corning

- Fujitsu

- Nlyte Software

- Quanta Computer

- Sify Technologies

- Telefonaktiebolaget LM Ericsson

- Tencent

目次

The Global Hyperscale Data Center Market was valued at USD 58.3 billion in 2024 and is estimated to grow at a CAGR of 26.3% to reach USD 591 billion by 2034. This expansion is driven by the surge in demand for digital services, cloud computing, artificial intelligence (AI), and big data analytics. Hyperscale data centers, designed for massive scalability, energy efficiency, and high-performance computing, are becoming critical for technology providers, corporations, and government agencies alike. As data consumption grows from various sources like social media, IoT devices, and enterprise applications, the need for these advanced data centers intensifies across global regions.

The COVID-19 pandemic played a pivotal role in accelerating market growth. While there were initial disruptions in construction and equipment supply in 2020, demand soared in 2021 due to the global shift towards remote work, e-learning, and online services. This led hyperscale providers to ramp up investments in expanding their networks, edge computing, and hybrid cloud infrastructures. Additionally, automation and remote management tools were adopted to maintain operations amid workforce challenges. As a result, services like AI-powered data management platforms, edge colocation, and workload orchestration have become increasingly crucial for market differentiation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $58.3 Billion |

| Forecast Value | $591 Billion |

| CAGR | 26.3% |

In 2024, the solutions segment accounted for 78.8% share, with a growth rate of 27.1% expected through 2034. This segment leads the market due to the increasing demand for scalable, high-performance IT infrastructure, such as servers, storage, networking hardware, and power and cooling solutions, which are essential for hyperscale environments. The booming sectors of cloud computing, AI, big data analytics, and streaming are driving the need for more robust, energy-efficient systems that enterprises are investing in.

The enterprise segment held the largest share, with 55% in 2024, and is forecasted to grow at a CAGR of 24.8% from 2025 to 2034. This dominance reflects the growing adoption of private and hybrid cloud infrastructure, essential for supporting mission-critical workloads, regulatory compliance, and data control. Enterprises in sectors such as banking, healthcare, telecom, and manufacturing are deploying hyperscale systems to modernize their IT frameworks, boost agility, and fortify cybersecurity.

U.S. Hyperscale Data Center Market held 81.6% share in 2024, generating USD 17.5 billion. The country's dominance is driven by a strong cloud computing ecosystem, extensive digital infrastructure, and substantial investments from major technology companies. The U.S. remains both a primary hub for hyperscale data operations and a key market for cloud adoption and enterprise digital transformation.

Leading companies in the Global Hyperscale Data Center Market include Microsoft, IBM, Amazon Web Services, Huawei Technologies, Alphabet, Broadcom, and Equinix. To strengthen their market presence, companies in the hyperscale data center sector are focusing on expanding their global footprints, investing in innovative technologies, and diversifying their service offerings. Cloud service providers are prioritizing automation and AI-driven data management solutions to enhance operational efficiency and reduce overhead costs. They are also investing heavily in edge computing to improve data processing speeds and reduce latency for customers. Additionally, collaboration with industry players and the implementation of hybrid cloud architectures are becoming standard strategies to meet customer demands for flexibility and scalability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 End use

- 2.2.4 Application

- 2.2.5 Power Capacity

- 2.2.6 Data Center

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing focus on R&D investments and product innovation

- 3.2.1.2 Introduction of electric power sport vehicles

- 3.2.1.3 Growing inclination towards recreational activities

- 3.2.1.4 Rising number of off-roading events

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost of power sports vehicles

- 3.2.2.2 Increasing safety and environmental impact concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of electric power sports vehicle segment

- 3.2.3.2 Growing adventure tourism and eco-tourism

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Skills gap analysis and workforce development

- 3.8.1 Current data center skills shortage assessment

- 3.8.2 Future workforce requirements

- 3.8.3 Reskilling and upskilling initiatives

- 3.8.4 Corporate training vs individual certification

- 3.8.5 Academic institution partnerships

- 3.8.6 Government training programs

- 3.8.7 Career path development in data center management

- 3.9 Pricing analysis and cost models

- 3.9.1 Infrastructure cost structure analysis

- 3.9.2 Vendor pricing strategies

- 3.9.3 Subscription vs consumption-based models

- 3.9.4 Colocation pricing packages

- 3.9.5 Power usage cost breakdown

- 3.9.6 ROI assessment for hyperscale investment

- 3.9.7 Cost comparison across regions

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use cases

- 3.13 Best-case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Cooling

- 5.2.2 Power

- 5.2.3 IT racks & enclosures

- 5.2.4 LV/MV distribution

- 5.2.5 Networking equipment

- 5.2.6 DCIM

- 5.3 Service

- 5.3.1 Installation & deployment

- 5.3.2 Maintenance & support

- 5.3.3 Monitoring services

Chapter 6 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cloud providers

- 6.3 Colocation providers

- 6.4 Enterprises

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 BFSI

- 7.3 Retail & e-commerce

- 7.4 Government

- 7.5 IT & telecom

- 7.6 Entertainment & media

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Power Capacity, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 20 MW To 50 MW

- 8.3 50 MW To 100 MW

Chapter 9 Market Estimates & Forecast, By Data Center, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Enterprise / Hyperscale Self-Build

- 9.3 Hyperscale Colocation

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 ABB

- 11.1.2 Alibaba Cloud

- 11.1.3 Alphabet

- 11.1.4 Amazon Web Services

- 11.1.5 Broadcom

- 11.1.6 Cisco Systems

- 11.1.7 Dell

- 11.1.8 Digital Realty Trust

- 11.1.9 Equinix

- 11.1.10 HPE

- 11.1.11 Huawei

- 11.1.12 IBM

- 11.1.13 Inspur

- 11.1.14 Intel

- 11.1.15 Lenovo

- 11.1.16 Marvell Technology

- 11.1.17 Microsoft

- 11.1.18 NVIDIA

- 11.1.19 Oracle

- 11.1.20 Schneider Electric

- 11.1.21 Vertiv

- 11.1.22 Western Digital

- 11.2 Regional Players

- 11.2.1 Colt

- 11.2.2 Corning

- 11.2.3 Fujitsu

- 11.2.4 Nlyte Software

- 11.2.5 Quanta Computer

- 11.2.6 Sify Technologies

- 11.2.7 Telefonaktiebolaget LM Ericsson

- 11.2.8 Tencent

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 310 Pages

- 納期

- 2~3営業日