|

市場調査レポート

商品コード

1801905

コンクリート舗装機器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Concrete Paving Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| コンクリート舗装機器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年08月11日

発行: Global Market Insights Inc.

ページ情報: 英文 300 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

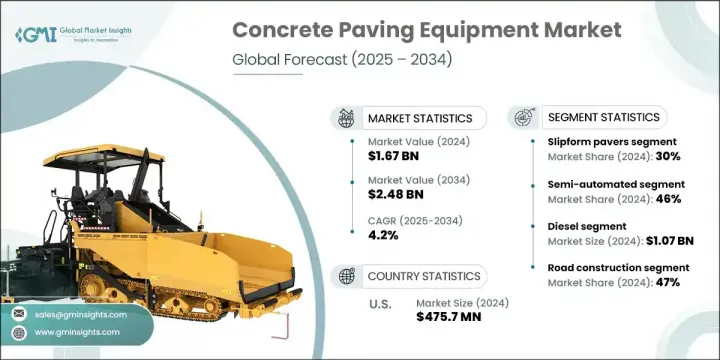

コンクリート舗装機器の世界市場規模は、2024年に16億7,000万米ドルとなり、CAGR 4.2%で成長し、2034年には24億8,000万米ドルに達すると予測されています。

この右肩上がりの成長は、世界のインフラ開発、特に道路、高速道路、橋、空港の建設に継続的な勢いがあることに起因しています。特に新興国では、混雑を緩和し経済拡大を支援するため、政府が交通機関の改善を優先しています。高精度の道路工事と長期的な耐久性が重視されるようになり、最新の舗装設備への信頼が高まっています。コンクリート舗装システムも自動化へのシフトが急速に進んでおり、メーカーはAI、GPS、テレマティクスを機械に組み込んで舗装精度と作業効率を高めています。機械学習に支えられた予知保全システムは、ダウンタイムを最小化し、現場パフォーマンスを最適化することで地歩を固めつつあります。

スリップフォーム舗装機セグメントは2024年に30%のシェアを占め、2034年までCAGR 5%で成長すると予測されています。これらの機械は、あらかじめ設置された側面型枠を必要とせずに連続的なコンクリート打設を行うため、大規模な用途に最適です。この市場は、企業が大規模なインフラ工事においてスピードと表面品質の向上を求めていることから、このような高性能機械に対する需要が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 16億7,000万米ドル |

| 予測金額 | 24億8,000万米ドル |

| CAGR | 4.2% |

2024年、半自動舗装機械セグメントは46%のシェアを獲得し、2034年まで4%の成長が見込まれます。これらの機械は、手動制御と自動ガイダンスシステムの融合を提供し、材料の分配と仕上げをより正確に行う。センサー・アシスト油圧やGPSガイド・ステアリングのような先進技術により、これらの機械はより効率的で費用対効果が高く、性能と操作の柔軟性のバランスが取れています。

米国コンクリート舗装機器市場は85%のシェアを占め、2024年には4億7,570万米ドルを生み出します。インフラ再生を支援する連邦政府の強力なプログラムが、最新の舗装システムの採用を加速し続けています。政府の主要政策は、自動マシンガイダンス(AMG)のような技術の統合を強調しています。AMGは、衛星ベースの測位を活用し、より優れた勾配制御、舗装の均一性、材料利用を実現します。同国は自動化を好み、連邦政府から一貫した資金援助を受けているため、業界の最前線に君臨し続けています。

コンクリート舗装機器の世界市場における主要企業は、Gomaco Corporation、Bid-well、Caterpillar、BESSER、Wirtgen Group、Ammann Group、SANY Groupなどです。市場での地位を強化するため、主要企業は技術革新、技術統合、世界展開に焦点を当てた戦略を組み合わせて活用しています。開発メーカーは、大規模舗装プロジェクトと小規模舗装プロジェクトの両方をサポートする、モジュール式で適応性の高い機器を積極的に開発しています。インフラ開発業者との戦略的提携は、長期契約の確保に役立っています。また、スマートセンサーやテレマティクスのような高度な自動化機能に投資し、効率を高め、労働力への依存を減らしています。機械制御システムやAIを活用したメンテナンスツールの継続的な改善により、稼働率の向上が実現しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料供給者

- 部品供給業者

- ティア1 OEM

- ディーラー/販売代理店

- アフターサービス

- 最終用途

- コスト構造

- 利益率

- 各段階での付加価値

- サプライチェーンに影響を与える要因

- 破壊者

- サプライヤーの情勢

- 影響要因

- 促進要因

- 都市化とインフラ整備の開発

- 現代の舗装機械の進歩の向上

- 道路の安全性と耐久性への重点の高まり

- 新興市場の経済拡大

- 業界の潜在的リスク&課題

- 熟練労働者の不足

- 原材料価格の変動

- 市場機会

- レンタル・リースサービス

- スマートで自律的な舗装技術

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

- 生産統計

- 生産と消費の中心地

- 輸出入分析

- 貿易フローパターン

- テクノロジーとイノベーションの情勢

- 現在の技術

- ストリングレス舗装技術の優位性

- インテリジェント制御システムの進化

- 新興技術

- 人工知能(AI)と機械学習(ML)の統合

- モノのインターネット(IoT)と接続革命

- スマート材料とコンクリートのイノベーション

- 電動化と代替パワートレイン

- デジタルツインとビルディングインフォメーションモデリング

- イノベーションエコシステムとパートナーシップ

- テクノロジーパートナーシップ戦略

- イノベーション加速メカニズム

- 現在の技術

- 特許分析

- 規制情勢

- 北米

- 規制枠組みのアーキテクチャ

- コンプライアンスコストの影響

- 欧州

- EU規制の調和

- テクノロジー統合要件

- アジア太平洋地域

- 中国の規制の進化

- 地域調和の取り組み

- ラテンアメリカ

- 中東・アフリカ

- 北米

- 価格動向

- 過去の価格推移

- 主要地域の価格動向

- 北米の価格パターン

- アジア太平洋のコスト優位性

- 欧州プレミアム市場におけるポジショニング

- 価格弾力性と感度分析

- 価格要因分析

- 将来の価格予測

- コスト内訳分析

- コストの内訳の分析

- 重要なポイント

- 将来の市場の進化

- 持続可能性主導の市場変革

- スマート建設エコシステムの進化

- パフォーマンスベースの仕様革命

- 迅速な配送の必要性

- シナリオ計画と戦略的対応

- 貿易フロー分析

- HSコード分類フレームワーク

- 主な機器の分類

- 製品および材料の分類

- 世界の貿易フローのパターン

- 建設業界の貿易概要

- コンクリート舗装機器貿易フロー

- 港湾と物流の分析

- 関税および貿易政策の分析

- 米国の貿易政策の枠組み

- 国際貿易規制

- HSコード分類フレームワーク

- 持続可能性分析

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- スリップフォーム舗装材

- ローラー舗装機

- コンクリートスプレッダー

- バッチ舗装機

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- マニュアル

- 半自動

- 完全自動化

第7章 市場推計・予測:電源別、2021年~2034年

- 主要動向

- ディーゼル

- 電気

- ハイブリッド

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 住宅建設

- 道路建設

- 商業建設

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 政府機関

- 建設会社

- レンタル会社

第10章 市場推計・予測:地域別、2021年~2034年

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベルギー

- オランダ

- スウェーデン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- シンガポール

- 韓国

- ベトナム

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 世界企業

- Caterpillar

- CMI Roadbuilding

- Dynapac

- Fayat Group

- Gomaco Corporation

- JCB

- Komatsu

- Liebherr

- SANY Group

- Terex Corporation(Bid-Well)

- Volvo CE

- Wirtgen Group

- XCMG Group

- 地域企業

- BESSER

- Guntert &Zimmerman

- HEM Paving Equipment

- Power Curbers Companies

- SCHWING Stetter

- 新興企業

- Aimix Group

- Curb Fox

The Global Concrete Paving Equipment Market was valued at USD 1.67 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 2.48 billion by 2034. This steady rise is attributed to ongoing momentum in global infrastructure development, particularly across the construction of roads, highways, bridges, and airports. A surge in urbanization is fueling infrastructure investments, especially in emerging economies, where governments are prioritizing transportation upgrades to reduce congestion and support economic expansion. The increased focus on high-precision roadwork and long-term durability has created greater reliance on modern paving equipment. Concrete paving systems are also seeing a rapid shift toward automation, with manufacturers integrating AI, GPS, and telematics into machines to enhance paving precision and operational efficiency. Predictive maintenance systems, supported by machine learning, are gaining ground by minimizing downtime and optimizing field performance.

The slipform pavers segment held a 30% share in 2024 and is projected to grow at a CAGR of 5% through 2034. These machines deliver continuous concrete placement without requiring pre-installed side forms, making them ideal for large-scale applications. The market is experiencing rising demand for such high-performance machinery as companies look to enhance speed and surface quality across major infrastructure jobs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.67 Billion |

| Forecast Value | $2.48 Billion |

| CAGR | 4.2% |

In 2024, the semi-automated paving machines segment captured a 46% share and is expected to grow at 4% through 2034. These machines offer a blend of manual control with automated guidance systems that ensure material is distributed and finished more accurately. Advanced technologies like sensor-assisted hydraulics and GPS-guided steering make these units more efficient and cost-effective, balancing performance with operational flexibility.

United States Concrete Paving Equipment Market held an 85% share and generated USD 475.7 million in 2024. The strong presence of federal programs supporting infrastructure revitalization continues to accelerate the adoption of modern paving systems. Key government policies are emphasizing the integration of technologies like Automatic Machine Guidance (AMG), which leverages satellite-based positioning for better grade control, paving uniformity, and material utilization. The country's preference for automation and consistent federal funding has kept it at the forefront of industry.

The leading players in the Global Concrete Paving Equipment Market include Gomaco Corporation, Bid-well, Caterpillar, BESSER, Wirtgen Group, Ammann Group, and SANY Group. To strengthen their market position, key companies are leveraging a combination of strategies that focus on innovation, technology integration, and global expansion. Manufacturers are actively developing modular and adaptable equipment that supports both large- and small-scale paving projects. Strategic collaborations with infrastructure developers are helping them secure long-term contracts. They are also investing in advanced automation features like smart sensors and telematics to increase efficiency and reduce labor dependency. Continuous improvements in machine control systems and AI-driven maintenance tools are enabling better uptime.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Data mining sources

- 1.2.1 Global

- 1.2.2 Regional/Country

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Type

- 2.2.4 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Tier 1 OEMs

- 3.1.1.4 Dealers/distributors

- 3.1.1.5 Aftermarket services

- 3.1.1.6 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing urbanization and infrastructure development

- 3.2.1.2 Raising advancements in modern paving machines

- 3.2.1.3 Increasing focus on road safety and durability

- 3.2.1.4 Economic expansion in emerging markets

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Skilled Labor Shortage

- 3.2.2.2 Volatility in Raw Material Prices

- 3.2.3 Market opportunities

- 3.2.3.1 Rental & leasing services

- 3.2.3.2 Smart & autonomous paving technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Production statistics

- 3.6.1 Production and consumption hubs

- 3.6.2 Export and import analysis

- 3.6.3 Trade flow patterns

- 3.7 Technology & innovation landscape

- 3.7.1 Current technologies

- 3.7.1.1 Stringless paving technology dominance

- 3.7.1.2 Intelligent control systems evolution

- 3.7.2 Emerging technologies

- 3.7.2.1 Artificial intelligence (AI) and machine learning (ML) integration

- 3.7.2.2 Internet of Things (IoT) and connectivity revolution

- 3.7.2.3 Smart materials and concrete innovation

- 3.7.2.4 Electrification and alternative powertrains

- 3.7.2.5 Digital twin and building information modeling

- 3.7.3 Innovation ecosystem and partnerships

- 3.7.3.1 Technology partnership strategy

- 3.7.3.2 Innovation acceleration mechanisms

- 3.7.1 Current technologies

- 3.8 Patent analysis

- 3.9 Regulatory landscape

- 3.9.1 North America

- 3.9.1.1 Regulatory framework architecture

- 3.9.1.2 Compliance cost implications

- 3.9.2 Europe

- 3.9.2.1 EU Regulatory Harmonization

- 3.9.2.2 Technology integration requirements

- 3.9.3 Asia Pacific

- 3.9.3.1 China's regulatory evolution

- 3.9.3.2 Regional harmonization efforts

- 3.9.4 Latin America

- 3.9.5 Middle East & Africa

- 3.9.1 North America

- 3.10 Price trends

- 3.10.1 Historical price trajectory

- 3.10.2 Major regions price dynamics

- 3.10.2.1 North American pricing patterns

- 3.10.2.2 Asia-Pacific cost advantages

- 3.10.2.3 European premium positioning

- 3.10.3 Price elasticity and sensitivity analysis

- 3.10.4 Price driver analysis

- 3.10.5 Future price projection

- 3.11 Cost breakdown analysis

- 3.11.1 Analysis of the cost breakdown

- 3.11.2 Key takeaways

- 3.12 Future market evolution

- 3.12.1 Sustainability-driven market transformation

- 3.12.2 Smart construction ecosystem evolution

- 3.12.3 Performance-based specification revolution

- 3.12.4 Accelerated delivery imperatives

- 3.12.5 Scenario planning and strategic responses

- 3.13 Trade flow analysis

- 3.13.1 HS code classification framework

- 3.13.1.1 Primary equipment classifications

- 3.13.1.2 Product and material classifications

- 3.13.2 Global trade flow patterns.

- 3.13.2.1 Construction industry trade overview

- 3.13.2.2 Concrete paving equipment trade flows

- 3.13.2.3 Port and logistics analysis

- 3.13.3 Tariff and trade policy analysis.

- 3.13.3.1 U.S. trade policy framework.

- 3.13.3.2 International trade regulations

- 3.13.1 HS code classification framework

- 3.14 Sustainability analysis

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly initiatives

- 3.14.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Slipform pavers

- 5.3 Roller pavers

- 5.4 Concrete spreaders

- 5.5 Batch pavers

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-automated

- 6.4 Fully automated

Chapter 7 Market Estimates & Forecast, By Power Source, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Diesel

- 7.3 Electric

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Residential construction

- 8.3 Road construction

- 8.4 Commercial construction

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Government agencies

- 9.3 Construction companies

- 9.4 Rental companies

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 North America

- 10.1.1 U.S.

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Belgium

- 10.2.7 Netherlands

- 10.2.8 Sweden

- 10.2.9 Russia

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 Singapore

- 10.3.6 South Korea

- 10.3.7 Vietnam

- 10.3.8 Indonesia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Caterpillar

- 11.1.2 CMI Roadbuilding

- 11.1.3 Dynapac

- 11.1.4 Fayat Group

- 11.1.5 Gomaco Corporation

- 11.1.6 JCB

- 11.1.7 Komatsu

- 11.1.8 Liebherr

- 11.1.9 SANY Group

- 11.1.10 Terex Corporation (Bid-Well)

- 11.1.11 Volvo CE

- 11.1.12 Wirtgen Group

- 11.1.13 XCMG Group

- 11.2 Regional Players

- 11.2.1 BESSER

- 11.2.2 Guntert & Zimmerman

- 11.2.3 HEM Paving Equipment

- 11.2.4 Power Curbers Companies

- 11.2.5 SCHWING Stetter

- 11.3 Emerging Players

- 11.3.1 Aimix Group

- 11.3.2 Curb Fox