HIV診断市場の市場機会、成長促進要因、産業動向分析、2025年~2034年の予測

HIV Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 98 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801898

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

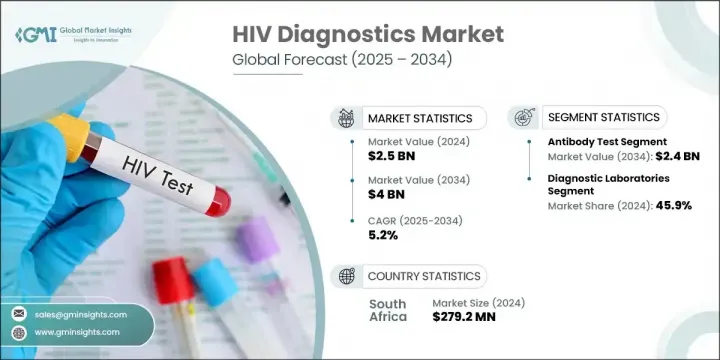

世界のHIV診断市場は、2024年には25億米ドルと評価され、CAGR 5.2%で成長し、2034年には40億米ドルに達すると推定されています。

この増加傾向は、中低所得地域におけるHIV罹患率の上昇と、より信頼性が高く利用しやすい診断方法に対する需要に支えられています。世界のキャンペーンを通じてHIV検査に対する意識が高まるにつれ、公的・私的医療システムの双方で高度な検査ソリューションの導入が進んでいます。ポイントオブケア診断法は、その迅速性、利便性、インフラの限られた地域での適合性により、勢いを増しています。

HIV感染の特定に使用される診断技術は、早期介入、患者のモニタリング、適切な治療経路の決定において中心的な役割を果たします。さまざまな世界の保健活動や資金援助イニシアティブは、利用しやすいHIV検査ソリューションへの需要を生み出し続けています。ヘルスケアへのアクセスやヘルスリテラシーが向上するにつれて、特に十分なサービスを受けていない地域社会におけるHIV検査キットの採用は増加の一途をたどっています。技術革新と、より迅速でコスト効率の高い検査ソリューションが、公衆衛生の取り組みと臨床現場の両方における普及をさらに後押ししています。政策支援、一般市民の意識の向上、迅速な診断の進歩が相まって、世界的にHIV診断の状況は変化し続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 25億米ドル |

| 予測金額 | 40億米ドル |

| CAGR | 5.2% |

抗体検査分野は、費用対効果、簡便性、迅速な結果提供能力により、2024年の市場をリードし、最大シェアを占めました。自己検査キットでの利用が拡大していることも、特に低資源環境での普及に寄与しています。これらの検査は、複雑な医療環境を必要とせず、利用しやすく、実施も簡単であるため、集団スクリーニングに理想的です。特にヘルスケアへの偏見や診療所へのアクセス制限が懸念される地域では、プライバシーを重視した自己検査法を選択する個人が増えており、その関連性は高まり続けています。

診断検査施設セグメントは2024年に45.9%のシェアを占めます。これらの施設は、大量の検査を効率的に管理するための設備が整っているため、HIV検査に望ましい選択肢であり続けています。HIV有病率の増加に伴い、正確で高スループットの検査に対するニーズは拡大しています。検査施設は、高度な機器と自動化システムを活用して信頼性の高い検査結果を提供するため、公衆衛生プログラムや大規模な検査キャンペーンを支援する上で不可欠な存在となっています。

中東・アフリカHIV診断2024年の市場シェアは30.1%。同地域における感染率の上昇が、より効果的で利用しやすい診断ツールへの需要を引き続き促進しています。HIVの蔓延を管理するためにより多くの意識と資源が向けられる中、スケーラブルで正確な検査ソリューションの必要性が引き続き市場を牽引しています。

HIV診断市場の主要企業には、Bioneer、Hologic、Genlantis Diagnostics、Qiagen、ChemBio Diagnostics、OraSure Technologies、Becton、Dickinson and Company(BD)、F. Hoffmann-La Roche、Abbott Laboratories、Biomerieux、Cepheidなどがあります。HIV診断分野の主要企業は、検査ポートフォリオの拡充、ポイントオブケアプラットフォームの強化、研究開発への投資によって市場での存在感を強めています。多くの企業が、スピード、携帯性、正確性を優先し、分散化したヘルスケア環境に対応した次世代診断キットを発売しています。

ヘルスケア機関、NGO、政府との提携は、企業が大規模な供給契約を確保するのに役立ち、地域提携による地域拡大は流通を強化します。競争力を維持するため、いくつかの企業は検査キットにデジタルツールを統合し、リアルタイムのデータ追跡や遠隔モニタリングを可能にしています。また、HIV罹患率が上昇している未開拓地域での市場参入を加速するため、規制当局の承認や認証に注力している企業もあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 低・中所得国におけるエイズ/HIV感染率の上昇

- HIV啓発のための政府の取り組みの強化

- ポイントオブケア(POC)開発

- 米国の好ましい規制状況

- 業界の潜在的リスク&課題

- 未開発市場における浸透度の低さ

- 社会的偏見と差別

- 市場機会

- 継続的な技術進歩

- デジタルヘルスプラットフォームとの統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 米国

- 欧州

- 技術的進歩

- 価格分析、2024年

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 戦略的ダッシュボード

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:検査タイプ別、2021年~2034年

- 主要動向

- 抗体検査

- ウイルス量検査

- CD4検査

第6章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 診断検査室

- 病院と診療所

- 在宅ケア

- その他

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第8章 企業プロファイル

- Abbott Laboratories

- Becton, Dickinson and Company(BD)

- Biomerieux

- Bioneer

- Cepheid

- ChemBio Diagnostics

- F. Hoffmann-La Roche

- Genlantis Diagnostics

- Hologic

- OraSure Technologies

- Qiagen

目次

The Global HIV Diagnostics Market was valued at USD 2.5 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 4 billion by 2034. This upward trend is supported by rising HIV incidence in lower- and middle-income regions, combined with the demand for more reliable and accessible diagnostic methods. As awareness surrounding HIV testing grows through global campaigns, both public and private healthcare systems are increasingly adopting advanced testing solutions. Point-of-care diagnostics are gaining momentum due to their speed, convenience, and suitability in regions with limited infrastructure.

Diagnostic technologies used to identify HIV infections play a central role in early intervention, patient monitoring, and determining suitable treatment paths. Various global health efforts and funding initiatives continue to create demand for accessible HIV testing solutions. As access to healthcare and health literacy improve, the adoption of HIV testing kits, especially in underserved communities, continues to rise. Technological innovation and faster, cost-efficient testing solutions are further supporting widespread adoption across both public health initiatives and clinical settings. The combination of policy support, increasing public awareness, and rapid diagnostic advancements continues to reshape the HIV diagnostics landscape globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Billion |

| Forecast Value | $4 Billion |

| CAGR | 5.2% |

The antibody tests segment led the market in 2024 and held the largest share due to their cost-effectiveness, simplicity, and ability to deliver quick results. Their growing use in self-testing kits has also contributed to widespread adoption, particularly in low-resource environments. These tests are ideal for mass screening as they are both accessible and easy to administer without requiring complex medical settings. Their relevance continues to grow as more individuals opt for privacy-driven self-testing methods, especially in regions where healthcare stigma or limited access to clinics is a concern.

The diagnostic laboratories segment held 45.9% share in 2024. These facilities remain the preferred choice for HIV testing because they are equipped to manage a large volume of tests efficiently. With growing HIV prevalence, the need for accurate and high-throughput testing is expanding. Laboratories utilize sophisticated instruments and automated systems to deliver reliable results, making them essential for supporting public health programs and large-scale testing campaigns.

Middle East and Africa HIV Diagnostics Market held 30.1% share in 2024. Rising infection rates in this region continue to fuel demand for more effective and accessible diagnostic tools. As more awareness and resources are directed toward managing the spread of HIV, the need for scalable and accurate testing solutions continues to drive the market forward.

Leading companies in the HIV Diagnostics Market include Bioneer, Hologic, Genlantis Diagnostics, Qiagen, ChemBio Diagnostics, OraSure Technologies, Becton, Dickinson and Company (BD), F. Hoffmann-La Roche, Abbott Laboratories, Biomerieux, and Cepheid. Major players in the HIV diagnostics sector are reinforcing their market presence by expanding testing portfolios, enhancing point-of-care platforms, and investing in R&D. Many are launching next-generation diagnostic kits that prioritize speed, portability, and accuracy, tailored for decentralized healthcare settings.

Collaborations with healthcare agencies, NGOs, and governments help companies secure large-scale supply contracts, while regional expansion through local partnerships strengthens distribution. To remain competitive, several firms are integrating digital tools with testing kits, enabling real-time data tracking and remote monitoring. Others focus on regulatory approvals and certifications to accelerate market entry in underserved regions with rising HIV incidence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Test type

- 2.2.3 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising AIDS/HIV prevalence in low and middle-income countries

- 3.2.1.2 Increasing government initiatives for HIV awareness

- 3.2.1.3 Point-of-care (POC) HIV diagnostics development

- 3.2.1.4 Favorable regulatory landscape in the U.S.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Low degree of penetration in underdeveloped market

- 3.2.2.2 Social stigma and discrimination

- 3.2.3 Market opportunities

- 3.2.3.1 Ongoing technology advancement

- 3.2.3.2 Integration with digital health platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technological advancements

- 3.6 Pricing analysis, 2024

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

- 4.7 Strategic dashboard

- 4.8 Key developments

- 4.8.1 Mergers and acquisitions

- 4.8.2 Partnerships and collaborations

- 4.8.3 New product launches

- 4.8.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Antibody test

- 5.3 Viral load test

- 5.4 CD4 test

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Diagnostic laboratories

- 6.3 Hospitals and clinics

- 6.4 Home settings

- 6.5 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott Laboratories

- 8.2 Becton, Dickinson and Company (BD)

- 8.3 Biomerieux

- 8.4 Bioneer

- 8.5 Cepheid

- 8.6 ChemBio Diagnostics

- 8.7 F. Hoffmann-La Roche

- 8.8 Genlantis Diagnostics

- 8.9 Hologic

- 8.10 OraSure Technologies

- 8.11 Qiagen

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 98 Pages

- 納期

- 2~3営業日