|

市場調査レポート

商品コード

1801892

内視鏡リプロセシングの市場機会、成長促進要因、産業動向分析、2025年~2034年の予測Endoscope Reprocessing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 内視鏡リプロセシングの市場機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年08月07日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

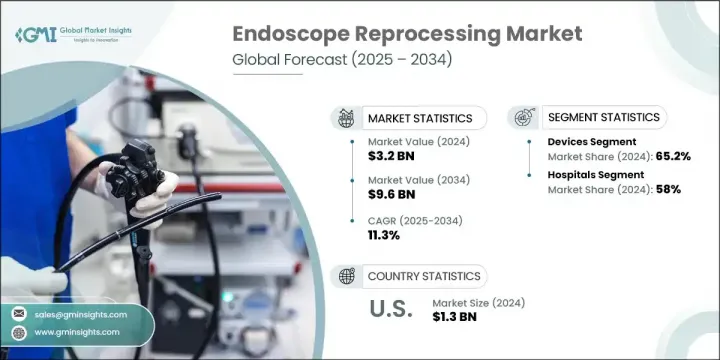

世界の内視鏡リプロセシング市場は、2024年に32億米ドルと評価され、CAGR 11.3%で成長し、2034年には96億米ドルに達すると推定されています。

この急速な市場拡大の背景には、低侵襲手術手技へのシフトが進んでいることに加え、消化器疾患やがんなど、頻繁な診断・治療が必要な内視鏡手術の有病率が上昇していることがあります。より多くの処置が外来手術センターや外来手術センターに移行するにつれて、ユーザー間の内視鏡の安全性を確保する信頼性が高く効率的な再処理システムの必要性がより重要になります。

再使用可能な内視鏡の消毒と安全性を確保することは、臨床環境における感染制御の中心です。規制機関は、内視鏡器具の洗浄と消毒のための厳格なプロトコルを施行し続けています。ヘルスケアプロバイダーが医療関連感染を軽減しなければならないという強いプレッシャーに直面する中、徹底的で有効な再処理プロトコルの重要性は著しく高まっています。さらに、抗菌剤耐性をめぐる懸念の高まりや、感染予防に対する要求の高まりは、効果的で高品質な内視鏡リプロセシングシステムの必要性をさらに高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 32億米ドル |

| 予測金額 | 96億米ドル |

| CAGR | 11.3% |

アクセサリー分野は、性能を高め、ワークフローを簡素化する装置部品の技術革新により、2034年までCAGR 10.9%の成長が見込まれます。研究開発への継続的な投資により、各企業はリプロセスの一貫性を向上させるだけでなく、しばしばばらつきや潜在的なエラーにつながる手作業への依存を減らす自動化技術を導入できるようになっています。自動化された内視鏡リプロセッサーが着実に台頭することで、規制遵守を確保しながら効率を高め、不適切な滅菌のリスクを最小限に抑えています。

2024年、病院セグメントのシェアは58%。このセグメントの優位性は主に、患者数の多さと、滅菌プロトコルの厳格な遵守による感染伝播の低減にますます焦点が当てられていることに起因しています。施設は、適切な消毒が一貫して達成されるよう、技術者のトレーニング、コンプライアンス追跡、洗浄サイクルの文書化に重点を置いています。その結果、病院はすべてのスコープの再処理履歴を監視し、ワークフローの安全性を最適化するために、高度な追跡システムを統合しています。

米国の内視鏡リプロセシングの2024年の市場規模は13億米ドル。同国の優位性は、慢性疾患に関連した処置件数の多さと、ヘルスケア施設全体の感染管理の改善に連邦政府が注力していることに起因します。ヘルスケアインフラのアップグレードと患者安全イニシアチブへの財政投資の増加が、北米全域で自動化・デジタル化されたリプロセシングソリューションの採用強化を支えています。

内視鏡リプロセシング世界市場の革新と競争を牽引する主要企業には、Olympus、Wassenburg Medical、Steelco、Getinge、Metrex、Ecolab、Belimed、ASP、Shinva Medical Instrument、Creo Medical、CONMED Corporation、Karl Storz、ARC Group of Companies、STERISなどがあります。内視鏡リプロセシング市場での地位を強化するため、主要企業は研究開発に多額の投資を行い、一貫した洗浄性能を実現し、ヒューマンエラーを低減する高度なシステムを開発しています。また、トレーサビリティの強化、ワークフローの効率化、規制遵守の徹底を図るため、自動化とデジタル統合に注力している企業も多いです。病院や手術センターとの戦略的提携は、顧客基盤の拡大や実際のニーズに合わせたソリューションの提供に役立っています。一部のプレーヤーは、スタッフトレーニング、メンテナンス、コンプライアンス追跡などの付加価値サービスを提供しています。各地域の製造施設や現地化されたサービス・サポートを通じた世界展開は、メーカーが市場浸透を高めるのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 内視鏡検査の需要増加

- 内視鏡リプロセシングにおける技術の進歩

- 低侵襲手術への関心の高まり

- 消化器疾患、がん、その他の慢性疾患の罹患率の増加

- 業界の潜在的リスク&課題

- 化学消毒剤の有害作用

- 内視鏡リプロセシングデバイスの高コスト

- 市場機会

- 感染対策への意識の高まり

- ヘルスケアインフラの成長

- 促進要因

- 成長の可能性

- 成長可能性分析

- 償還シナリオ

- 規制情勢

- 北米

- 欧州

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- 新製品開発の情勢

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- デバイス

- 自動内視鏡再処理装置(AER)

- タイプ別

- シングルドアAER

- 両開きドアAER

- ポータビリティ

- スタンドアロンAER

- ポータブルAER

- タイプ別

- 内視鏡の乾燥、保管、輸送システム

- その他のデバイス

- 自動内視鏡再処理装置(AER)

- 消耗品

- バルブとアダプター

- 高レベル消毒剤

- ベッドサイドキット

- その他の消耗品

- アクセサリー

第6章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- その他の用途

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- オーストリア

- スイス

- 中央欧州

- ポーランド

- ハンガリー

- ルーマニア

- チェコ共和国

- ブルガリア

- 中東欧のその他の地域

- 北欧諸国

- デンマーク

- スウェーデン

- ノルウェー

- その他の北欧諸国

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリアとニュージーランド

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- ARC Group of Companies

- ASP

- Belimed

- CONMED Corporation

- Creo Medical

- Ecolab

- Getinge

- Metrex

- Olympus

- Shinva Medical Instrument

- Steelco

- STERIS

- Karl Storz

- Wassenburg Medical

The Global Endoscope Reprocessing Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 11.3% to reach USD 9.6 billion by 2034. This rapid market expansion is being fueled by the increasing shift toward minimally invasive surgical techniques, coupled with the rising prevalence of conditions such as gastrointestinal diseases and cancers that require frequent diagnostic and therapeutic endoscopic procedures. As more procedures shift to outpatient and ambulatory surgical centers, the need for reliable and efficient reprocessing systems that ensure endoscope safety between users becomes more critical.

Ensuring the disinfection and safety of reusable endoscopes is central to infection control in clinical environments. Regulatory bodies continue to enforce strict protocols for cleaning and disinfecting endoscopic devices. As healthcare providers face heightened pressure to mitigate healthcare-associated infections, the importance of thorough, validated reprocessing protocols has grown considerably. Additionally, increasing concerns surrounding antimicrobial resistance and the demand for greater infection prevention continue to intensify the need for effective, high-quality endoscope reprocessing systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $9.6 Billion |

| CAGR | 11.3% |

The accessories segment is expected to grow at a CAGR of 10.9% through 2034, driven by innovation in device components that enhance performance and simplify workflows. Continued investments in R&D are allowing companies to introduce automated technologies that not only improve reprocessing consistency but also reduce reliance on manual labor, which often leads to variability and potential error. The steady rise of automated endoscope reprocessors is enhancing efficiency while ensuring regulatory compliance and minimizing the risk of improper sterilization.

In 2024, the hospitals segment held 58% share. The dominance of this segment is primarily attributed to the high volume of patients and the increasing focus on reducing infection transmission through strict adherence to sterilization protocols. Facilities are placing strong emphasis on technician training, compliance tracking, and documentation of cleaning cycles to ensure that proper disinfection is achieved consistently. As a result, hospitals are integrating advanced tracking systems to monitor the reprocessing history of every scope and optimize workflow safety.

U.S. Endoscope Reprocessing Market was valued at USD 1.3 billion in 2024. The country's dominance stems from high procedural volumes tied to chronic diseases, as well as federal focus on improving infection control across healthcare facilities. Upgrades to healthcare infrastructure and growing financial investment in patient safety initiatives are supporting stronger adoption of automated and digitalized reprocessing solutions across North America.

Key players driving innovation and competition in the Global Endoscope Reprocessing Market include Olympus, Wassenburg Medical, Steelco, Getinge, Metrex, Ecolab, Belimed, ASP, Shinva Medical Instrument, Creo Medical, CONMED Corporation, Karl Storz, ARC Group of Companies, and STERIS. To strengthen their position in the endoscope reprocessing market, leading companies are investing heavily in R&D to develop advanced systems that deliver consistent cleaning performance and reduce human error. Many are focusing on automation and digital integration to enhance traceability, improve workflow efficiency, and ensure regulatory compliance. Strategic collaborations with hospitals and surgical centers are helping expand their client base and tailor solutions to real-world needs. Some players are offering value-added services such as staff training, maintenance, and compliance tracking. Global expansion through regional manufacturing facilities and localized service support is helping manufacturers increase market penetration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for endoscopy procedures

- 3.2.1.2 Technological advancements in endoscope reprocessing

- 3.2.1.3 Rising preferences for minimally invasive procedures

- 3.2.1.4 Increasing prevalence of GI disorders, cancer, and other chronic ailments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Adverse effects of chemical disinfectants

- 3.2.2.2 High cost of endoscope reprocessing devices

- 3.2.3 Market opportunities

- 3.2.3.1 Rising awareness of infection control

- 3.2.3.2 Growth in healthcare infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential

- 3.4 Growth potential analysis

- 3.5 Reimbursement scenario

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Future market trends

- 3.9 New product development landscape

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Devices

- 5.2.1 Automated endoscope reprocessors (AERs)

- 5.2.1.1 By Type

- 5.2.1.1.1 Single-door AERs

- 5.2.1.1.2 Double-door AERs

- 5.2.1.2 By Portability

- 5.2.1.2.1 Standalone AERs

- 5.2.1.2.2 Portable AERs

- 5.2.1.1 By Type

- 5.2.2 Endoscope drying, storage, and transport systems

- 5.2.3 Other devices

- 5.2.1 Automated endoscope reprocessors (AERs)

- 5.3 Consumables

- 5.3.1 Valves and adaptors

- 5.3.2 High level disinfectants

- 5.3.3 Bedside kits

- 5.3.4 Other consumables

- 5.4 Accessories

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Ambulatory surgical centers

- 6.4 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.3.7 Austria

- 7.3.8 Switzerland

- 7.3.9 CEE

- 7.3.9.1 Poland

- 7.3.9.2 Hungary

- 7.3.9.3 Romania

- 7.3.9.4 Czech Republic

- 7.3.9.5 Bulgaria

- 7.3.9.6 Rest of CEE

- 7.3.10 Nordic countries

- 7.3.10.1 Denmark

- 7.3.10.2 Sweden

- 7.3.10.3 Norway

- 7.3.10.4 Rest of Nordic countries

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia and New Zealand

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 ARC Group of Companies

- 8.2 ASP

- 8.3 Belimed

- 8.4 CONMED Corporation

- 8.5 Creo Medical

- 8.6 Ecolab

- 8.7 Getinge

- 8.8 Metrex

- 8.9 Olympus

- 8.10 Shinva Medical Instrument

- 8.11 Steelco

- 8.12 STERIS

- 8.13 Karl Storz

- 8.14 Wassenburg Medical