エネルギー高密度材料の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Energy Dense Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801877

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

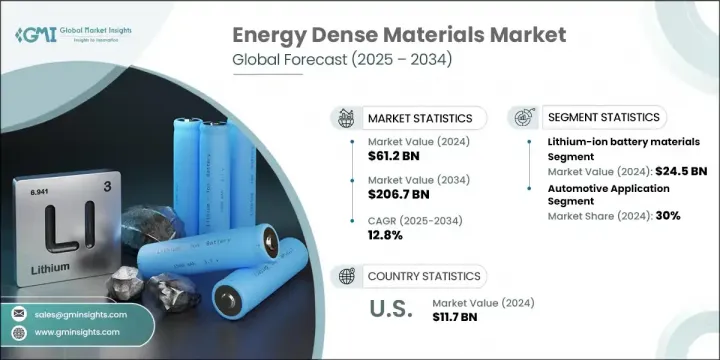

世界のエネルギー高密度材料市場は、2024年に612億米ドルと評価され、CAGR 12.8%で成長し、2034年には2,067億米ドルに達すると推定されています。

この市場は、二酸化炭素削減に対する緊急性の高まりと、より持続可能で電化されたエネルギーシステムへのシフトにより、強い勢いを見せています。再生可能エネルギー発電が牽引力を持ち続ける中、コンパクトで高効率なエネルギー貯蔵ソリューションの需要はますます重要になっています。エネルギー高密度材料は、送電網の安定性を確保し、ピーク時の供給バランスを調整し、断続的な電源からの電力供給の一貫性を改善することで、この移行をサポートします。効率的で軽量かつ大容量のエネルギー貯蔵に対する世界のニーズが高まるにつれ、その重要性はさまざまなセグメントで高まっています。

電動モビリティの台頭は、市場成長の主要因のひとつです。電気自動車が世界市場で急速に拡大するにつれて、航続距離の延長、急速充電、軽量化を実現するバッテリーの必要性が不可欠になっています。エネルギー高密度材料はまた、電動航空機やドローン用の航空宇宙推進システムでも重要な役割を果たしており、単位質量あたりのエネルギーを最大化することで、飛行時間の延長やペイロード能力の向上が実現し、最終的には航空輸送技術全体のイノベーションを促進します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 612億米ドル |

| 予測金額 | 2,067億米ドル |

| CAGR | 12.8% |

2024年、リチウムイオン電池材料セグメントは245億米ドルを生み出しました。リチウムイオン電池の普及は、燃料電池材料、スーパーコンデンサ、固体電池などの他の選択肢に比べてエネルギー密度が優れていることによる。リチウムイオン電池は、コンパクトで軽量な形態で大きなエネルギーを貯蔵するため、携帯電子機器、電気自動車、大規模エネルギー貯蔵システムに最適なソリューションとなっています。その強力な出力、サイクル寿命の延長、安定した性能により、リチウムイオン電池は現代のエネルギー貯蔵の基礎技術となっており、民生用電子機器製品から実用規模のグリッド・ストレージまで幅広い産業で急速な普及を支えています。

2024年に最大のシェアを占めたのは自動車用途で、30%のシェアを占めています。これらの用途は、より遠くまで走行でき、より早く充電でき、従来型エンジン性能に匹敵する自動車に対するニーズの高まりに後押しされ、エネルギー密度の高い材料技術革新の中心となっています。単位面積・重量当たりのエネルギー密度を高めるバッテリー技術は、消費者の航続距離に対する懸念に対応し、EVの普及を支えます。自動車産業が拡大を続けるなか、自動車産業は引き続き市場成長の重要な原動力となっています。

米国のエネルギー高密度材料市場は2024年に117億米ドルに達し、2034年まで13%のCAGRで成長すると予測されます。着実な経済拡大、エネルギー需要の増加、産業の成長に伴い、米国では効率的な電池、磁石、燃料電池部品の需要が高まっています。エネルギー高密度材料は、産業がエネルギー使用を最適化し、コストを削減し、システム全体の性能を向上させるのに役立っています。エネルギー貯蔵と変換におけるその役割は、部門を問わず、より強靭で効率的なエネルギーインフラを構築するために不可欠であり続けています。

エネルギー高密度材料の世界市場で事業を展開している主要企業には、LG Energy Solution、Panasonic Corporation、Samsung SDI Co.Ltd.(CATL)などがあります。世界のエネルギー高密度材料市場における骨格を固めるため、主要企業はいくつかの戦略的優先事項に注力しています。これには、エネルギー密度、安全性、ライフサイクルを改善する先端化学品の研究開発への積極的な投資が含まれます。各社はまた、特に主要成長地域におけるEVとグリッド需要の増加に対応するため、生産能力を拡大しています。自動車メーカーやエネルギープロバイダとの戦略的提携は、長期契約の確保に役立っています。さらに、企業は製品ポートフォリオを多様化し、ソリッドステート技術やリチウム硫黄技術のような次世代材料を含めると同時に、コスト効率と安定性のために世界サプライチェーンを最適化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 産業の潜在的リスク・課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- 価格動向

- 地域別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場規模・予測:材料別、2021~2034年

- 主要動向

- リチウムイオン電池材料

- 正極材料(LFP、NMC、NCA、LCO)

- 負極材料(黒鉛、シリコン、リチウム金属)

- 電解質材料

- セパレーター材料

- 固体電池材料

- 固体電解質(酸化物、硫化物、ポリマー)

- インターフェース材料

- 先進電極材料

- スーパーコンデンサ材料

- 電極材料(炭素系、金属酸化物)

- 電解質溶液

- セパレーター材料

- 先進炭材料料

- グラフェンとその誘導体

- カーボンナノチューブ

- 炭素繊維複合材

- エネルギー材料

- 高エネルギー密度化合物

- 推進剤

- 爆発物

- 燃料電池材料

- 触媒材料

- 膜材料

- 電極材料

第6章 市場規模・予測:用途別、2021~2034年

- 主要動向

- 自動車用途

- 電気自動車(BEV、PHEV、HEV)

- 自動車用電子機器

- スタートストップシステム

- 民生用電子機器

- スマートフォンとタブレット

- ノートパソコンとウェアラブル

- パワーバンクとポータブルデバイス

- エネルギー貯蔵システム

- グリッドスケール貯蔵

- 住宅エネルギー貯蔵

- 商業と産業用貯蔵

- 航空宇宙と防衛

- 航空機と宇宙船への用途

- 軍事と防衛システム

- 無人車両とドローン

- 産業用途

- マテリアルハンドリング機器

- バックアップ電源システム

- 通信インフラ

- 医療とヘルスケア

- 埋め込み型デバイス

- 携帯型医療機器

- 救急医療システム

第7章 市場規模・予測:技術別、2021~2034年

- 主要動向

- バッテリー技術

- リチウムイオン電池

- 全固体電池

- ナトリウムイオン電池

- 金属空気電池

- コンデンサ技術

- スーパーコンデンサ/ウルトラコンデンサ

- ハイブリッドコンデンサ

- セラミックコンデンサ

- 燃料電池技術

- プロトン交換膜(PEM)

- 固体酸化物燃料電池(SOFC)

- アルカリ燃料電池

- エネルギーハーベスティング技術

- 熱電材料

- 圧電材料

- 太陽光発電材料

第8章 市場規模・予測:最終用途産業別、2021~2034年

- 主要動向

- 自動車産業

- 電子機器と半導体

- エネルギーと公益事業

- 航空宇宙と防衛

- ヘルスケアと医療機器

- 工業製造業

- 通信

- 海運・輸送

第9章 市場規模・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他の中東・アフリカ

第10章 企業プロファイル

- Tesla

- Panasonic Corporation

- Samsung SDI

- LG Energy Solution

- Contemporary Amperex Technology

- BYD Company Limited

- QuantumScape Corporation

- Solid Power

- Sila Nanotechnologies

- Group14 Technologies

- Wildcat Discovery Technologies

- Amprius Technologies

- Enovix Corporation

- Ion Storage Systems

- Ampcera

- Sion Power Corporation

- Oxis Energy

目次

The Global Energy Dense Materials Market was valued at USD 61.2 billion in 2024 and is estimated to grow at a CAGR of 12.8% to reach USD 206.7 billion by 2034. This market is experiencing strong momentum due to the increasing urgency around carbon reduction and the shift toward more sustainable, electrified energy systems. As renewable energy continues to gain traction in power generation, the demand for compact and highly efficient energy storage solutions is becoming more critical. Energy dense materials support this transition by ensuring grid stability, balancing supply during peak demand, and improving the consistency of power delivery from intermittent sources. Their importance is rising across various sectors as the global appetite for efficient, lightweight, and high-capacity energy storage continues to grow.

The rise of electric mobility is one of the primary contributors to market growth. As electric vehicles scale quickly across global markets, the need for batteries that deliver longer range, faster charging, and reduced weight becomes vital. Energy dense materials also serve an important role in aerospace propulsion systems for electric aircraft and drones, where maximizing energy per unit of mass results in longer flight duration and greater payload capabilities, ultimately driving innovation across air transport technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $61.2 Billion |

| Forecast Value | $206.7 Billion |

| CAGR | 12.8% |

In 2024, the lithium-ion battery materials segment generated USD 24.5 billion. Their widespread use is driven by their superior energy density relative to other options such as fuel cell materials, supercapacitors, and solid-state batteries. Lithium-ion batteries store significant energy in compact, lightweight formats, making them the go-to solution for portable electronics, electric vehicles, and large-scale energy storage systems. Their strong power output, extended cycle life, and stable performance have made them a foundational technology in modern energy storage and have supported fast adoption across industries ranging from consumer electronics to utility-scale grid storage.

The automotive applications segment held the largest share in 2024, accounting for 30% share. These applications are at the heart of energy dense material innovation, driven by the rising need for vehicles that can travel further, charge quicker, and match traditional engine performance. Battery technologies delivering greater energy density per unit of space and weight help address consumer range concerns and support widespread EV adoption. As the automotive industry continues to expand, it remains a key force behind the market's growth.

U.S. Energy Dense Materials Market reached USD 11.7 billion in 2024 and is forecasted to grow at a CAGR of 13% through 2034. With steady economic expansion, increased energy needs, and industrial growth, the U.S. has seen rising demand for efficient batteries, magnets, and fuel cell components. Energy dense materials are helping industries optimize energy use, reduce costs, and improve overall system performance. Their role in energy storage and conversion across sectors continues to make them essential for building a more resilient and efficient energy infrastructure.

Key companies operating in the Global Energy Dense Materials Market include LG Energy Solution, Panasonic Corporation, Samsung SDI Co., Ltd., Tesla, Inc., and Contemporary Amperex Technology Co. Limited (CATL). To strengthen their foothold in the global energy dense materials landscape, leading companies are focusing on several strategic priorities. These include aggressive investment in R&D for advanced chemistries that improve energy density, safety, and lifecycle. Companies are also scaling up production capacities to meet rising EV and grid demand, particularly in key growth regions. Strategic alliances with automakers and energy providers are helping secure long-term contracts. Additionally, firms are diversifying product portfolios to include next-gen materials like solid-state and lithium-sulfur technologies, while optimizing their global supply chains for cost efficiency and stability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material type

- 2.2.3 Application

- 2.2.4 End Use Industry

- 2.2.5 Technology

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Material Type, 2021-2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Lithium-ion battery materials

- 5.2.1 Cathode materials (LFP, NMC, NCA, LCO)

- 5.2.2 Anode materials (graphite, silicon, lithium metal)

- 5.2.3 Electrolyte materials

- 5.2.4 Separator materials

- 5.3 Solid-state battery materials

- 5.3.1 Solid electrolytes (oxide, sulfide, polymer)

- 5.3.2 Interface materials

- 5.3.3 Advanced electrode materials

- 5.4 Supercapacitor materials

- 5.4.1 Electrode materials (carbon-based, metal oxides)

- 5.4.2 Electrolyte solutions

- 5.4.3 Separator materials

- 5.5 Advanced carbon materials

- 5.5.1 Graphene and derivatives

- 5.5.2 Carbon nanotubes

- 5.5.3 Carbon fiber composites

- 5.6 Energetic materials

- 5.6.1 High energy density compounds

- 5.6.2 Propellant materials

- 5.6.3 Explosive materials

- 5.7 Fuel cell materials

- 5.7.1 Catalyst materials

- 5.7.2 Membrane materials

- 5.7.3 Electrode materials

Chapter 6 Market Size and Forecast, By Application, 2021-2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Automotive applications

- 6.2.1 Electric vehicles (BEV, PHEV, HEV)

- 6.2.2 Automotive electronics

- 6.2.3 Start-stop systems

- 6.3 Consumer electronics

- 6.3.1 Smartphones and tablets

- 6.3.2 Laptops and wearables

- 6.3.3 Power banks and portable devices

- 6.4 Energy storage systems

- 6.4.1 Grid-scale storage

- 6.4.2 Residential energy storage

- 6.4.3 Commercial and industrial storage

- 6.5 Aerospace and defense

- 6.5.1 Aircraft and spacecraft applications

- 6.5.2 Military and defense systems

- 6.5.3 Unmanned vehicles and drones

- 6.6 Industrial applications

- 6.6.1 Material handling equipment

- 6.6.2 Backup power systems

- 6.6.3 Telecommunications infrastructure

- 6.7 Medical and healthcare

- 6.7.1 Implantable devices

- 6.7.2 Portable medical equipment

- 6.7.3 Emergency medical systems

Chapter 7 Market Size and Forecast, By Technology, 2021-2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Battery technologies

- 7.2.1 Lithium-ion batteries

- 7.2.2 Solid-state batteries

- 7.2.3 Sodium-ion batteries

- 7.2.4 Metal-air batteries

- 7.3 Capacitor technologies

- 7.3.1 Supercapacitors/ultracapacitors

- 7.3.2 Hybrid capacitors

- 7.3.3 Ceramic capacitors

- 7.4 Fuel cell technologies

- 7.4.1 Proton exchange membrane (PEM)

- 7.4.2 Solid oxide fuel cells (SOFC)

- 7.4.3 Alkaline fuel cells

- 7.5 Energy harvesting technologies

- 7.5.1 Thermoelectric materials

- 7.5.2 Piezoelectric materials

- 7.5.3 Photovoltaic materials

Chapter 8 Market Size and Forecast, By End Use Industry, 2021-2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 Automotive industry

- 8.3 Electronics and semiconductors

- 8.4 Energy and utilities

- 8.5 Aerospace and defense

- 8.6 Healthcare and medical devices

- 8.7 Industrial manufacturing

- 8.8 Telecommunications

- 8.9 Marine and transportation

Chapter 9 Market Size and Forecast, By Region, 2021-2034 (USD Million) (Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Tesla

- 10.2 Panasonic Corporation

- 10.3 Samsung SDI

- 10.4 LG Energy Solution

- 10.5 Contemporary Amperex Technology

- 10.6 BYD Company Limited

- 10.7 QuantumScape Corporation

- 10.8 Solid Power

- 10.9 Sila Nanotechnologies

- 10.10 Group14 Technologies

- 10.11 Wildcat Discovery Technologies

- 10.12 Amprius Technologies

- 10.13 Enovix Corporation

- 10.14 Ion Storage Systems

- 10.15 Ampcera

- 10.16 Sion Power Corporation

- 10.17 Oxis Energy

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日