ハイブリッドUAVの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Hybrid UAV Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801832

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

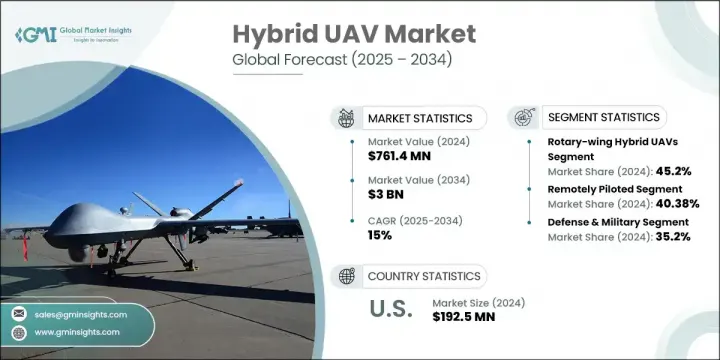

ハイブリッドUAVの世界市場は、2024年には7億6,140万米ドルとなり、CAGR15%で成長し、2034年までには30億米ドルに達すると推定されています。

この拡大に拍車をかけている最大の要因の1つは、監視・偵察活動における飛行時間の延長に対する需要の高まりです。従来のバッテリー駆動のドローンでは、大規模なエリアや遠隔地をカバーするのに必要な耐久性には到底及びません。電気推進システムと燃料推進システムを組み合わせたハイブリッドUAVは、このギャップを埋めるために参入し、しばしば10時間から12時間を超える飛行時間を提供しています。継続的なリアルタイムデータを提供できるため、戦場監視、海上パトロール、国境監視、災害対応などさまざまな分野で重宝されています。その存在は農業分野でも急速に拡大しており、作物のモニタリング、土壌分析、灌漑計画、害虫検出などを支援しています。広大で不規則な土地を効率的に運用できるハイブリッドUAVは、精密農業や環境モニタリングのツールとして好まれるようになっています。

様々なカテゴリーの中で、回転翼型ハイブリッドUAVが最も急成長を遂げており、2025年から2034年のCAGRは15.2%と予想されています。ホバリング、垂直離陸、狭い空間での航行が可能なため、人口密集地やインフラが多い環境での使用に最適です。これらのUAVに対する政府部門と商業部門の両方からの需要は増加し続けており、特に救急サービス、検査、戦術的監視に使用されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 7億6,140万米ドル |

| 予測金額 | 30億米ドル |

| CAGR | 15% |

遠隔操縦ハイブリッドUAV分野は、2024年に3億750万米ドルを生み出しました。これらのシステムは、人間が直接関与する必要があるミッションに不可欠なコンポーネントであり続けています。防衛や緊急対応などの分野では、運用の柔軟性と比較的低コストであることから、手動操縦のUAVに対する需要が強いです。特に人間の判断が重要な任務では、監視・警備活動におけるUAVの重要性は高まり続けています。

米国のハイブリッドUAV市場は2024年に1億9,250万米ドルを生み出し、CAGR15.5%で成長しました。同国は、防衛能力を近代化し、自動化を部門横断的に拡大する取り組みを加速しています。研究開発への投資、有利な規制支援、主要な防衛イニシアティブが、ハイブリッドUAVシステムの採用を後押ししています。これらの航空機は、ロジスティクス、スマート農業、インフラ評価、緊急アプリケーションに積極的に導入されています。ドローンを商業および民間事業に統合することを目的としたプログラムは、今後さらに成長を促進すると予想されます。

ハイブリッドUAV市場を形成する主要企業には、Lockheed Martin、eroVironment、eonardo S.p.A.、Israel Aerospace Industries (IAI)、DJI Innovations、General Atomics、BAE Systems、Boeing、Thales Group、Elbit Systems、Parrot SA、Airbus、Saab AB、Textron Systems、Northrop Grummanなどがあります。市場ポジションを確固たるものにするため、ハイブリッドUAV分野の企業は技術革新と技術統合に重点を置いています。大手企業は、燃料効率の向上、二重推進機能、AIベースのデータ処理を備えたUAVプラットフォームを開発し、耐久性と性能を伸ばしています。多くの企業は、農業から安全保障に至るまで、さまざまなミッションプロファイルに合わせたカスタマイズを可能にするモジュール式UAV設計に投資しています。政府機関や防衛機関との戦略的パートナーシップにより、市場への浸透が進んでいます。さらに、企業は需要の増加に対応するため、生産能力を拡大し、世界サプライチェーンを確立しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 成長促進要因

- 長時間にわたる監視・偵察任務の需要増加

- 商業農業における無人航空機(UAV)の導入増加

- ラストマイル配送物流におけるドローンの利用増加

- 先進的な無人機の調達を支援する防衛予算の拡大

- ハイブリッド推進ドローン技術への投資を加速

- 業界の潜在的リスク・課題

- ハイブリッドシステムの開発・保守コストが高め

- BVLOS・自律型UAVの運用に関する規制上の制限

- 成長促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 過去の価格分析(2021年~2024年)

- 価格動向の要因

- 地域による価格差

- 価格予測(2025年~2034年)

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 持続可能な材料の評価

- カーボンフットプリント分析

- 循環型経済の実現

- 持続可能性の認証と基準

- 持続可能性ROI分析

- 世界の消費者感情分析

- 特許分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 市場集中分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- チャレンジャー

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展、2021年~2024年

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 固定翼ハイブリッドUAV

- 回転翼ハイブリッドUAV

- VTOL(垂直離着陸)ハイブリッドUAV

第6章 市場推計・予測:動作モード別、2021年~2034年

- 主要動向

- 遠隔操縦

- 有人操縦オプション

- 完全自律

第7章 市場推計・予測:電源別、2021年~2034年

- 主要動向

- ガソリン電気ハイブリッド

- 太陽光発電ハイブリッド

- 燃料電池ハイブリッド

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 監視と偵察

- マッピングと測量

- 農業(例:作物の監視、散布)

- 配送と物流

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 防衛・軍事

- 固定翼ハイブリッドUAV

- 回転翼ハイブリッドUAV

- VTOL(垂直離着陸)ハイブリッドUAV

- 商業用

- 固定翼ハイブリッドUAV

- 回転翼ハイブリッドUAV

- VTOL(垂直離着陸)ハイブリッドUAV

- 政府・法執行機関

- 固定翼ハイブリッドUAV

- 回転翼ハイブリッドUAV

- VTOL(垂直離着陸)ハイブリッドUAV

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- グローバルプレーヤー

- AeroVironment

- Alpha Unmanned Systems

- Autel Robotics

- BAE Systems

- Boeing

- Delair

- DJI Innovations

- EHang

- Elbit Systems

- General Atomics

- Israel Aerospace Industries(IAI)

- Kratos Defense &Security Solutions

- Leonardo S.p.A.

- Lockheed Martin

- Northrop Grumman

- Parrot SA

- Quantum Systems

- Saab AB

- Skyfront

- Textron Systems

- Thales Group

- Zipline

- 地域プレーヤー

- American Robotics

- AgEagle Aerial Systems

- Draganfly Inc.

- Airbus SE

- Delair SAS

- Ehang Holdings Ltd.

- Turkish Aerospace Industries

- 新興プレーヤー

- Anduril Industries

- Shield AI

- Skydio

目次

The Global Hybrid UAV Market was valued at USD 761.4 million in 2024 and is estimated to grow at a CAGR of 15% to reach USD 3 billion by 2034. One of the biggest factors fueling this expansion is the rising demand for extended flight time in surveillance and reconnaissance operations. Traditional battery-powered drones simply can't match the endurance needed for large-scale or remote area coverage. Hybrid UAVs, with their combination of electric and fuel propulsion systems, are stepping in to bridge this gap, offering flight times that often exceed 10 to 12 hours. Their ability to deliver continuous real-time data makes them valuable in various sectors such as battlefield monitoring, maritime patrolling, border surveillance, and disaster response. Their presence is also expanding rapidly in agriculture, where they assist with crop monitoring, soil analysis, irrigation planning, and pest detection. With their capability to operate over large and irregular landscapes efficiently, hybrid UAVs are becoming a preferred tool for precision farming and environmental monitoring.

Among the various categories, the rotary-wing hybrid UAVs are witnessing the fastest growth, with an expected CAGR of 15.2% during 2025-2034. Their ability to hover, take off vertically, and navigate tight spaces has made them a top choice for use in densely populated and infrastructure-heavy environments. Demand from both government and commercial sectors for these UAVs continues to rise, particularly for use in emergency services, inspections, and tactical surveillance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $761.4 Million |

| Forecast Value | $3 Billion |

| CAGR | 15% |

The remotely piloted hybrid UAVs segment generated USD 307.5 million in 2024. These systems remain a vital component of missions that require direct human involvement. In sectors such as defense and emergency response, the demand for manually controlled UAVs is strong due to their operational flexibility and relatively low cost. Their importance in surveillance and security operations continues to grow, especially for tasks where human judgment is critical.

United States Hybrid UAV Market was valued at USD 192.5 million in 2024, growing at a CAGR of 15.5%. The country is accelerating efforts to modernize its defense capabilities and expand automation across sectors. Investments in R&D, favorable regulatory support, and major defense initiatives are boosting the adoption of hybrid UAV systems. These aircraft are being actively deployed in logistics, smart agriculture, infrastructure assessment, and emergency applications. Programs aimed at integrating drones into commercial and civilian operations are expected to further drive growth in the years ahead.

Key players shaping the Hybrid UAV Market include Lockheed Martin, AeroVironment, Leonardo S.p.A., Israel Aerospace Industries (IAI), DJI Innovations, General Atomics, BAE Systems, Boeing, Thales Group, Elbit Systems, Parrot SA, Airbus, Saab AB, Textron Systems, and Northrop Grumman. To solidify their market position, companies in the hybrid UAV space are focusing heavily on innovation and technological integration. Leading players are developing UAV platforms with enhanced fuel efficiency, dual-propulsion capabilities, and AI-based data processing to extend endurance and performance. Many firms are investing in modular UAV designs that allow customization for different mission profiles, from agriculture to security. Strategic partnerships with government agencies and defense organizations are enabling deeper market penetration. Additionally, businesses are expanding production capacity and establishing global supply chains to meet rising demand.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Packaging type trends

- 2.2.2 Material trends

- 2.2.3 Application trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspective: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for long-endurance surveillance and reconnaissance missions

- 3.2.1.2 Rising adoption of UAVs in commercial agriculture

- 3.2.1.3 Growing use of drones for last-mile delivery logistics

- 3.2.1.4 Expansion of defense budgets supporting advanced UAV procurement

- 3.2.1.5 Accelerating investment in hybrid propulsion drone technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and maintenance costs of hybrid systems

- 3.2.2.2 Regulatory restrictions on BVLOS and autonomous UAV operations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2021-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2025-2034)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.12.1 Sustainable materials assessment

- 3.12.2 Carbon footprint analysis

- 3.12.3 Circular economy implementation

- 3.12.4 Sustainability certifications and standards

- 3.12.5 Sustainability roi analysis

- 3.13 Global consumer sentiment analysis

- 3.14 Patent analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Fixed-Wing Hybrid UAVs

- 5.3 Rotary-Wing Hybrid UAVs

- 5.4 VTOL (Vertical Take-Off and Landing) Hybrid UAVs

Chapter 6 Market Estimates and Forecast, By Mode of Operation, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Remotely Piloted

- 6.3 Optionally Piloted

- 6.4 Fully Autonomous

Chapter 7 Market Estimates and Forecast, By Power Source, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Gasoline-Electric Hybrid

- 7.3 Solar-Electric Hybrid

- 7.4 Fuel Cell-Electric Hybrid

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Surveillance & Reconnaissance

- 8.3 Mapping & Surveying

- 8.4 Agriculture (e.g., crop monitoring, spraying)

- 8.5 Delivery & Logistics

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 Defense & Military

- 9.2.1 Fixed-Wing Hybrid UAVs

- 9.2.2 Rotary-Wing Hybrid UAVs

- 9.2.3 VTOL (Vertical Take-Off and Landing) Hybrid UAVs

- 9.3 Commercial

- 9.3.1 Fixed-Wing Hybrid UAVs

- 9.3.2 Rotary-Wing Hybrid UAVs

- 9.3.3 VTOL (Vertical Take-Off and Landing) Hybrid UAVs

- 9.4 Government & Law Enforcement

- 9.4.1 Fixed-Wing Hybrid UAVs

- 9.4.2 Rotary-Wing Hybrid UAVs

- 9.4.3 VTOL (Vertical Take-Off and Landing) Hybrid UAVs

- 9.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 AeroVironment

- 11.1.2 Alpha Unmanned Systems

- 11.1.3 Autel Robotics

- 11.1.4 BAE Systems

- 11.1.5 Boeing

- 11.1.6 Delair

- 11.1.7 DJI Innovations

- 11.1.8 EHang

- 11.1.9 Elbit Systems

- 11.1.10 General Atomics

- 11.1.11 Israel Aerospace Industries (IAI)

- 11.1.12 Kratos Defense & Security Solutions

- 11.1.13 Leonardo S.p.A.

- 11.1.14 Lockheed Martin

- 11.1.15 Northrop Grumman

- 11.1.16 Parrot SA

- 11.1.17 Quantum Systems

- 11.1.18 Saab AB

- 11.1.19 Skyfront

- 11.1.20 Textron Systems

- 11.1.21 Thales Group

- 11.1.22 Zipline

- 11.2 Regional Players

- 11.2.1 American Robotics

- 11.2.2 AgEagle Aerial Systems

- 11.2.3 Draganfly Inc.

- 11.2.4 Airbus SE

- 11.2.5 Delair SAS

- 11.2.6 Ehang Holdings Ltd.

- 11.2.7 Turkish Aerospace Industries

- 11.3 Emerging Players

- 11.3.1 Anduril Industries

- 11.3.2 Shield AI

- 11.3.3 Skydio

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日