|

市場調査レポート

商品コード

1801819

ポイントオブケアCTイメージングシステムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Point-of-care CT Imaging Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ポイントオブケアCTイメージングシステムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年08月12日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

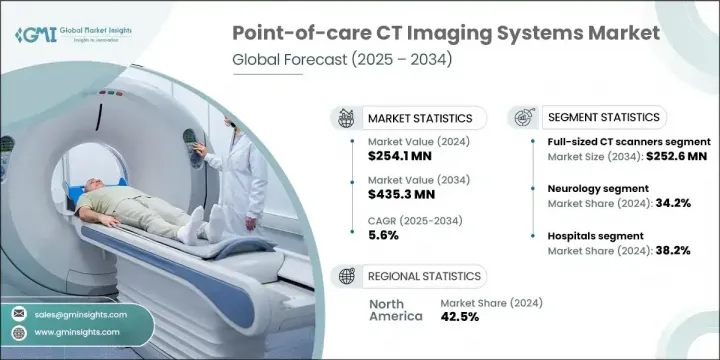

ポイントオブケアCTイメージングシステムの世界市場は、2024年には2億5,410万米ドルとなり、CAGR5.6%で成長し、2034年までには4億3,530万米ドルに達すると予測されています。

この市場の成長は、主に慢性的な健康状態の割合の増加と世界人口の急速な高齢化によって促進されています。このような要因により、迅速かつ簡便な診断ソリューションに対する需要が高まっています。ポイントオブケアCTシステムは、迅速でアクセスしやすい画像診断を提供する小型のモバイルプラットフォームであり、救急医療、外来患者センター、集中治療環境において不可欠なものとなっています。ヘルスケアモデルが患者中心の診断にシフトする中、ポータブルCTテクノロジーは、集中型病院システムに依存することなく呼吸器評価をサポートし、リアルタイムの画像診断を提供する能力で支持を集めています。

早期かつ正確な診断が転帰の管理に不可欠であることから、呼吸器疾患の症例数が増加しており、市場はさらに拡大しています。この動向の主な要因の1つは、季節的なウイルス感染症の急増で、呼吸器系医療システムの負担が大きくなっています。その結果、迅速な評価によって治療方針を即座に決定する必要がある臨床現場で、ポイントオブケアCTシステムの採用が拡大しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 2億5,410万米ドル |

| 予測金額 | 4億3,530万米ドル |

| CAGR | 5.6% |

2024年、フルサイズCTスキャナ部門は1億4,930万米ドルを売り上げました。この分野は、CAGR5.5%で成長し、2034年までには2億5,260万米ドルになると予測されています。これらのシステムは、高解像度の出力と総合的な診断能力で支持されており、重篤な救急医療に適した選択肢となっています。フルサイズモデルは、手術室、外傷治療室、集中治療部などで一般的に使用され、画像診断のスピードと詳細さが患者の転帰に重要な役割を果たします。幅広い臨床ニーズに対応できるため、病院のワークフローに欠かせません。

病院セグメントは2024年に38.2%のシェアを占め、このセグメントで最大のエンドユーザーグループであり続けています。病院の優位性は、確立された診断インフラと訓練された放射線スタッフが利用可能であることに起因します。これらの施設では、神経学、外傷、肺疾患などの複雑な症例が日常的に扱われており、迅速なポイントオブケアイメージングソリューションの恩恵を受けています。病院が診断スピードとサービス提供を強化し続けるにつれて、モバイルCTシステムに対する需要はますます高まっています。

米国のポイントオブケアCTイメージングシステムは2024年に1億190万米ドルを生み出し、世界市場における主導権を維持しています。慢性疾患やがんの罹患率が高く、強固なヘルスケア提供体制が継続的な普及を後押ししています。さらに、良好な規制状況、早期診断に対する意識の高まり、先進医療用画像処理技術への多額の投資が、市場の持続的な拡大を支えています。

ポイントオブケアCTイメージングシステム市場を積極的に形成している主要企業には、Carestream Dental、Planmed、Xoran Technologies、CurveBeam、Siemens Healthineers、NeuroLogica、Epica International、SOREDEX、Stryker、Alinetaなどがあります。ポイントオブケアCTイメージングシステム市場の主要企業は、画質、携帯性、システムの使いやすさを向上させるため、技術革新に多額の投資を行っています。差別化を図るため、多くの企業が診断スピードと精度を高めるAI統合プラットフォームの開発に注力しています。病院、診断センター、遠隔医療プロバイダーとの戦略的提携は、特に分散型医療環境での採用を後押しします。複数のメーカーが、外来、ICU、地方医療環境に合わせたコンパクトなワイヤレスシステムで製品ポートフォリオを拡大しています。各社はまた、規制当局の承認やファストトラッククリアランスを活用して、先進モデルをより早く市場に投入しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- 慢性疾患の有病率の増加

- 高齢化人口の増加

- 早期診断と治療の重要性の高まり

- 画像システムの技術的進歩

- 業界の潜在的リスク・課題

- 画像システムの高コスト

- 規制と償還の障壁

- 市場機会

- 農村部や遠隔地への拡大

- AIと遠隔医療との統合

- 成長促進要因

- 成長可能性分析

- 規制情勢

- 技術的進歩

- 現在の技術動向

- 新興技術

- サプライチェーン分析

- 償還シナリオ

- 価格分析、2024年

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- コンパクトCTスキャナー

- フルサイズCTスキャナー

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 神経学

- 呼吸器

- 筋骨格

- 耳鼻咽喉科

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- クリニック

- その他の用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Arineta

- Carestream Dental

- CurveBeam

- Epica International

- NeuroLogica

- Planmed

- Siemens Healthineers

- SOREDEX

- Stryker

- Xoran Technologies

The Global Point-of-care CT Imaging Systems Market was valued at USD 254.1 million in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 435.3 million by 2034. Growth in this market is primarily fueled by the increasing rates of chronic health conditions and a rapidly aging global population. These factors are driving higher demand for immediate and convenient diagnostic solutions. Point-of-care CT systems are compact, mobile platforms that offer fast and accessible imaging, making them essential in emergency care, outpatient centers, and intensive care environments. As healthcare models shift toward patient-centric diagnostics, portable CT technologies are gaining traction for their ability to support respiratory evaluations and deliver real-time imaging without depending on centralized hospital systems.

Rising cases of respiratory conditions are further strengthening the market, as early and accurate diagnosis remains critical in managing outcomes. One of the major contributors to this trend is the seasonal spike in viral infections, which significantly adds to the burden on respiratory health systems. As a result, there's growing adoption of point-of-care CT systems across clinical settings where fast assessments are needed to inform immediate treatment decisions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $254.1 Million |

| Forecast Value | $435.3 Million |

| CAGR | 5.6% |

In 2024, the full-sized CT scanners segment generated USD 149.3 million. This segment is projected to grow to USD 252.6 million by 2034, advancing at a CAGR of 5.5%. These systems are favored for their high-resolution output and comprehensive diagnostic capabilities, making them the preferred option for critical and emergency care. Full-sized models are commonly used in surgical theaters, trauma units, and intensive care departments where speed and detail in imaging play a vital role in patient outcomes. Their ability to support a wide range of clinical needs makes them indispensable in hospital workflows.

The hospitals segment held a 38.2% share in 2024, remaining the largest End user group in this segment. The dominance of hospitals is attributed to their established diagnostic infrastructure and the availability of trained radiology staff. These institutions routinely handle complex cases in neurology, trauma, and pulmonary care, all of which benefit from rapid point-of-care imaging solutions. As hospitals continue to enhance their diagnostic speed and service delivery, the demand for mobile CT systems grows stronger.

U.S. Point-of-care CT Imaging Systems Market generated USD 101.9 million in 2024, maintaining its leadership in the global space. The country's high incidence of chronic illnesses and cancer, paired with its robust healthcare delivery systems, drives ongoing adoption. Furthermore, a favorable regulatory landscape, increasing awareness of early diagnostics, and substantial investments in advanced medical imaging technologies support sustained market expansion.

Key players actively shaping the Point-of-care CT Imaging Systems Market include Carestream Dental, Planmed, Xoran Technologies, CurveBeam, Siemens Healthineers, NeuroLogica, Epica International, SOREDEX, Stryker, and Arineta. Leading companies in the point-of-care CT imaging systems market are investing heavily in innovation to improve image quality, portability, and system usability. To differentiate themselves, many are focusing on the development of AI-integrated platforms that enhance diagnostic speed and accuracy. Strategic collaborations with hospitals, diagnostic centers, and telehealth providers help boost adoption, particularly in decentralized care settings. Several manufacturers are expanding their product portfolios with compact, wireless systems tailored for outpatient, ICU, and rural care environments. Companies are also leveraging regulatory approvals and fast-track clearances to bring advanced models to market faster.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic disorders

- 3.2.1.2 Growing aging population

- 3.2.1.3 Rising emphasis on early diagnosis and treatment

- 3.2.1.4 Technological advancements in imaging system

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of imaging systems

- 3.2.2.2 Regulatory and reimbursement barriers

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into rural and remote areas

- 3.2.3.2 Integration with AI and telemedicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.9 Future market trends

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Compact CT scanners

- 5.3 Full-sized CT scanners

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Neurology

- 6.3 Respiratory

- 6.4 Musculoskeletal

- 6.5 ENT

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgery centers

- 7.4 Clinics

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Arineta

- 9.2 Carestream Dental

- 9.3 CurveBeam

- 9.4 Epica International

- 9.5 NeuroLogica

- 9.6 Planmed

- 9.7 Siemens Healthineers

- 9.8 SOREDEX

- 9.9 Stryker

- 9.10 Xoran Technologies