家庭紙市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Household Paper Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801802

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

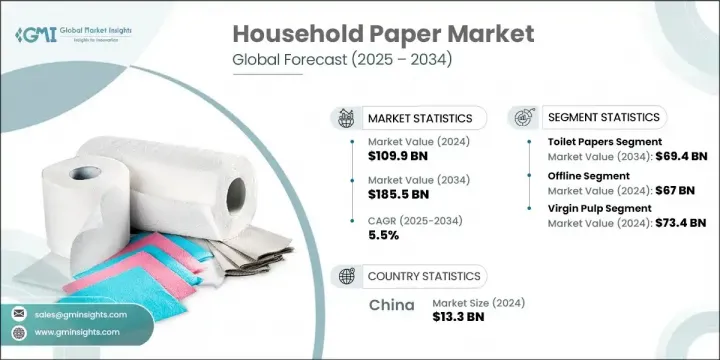

世界の家庭紙市場は、2024年には1,099億米ドルとなり、CAGR 5.5%で成長し、2034年には1,855億米ドルに達すると推定されています。

ライフスタイルの変化、都市人口の拡大、可処分所得の増加により、消費者の習慣が再構築され、この増加傾向は続いています。都市に移り住む人が増えるにつれ、便利で衛生的な紙製品への需要が高まっています。都会での生活は、日常生活が忙しくなるだけでなく、水へのアクセスが限られているなどの課題ももたらし、使い捨ての衛生用品へのニーズが高まっています。これとは対照的に、低所得層ではこうした製品へのアクセスが制限されており、世界市場の軌道を左右する格差が生じています。

可処分所得の高い消費者は、より柔らかく、耐久性に優れ、ブランド品質の高い高級紙製品を好む傾向があります。こうした消費者は、ティッシュ、ペーパータオル、トイレットペーパーといった必需品に付加価値を求める傾向が強いです。さらに、世界の衛生基準に対する意識の高まりが、使い捨て紙製品の需要を拡大しています。市場はまた、技術革新によるダイナミックな変化を目の当たりにしています。環境に優しい素材、超ソフトな肌触り、多層構造などの新機能は、快適さと持続可能性に重点を置く現代的な購買層の進化する嗜好に対応するためにブランドを支援しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,099億米ドル |

| 予測金額 | 1,855億米ドル |

| CAGR | 5.5% |

トイレットペーパー部門は2024年に396億米ドルを生み出し、2034年には694億米ドルに増加すると予測されています。トイレットペーパーは、最も支配的な家庭紙カテゴリーとしてリードを維持しています。その実用的な性質、広く受け入れられていること、ソフトで香り高く高品質な製品への嗜好の高まりが、先進経済諸国と新興経済諸国の両方で好調な業績を牽引しています。所得水準が上昇し、都市化が進むにつれて、トイレットペーパーは世界中の家庭で日常的に使用される製品としての役割を固め続けています。

2024年、オフライン小売チャネル部門の売上高は670億米ドルで、2025~2034年のCAGRは5.3%で成長すると予想されています。オフライン販売は、アクセスのしやすさ、製品の即時入手可能性、物理的な小売環境に対する消費者の信頼といった要因から、依然として世界最大のシェアを占めています。このセグメントには、スーパーマーケット、コンビニエンスストア、ハイパーマーケットなどの小売チェーンが含まれます。これらの小売チェーンでは、顧客が実際に商品を手に取って評価することができるため、オンラインチャネルよりも効果的に購買行動に影響を与えることが多いです。

中国の家庭紙市場は2024年に133億米ドルを生み出し、2025年から2034年にかけてCAGR 6.2%で力強い成長を遂げようとしています。中国では、衛生意識の高まり、中間層の拡大、消費者の消費意欲の高まりにより、この分野が急速に拡大しています。近代的な小売システムとデジタル・プラットフォームにより、製品へのリーチと入手性が向上しており、健康に対する社会的関心(特に世界の健康イベント後)の高まりにより、家庭紙商品の常用へのシフトが強化され続けています。

世界の家庭紙市場を形成している著名企業には、Kimberly-Clark、Essity、Hengan International Group、Georgia-Pacific、Sofidel Group、Asia Pulp &Paper、WEPA Group、SCA Group/Svenska Cellulosa Aktiebolaget、日本製紙、王子ホールディングス、Procter &Gamble、Kruger Products、Metsa Tissue-Metsa Group、Vinda International Holdings、Cascadesなどがあります。進化する市場競争の中で競争力を維持するため、大手企業はいくつかの主要戦略に注力してきました。そのひとつが、健康や環境に配慮する消費者にアピールする、環境に配慮した素材や多機能デザインなどの製品イノベーションへの投資です。各社はまた、特に新興国において、小売拠点の拡大やオムニチャネル戦略の活用により、流通網を強化しています。戦略的パートナーシップや合併は、企業が地理的なフットプリントを拡大するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 機会

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 規制の枠組み

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーターのファイブフォース分析

- PESTEL分析

- 消費者行動分析

- 購入パターン

- 嗜好分析

- 消費者行動の地域差

- eコマースが購買決定に与える影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ航空

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- トイレットペーパー

- トイレットペーパー

- キッチンペーパー

- ティッシュペーパー

- その他

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- バージンパルプ

- リサイクルパルプ

第7章 市場推計・予測:価格別、2021年~2034年

- 主要動向

- 低価格

- 中価格

- 高価格

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- オンライン

- Eコマースウェブサイト

- 会社所有のウェブサイト

- オフライン

- ハイパーマーケット/スーパーマーケット

- デパート

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第10章 企業プロファイル

- Asia Pulp &Paper

- Cascades

- Essity

- Georgia-Pacific

- Hengan International Group

- Kimberly-Clark

- Kruger Products

- Metsa Tissue-Metsa Group

- Nippon Paper Industries

- Oji Holdings

- Procter &Gamble

- SCA Group/Svenska Cellulosa Aktiebolaget

- Sofidel Group

- Vinda International Holdings

- WEPA Group

目次

The Global Household Paper Market was valued at USD 109.9 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 185.5 billion by 2034. This upward trend continues as shifting lifestyles, expanding urban populations, and rising disposable incomes reshape consumer habits. As more people move into cities, the demand for convenience and hygiene-related paper products has intensified. Urban living not only leads to busier routines but also brings challenges like limited access to water, increasing the need for disposable hygiene products. In contrast, households in lower-income brackets face restricted access to such products, creating disparities that still influence the global market's trajectory.

Consumers with higher disposable incomes tend to gravitate toward premium paper products that offer better softness, durability, and branded quality. These consumers are more likely to seek added value in essentials such as tissues, paper towels, and toilet paper. Furthermore, growing awareness around hygiene standards worldwide is driving broader demand for disposable paper items. The market is also witnessing dynamic shifts thanks to innovation-new features such as eco-friendly materials, ultra-soft textures, and multi-ply construction are helping brands cater to the evolving preferences of modern buyers focused on comfort and sustainability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $109.9 Billion |

| Forecast Value | $185.5 Billion |

| CAGR | 5.5% |

The toilet paper segment generated USD 39.6 billion in 2024 and is forecast to rise to USD 69.4 billion by 2034. It has maintained its lead as the most dominant household paper category. Its practical nature, widespread acceptance, and growing preference for soft, fragranced, and high-quality variants have driven strong performance across both developed and emerging economies. As income levels rise and urbanization expands, toilet paper continues to solidify its role as a daily-use product within homes worldwide.

In 2024, the offline retail channels segment generated USD 67 billion and is expected to grow at a CAGR of 5.3% during 2025-2034. Offline sales still hold the largest share globally due to factors like easy accessibility, immediate product availability, and consumer trust in physical retail environments. This segment includes retail chains such as supermarkets, convenience stores, and hypermarkets, which offer customers the ability to assess products in person-often influencing purchasing behavior more effectively than online channels.

China Household Paper Market generated USD 13.3 billion in 2024 and is poised for strong growth at a CAGR of 6.2% between 2025 and 2034. China is seeing rapid expansion in this sector due to increasing hygiene consciousness, a swelling middle class, and higher consumer spending power. Modern retail systems and digital platforms are improving product reach and availability, and growing public concern about health-particularly after global health events-continues to reinforce the shift toward regular use of household paper goods.

Prominent companies shaping the Global Household Paper Market include Kimberly-Clark, Essity, Hengan International Group, Georgia-Pacific, Sofidel Group, Asia Pulp & Paper, WEPA Group, SCA Group / Svenska Cellulosa Aktiebolaget, Nippon Paper Industries, Oji Holdings, Procter & Gamble, Kruger Products, Metsa Tissue - Metsa Group, Vinda International Holdings, and Cascades. To remain competitive in the evolving household paper market, leading players have focused on several key strategies. One major area has been investment in product innovation, such as eco-conscious materials and multi-functional designs that appeal to health- and environment-conscious consumers. Companies are also strengthening their distribution networks-particularly in emerging economies-by expanding retail presence and leveraging omnichannel strategies. Strategic partnerships and mergers are helping firms broaden their geographic footprint.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 Pricing

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory framework

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's five forces analysis

- 3.9 PESTEL analysis

- 3.10 Consumer behavior analysis

- 3.10.1 Purchasing patterns

- 3.10.2 Preference analysis

- 3.10.3 Regional variations in consumer behavior

- 3.10.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 MEA

- 4.2.1.5 LATAM

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 ($Bn, Tons)

- 5.1 Key trends

- 5.2 Toilet papers

- 5.3 Bathroom tissues

- 5.4 Kitchen papers

- 5.5 Facial tissues

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Material, 2021-2034 ($Bn, Tons)

- 6.1 Key trends

- 6.2 Virgin pulp

- 6.3 Recycled pulp

Chapter 7 Market Estimates & Forecast, By Pricing, 2021-2034 ($Bn, Tons)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 ($Bn, Tons)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-commerce website

- 8.2.2 Company owned website

- 8.3 Offline

- 8.3.1 Hypermarket/Supermarket

- 8.3.2 Departmental stores

- 8.3.3 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034, ($Bn, Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 10.1 Asia Pulp & Paper

- 10.2 Cascades

- 10.3 Essity

- 10.4 Georgia-Pacific

- 10.5 Hengan International Group

- 10.6 Kimberly-Clark

- 10.7 Kruger Products

- 10.8 Metsa Tissue - Metsa Group

- 10.9 Nippon Paper Industries

- 10.10 Oji Holdings

- 10.11 Procter & Gamble

- 10.12 SCA Group / Svenska Cellulosa Aktiebolaget

- 10.13 Sofidel Group

- 10.14 Vinda International Holdings

- 10.15 WEPA Group

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日