|

市場調査レポート

商品コード

1797782

自動車用コンデンサーの市場機会、成長促進要因、産業動向分析、2025~2034年予測Automotive Condenser Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用コンデンサーの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年07月16日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

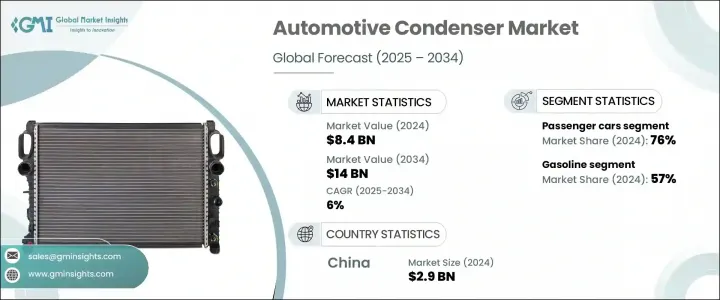

自動車用コンデンサーの世界市場規模は、2024年に84億米ドルとなり、CAGR 6%で成長し、2034年には140億米ドルに達すると予測されています。

電気自動車や次世代熱管理システムへの移行が進んでおり、自動車用コンデンサーの開発と採用に大きな影響を与えています。最新の自動車がよりコンパクトで効率的なコンポーネントを搭載するにつれて、高度な冷媒フロー、熱負荷バランシング、電気自動車に特化したHVAC構成に関する技術的習熟の必要性が高まっています。この進化は、OEMとTier-1サプライヤーの双方に、新たな需要に対応するための人材開発と専門トレーニングを優先するよう促しています。

自動車メーカーは、低GWP冷媒の使用、軽量素材、ハイブリッドおよび電気プラットフォームに合わせた高効率コンデンサーシステムに重点を移しています。この技術的転換により、特にサーマルシステムのメンテナンス、診断、コンポーネント統合において、役割に応じた業務別トレーニングが不可欠となっています。市場の成長は、熟練労働力を生み出すための教育機関と民間企業との協力関係の強化によっても支えられています。自動車プラットフォームが進化を続ける中、気候帯を超えた製品効率の確保と最適な熱性能の維持は、世界のメーカーにとって重要な検討事項となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 84億米ドル |

| 予測金額 | 140億米ドル |

| CAGR | 6% |

乗用車セグメントは2024年に76%のシェアを占め、2025年から2034年にかけてCAGR 6.8%で成長すると予想されます。このセグメントのコンデンサーは、省スペースアーキテクチャ、燃費、冷媒の国際規格への準拠を重視して設計されています。自動車メーカーは、車室内の温度調節とバッテリーの温度調節をサポートするために、高効率で軽量なコンデンサー・ユニットを統合することで、内燃エンジンと電気自動車の両プラットフォームを強化しています。特にアジア太平洋と欧州での生産台数の多さが、このセグメントの成長を促進する上で重要な役割を果たしています。

ガソリン車セグメントは2024年に57%のシェアを占め、2025~2034年のCAGRは7%と予測されます。ガソリン車が優位を保っているのは、乗用車と小型商用車の両セグメントで世界的に広く普及していることが大きな要因です。これらの車両は信頼性の高い冷却性能と曇り止め性能を要求するため、自動車メーカーはコスト効率と軽量性を維持しながら優れた熱交換効率を実現するアルミニウムベースのコンデンサー・ソリューションを進めています。設計革新は、熱効率を向上させ、このカテゴリの進化する車両プラットフォームのニーズに対応する上で、依然として中心的な役割を担っています。

中国自動車用コンデンサー2024年の市場規模は29億米ドル、シェアは65%。中国の主導的地位は、同国の膨大な自動車生産能力、確立されたサプライ・チェーン・ネットワーク、および自動車の電動化の野心的な推進によって支えられています。さらに、省エネ、排ガス規制、冷媒代替をめぐる国の政策が、国内自動車生産における先進的な熱技術の展開を加速させており、世界のコンデンサー市場における中国の牙城をより強固なものにしています。

自動車用コンデンサー市場の上位を占める企業は、Modine Manufacturing Company、Valeo、ケーヒン、Sanden Holdings、Hanon Systems、Denso Corporation、MAHLEなどです。これらのプレーヤーは、技術革新と事業規模を通じて市場を形成しています。主要企業は、自動車用コンデンサー市場での競争力を強化するため、EVやハイブリッド・プラットフォームに最適化された高性能かつ軽量なコンデンサー・ソリューションを開発するための研究開発に多額の投資を行っています。ハノンシステムズ、ケーヒン、Modineなどのメーカーは、最新のモビリティ・ソリューションの熱需要を満たすコンパクトでエネルギー効率の高いユニットの設計に注力しています。自動車メーカーとの共同開発により、プラットフォームに特化した熱管理システムを共同開発することは、中核的な戦略です。また、多くの企業が世界な生産施設を拡大し、地域ごとのサプライチェーンを強化することで、より迅速な納品と各地域のコンプライアンスを確保しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 世界の自動車生産の増加

- 車両空調システムの需要増加

- HVACシステムの技術的進歩

- 政府はEVインフラと部品を支援

- 軽量・コンパクトなコンデンサ設計への移行

- 先進的なバッテリー熱管理システムへのコンデンサの統合

- 業界の潜在的リスク&課題

- サプライチェーンの混乱

- 厳しい環境規制

- 市場機会

- 商用車における電動化の増加

- 自動運転車における熱ソリューションの需要

- 環境に優しい冷媒対応コンデンサー技術の開発

- 新興国におけるアフターマーケット需要の拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV

- 商用車

- 軽作業

- 中型

- ヘビーデューティー

第6章 市場推計・予測:推進力別、2021-2034

- 主要動向

- ガソリン

- ディーゼル

- 電気

- PHEV

- ハイブリッド車

- 燃料電池自動車

第7章 市場推計・予測:デザイン別、2021-2034

- 主要動向

- 蛇紋岩

- 平行流

- チューブとフィン

第8章 市場推計・予測:材料別、2021-2034

- 主要動向

- アルミニウム

- 銅

第9章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- インドネシア

- フィリピン

- タイ

- 韓国

- シンガポール

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- AVIC Xinhang

- Calsonic Kansei

- Chaoli Hi-Tech

- Delphi Technologies

- Denso

- Fawer

- Hanon Systems

- Keihin

- Koyorad

- LUZHOU North Chemical Industries

- MAHLE

- Mitsubishi Electric

- Modine Manufacturing Company

- Nissens Automotive A/S

- Pranav Vikas

- Sanden Holdings

- Tata AutoComp Systems

- Transpro

- Valeo

- Zhejiang Yinlun Machinery

The Global Automotive Condenser Market was valued at USD 8.4 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 14 billion by 2034. The ongoing transformation toward electric vehicles and next-generation thermal management systems is significantly influencing the development and adoption of automotive condensers. As modern vehicles incorporate more compact and efficient components, there is a growing need for technical proficiency in advanced refrigerant flow, thermal load balancing, and EV-specific HVAC configurations. This evolution is prompting both OEMs and Tier-1 suppliers to prioritize workforce development and specialized training to align with emerging demands.

Automotive manufacturers are shifting focus toward low-GWP refrigerant usage, lightweight materials, and high-efficiency condenser systems tailored for hybrid and electric platforms. This technological transition has made role-based and task-specific training essential, especially in thermal systems maintenance, diagnostics, and component integration. The market's growth is also being supported by increased collaboration between training institutions and the private sector to produce a skilled labor force. As automotive platforms continue to evolve, ensuring product efficiency across climate zones and maintaining optimal thermal performance is becoming a key consideration for global manufacturers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $14 Billion |

| CAGR | 6% |

The passenger cars segment held a 76% share in 2024 and is expected to grow at a CAGR of 6.8% between 2025 and 2034. Condensers in this segment are being designed with an emphasis on space-saving architecture, fuel economy, and compliance with international standards for refrigerants. Automakers are enhancing both internal combustion engine and electric vehicle platforms by integrating high-efficiency, lightweight condenser units to support cabin climate control and battery temperature regulation. High production volumes, particularly across Asia-Pacific and Europe, are playing a vital role in propelling growth in this segment.

The gasoline-powered vehicles segment held a 57% share in 2024, with growth projected at a CAGR of 7% during 2025-2034. The sustained dominance of gasoline vehicles is largely due to their widespread global presence in both passenger and light commercial segments. As these vehicles demand reliable cooling and defogging performance, automakers are advancing aluminum-based condenser solutions that deliver excellent heat exchange efficiency while remaining cost-effective and lightweight. Design innovation remains central to improving thermal efficiency and meeting evolving vehicle platform needs in this category.

China Automotive Condenser Market generated USD 2.9 billion and held a 65% share in 2024. Its leadership position is supported by the country's vast vehicle manufacturing capacity, established supply chain networks, and ambitious push for vehicle electrification. Additionally, national policies around energy savings, emissions control, and refrigerant substitution are accelerating the deployment of advanced thermal technologies in domestic vehicle production, thereby reinforcing China's stronghold in the global condenser market.

The top-performing companies in the Automotive Condenser Market include Modine Manufacturing Company, Valeo, Keihin, Sanden Holdings, Hanon Systems, Denso Corporation, and MAHLE. These players are shaping the market through technological innovation and operational scale. To reinforce their competitive position in the automotive condenser market, leading companies are heavily investing in R&D to develop high-performance and lightweight condenser solutions optimized for EVs and hybrid platforms. Manufacturers like Hanon Systems, Keihin, and Modine are focused on designing compact and energy-efficient units that meet the thermal demands of modern mobility solutions. Collaboration with automotive OEMs to co-develop platform-specific thermal management systems is a core strategy. Many companies are also expanding global production facilities and enhancing regional supply chains to ensure faster delivery and local compliance.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Design

- 2.2.5 Material

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production

- 3.2.1.2 Growing demand for vehicle air conditioning system

- 3.2.1.3 Technological advancements in HVAC systems

- 3.2.1.4 Government supports EV infrastructure and components

- 3.2.1.5 Shift towards lightweight, compact condenser designs

- 3.2.1.6 Integration of condensers in advanced battery thermal management systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain disruptions

- 3.2.2.2 Stringent environmental regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Increased vehicle electrification in commercial fleets

- 3.2.3.2 Demand for thermal solutions in autonomous vehicles

- 3.2.3.3 Development of eco-friendly refrigerant-compatible condenser technologies

- 3.2.3.4 Expansion of aftermarket demand in emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Sedans

- 5.2.2 Hatchbacks

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light duty

- 5.3.2 Medium duty

- 5.3.3 Heavy duty

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 Electric

- 6.4.1 PHEV

- 6.4.2 HEV

- 6.4.3 FCEV

Chapter 7 Market Estimates & Forecast, By Design, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Serpentine

- 7.3 Parallel flow

- 7.4 Tube and fin

Chapter 8 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Aluminium

- 8.3 Copper

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Indonesia

- 10.4.6 Philippines

- 10.4.7 Thailand

- 10.4.8 South Korea

- 10.4.9 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AVIC Xinhang

- 11.2 Calsonic Kansei

- 11.3 Chaoli Hi-Tech

- 11.4 Delphi Technologies

- 11.5 Denso

- 11.6 Fawer

- 11.7 Hanon Systems

- 11.8 Keihin

- 11.9 Koyorad

- 11.10 LUZHOU North Chemical Industries

- 11.11 MAHLE

- 11.12 Mitsubishi Electric

- 11.13 Modine Manufacturing Company

- 11.14 Nissens Automotive A/S

- 11.15 Pranav Vikas

- 11.16 Sanden Holdings

- 11.17 Tata AutoComp Systems

- 11.18 Transpro

- 11.19 Valeo

- 11.20 Zhejiang Yinlun Machinery