採尿デバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Urine Collection Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 145 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797744

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

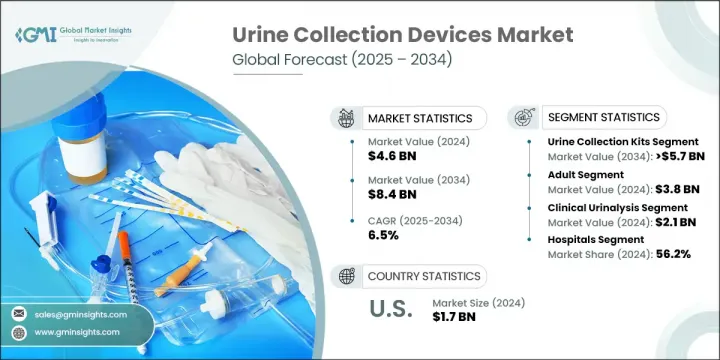

採尿デバイスの世界市場は、2024年には46億米ドルと評価され、CAGR 6.5%で成長し、2034年には84億米ドルに達すると予測されています。

市場の拡大は、慢性腎臓病、尿路感染症、失禁を抱える高齢化社会の負担増に強く支えられています。在宅ヘルスケアへのシフト、ポイントオブケア診断の成長、機器の機能とデザインにおける継続的な技術革新が、引き続き市場動向を形成しています。採尿デバイスは、安全で無菌かつ正確なサンプルの採取、輸送、保管を可能にすることで、診断において重要な役割を果たしています。これらのツールは、コップや検体バッグから、採取キットや輸送容器に至るまで、病院、診療所、検査室、在宅環境において幅広く使用されています。特に慢性期医療や代謝診断における疾患スクリーニングの頻度の増加が、これらのサービスに対する持続的な需要を牽引しています。医療の分散化が顕著になり、患者中心のケアモデルが進化するにつれ、使いやすく衛生的で信頼性の高い採尿システムへの関心が高まっています。こうした市場力学は、企業が生産規模を拡大する一方で、サンプルの取り扱いと診断精度を高める技術に投資するのに役立っています。

腎臓学、腫瘍学、内分泌学などの分野で臨床試験の数が増加していることから、ゲノム、プロテオミクス、バイオマーカー検査に対応した高度な採尿ソリューションに対する需要が高まっています。研究者は、輸送中や分析中にサンプルの完全性を維持する無菌で化学的に安定した容器をますます必要としています。その結果、サプライヤーは研究室での研究に合わせたより専門的なキットを開発し、より広範な臨床研究のエコシステムをサポートしています。さらに、移動が困難な患者や慢性疾患の患者に対する在宅医療の拡大により、従来の臨床現場以外での採尿用品の使用が拡大しています。この移行は、携帯性、安全性、使いやすさに焦点を当てた製品設計の進化に寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 46億米ドル |

| 予測金額 | 84億米ドル |

| CAGR | 6.5% |

採尿キットセグメントは2024年に69.4%のシェアを占めました。この強い地位は主に、家庭用診断キットへの依存の高まり、分散型臨床試験の成長、無菌で安全な検体取り扱いの重要性の高まりによるものです。これらのキットは、臨床施設外のユーザーにも利便性とアクセシビリティを提供し、診断コンプライアンスとケアの継続性の向上に役立ちます。採尿キットの高い採用率は、慢性疾患のモニタリング、生殖医療、薬物検査などの用途で見られます。

臨床尿検査アプリケーション分野は、2024年に21億米ドルを生み出し、2025年から2034年にかけてCAGR 6.1%で成長すると予測されています。尿検査は、尿路結石や糖尿病から腎臓病や代謝性疾患に至るまで、幅広い疾患を特定するための最前線の診断ツールであり続けているため、このセグメントは市場をリードしています。病院と診断センターが主なエンドユーザーであり、正確な検査結果を維持するために化学的に安定し、汚染に強い装置に依存しています。定期的な健康診断と慢性疾患診断の増加により、尿検査は予防医療と急性期医療の要として確固たる地位を築いています。

欧州採尿デバイス市場は2024年に13億米ドルに達しました。同地域は高度に発達したヘルスケアインフラと非侵襲的検査法の広範な採用がメリット。一人当たり医療費の高さと幅広い公的スクリーニングプログラムが、病院と在宅の両方で尿検査の需要を加速させています。西欧とスカンジナビア諸国では、高齢者集団の慢性泌尿器疾患の管理に重点が置かれているため、特に高い使用率を示しています。

採尿デバイスの世界市場に参入している主な企業は、BioTouch、QIAGEN、Ardo Medical、Thermo Fisher Scientific、Roche、Abbott、POLYMED、Aspen Surgical、Cardinal Health、HENSO、Convatec、Becton, Dickinson and Company、Labcorp(Litholink)、MEDLINE、ANGIPLASTなどです。採尿デバイス市場で競合する企業は、製品イノベーション、戦略的パートナーシップ、世界展開を活用して足場を固めています。中核となるのは、最新の臨床および在宅ケアのワークフローに沿った、ユーザー中心の無菌使い捨てキットの開発です。多くの企業は、進化する診断基準を満たすため、改ざん防止機能やサンプル保存機能を備えたスマート・パッケージング・ソリューションに投資しています。ヘルスケアプロバイダーや検査室との共同開発により、特定の検査用途に合わせた目的主導型製品の共同開発が可能になっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性腎臓病(CKD)の有病率の増加

- 高齢化人口の増加

- 非侵襲性診断ツールの需要の高まり

- 採尿デバイスにおける技術の進歩

- 業界の潜在的リスク&課題

- 汚染やサンプル取り扱いエラーのリスク

- 市場機会

- 尿を用いた液体生検とゲノム検査の利用増加

- 小児に優しくスマートな開発採尿デバイス

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 現在の技術動向

- 新興技術

- 価格分析、2024

- ギャップ分析

- ポーター分析

- PESTEL分析

- 将来の市場動向

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品タイプの発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 尿採取キット

- 尿検体バッグ

- 尿カップと容器

第6章 市場推計・予測:患者別、2021年~2034年

- 主要動向

- 成人

- 小児

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 臨床尿検査

- 尿路感染症(UTI)

- 腎臓疾患

- その他の臨床尿検査

- 薬物検査

- 妊娠検査

- 臨床調査と調査

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 診断ラボ

- 在宅ケア環境

- その他の用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Abbott

- ANGIPLAST

- Ardo Medical

- Aspen Surgical

- Becton, Dickinson and Company

- BioTouch

- Cardinal Health

- convatec

- HENSO

- Labcorp(Litholink)

- MEDLINE

- POLYMED

- QIAGEN

- Roche

- Thermo Fisher Scientific

目次

The Global Urine Collection Devices Market was valued at USD 4.6 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 8.4 billion by 2034. Market expansion is strongly supported by the rising burden of chronic kidney diseases, urinary tract infections, and an aging population dealing with incontinence. The shift toward home-based healthcare, together with the growth in point-of-care diagnostics and ongoing innovation in device functionality and design, continues to shape market trends. Urine collection devices play a crucial role in diagnostics by enabling safe, sterile, and accurate sample gathering, transportation, and storage. These tools-ranging from cups and specimen bags to collection kits and transport containers-are extensively used across hospitals, clinics, laboratories, and at-home settings. The increased frequency of disease screening, particularly in chronic care and metabolic diagnostics, is driving sustained demand for these services. As decentralized healthcare becomes more prominent and patient-centric care models evolve, there is significant interest in user-friendly, hygienic, and reliable urine collection systems. These market dynamics are helping companies scale production while investing in technology that enhances sample handling and diagnostic precision.

The rising number of clinical investigations in fields such as nephrology, oncology, and endocrinology is pushing demand for advanced urine collection solutions that are compatible with genomic, proteomic, and biomarker testing. Researchers increasingly require sterile, chemically stable containers that preserve sample integrity during transport and analysis. As a result, suppliers are developing more specialized kits tailored to lab research, supporting the wider clinical research ecosystem. Additionally, the expansion of home-based care for patients with limited mobility or chronic illness is promoting broader use of urine collection products outside traditional clinical settings. This transition is contributing to an evolving product design landscape focused on portability, safety, and ease of use.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.6 Billion |

| Forecast Value | $8.4 Billion |

| CAGR | 6.5% |

The urine collection kits segment held a 69.4% share in 2024. This strong position is primarily due to the increasing reliance on at-home diagnostic kits, growth in decentralized clinical trials, and the rising importance of sterile and secure specimen handling. These kits offer convenience and accessibility to users outside of clinical facilities, helping improve diagnostic compliance and continuity of care. High adoption of urine collection kits is seen in applications like chronic disease monitoring, reproductive health, and drug testing.

The clinical urinalysis application segment generated USD 2.1 billion in 2024 and is projected to grow at a CAGR of 6.1% during 2025-2034. This segment leads the market because urine testing remains a frontline diagnostic tool in identifying a wide range of disorders, from UTIs and diabetes to kidney and metabolic conditions. Hospitals and diagnostic centers are the main end users, relying on chemically stable, contamination-resistant devices to maintain accurate laboratory results. The growing volume of regular health screenings and chronic condition diagnostics has solidified urinalysis as a cornerstone in preventative and acute care.

Europe Urine Collection Devices Market reached USD 1.3 billion in 2024. The region benefits from a highly developed healthcare infrastructure and widespread adoption of non-invasive testing methods. High per capita health expenditure and broad public screening programs are helping accelerate demand for urine testing in both hospitals and home-based settings. Countries in Western Europe and Scandinavia show particularly high usage due to increased focus on managing chronic urological conditions in elderly populations.

Major players operating in the Global Urine Collection Devices Market include BioTouch, QIAGEN, Ardo Medical, Thermo Fisher Scientific, Roche, Abbott, POLYMED, Aspen Surgical, Cardinal Health, HENSO, Convatec, Becton, Dickinson and Company, Labcorp (Litholink), MEDLINE, and ANGIPLAST. Companies competing in the urine collection devices market are leveraging product innovation, strategic partnerships, and global expansion to strengthen their foothold. A core focus lies in developing user-centric, sterile, and disposable kits that align with modern clinical and home care workflows. Many firms are investing in smart packaging solutions with tamper-evidence and sample-preservation features to meet evolving diagnostic standards. Collaborations with healthcare providers and laboratories are enabling co-development of purpose-driven products tailored to specific testing applications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Patient trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic kidney diseases (CKD)

- 3.2.1.2 Growing geriatric population

- 3.2.1.3 Rising demand for non-invasive diagnostic tools

- 3.2.1.4 Technological advancements in urine collection devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of contamination and sample handling errors

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing use of urine-based liquid biopsy and genomic testing

- 3.2.3.2 Development of pediatric-friendly and smart urine collection devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America

- 4.3.6 MEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Urine collection kits

- 5.3 Urine specimen bags

- 5.4 Urine cups and containers

Chapter 6 Market Estimates and Forecast, By Patient, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Clinical urinalysis

- 7.2.1 Urinary tract infections (UTI)

- 7.2.2 Kidney disorders

- 7.2.3 Other clinical urinalysis

- 7.3 Drug screening

- 7.4 Pregnancy testing

- 7.5 Clinical research and studies

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Diagnostic laboratories

- 8.4 Home care settings

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott

- 10.2 ANGIPLAST

- 10.3 Ardo Medical

- 10.4 Aspen Surgical

- 10.5 Becton, Dickinson and Company

- 10.6 BioTouch

- 10.7 Cardinal Health

- 10.8 convatec

- 10.9 HENSO

- 10.10 Labcorp (Litholink)

- 10.11 MEDLINE

- 10.12 POLYMED

- 10.13 QIAGEN

- 10.14 Roche

- 10.15 Thermo Fisher Scientific

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 145 Pages

- 納期

- 2~3営業日