NFC(近距離無線通信)市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Near Field Communication (NFC) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797740

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

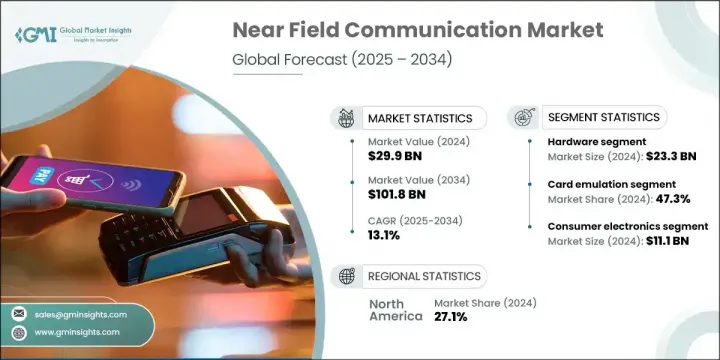

世界のNFC(近距離無線通信)市場は、2024年に299億米ドルと評価され、CAGR13.1%で成長し、2034年には1,018億米ドルに達すると推定されています。

市場成長の原動力となっているのは、多様な消費者向け電子製品にNFCが搭載されつつあることです。ウェアラブルやタブレットからラップトップやスマートテレビに至るまで、この技術は安全な認証、シームレスなコンテンツ共有、素早いデバイスペアリングのための中核的なイネーブラとなりつつあります。2024年現在、世界中で40億台以上のNFC対応装置が広く使用されていることは、消費者技術におけるNFCの強力な足場を示しています。

このレベルの普及は、タッチレス相互作用や迅速な無線通信に適した方法としてのNFCの地位を強化し続けています。メーカーがその装置の接続性とユーザーの利便性を強化し続ける中、NFCの統合はユーザー体験を形成し製品価値を促進する上で重要な役割を果たしています。需要の急増はチップ設計への投資の動機付けにもなっており、各社は様々な使用事例に合わせたコンパクトで効率的かつ安全なソリューションの提供に取り組んでいます。デジタルトランスフォーメーションの拡大と、個人と企業の両方の環境における非接触技術の急速な普及によって、業界の勢いはさらに維持されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 299億米ドル |

| 予測金額 | 1,018億米ドル |

| CAGR | 13.1% |

ハードウェア分野は2024年に233億米ドルを生み出しました。このリーダーシップは、POS端末、車載コンソール、および消費者向け機器を含む様々なプラットフォームへのNFCリーダ、チップ、およびタグの急速な統合に結びついています。このセグメントは、産業オートメーションやコネクテッドIoTのエコシステムが高速で低消費電力のワイヤレスデータ交換ツールを求めるにつれて牽引力を増しています。競争力を維持するため、企業は次世代ハードウェアの研究開発、特にチップの小型化や低エネルギー消費などの分野に資源を投入しています。この進化はまた、電子機器メーカーとの戦略的パートナーシップの道筋を作り、広範な展開をさらに支援し、機器メーカーがコンパクトな設計に高度なNFC機能を組み込むことを可能にします。

カードエミュレーション分野は2024年に47.3%のシェアを占め、デジタル決済や交通アクセスシステムの広範な利用に後押しされています。この機能を活用したデバイスは非接触カードを模倣し、消費者が日常的な取引を行うための便利で安全なインターフェースを提供します。小売、モビリティ、および金融サービスの各業界は、摩擦を減らし顧客体験を向上させるためにNFCベースのエミュレーションシステムを採用しています。ベンダーは現在、高度なトークン化、セキュアエレメントの組み込み、および簡素化された本人確認を自社のプラットフォームに統合することで、自社製品の強化に注力しています。

米国のNFC(近距離無線通信)市場は、2024年に71億米ドルと評価されました。同地域の市場成長は、モバイル機器導入の増加や、各業界におけるPOSインフラの近代化によって大きく後押しされています。小売業にとどまらず、自動車技術、ヘルスケア、交通アクセス、および安全な入館システムにおけるNFCアプリケーションが新たな成長経路を生み出しています。米国におけるNFCの多様な応用は、その柔軟性と消費者や商業環境にわたる長期的価値を証明しています。企業はこの技術をより日常的な体験に組み込んでおり、決済を超えた普及の拡大に貢献しています。

NFC(近距離無線通信)市場の主要企業には、Infineon Technologies、Broadcom Inc.、Qualcomm Technologies、NXP Semiconductorsなどがあります。主要なNFCソリューション・プロバイダーは、超低消費電力と小型化をサポートする高度なチップ設計に多額の投資を行っており、小型機器へのスムーズな統合を実現しています。各社はフィンテック企業や家電メーカーと戦略的提携を結び、モバイル決済、入退室管理、および車載用のオーダーメイドソリューションを開発しています。また、世界市場全体で様々な通信規格やセキュリティ要件に対応するためのマルチプロトコルNFCプラットフォームの開発にも注目が集まっています。ベンダーは生産能力を拡大し、アジア太平洋や欧州のような高成長地域における販売網を強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 影響要因

- 促進要因

- 非接触型決済ソリューションの採用増加

- 家電製品におけるNFC技術の拡大

- 小売業やeコマースにおけるNFCの利用増加

- ヘルスケアにおけるNFCアプリケーションの拡大

- 交通機関におけるNFCの利用増加

- 業界の潜在的リスク&課題

- 実装と統合のコストが高め

- 代替無線通信技術との競合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 新たなビジネスモデル

- コンプライアンス要件

- 消費者感情分析

- 特許および知的財産分析

- 地政学と貿易のダイナミクス

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 市場集中分析

- 主要プレーヤーの競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- デジタル変革イニシアチブ

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:提供別、2021年~2034年

- 主要動向

- ハードウェア

- NFCチップ/IC

- NFCタグ

- NFCリーダー

- アンテナとトランシーバー

- その他

- ソフトウェア

- サービス

- システム統合と展開

- コンサルティングおよびアドバイザリーサービス

- マネージドサービスとサポート

- その他

第6章 市場推計・予測:動作モード別、2021年~2034年

- 主要動向

- リーダーエミュレーション

- ピアツーピア

- カードエミュレーション

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 支払い

- アクセス制御

- ペアリングと試運転

- アイデンティティと認証

- スマートなポスターとマーケティング

- IoTのプロビジョニングと管理

- その他

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- コンシューマーエレクトロニクス

- スマートフォン

- ウェアラブル

- PCとノートパソコン

- スマートテレビとメディアデバイス

- その他

- 小売業とeコマース

- 非接触型POS端末

- スマートシェルフとインタラクティブキオスク

- 製品認証と偽造防止タグ

- クリック&コレクトとラストマイル物流

- 公共交通機関の乗車券システム

- その他

- 運輸・物流

- 駐車場および通行料金徴収システム

- 車両アクセスと車両管理

- 資産追跡

- 乗客情報とスマートサイネージ

- コールドチェーン監視

- その他

- 銀行および金融サービス

- モバイルウォレットプラットフォーム

- 安全なIDとアクセスカード

- NFC対応ATMと支店キオスク

- トークン化サービス

- その他

- ヘルスケア

- NFC対応医療機器

- 医薬品包装

- 患者エンゲージメントツール

- その他

- 自動車

- 車載デバイスのペアリング

- 機器のメンテナンスおよびサービスタグ

- テレマティクスソリューション

- その他

- 工業および製造業

- ツールおよび資産追跡システム

- 施設へのアクセスと従業員IDのセキュリティ

- 製品構成

- 倉庫と在庫の自動化

- その他

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 世界の企業

- NXP Semiconductors

- Broadcom Inc.

- Infineon Technologies

- STMicroelectronics

- Qualcomm Technologies

- 地域の企業

- 北米

- Texas Instruments

- Apple Inc.

- Google LLC

- Zebra Technologies Inc.

- Avery Dennison

- HID Global

- 欧州

- Thales Group

- ams-OSRAM

- smart-TEC GmbH & Co. KG

- アジア太平洋地域

- Samsung Electronics

- Sony Corporation

- Renesas Electronics

- 北米

- ニッチ企業/ディスラプター

- Identiv

- MagTek

- Tageos

- Pragmatic Semiconductor

目次

The Global Near Field Communication Market was valued at USD 29.9 billion in 2024 and is estimated to grow at a CAGR of 13.1% to reach USD 101.8 billion by 2034. Market growth is being fueled by the increasing incorporation of NFC across a diverse range of consumer electronic products. From wearables and tablets to laptops and smart televisions, the technology is becoming a core enabler for secure authentication, seamless content sharing, and fast device pairing. The widespread use of over 4 billion NFC-enabled devices worldwide as of 2024 illustrates its strong foothold in consumer technology.

This level of adoption continues to reinforce NFC's position as the preferred method for touchless interaction and quick wireless communication. As manufacturers continue to enhance the connectivity and user convenience of their devices, NFC integration plays a critical role in shaping user experience and driving product value. The demand surge is also motivating investments in chip design, with companies working to deliver compact, efficient, and secure solutions tailored to different use cases. Industry momentum is further sustained by growing digital transformation and the rapid proliferation of contactless technologies in both personal and enterprise environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $29.9 Billion |

| Forecast Value | $101.8 Billion |

| CAGR | 13.1% |

The hardware segment generated USD 23.3 billion in 2024. This leadership is tied to the rapid integration of NFC readers, chips, and tags into a growing spectrum of platforms, including point-of-sale terminals, automotive consoles, and consumer devices. The segment is gaining traction as industrial automation and connected IoT ecosystems seek fast, low-power, wireless data exchange tools. To stay competitive, businesses are channeling resources into next-gen hardware R&D, particularly in areas like chip miniaturization and low energy consumption. This evolution also creates avenues for strategic partnerships with electronics makers, further supporting widespread deployment and enabling device manufacturers to embed advanced NFC features into compact designs.

The card emulation segment held a 47.3% share in 2024, fueled by widespread use of digital payments and transit access systems. Devices leveraging this functionality mimic contactless cards, offering a convenient and secure interface for consumers to carry out everyday transactions. Industries across retail, mobility, and financial services are adopting NFC-based emulation systems to reduce friction and improve customer experience. Vendors are now focusing on strengthening their offerings by integrating advanced tokenization, embedded secure elements, and simplified identity verification into their platforms.

United States Near Field Communication (NFC) Market was valued at USD 7.1 billion in 2024. Market growth in the region is largely propelled by the uptick in mobile device adoption and the modernization of POS infrastructure across industries. Beyond retail, NFC applications in automotive technology, healthcare, transit access, and secure entry systems are creating new growth paths. The diverse application of NFC in the U.S. proves its flexibility and long-term value across consumer and commercial settings. Businesses are integrating this technology into more everyday experiences, helping scale adoption beyond payments.

Prominent players in the Near Field Communication (NFC) Market include Infineon Technologies, Broadcom Inc., Qualcomm Technologies, and NXP Semiconductors. Major NFC solution providers are heavily investing in advanced chip design that supports ultra-low power consumption and smaller form factors, ensuring smooth integration into compact devices. Companies are forming strategic alliances with fintech firms and consumer electronics manufacturers to develop tailor-made solutions for mobile payments, access control, and automotive use. A growing focus is also on developing multi-protocol NFC platforms to handle various communication standards and security requirements across global markets. Vendors are expanding production capabilities and enhancing distribution networks in high-growth regions like Asia Pacific and Europe.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Offering trends

- 2.2.2 Operating mode trends

- 2.2.3 Application trends

- 2.2.4 End use industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of contactless payment solutions

- 3.2.1.2 Expansion of NFC technology in consumer electronics

- 3.2.1.3 Increasing use of NFC in retail and e-commerce

- 3.2.1.4 Expansion of NFC applications in healthcare

- 3.2.1.5 Increasing use of NFC in transportation

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High implementation and integration costs

- 3.2.2.2 Competition from alternative wireless communication technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Consumer sentiment analysis

- 3.11 Patent and IP analysis

- 3.12 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital Transformation Initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates & Forecast, By Offering, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 NFC chips / ICs

- 5.2.2 NFC tags

- 5.2.3 NFC readers

- 5.2.4 Antennas & transceivers

- 5.2.5 Others

- 5.3 Software

- 5.4 Services

- 5.4.1 System integration & deployment

- 5.4.2 Consulting & advisory services

- 5.4.3 Managed services & support

- 5.4.4 Others

Chapter 6 Market Estimates & Forecast, By Operating Mode, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Reader emulation

- 6.3 Peer-to-peer

- 6.4 Card emulation

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 Payments

- 7.3 Access control

- 7.4 Pairing and commissioning

- 7.5 Identity and authentication

- 7.6 Smart posters and marketing

- 7.7 IoT provisioning and management

- 7.8 Other

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Consumer electronics

- 8.2.1 Smartphones

- 8.2.2 Wearables

- 8.2.3 PCs and laptops

- 8.2.4 Smart TVs and media devices

- 8.2.5 Others

- 8.3 Retail and e-commerce

- 8.3.1 Contactless POS terminals

- 8.3.2 Smart shelves and interactive kiosks

- 8.3.3 Product authentication and anti-counterfeit tags

- 8.3.4 Click and collect and last-mile logistics

- 8.3.5 Public transit ticketing systems

- 8.3.6 Others

- 8.4 Transportation and logistics

- 8.4.1 Parking and toll collection systems

- 8.4.2 Vehicle access and fleet management

- 8.4.3 Asset tracking

- 8.4.4 Passenger information and smart signage

- 8.4.5 Cold chain monitoring

- 8.4.6 Others

- 8.5 Banking and financial services

- 8.5.1 Mobile wallet platforms

- 8.5.2 Secure ID and access cards

- 8.5.3 NFC-enabled ATMs and branch kiosks

- 8.5.4 Tokenization services

- 8.5.5 Others

- 8.6 Healthcare

- 8.6.1 NFC-enabled medical devices

- 8.6.2 Pharmaceutical packaging

- 8.6.3 Patient engagement tools

- 8.6.4 Others

- 8.7 Automotive

- 8.7.1 In-vehicle device pairing

- 8.7.2 Equipment maintenance and service tags

- 8.7.3 Telematics solutions

- 8.7.4 Others

- 8.8 Industrial and manufacturing

- 8.8.1 Tool and asset tracking systems

- 8.8.2 Secure facility access and employee IDs

- 8.8.3 Product configuration

- 8.8.4 Warehouse and inventory automation

- 8.8.5 Others

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 NXP Semiconductors

- 10.1.2 Broadcom Inc.

- 10.1.3 Infineon Technologies

- 10.1.4 STMicroelectronics

- 10.1.5 Qualcomm Technologies

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 Texas Instruments

- 10.2.1.2 Apple Inc.

- 10.2.1.3 Google LLC

- 10.2.1.4 Zebra Technologies Inc.

- 10.2.1.5 Avery Dennison

- 10.2.1.6 HID Global

- 10.2.2 Europe

- 10.2.2.1 Thales Group

- 10.2.2.2 ams-OSRAM

- 10.2.2.3 smart-TEC GmbH & Co. KG

- 10.2.3 Asia Pacific

- 10.2.3.1 Samsung Electronics

- 10.2.3.2 Sony Corporation

- 10.2.3.3 Renesas Electronics

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Identiv

- 10.3.2 MagTek

- 10.3.3 Tageos

- 10.3.4 Pragmatic Semiconductor

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日