建設スケール3Dプリンティング用ポリマーフィラメントの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Polymer Filaments for Construction-Scale 3D Printing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797708

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

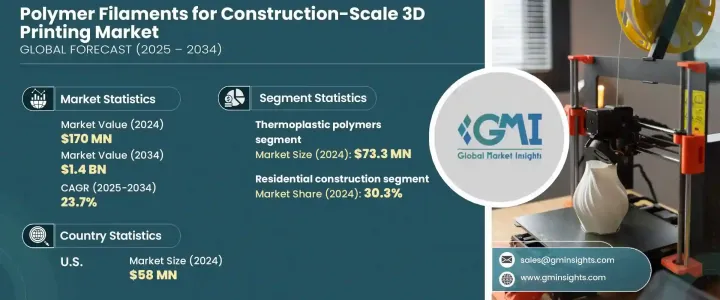

世界の建設スケール3Dプリンティング用ポリマーフィラメント市場は、2024年には1億7,000万米ドルと評価され、CAGR23.7%で成長し、2034年までには14億米ドルに達すると推定されています。

この急成長の背景には、革新的で持続可能な建築方法に対する需要の増加があります。ABS、PLA、PETなどのエンジニアリング熱可塑性プラスチックは、構造部品から建物全体まで、大判の積層造形用途に最適化されつつあります。3Dプリンティングの多用途性により、建築家やエンジニアは、従来の方法では対応できない軽量で複雑な構造を作成できます。この能力により、先端ポリマーフィラメントの急速な採用が促進されています。

政府が支援するインフラ開発イニシアチブと持続可能性基準が、この技術への関心を加速させています。また、3Dプリンティングの自動化機能により、材料の無駄や手作業が削減され、建設におけるコスト効率の高いソリューションになります。世界的にスマートインフラが重視されており、特にアジア太平洋の急速に都市化している地域では、インド、中国、日本などの国々が、建築および開発プロジェクトに高性能3Dプリント材料を採用するリーダー的存在となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 1億7,000万米ドル |

| 予測金額 | 14億米ドル |

| CAGR | 23.7% |

2024年の住宅建設セグメントのシェアは30.3%を占めました。この用途は、住宅不足と値ごろ感に対処する役割を果たすとして支持を集めています。ポリマーフィラメントを使用することで、コンポーネントを迅速に製造することができ、建設スケジュールと人件費の両方を削減することができます。また、この素材はリフォームやモジュール建築にも対応しており、市場のニーズに即応した幅広い住宅ソリューションに理想的です。

大規模溶融積層造形(FDM)技術分野は、その操作の簡便さと比較的低いセットアップコストにより、2024年に注目すべきシェアを占めました。そのスケーラブルな性質により、基礎的な部品から本格的な住宅や商業ビルまで、さまざまなレベルの建設に理想的なソリューションとなっています。押出成形ベースの設備は入手しやすいため、その普及と性能の信頼性に貢献しています。

米国の建設スケール3Dプリンティング用ポリマーフィラメント市場は2024年に5,800万米ドルの規模を生み出しました。この強力な市場プレゼンスは、強固なイノベーションエコシステム、研究開発努力の増加、持続可能な建設手法への需要によってもたらされています。米国の企業は、環境とコスト効率の目標に沿いながら、大規模建築の技術的ニーズを満たす先端フィラメント材料の開発を加速させています。この焦点は、この分野における米国のリーダーシップを強化し続けています。

建設スケール3Dプリンティング用ポリマーフィラメント市場の主要企業には、Coex 3D、Arkema、BASF SE、Sika AG、Skanska AB、Covestro、MudBots、Mighty Buildings、Tvasta Manufacturing Solutions、Manlon Polymersなどがあります。建設スケール3Dプリンティング用ポリマーフィラメント市場の各社は、建設部門の進化するニーズに対応するため、高性能、リサイクル可能、気候変動に強い材料の開発に注力しています。研究開発への投資は、フィラメント組成物の強度、耐久性、耐熱性の向上に役立っています。多くのメーカーが建設技術企業や学術機関と協力関係を結び、技術革新と商業化への準備を加速させています。また、世界的な流通と現地生産能力の開発により、企業は急速に発展する地域のインフラプロジェクトに対応することができます。戦略的合併や技術ライセンシングは、独自の付加製造プラットフォームへのアクセスを得るために利用されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 成長促進要因

- 業界の潜在的リスク・課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 素材タイプ別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)

(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:材質別、2021年~2034年

- 主要動向

- 熱可塑性ポリマー

- PLA(ポリ乳酸)とバイオベースの熱可塑性プラスチック

- ABS(アクリロニトリルブタジエンスチレン)・エンジニアリングプラスチック

- PETG(ポリエチレンテレフタレートグリコール)・特殊ポリマー

- 高性能エンジニアリングプラスチック(PEEK、PEI、PEKK)

- 繊維強化複合材料

- 炭素繊維強化ポリマー(CFRP)

- ガラス繊維強化ポリマー(GFRP)

- 天然繊維強化複合材料

- 常用繊維強化システム

- 持続可能なバイオベースの素材

- バイオベースポリマー配合

- リサイクル素材と使用済み素材

- 生分解性・堆肥化可能なポリマー

- 廃棄物由来・循環型経済材料

- 特殊機能材料

- 耐火性・難燃性ポリマー

- 断熱材・省エネ材料

- 導電性・スマート材料システム

- 多機能・ハイブリッド材料ソリューション

- 新興・先端材料

- ナノ複合材料と高性能材料

- 形状記憶・応答性ポリマーシステム

- 自己修復・適応型材料技術

- 生体模倣と自然に着想を得た材料ソリューション

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 住宅建設

- 商業建設

- インフラと土木工学

- 建築・装飾要素

- 特殊用途・ニッチ用途

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 大規模熱溶解積層法(FDM)

- ロボット建設システム

- 常用製造技術

- 新興技術と先進技術

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 建設会社・ゼネコン

- 建築家・デザイン専門家

- 不動産開発業者・建物所有者

- 調査教育機関

- 政府・公共部門

第9章 市場推計・予測:設備規模別、2021年~2034年

- 主要動向

- 大規模産業システム

- 中規模産業システム

- コンパクト・ポータブルシステム

- ハイブリッド・マルチテクノロジーシステム

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第11章 企業プロファイル

- Arkema

- BASF SE

- Coex 3D

- Covestro

- Manlon Polymers

- Mighty Buildings

- MudBots

- Sika AG

- Skanska AB

- Tvasta Manufacturing Solutions

目次

The Global Polymer Filaments for Construction-Scale 3D Printing Market was valued at USD 170 million in 2024 and is estimated to grow at a CAGR of 23.7% to reach USD 1.4 billion by 2034. This rapid growth is driven by the increasing demand for innovative and sustainable building methods. Engineered thermoplastics such as ABS, PLA, and PET are being optimized for large-format additive manufacturing applications, from structural parts to entire buildings. The versatility of 3D printing enables architects and engineers to create lightweight, complex structures that traditional methods cannot support. This capability is fostering rapid adoption of advanced polymer filaments.

Government-backed infrastructure development initiatives and sustainability standards are accelerating interest in this technology. The automation capabilities of 3D printing also reduce material waste and manual labor, making it a more cost-efficient solution for construction. Global emphasis on smart infrastructure, especially across rapidly urbanizing regions in Asia-Pacific, is positioning countries like India, China, and Japan as leaders in the adoption of high-performance 3D printing materials for building and development projects.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $170 million |

| Forecast Value | $1.4 billion |

| CAGR | 23.7% |

The residential construction segment held a 30.3% share in 2024. This application is gaining traction for its role in addressing housing shortages and affordability. Using polymer filaments, components can be produced quickly, cutting down both construction timelines and labor costs. These materials also support renovation and modular builds, making them ideal for a wide range of housing solutions that respond to immediate market needs.

The large-scale fused deposition modeling (FDM) technology segment held a notable share in 2024 due to its operational simplicity and relatively low setup costs. Its scalable nature makes it an ideal solution for different levels of construction - from foundational components to full-scale residential or commercial buildings. The accessibility of extrusion-based equipment has contributed to its widespread adoption and performance reliability.

U.S. Polymer Filaments for Construction-Scale 3D Printing Market generated USD 58 million in 2024. This strong market presence is driven by a robust innovation ecosystem, increasing R&D efforts, and the demand for sustainable construction methods. Companies in the U.S. are accelerating development of advanced filament materials that meet the technical needs of large-scale construction while aligning with environmental and cost-efficiency objectives. This focus continues to strengthen the country's leadership in the sector.

Key players in Polymer Filaments for Construction-Scale 3D Printing Market include Coex 3D, Arkema, BASF SE, Sika AG, Skanska AB, Covestro, MudBots, Mighty Buildings, Tvasta Manufacturing Solutions, and Manlon Polymers. Companies in the polymer filaments for construction-scale 3D printing market are focusing on developing high-performance, recyclable, and climate-resilient materials to meet the evolving needs of the construction sector. Investments in R&D help improve the strength, durability, and thermal resistance of filament compositions. Many manufacturers are forming collaborations with construction tech firms and academic institutions to speed up innovation and commercial readiness. Expanding global distribution and localized production capabilities also allows companies to serve infrastructure projects in fast-developing regions. Strategic mergers and technology licensing are used to gain access to proprietary additive manufacturing platforms.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Application trends

- 2.2.3 Technology trends

- 2.2.4 End use trends

- 2.2.5 Equipment scale trends

- 2.2.6 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By material type

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021-2034 (USD Million) (Units)

- 5.1 Key trends

- 5.2 Thermoplastic polymers

- 5.2.1 PLA (polylactic acid) and bio-based thermoplastics

- 5.2.2 ABS (acrylonitrile butadiene styrene) and engineering plastics

- 5.2.3 PETG (polyethylene terephthalate glycol) and specialty polymers

- 5.2.4 High-performance engineering plastics (PEEK, PEI, PEKK)

- 5.3 Fiber-reinforced composites

- 5.3.1 Carbon fiber reinforced polymers (CFRP)

- 5.3.2 Glass fiber reinforced polymers (GFRP)

- 5.3.3 Natural fiber reinforced composites

- 5.3.4 Continuous fiber reinforcement systems

- 5.4 Sustainable and bio-based materials

- 5.4.1 Bio-based polymer formulations

- 5.4.2 Recycled content and post-consumer materials

- 5.4.3 Biodegradable and compostable polymers

- 5.4.4 Waste-derived and circular economy materials

- 5.5 Specialty and functional materials

- 5.5.1 Fire-resistant and flame-retardant polymers

- 5.5.2 Thermal insulation and energy-efficient materials

- 5.5.3 Conductive and smart material systems

- 5.5.4 Multi-functional and hybrid material solutions

- 5.6 Emerging and advanced materials

- 5.6.1 Nanocomposite and enhanced performance materials

- 5.6.2 Shape memory and responsive polymer systems

- 5.6.3 Self-healing and adaptive material technologies

- 5.6.4 Biomimetic and nature-inspired material solutions

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Units)

- 6.1 Key trends

- 6.2 Residential construction

- 6.3 Commercial construction

- 6.4 Infrastructure and civil engineering

- 6.5 Architectural and decorative elements

- 6.6 Specialty and niche applications

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 (USD Million) (Units)

- 7.1 Key trends

- 7.2 Large-scale fused deposition modelling (FDM)

- 7.3 Robotic construction systems

- 7.4 Continuous manufacturing technologies

- 7.5 Emerging and advanced technologies

Chapter 8 Market Estimates and Forecast, By End Use, 2021-2034 (USD Million) (Units)

- 8.1 Key trends

- 8.2 Construction companies and general contractors

- 8.3 Architects and design professionals

- 8.4 Real estate developers and building owners

- 8.5 Research and educational institutions

- 8.6 Government and public sector

Chapter 9 Market Estimates and Forecast, By Equipment Scale, 2021-2034 (USD Million) (Units)

- 9.1 Key trends

- 9.2 Large-scale industrial systems

- 9.3 Medium- scale industrial systems

- 9.4 Compact and portable systems

- 9.5 Hybrid and multi-technology systems

Chapter 10 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Arkema

- 11.2 BASF SE

- 11.3 Coex 3D

- 11.4 Covestro

- 11.5 Manlon Polymers

- 11.6 Mighty Buildings

- 11.7 MudBots

- 11.8 Sika AG

- 11.9 Skanska AB

- 11.10 Tvasta Manufacturing Solutions

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日