|

市場調査レポート

商品コード

1797706

光ファイバーコンポーネント市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Fiber Optic Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 光ファイバーコンポーネント市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年07月31日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

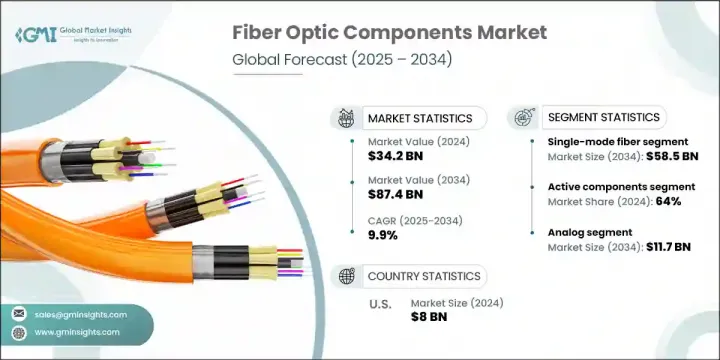

光ファイバーコンポーネントの世界市場規模は、2024年に342億米ドルとなり、CAGR 9.9%で成長し、2034年には874億米ドルに達すると予測されています。

この堅調な成長は、主にクラウドコンピューティング、エッジインフラ、ハイパースケールデータセンターの拡大により、高速データ伝送のニーズが高まっていることが背景にあります。産業用および都市用アプリケーションにおけるIoT技術とコネクテッド・エコシステムの統合の高まりは、需要をさらに強化しています。産業が近代化し、デジタル化へとシフトするにつれて、高速で信頼性の高い通信インフラへのニーズが、いくつかのセクターで光ファイバーの採用を促進しています。ブロードバンド展開、スマートグリッド、デジタルサービスへの政府投資は、特に新興経済諸国において、世界的に光ファイバーコンポーネントの市場浸透を加速させています。ファイバーインフラの役割は、データ集約的で遅延の影響を受けやすい環境において、高性能な接続性を実現する上で不可欠なものとなっています。

5Gの展開は、特にネットワークフロントホールとバックホールセグメントにおいて、光ファイバーコンポーネントの必要性を著しく高めています。電気通信事業者は、低遅延、広帯域幅の要件を満たすためにインフラを急速に拡張しています。光ファイバーベースの接続性は、スマートシティのフレームワークにも不可欠であり、IoT、監視、デジタルサービスプラットフォームに電力を供給します。このような変化により、シームレスな通信と弾力性のあるパフォーマンスを提供できるコンポーネントの市場が拡大しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 342億米ドル |

| 予測金額 | 874億米ドル |

| CAGR | 9.9% |

2024年、アクティブコンポーネントセグメントは、光ファイバーコンポーネント市場で64%のトップシェアを占めました。5Gネットワーク、データセンタ、メトロ光インフラにおけるトランシーバ、アンプ、変調器の大量導入が、このセグメントを推進し続けています。システムがポート密度を高め、光レイヤ全体の消費電力を削減する方向に向かうにつれて、コンパクトでエネルギー効率の高い設計への要求が高まっています。

シングルモードファイバオプティクスセグメントは、2034年には585億米ドルになると予測されています。長距離伝送における優位性、減衰の少なさ、メトロやコアネットワークアプリケーションでの使用の増加が、その関連性を確固たるものにしています。海底通信システムと5Gバックホールインフラの拡大は、特にデータ消費パターンが高スループットでクラウドネイティブなアプリケーションにシフトする中で、このセグメントの勢いに大きく寄与しています。

2024年の米国の光ファイバーコンポーネント市場規模は80億米ドル。AI主導のワークロードの成長、クラウドへの急速な移行、次世代データセンターの拡大が、高度なファイバーソリューションの需要を促進しています。国内サプライヤは、進化するパフォーマンス要件に対応するために、熱効率とクロスプラットフォーム相互運用性に優れた低レイテンシ、大容量光コンポーネントの開発に注力しています。

光ファイバーコンポーネント市場に参入している企業には、フジクラ、Broadex Technologies、Ciena、Cisco Systems、古河電工、Accelink Technologies、Corning、3M、Broadcom、Amphenol、CommScopeなどがあります。光ファイバーコンポーネント市場におけるプレゼンスを強化するため、主要企業は多方面にわたる戦略を採用しています。主要企業は、AI、クラウド、5Gインフラに合わせたコンパクト、エネルギー効率、高速光技術を提供するためにR&D投資を優先しています。通信事業者やハイパースケーラとのパートナーシップは、製品イノベーションを展開ニーズに合わせるのに役立ちます。製造能力を拡大し、地域のサプライチェーンを強化することで、より迅速な納品サイクルを可能にし、地方自治体のデジタル化プログラムをサポートします。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- IoTとコネクテッドデバイスの普及拡大

- 5Gインフラの世界の拡大

- データセンターとクラウドコンピューティングサービスの成長

- スマートシティとスマートグリッドの普及

- 軍事および航空宇宙用途からの需要の増加

- 業界の潜在的リスク&課題

- 初期導入および設置コストが高め

- ネットワークインフラストラクチャ管理の複雑さ

- 市場機会

- 新興経済諸国における新たな需要

- 5G以降の技術における光ファイバーの統合

- 高帯域幅アプリケーション(AR/VR、ストリーミング、AI)の需要の高まり

- 防衛・航空宇宙分野における光ファイバーの採用

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 特許および知的財産分析

- 地政学と貿易のダイナミクス

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 主要プレーヤーの競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:コンポーネントタイプ別、2021年~2034年

- 主要動向

- 能動部品

- 送信機

- 受信機

- 光増幅器

- 受動部品

- 光ファイバーケーブル

- コネクタとアダプタ

- カプラとスプリッタ

- 光スイッチ

- その他

第6章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- シングルモードファイバー

- マルチモードファイバー

第7章 市場推計・予測:データ転送速度別、2021年~2034年

- 主要動向

- 10 GBPS未満

- 10~40 GBPS

- 40~100 GBPS

- 100 GBPS以上

第8章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- アナログ光ファイバーコンポーネント

- デジタル光ファイバーコンポーネント

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 電気通信およびデータ通信

- 長距離伝送ネットワーク

- メトロ/コアネットワーク

- アクセスネットワーク

- モバイルバックホール/フロントホール

- エンタープライズネットワーク(LAN/WAN)

- その他

- データセンターとクラウドインフラストラクチャ

- データセンター内接続

- データセンター間

- 高速トランシーバー

- ストレージエリアネットワーク(SAN)

- その他

- 軍事・防衛

- 安全な戦術通信ネットワーク

- レーダーおよびセンサーシステム

- 指揮統制システム

- 航空電子機器および海軍通信システム

- その他

- 医療とヘルスケア

- 医療画像システム

- レーザー送達システム

- 生体医学センサーと計測機器

- 病院ネットワークインフラ

- その他

- 産業オートメーション

- 工場自動化およびプロセス制御ネットワーク

- ロボット工学とマシンビジョンシステム

- リモートセンシングとモニタリング

- 産業用イーサネット

- その他

- 放送およびビデオ伝送

- ライブイベント放送インフラ

- スタジオから送信機へのリンク(STL)

- ケーブルテレビとIPTV配信ネットワーク

- 屋外放送(OB)バンとモバイル制作

- その他

- 石油・ガス

- ダウンホール光ファイバーセンシング

- 海底通信リンク

- パイプライン監視および漏れ検出システム

- リモートサイト接続

- その他

- 航空宇宙

- 航空電子データネットワーク

- 衛星地上局の接続

- 機内エンターテイメント(IFE)システム

- 宇宙船の光通信システム

- その他

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- 世界の主要企業

- Broadcom

- Cisco Systems

- Corning

- Fujikura

- Huawei Technologies

- 地域の主要企業

- 北米

- Ciena

- CommScope

- Lumentum Holdings

- Viavi Solutions

- TE Connectivity

- 欧州

- Amphenol

- Molex

- Prysmian Group

- アジア太平洋地域

- Furukawa Electric

- Sumitomo Electric

- ZTE

- 北米

- ニッチプレーヤー/ディスラプター

- 3Ms

- Accelink Technologies

- Broadex Technologies

- Luxshare-ICT

- Optosun Technology

- Senko

The Global Fiber Optic Components Market was valued at USD 34.2 billion in 2024 and is estimated to grow at a CAGR of 9.9% to reach USD 87.4 billion by 2034. This robust growth is primarily driven by the increasing need for high-speed data transmission, fueled by the expansion of cloud computing, edge infrastructure, and hyperscale data centers. The rising integration of IoT technologies and connected ecosystems across industrial and urban applications is further strengthening demand. As industries modernize and shift towards digitalization, the need for fast, reliable communication infrastructure is driving the adoption of fiber optics across several sectors. Government investments in broadband rollout, smart grids, and digital services-especially in developing economies-are accelerating market penetration of fiber optic components globally. The role of fiber infrastructure has become essential in enabling high-performance connectivity across data-intensive and latency-sensitive environments.

The rollout of 5G is significantly increasing the need for fiber optic components, particularly in network fronthaul and backhaul segments. Telecom providers are rapidly scaling their infrastructure to meet low-latency, high-bandwidth requirements. Fiber-based connectivity is also critical for smart city frameworks, powering IoT, surveillance, and digital service platforms. These changes are pushing the market for components capable of delivering seamless communication and resilient performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $34.2 Billion |

| Forecast Value | $87.4 Billion |

| CAGR | 9.9% |

In 2024, the active components segment held the leading share of 64% in the fiber optic components market. High-volume deployment of transceivers, amplifiers, and modulators in 5G networks, data centers, and metro optical infrastructure continues to propel this segment. The demand for compact, energy-efficient designs is increasing as systems move toward higher port densities and reduced power consumption across optical layers.

The single-mode fiber optics segment is anticipated to generate USD 58.5 billion by 2034. Their advantage in long-range transmission, lower attenuation, and increasing use in metro and core network applications solidifies their relevance. The expansion of submarine communication systems and 5G backhaul infrastructure has significantly contributed to this segment's momentum, particularly as data consumption patterns shift toward high-throughput, cloud-native applications.

U.S. Fiber Optic Components Market was valued at USD 8 billion in 2024. Growth in AI-driven workloads, rapid migration to the cloud, and expansion of next-gen data centers are fueling demand for advanced fiber solutions. Domestic suppliers are focusing on developing low-latency, high-capacity optical components with better thermal efficiency and cross-platform interoperability to meet evolving performance requirements.

Companies operating in the Fiber Optic Components Market include Fujikura, Broadex Technologies, Ciena, Cisco Systems, Furukawa Electric, Accelink Technologies, Corning, 3M, Broadcom, Amphenol, and CommScope. To strengthen their presence in the Fiber Optic Components Market, key players are embracing a multi-pronged strategy. Leading companies are prioritizing R&D investments to deliver compact, energy-efficient, and high-speed optical technologies tailored for AI, cloud, and 5G infrastructure. Partnerships with telecom operators and hyperscalers help align product innovation with deployment needs. Expanding manufacturing capabilities and strengthening regional supply chains enable faster delivery cycles and support local government digitalization programs.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Component type trends

- 2.2.2 Type trends

- 2.2.3 Data transfer rate trends

- 2.2.4 Technology trends

- 2.2.5 Application trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing penetration of IoT and connected devices

- 3.2.1.2 Expansion of 5G infrastructure globally

- 3.2.1.3 Growth in data centers and cloud computing services

- 3.2.1.4 Proliferation of smart cities and smart grids

- 3.2.1.5 Growing demand from military and aerospace applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial deployment and installation costs

- 3.2.2.2 Complexity in network infrastructure management

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging demand in developing economies

- 3.2.3.2 Integration of fiber optics in 5g and beyond technologies

- 3.2.3.3 Growing need for high-bandwidth applications (AR/VR, streaming, AI)

- 3.2.3.4 Adoption of fiber optics in defense and aerospace sectors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component Type, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Active components

- 5.2.1 Transmitters

- 5.2.2 Receivers

- 5.2.3 Optical amplifiers

- 5.3 Passive components

- 5.3.1 Fiber optic cables

- 5.3.2 Connectors & adapters

- 5.3.3 Couplers & splitters

- 5.3.4 Optical switches

- 5.3.5 Others

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Single-mode fiber

- 6.3 Multi-mode fiber

Chapter 7 Market Estimates and Forecast, By Data Transfer Rate, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Less than 10 GBPS

- 7.3 10 to 40 GBPS

- 7.4 40 to 100 GBPS

- 7.5 More than 100 GBPS

Chapter 8 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 Analog fiber optic components

- 8.3 Digital fiber optic components

Chapter 9 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion)

- 9.1 Key trends

- 9.2 Telecommunications & data communication

- 9.2.1 Long-haul transmission networks

- 9.2.2 Metro/core networks

- 9.2.3 Access networks

- 9.2.4 Mobile backhaul / fronthaul

- 9.2.5 Enterprise networks (LAN/WAN)

- 9.2.6 Others

- 9.3 Data centers & cloud infrastructure

- 9.3.1 Intra-data center connectivity

- 9.3.2 Inter-data center

- 9.3.3 High-speed transceivers

- 9.3.4 Storage area networks (SAN)

- 9.3.5 Others

- 9.4 Military & defense

- 9.4.1 Secure tactical communication networks

- 9.4.2 Radar & sensor systems

- 9.4.3 Command and control systems

- 9.4.4 Avionics and naval communication systems

- 9.4.5 Others

- 9.5 Medical & healthcare

- 9.5.1 Medical imaging systems

- 9.5.2 Laser delivery systems

- 9.5.3 Biomedical sensors & instrumentation

- 9.5.4 Hospital network infrastructure

- 9.5.5 Others

- 9.6 Industrial automation

- 9.6.1 Factory automation and process control networks

- 9.6.2 Robotics & machine vision systems

- 9.6.3 Remote sensing and monitoring

- 9.6.4 Industrial Ethernet

- 9.6.5 Others

- 9.7 Broadcasting & video transmission

- 9.7.1 Live event broadcasting infrastructure

- 9.7.2 Studio-to-transmitter links (STL)

- 9.7.3 Cable TV & IPTV distribution networks

- 9.7.4 Outside broadcast (OB) vans & mobile production

- 9.7.5 Others

- 9.8 Oil & gas

- 9.8.1 Downhole fiber optic sensing

- 9.8.2 Subsea communication links

- 9.8.3 Pipeline monitoring & leak detection systems

- 9.8.4 Remote site connectivity

- 9.8.5 Others

- 9.9 Aerospace

- 9.9.1 Avionics data networks

- 9.9.2 Satellite ground station connectivity

- 9.9.3 In-flight entertainment (IFE) systems

- 9.9.4 Spacecraft optical communication systems

- 9.9.5 Others

- 9.10 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Broadcom

- 11.1.2 Cisco Systems

- 11.1.3 Corning

- 11.1.4 Fujikura

- 11.1.5 Huawei Technologies

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 Ciena

- 11.2.1.2 CommScope

- 11.2.1.3 Lumentum Holdings

- 11.2.1.4 Viavi Solutions

- 11.2.1.5 TE Connectivity

- 11.2.2 Europe

- 11.2.2.1 Amphenol

- 11.2.2.2 Molex

- 11.2.2.3 Prysmian Group

- 11.2.3 APAC

- 11.2.3.1 Furukawa Electric

- 11.2.3.2 Sumitomo Electric

- 11.2.3.3 ZTE

- 11.2.1 North America

- 11.3 Niche Players / Disruptors

- 11.3.1 3Ms

- 11.3.2 Accelink Technologies

- 11.3.3 Broadex Technologies

- 11.3.4 Luxshare-ICT

- 11.3.5 Optosun Technology

- 11.3.6 Senko