|

市場調査レポート

商品コード

1684561

受動光部品の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Passive Optical Component Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 受動光部品の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年01月06日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

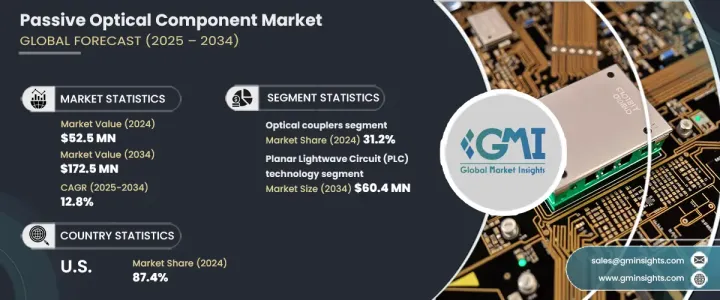

受動光部品の世界市場は、2024年に5,250万米ドルに達し、2025年から2034年にかけてCAGR12.8%という驚異的な成長が予測されています。

高速インターネット需要の高まりとデータ消費の急激な増加が、現代のネットワークインフラの重要な要素として光ファイバ通信の採用を促進しています。産業界や消費者がシームレスなデジタル接続を優先する中、受動光部品はデータの効率的なトランスミッション、ルーティング、増幅を確保するために不可欠なものとなっています。さらに、5G、人工知能(AI)、モノのインターネット(IoT)などの次世代技術の台頭により、堅牢な光ネットワークの必要性が高まっています。これらのコンポーネントは、高帯域幅、低遅延、エネルギー効率の高いデータトランスミッションをサポートし、通信事業者、企業、ハイパースケールデータセンターにとって不可欠なものとなっています。

クラウドコンピューティングは、企業がクラウドベースのアプリケーションやストレージソリューションに移行するにつれて、支持を集め続けています。これらのクラウドサービスのバックボーンを形成するハイパースケールデータセンターは、膨大な量のデータトラフィックを管理するために高度な光ネットワークに大きく依存しています。光カプラ、スプリッタ、波長分割マルチプレクサ(WDM)などの受動光部品は、これらのネットワーク内でシームレスなデータフローを実現する上で極めて重要な役割を果たしています。データルーティングと信号分配のための効率的で費用対効果の高いソリューションを提供するその能力は、現代のデジタルインフラの礎となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 5,250万米ドル |

| 予測金額 | 1億7,250万米ドル |

| CAGR | 12.8% |

市場は、光カプラ、光スプリッタ、光フィルタ、光サーキュレータ、WDM、その他コンポーネントのタイプ別に区分されます。2024年には、光カプラが市場シェアの31.2%を占めました。これらのデバイスは、光ファイバネットワークに不可欠であり、光信号を電気信号に変換することなく、光信号の結合または分割を可能にし、それによって効率と完全性を維持します。光カプラは、信頼性の高い信号ルーティングが優先される通信、産業オートメーション、データセンターなどのアプリケーションで広く使用されています。

技術的には、受動光部品市場には、平面光波回路(PLC)技術、ファイバブラッググレーティング(FBG)技術、薄膜技術、溶融バイコニカルテーパ(FBT)技術、その他が含まれます。PLC技術は、シリカ基板に光導波路をエッチングする高度な製造プロセスによって、2034年には6,040万米ドルに達すると予測されています。この技術は精度を保証し、小型化を可能にするため、スプリッタやマルチプレクサなどの部品に最適です。

米国では、受動光部品市場は2024年に87.4%のシェアを占めました。北米の成長は、5G展開、FTTH(fiber-to-the-home)イニシアティブ、データセンタ拡張など、インフラへの大規模投資が後押ししています。電気通信事業者や技術企業はデジタル接続強化の最前線にあり、カプラ、スプリッタ、WDMデバイスなどの部品需要を牽引しています。米国は、技術革新と高度なネットワーク技術の導入に注力しており、世界市場をリードし続けています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 一次

- 二次

- 有料ソース

- 公的ソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 変革

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュース

- 規制状況

- 影響要因

- 成長促進要因

- 光ファイバー通信の普及

- クラウドサービスとデータセンターの普及

- 5Gインフラへの投資の増加

- 受動光技術の進歩

- 業界の潜在的リスク・課題

- 複雑な設置とメンテナンス

- 無線技術との競合

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業市場シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- ガラス

- プラスチック

- その他

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 平面光波回路(PLC)技術

- ファイバーブラッググレーティング(FBG)技術

- 薄膜技術

- 溶融バイコニカルテーパー(FBT)技術

- その他

第7章 市場推計・予測:コンポーネントタイプ別、2021年~2034年

- 主要動向

- 光カプラ

- 光スプリッタ

- 光フィルター

- 光サーキュレータ

- 波長分割マルチプレクサ(WDM)

- その他

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 通信

- データセンター

- ケーブルテレビ(CATV)

- FTTH(Fiber To The Home)

- 企業ネットワーク

- 航空宇宙・防衛

- 医療・ヘルスケア

- 産業用ネットワーク

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Accelink Technologies Co., Ltd.

- Amphenol Corporation

- Broadcom Inc.

- Ciena Corporation

- Cisco Systems, Inc.

- Corning Incorporated

- Fujitsu Limited

- Furukawa Electric Co., Ltd.

- Huawei Technologies Co., Ltd.

- Huber+Suhner AG

- II-VI Incorporated

- Lumentum Holdings Inc.

- Molex LLC

- NEC Corporation

- Nokia Corporation

- Sterlite Technologies Limited

- Sumitomo Electric Industries Ltd.

- TE Connectivity

- Tellabs Inc.

- ZTE Corporation

The Global Passive Optical Component Market reached USD 52.5 million in 2024 and is projected to grow at an impressive CAGR of 12.8% between 2025 and 2034. The growing demand for high-speed internet and the exponential increase in data consumption are driving the adoption of fiber optic communication as a critical element of modern network infrastructures. As industries and consumers prioritize seamless digital connectivity, passive optical components have become indispensable for ensuring the efficient transmission, routing, and amplification of data. Furthermore, the rise of next-generation technologies, such as 5G, artificial intelligence (AI), and the Internet of Things (IoT), is fueling the need for robust optical networks. These components support high bandwidth, low latency, and energy-efficient data transmission, making them essential for telecom operators, enterprises, and hyperscale data centers.

Cloud computing continues to gain traction as businesses migrate to cloud-based applications and storage solutions. Hyperscale data centers, which form the backbone of these cloud services, depend heavily on advanced optical networks to manage vast volumes of data traffic. Passive optical components, including optical couplers, splitters, and wavelength division multiplexers (WDMs), play a pivotal role in enabling seamless data flow within these networks. Their ability to provide efficient, cost-effective solutions for data routing and signal distribution makes them a cornerstone of modern digital infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $52.5 Million |

| Forecast Value | $172.5 Million |

| CAGR | 12.8% |

The market is segmented by component type, including optical couplers, optical splitters, optical filters, optical circulators, WDMs, and other components. In 2024, optical couplers accounted for 31.2% of the market share. These devices are integral to optical fiber networks, enabling the combination or division of light signals without converting them to electrical signals, thereby preserving their efficiency and integrity. Optical couplers are widely used in applications such as telecommunications, industrial automation, and data centers, where reliable signal routing is a priority.

In terms of technology, the passive optical component market encompasses Planar Lightwave Circuit (PLC) technology, Fiber Bragg Grating (FBG) technology, thin-film technology, Fused Biconical Taper (FBT) technology, and others. PLC technology is projected to reach USD 60.4 million by 2034, driven by its advanced fabrication processes that etch optical waveguides onto silica substrates. This technology ensures precision and enables miniaturization, making it ideal for components like splitters and multiplexers.

In the United States, the passive optical component market held an 87.4% share in 2024. Growth in North America is propelled by significant investments in infrastructure, including 5G rollouts, fiber-to-the-home (FTTH) initiatives, and data center expansions. Telecom operators and technology firms are at the forefront of enhancing digital connectivity, driving demand for components like couplers, splitters, and WDM devices. The U.S. continues to lead the global market thanks to its focus on innovation and adoption of advanced networking technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising adoption of fiber optic communication

- 3.6.1.2 Proliferation of cloud services and data centers

- 3.6.1.3 Increasing investments in 5G infrastructure

- 3.6.1.4 Advancements in passive optical technologies

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Complex installation and maintenance

- 3.6.2.2 Competition from wireless technologies

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Glass

- 5.3 Plastic

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Planar Lightwave Circuit (PLC) Technology

- 6.3 Fiber Bragg Grating (FBG) Technology

- 6.4 Thin film technology

- 6.5 Fused Biconical Taper (FBT) Technology

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Component Type, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Optical couplers

- 7.3 Optical splitters

- 7.4 Optical filters

- 7.5 Optical circulators

- 7.6 Wavelength Division Multiplexers (WDMs)

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Telecommunications

- 8.3 Data centers

- 8.4 Cable Television (CATV)

- 8.5 Fiber to the Home (FTTH)

- 8.6 Enterprise networks

- 8.7 Aerospace and defense

- 8.8 Medical and healthcare

- 8.9 Industrial networking

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Accelink Technologies Co., Ltd.

- 10.2 Amphenol Corporation

- 10.3 Broadcom Inc.

- 10.4 Ciena Corporation

- 10.5 Cisco Systems, Inc.

- 10.6 Corning Incorporated

- 10.7 Fujitsu Limited

- 10.8 Furukawa Electric Co., Ltd.

- 10.9 Huawei Technologies Co., Ltd.

- 10.10 Huber+Suhner AG

- 10.11 II-VI Incorporated

- 10.12 Lumentum Holdings Inc.

- 10.13 Molex LLC

- 10.14 NEC Corporation

- 10.15 Nokia Corporation

- 10.16 Sterlite Technologies Limited

- 10.17 Sumitomo Electric Industries Ltd.

- 10.18 TE Connectivity

- 10.19 Tellabs Inc.

- 10.20 ZTE Corporation