|

市場調査レポート

商品コード

1797687

フローリング用化学品の市場機会と促進要因、業界動向分析、2025年~2034年予測Flooring Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| フローリング用化学品の市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年07月31日

発行: Global Market Insights Inc.

ページ情報: 英文 192 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

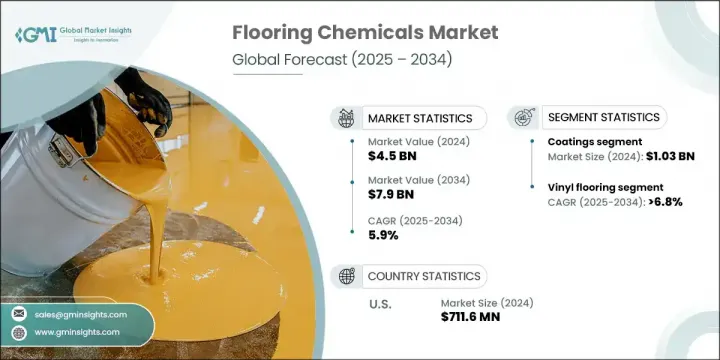

フローリング用化学品の世界市場規模は、2024年に45億米ドルとなり、CAGR 5.9%で成長し、2034年には79億米ドルに達すると予測されています。

同市場は、環境に優しい素材や低排出化学処方へのシフトにより急速に発展しています。持続可能性が重視される中、メーカーは環境規制と消費者の期待の変化の両方に対応するため、VOCレベルを低減し、バイオベースの含有量を増やした高度なフローリングソリューションを開発しています。スマートな製造技術とデジタル・ツールは、より高い工程効率、品質管理、需要への対応力を確保するため、生産に統合されつつあります。

デジタル化の進展は、リアルタイムのモニタリング、サプライチェーンの調整改善、顧客ニーズの的確なターゲティングを可能にしています。高性能で耐久性に優れ、持続可能な床材を求める動きは、住宅、商業施設、工業施設の建設に広く需要をもたらしています。樹脂、コーティング剤、接着剤などのフローリング用化学品は、さまざまな環境負荷のもとで、床の美観、耐摩耗性、機能性を向上させる中心的存在です。同市場は、弾力性、メンテナンスの容易さ、環境への影響の少なさを兼ね備えた床材システムの強力な技術革新と急速な採用から恩恵を受けており、先進地域と新興地域にわたる世界の拡大をさらに強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 45億米ドル |

| 予測金額 | 79億米ドル |

| CAGR | 5.9% |

コーティング分野は2024年に10億3,000万米ドルを生み出し、2034年までCAGR 7.2%で成長し続けると予測されます。コーティング剤、接着剤、シーリング剤は、木材、タイル、ラミネート、ビニールなど様々な素材の床の施工と保護に不可欠です。排出に関する意識の高まりを受けて、企業は低VOCで速硬化性の接着剤処方を革新しており、住宅と商業建築の両方で需要を押し上げています。水性接着剤とバイオ接着剤の製品タイプは、環境への影響を最小限に抑え、多様な床材タイプに適応できることから支持を集めています。

ビニル床材セグメントは、2025年から2034年にかけてCAGR 6.8%の成長が見込まれています。この床材は、多用途性と弾力性によって勢いを増しており、裏打ち材、接着剤、表面コーティングの化学革新によって強化され、湿気の多い場所や人の出入りの多い場所での性能を高めています。カーペットのような他の一般的な床材では、抗菌治療や低排出材料が進歩し、グリーンビルディング基準や公衆衛生の期待に沿うようになっています。

米国フローリング用化学品市場は2024年に80%のシェアを占め、7億1,160万米ドルを創出しました。米国のフローリング用化学品分野は、好調な住宅建設、リフォーム動向、性能重視の床材システムの需要を背景に活況を呈しています。気候が多様で、地域によって建築基準法が異なるため、コーティング剤、プライマー、接着剤の技術革新は気候に強く、構造に特化したソリューションに集中しています。このため米国は、床材化学技術革新の重要な拠点となっています。

世界フローリング用化学品市場の主要企業には、Sika AG、BASF SE、The Dow Chemical Company、Henkel AG &Co.KGaA、3M Companyなどです。フローリング用化学品市場の主要企業は、VOC排出量が少なく耐久性が改善された高度な配合物を開発するために研究開発に投資しています。進化する規制に対応し、持続可能な製品に対する消費者の需要の高まりに応えるため、より環境に優しい化学物質へとシフトしています。床材メーカーや建設会社との戦略的パートナーシップは、多様な施工ニーズに合わせた統合ソリューションを生み出すために形成されています。各社は、高成長地域に新たな製造施設を開設し、流通網を強化することで、世界な足跡を拡大しています。リアルタイム分析やスマート・ロジスティクスを含むデジタルトランスフォーメーションが業務効率を高めています。マーケティング戦略は、環境意識の高いバイヤーや環境意識の高い消費者の注目を集めるため、環境と健康に配慮したフローリング用化学品の利点を大きく取り上げるようになっています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 接着剤

- 水性接着剤

- 溶剤系接着剤

- ウレタン系/湿気硬化型接着剤

- 粉体接着剤

- ホットメルト接着剤

- シーラント

- シリコンシーラント

- ポリウレタンシーラント

- アクリルシーラント

- ブチルシーラント

- コーティング

- エポキシコーティング

- ポリウレタンコーティング

- ポリアスパラギン酸コーティング

- アクリルコーティング

- 抗菌コーティング

- プライマーと表面処理

- エポキシプライマー

- アクリルプライマー

- ポリウレタンプライマー

- 表面処理用化学薬品

- 下地材と平滑化剤

- セルフレベリングコンパウンド

- 防湿バリア

- 防音下地

- 床仕上げ剤と研磨剤

- 水性仕上げ

- 溶剤系仕上げ

- UV硬化仕上げ

- メンテナンス用ポリッシュ

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 堅木張りの床

- ラミネートフローリング

- ビニール床材

- カーペット床

- タイルと石の床

- コンクリート床

- その他の床材

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 住宅用

- 一戸建て住宅

- 集合住宅

- 改修と改造

- 商業用

- オフィスビル

- 小売スペース

- ホスピタリティ

- ヘルスケア施設

- 教育機関

- 産業

- 製造施設

- 倉庫と配送センター

- 食品加工工場

- 医薬品施設

- 化学処理工場

第8章 市場推計・予測:技術別、2021-2034

- 主要動向

- 従来の化学システム

- 従来のエポキシシステム

- 標準的なポリウレタン配合

- 従来のアクリルシステム

- 高度な化学技術

- ナノテクノロジーを活用した処方

- スマートで機能的なコーティング

- 自己修復材料

- 抗菌技術

- 持続可能でバイオベースのシステム

- バイオベースポリウレタン

- 植物由来の接着剤

- リサイクルコンテンツの配合

- 低VOCおよびゼロVOCシステム

- 特殊および高性能システム

- 耐薬品性製剤

- 耐高温システム

- 静電気防止および導電性システム

- 装飾と美的システム

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- フィリピン

- ベトナム

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

第10章 企業プロファイル

- BASF SE

- Sika AG

- Henkel AG &Co. KGaA

- The Dow Chemical Company

- 3M Company

- Sherwin-Williams Company

- Mapei S.p.A.

- H.B. Fuller Company

- RPM International Inc.

- Arkema Group

The Global Flooring Chemicals Market was valued at USD 4.5 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 7.9 billion by 2034. The market is rapidly evolving due to a shift toward eco-friendly materials and low-emission chemical formulations. As sustainability becomes a core focus, manufacturers are developing advanced flooring solutions with reduced VOC levels and increased bio-based content to meet both environmental regulations and changing consumer expectations. Smart manufacturing techniques and digital tools are being integrated into production to ensure greater process efficiency, quality control, and responsiveness to demand.

Increasing digitalization is enabling real-time monitoring, improved supply chain coordination, and precise targeting of customer needs. The push for high-performance, durable, and sustainable flooring materials is fueling widespread demand across residential, commercial, and industrial construction. Flooring chemicals such as resins, coatings, and adhesives are central to improving floor aesthetics, wear resistance, and functionality under varying environmental loads. The market is benefiting from strong innovation and rapid adoption of flooring systems that combine resilience, easy maintenance, and minimal environmental impact, further reinforcing its global expansion across developed and emerging regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.5 Billion |

| Forecast Value | $7.9 Billion |

| CAGR | 5.9% |

The coatings segment generated USD 1.03 billion in 2024 and is expected to continue growing at 7.2% CAGR through 2034. Coatings, adhesives, and sealants remain critical to floor installation and protection across multiple materials including wood, tile, laminate, and vinyl. With rising awareness around emissions, companies are innovating low-VOC and fast-curing adhesive formulations, boosting demand across both residential and commercial construction. Product advancements in water-based and bio-based adhesives have gained traction for their minimal environmental footprint and adaptability across diverse flooring types.

The vinyl flooring segment is expected to grow at a CAGR of 6.8% from 2025 to 2034. This flooring solution is gaining momentum due to its versatility and resilience, enhanced by chemical innovations in backings, adhesives, and surface coatings that boost performance in moisture-prone and high-traffic areas. Other popular flooring types, like carpet, are seeing advancements in antimicrobial treatments and low-emission materials to align with green building standards and public health expectations.

United States Flooring Chemicals Market held 80% share and generated USD 711.6 million in 2024. The U.S. flooring chemicals sector is thriving on the back of strong housing construction, renovation trends, and demand for performance-based flooring systems. With its diverse climate and varying construction codes across regions, innovation in coatings, primers, and adhesives is focused on climate-resilient and structure-specific solutions. This has positioned the U.S. as a key hub for innovation in flooring chemical technologies.

Leading companies in the Global Flooring Chemicals Market include Sika AG, BASF SE, The Dow Chemical Company, Henkel AG & Co. KGaA, and 3M Company. Major players in the flooring chemicals market are investing in R&D to develop advanced formulations with lower VOC emissions and improved durability. They are shifting toward greener chemistries to comply with evolving regulations and to meet rising consumer demand for sustainable products. Strategic partnerships with flooring material manufacturers and construction firms are being formed to create integrated solutions tailored to diverse installation needs. Companies are expanding their global footprints by opening new manufacturing facilities in high-growth regions and strengthening distribution networks. Digital transformation, including real-time analytics and smart logistics, is enhancing operational efficiency. Marketing strategies now focus heavily on the environmental and health benefits of eco-conscious flooring chemicals to capture the attention of both commercial buyers and environmentally aware consumers.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Applications

- 2.2.4 End use

- 2.2.5 Technology

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 ($Bn, Kilo tons)

- 5.1 Key trends

- 5.2 Adhesives

- 5.2.1 Water-based adhesives

- 5.2.2 Solvent-based adhesives

- 5.2.3 Urethane-based/moisture-cure adhesives

- 5.2.4 Powder adhesives

- 5.2.5 Hot-melt adhesives

- 5.3 Sealants

- 5.3.1 Silicone sealants

- 5.3.2 Polyurethane sealants

- 5.3.3 Acrylic sealants

- 5.3.4 Butyl sealants

- 5.4 Coatings

- 5.4.1 Epoxy coatings

- 5.4.2 Polyurethane coatings

- 5.4.3 Polyaspartic coatings

- 5.4.4 Acrylic coatings

- 5.4.5 Antimicrobial coatings

- 5.5 Primers and surface preparation

- 5.5.1 Epoxy primers

- 5.5.2 Acrylic primers

- 5.5.3 Polyurethane primers

- 5.5.4 Surface preparation chemicals

- 5.6 Underlayments and smoothing compounds

- 5.6.1 Self-leveling compounds

- 5.6.2 Moisture barriers

- 5.6.3 Sound dampening underlayments

- 5.7 Floor finishes and polishes

- 5.7.1 Water-based finishes

- 5.7.2 Solvent-based finishes

- 5.7.3 UV-cured finishes

- 5.7.4 Maintenance polishes

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Kilo tons)

- 6.1 Key trends

- 6.2 Hardwood flooring

- 6.3 Laminate flooring

- 6.4 Vinyl flooring

- 6.5 Carpet flooring

- 6.6 Tile and stone flooring

- 6.7 Concrete flooring

- 6.8 Other flooring types

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Kilo tons)

- 7.1 Key trends

- 7.2 Residential

- 7.2.1 Single-family homes

- 7.2.2 Multi-family residential

- 7.2.3 Renovation and remodeling

- 7.3 Commercial

- 7.3.1 Office buildings

- 7.3.2 Retail spaces

- 7.3.3 Hospitality

- 7.3.4 Healthcare facilities

- 7.3.5 Educational institutions

- 7.4 Industrial

- 7.4.1 Manufacturing facilities

- 7.4.2 Warehouses and distribution centers

- 7.4.3 Food processing plants

- 7.4.4 Pharmaceutical facilities

- 7.4.5 Chemical processing plants

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Kilo tons)

- 8.1 Key trends

- 8.2 Conventional chemical systems

- 8.2.1 Traditional epoxy systems

- 8.2.2 Standard polyurethane formulations

- 8.2.3 Conventional acrylic systems

- 8.3 Advanced chemical technologies

- 8.3.1 Nanotechnology-enhanced formulations

- 8.3.2 Smart and functional coatings

- 8.3.3 Self-healing materials

- 8.3.4 Antimicrobial technologies

- 8.4 Sustainable and bio-based systems

- 8.4.1 Bio-based polyurethanes

- 8.4.2 Plant-based adhesives

- 8.4.3 Recycled content formulations

- 8.4.4 Low-voc and zero-voc systems

- 8.5 Specialty and high-performance systems

- 8.5.1 Chemical-resistant formulations

- 8.5.2 High-temperature resistant systems

- 8.5.3 Anti-static and conductive systems

- 8.5.4 Decorative and aesthetic systems

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Kilo tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 France

- 9.3.3 Italy

- 9.3.4 Spain

- 9.3.5 Russia

- 9.3.6 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Egypt

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 Sika AG

- 10.3 Henkel AG & Co. KGaA

- 10.4 The Dow Chemical Company

- 10.5 3M Company

- 10.6 Sherwin-Williams Company

- 10.7 Mapei S.p.A.

- 10.8 H.B. Fuller Company

- 10.9 RPM International Inc.

- 10.10 Arkema Group