ワクチンの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Vaccines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日

- 商品コード

- 1782152

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

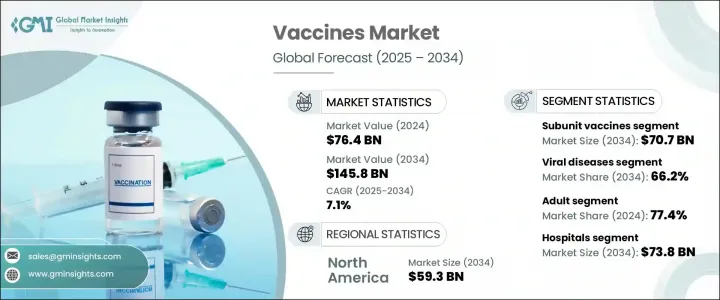

世界のワクチン市場は、2024年に764億米ドルと評価され、CAGR 7.1%で成長し、2034年には1,458億米ドルに達すると推定されています。

この成長は、肝炎、季節性インフルエンザ、新型ウイルス株などの感染症の継続的な出現によって大きく後押しされています。これらの疾病は公衆衛生に対する絶え間ない脅威であり続けるため、政府や医療機関は感染率を低下させるために予防接種の取り組みを強化しています。支持的な公的イニシアティブ、発展途上地域におけるヘルスケア予算の増加、ワクチン研究開発の進歩は、拡大のための有利な環境を形成し続けています。さらに、1回の接種で複数の疾患に対する免疫を獲得できる混合ワクチンの世界の増加は、技術革新を加速させ、予防接種プロトコルを簡素化しています。

がん、慢性感染症、自己免疫疾患などの複雑な病態をターゲットとした次世代型ワクチンの開発は、市場の治療範囲を拡大しています。特に先進国では高齢化が進んでおり、感染症にかかりやすい状況が続いているため、世界のワクチン需要がさらに高まっています。民間企業と公衆衛生機関との強力な協力関係や、mRNAや組換え蛋白質プラットフォームなどの進化する技術も相まって、ワクチンの有効性、送達、利用しやすさが向上しています。これらの要因が相まって、長期的な市場の勢いが強まっています。

| 市場規模 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 764億米ドル |

| 予測金額 | 1,458億米ドル |

| CAGR | 7.1% |

2024年、サブユニットワクチンセグメントは376億米ドルと評価され、CAGR 6.9%で成長し、2034年には707億米ドルに達すると推定されます。これらのワクチンには、組換え型、多糖類型、コンジュゲート型があり、それぞれ病原体全体を使用せずに免疫原性を高めることに貢献しています。病気の原因となる生物から特定のタンパク質をターゲットにするこれらの能力は、安全性プロファイルを改善し、望ましくない免疫反応を減少させる。T細胞依存的な免疫活性化により、より強力な記憶応答が促進され、長期間の防御が可能で、乳幼児などの脆弱な集団に適していることから、この分野は引き続き牽引役となっています。

ウイルス性疾患分野は2024年に66.2%のシェアを占め、2034年まで力強い成長を維持すると予想されています。このカテゴリーには、肝炎、インフルエンザ、HPV、ロタウイルス、帯状疱疹、MMR、COVID-19、その他のウイルスに対するワクチンが含まれます。認識と予防の取り組みが拡大するにつれて、予防接種プログラムは世界的に規模を拡大し、接種率とアクセスが向上しています。mRNAやサブユニット技術のような製造プラットフォームにおける最近の進歩により、ウイルス発生時の迅速な対応能力が強化され、世界中で強固な公衆衛生戦略を支えるとともに、あらゆる年齢層で予防接種の普及が進んでいます。

北米ワクチン2024年の市場規模は323億米ドルで、2034年にはCAGR 6.6%で593億米ドルに達する見込みです。この地域のリーダーシップは、包括的なヘルスケア・インフラ、継続的な公的予防接種キャンペーン、予防医療への多額の投資に起因します。一貫した政策レベルの取り組み、高い認知度、HPVやその他のウイルスの脅威をターゲットにしたワクチンに対する強い需要が、引き続き売上を牽引しています。米国では、学校単位での予防接種プログラムや成人への予防接種が広く実施されており、人口層全体におけるアクセスとコンプライアンスが強化されています。

ワクチン世界市場の競争力学に貢献している主要メーカーには、Sanofi、Serum Institute of India、Valneva、CSL Seqirus、Emergent Biosolutions、Pfizer、Moderna、Novavax、GlaxoSmithKline(GSK)、AstraZeneca、Biofarma、Sinovac、Bharat Biotech、Haffkine Bio-Pharmaceutical、VBIワクチン、Merckなどがあります。ワクチンセクターの主要企業は、研究開発、特にmRNA、組換えサブユニット、ベクターベースの製剤などの新規プラットフォームへの持続的な投資を通じて、パイプラインを積極的に進化させています。

バイオテクノロジー企業、学術機関、政府保健機関との提携や合弁事業は、次世代ワクチンの開発と規制当局の認可を迅速化するのに役立っています。企業はまた、アウトブレイク時の迅速な拡張性を確保し、十分なサービスを受けていない市場に効率的に対応するため、生産能力を世界に拡大しています。配合剤や治療用ワクチンの開発を含む戦略的な製品の多様化は、企業がより広範な疾病負担に対処するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 感染症の発生率の上昇

- 予防接種普及プログラムの拡大

- 新興経済諸国における小児人口の増加

- ワクチンの処方と生産効率の進歩

- 業界の潜在的リスク&課題

- 厳格な規制承認プロセス

- ワクチンの保管と輸送にかかる高コスト

- 市場機会

- ワクチン配布のための官民パートナーシップの拡大

- 組み合わせへの注目が高まるワクチン

- 促進要因

- 成長可能性分析

- テクノロジーの情勢

- パイプライン分析

- 規制情勢

- 将来の市場動向

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 拡張計画

第5章 市場推計・予測:ワクチンタイプ別、2021年~2034年

- 主要動向

- サブユニットワクチン

- 組み換えワクチン

- ワクチンを活用する

- 多糖類ワクチン

- トキソイドワクチン

- 無効化されたワクチン

- ライブ減衰ワクチン

- その他のワクチンタイプ

第6章 市場推計・予測:病気タイプ別、2021年~2034年

- 主要動向

- ウイルス性疾患

- 肝炎

- インフルエンザ

- HPV

- 麻疹、おたふく風邪、風疹(MMR)

- ロタウイルス

- 帯状疱疹

- COVID-19

- その他のウイルス性疾患

- 細菌性疾患

- 髄膜炎菌感染症

- 肺炎球菌性疾患

- 二回経口投与

- その他の細菌性疾患

第7章 市場推計・予測:年齢別、2021年~2034年

- 主要動向

- 小児科

- 成人用

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 公共

- プライベート

- 専門クリニック

- その他の用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AstraZeneca

- Bharat Biotech

- Biofarma

- CSL Seqirus

- Emergent Biosolutions

- GlaxoSmithKline(GSK)

- Haffkine Bio-Pharmaceutical

- Merck

- Moderna

- Novavax

- Pfizer

- Sanofi

- Serum Institute of India

- Sinovac

- Valneva

- VBI Vaccines

目次

The Global Vaccines Market was valued at USD 76.4 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 145.8 billion by 2034. This growth is largely propelled by the continuous emergence of infectious diseases such as hepatitis, seasonal influenza, and novel virus strains. As these diseases remain a constant threat to public health, governments and health organizations are ramping up immunization efforts to reduce infection rates. Supportive public initiatives, increasing healthcare budgets in developing regions, and advancements in vaccine R&D continue to shape a favorable environment for expansion. Additionally, the global rise in combination vaccines, which deliver immunity for multiple diseases through a single dose, is accelerating innovation and simplifying immunization protocols.

Development of next-generation vaccines targeting complex conditions such as cancers, chronic infections, and autoimmune diseases is expanding the market's therapeutic scope. A growing aging population, especially across developed nations, remains highly susceptible to infections, further fueling global vaccine demand. Strong collaborations between private firms and public health bodies, coupled with evolving technologies such as mRNA and recombinant protein platforms, are enhancing vaccine efficacy, delivery, and accessibility. Collectively, these factors are reinforcing long-term market momentum.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $76.4 Billion |

| Forecast Value | $145.8 Billion |

| CAGR | 7.1% |

In 2024, subunit vaccines segment was valued at USD 37.6 billion and is estimated to reach USD 70.7 billion by 2034, growing at a CAGR of 6.9%. These vaccines include recombinant, polysaccharide, and conjugate types, each contributing to heightened immunogenicity without using whole pathogens. Their ability to target specific proteins from disease-causing organisms improves safety profiles and reduces unwanted immune responses. The segment continues to gain traction due to its T cell-dependent immune activation, which promotes stronger memory responses, long-lasting protection, and suitability for vulnerable populations like infants and young children.

The viral diseases segment held 66.2% share in 2024 and is expected to maintain strong growth through 2034. The category comprises vaccines for hepatitis, influenza, HPV, rotavirus, herpes zoster, MMR, COVID-19, and other viruses. As awareness and prevention efforts have expanded, immunization programs have scaled globally, improving coverage and access. Recent advancements in manufacturing platforms like mRNA and subunit technologies have enhanced rapid-response capabilities during viral outbreaks, supporting robust public health strategies worldwide and increasing uptake across all age groups.

North America Vaccines Market generated USD 32.3 billion in 2024 and is expected to reach USD 59.3 billion by 2034 at a CAGR of 6.6%. The region's leadership stems from its comprehensive healthcare infrastructure, ongoing public immunization campaigns, and significant investment in preventive care. Consistent policy-level initiatives, high levels of awareness, and strong demand for vaccines targeting HPV and other viral threats continue to drive sales. The U.S. has implemented widespread school-based programs and adult immunization drives, enhancing access and compliance across population segments.

Key manufacturers contributing to the competitive dynamics of the Global Vaccines Market include Sanofi, Serum Institute of India, Valneva, CSL Seqirus, Emergent Biosolutions, Pfizer, Moderna, Novavax, GlaxoSmithKline (GSK), AstraZeneca, Biofarma, Sinovac, Bharat Biotech, Haffkine Bio-Pharmaceutical, VBI Vaccines, and Merck. Leading companies in the vaccines sector are actively advancing their pipelines through sustained investments in R&D, particularly in novel platforms like mRNA, recombinant subunits, and vector-based formulations.

Partnerships and joint ventures with biotech firms, academic institutions, and government health agencies are helping expedite development and regulatory clearance for next-gen vaccines. Firms are also expanding production capabilities globally to ensure rapid scalability during outbreaks and to serve underserved markets efficiently. Strategic product diversification, including development of combination and therapeutic vaccines, is helping companies address broader disease burdens.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vaccine type

- 2.2.3 Disease type

- 2.2.4 Age group

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of infectious disease

- 3.2.1.2 Growing immunization coverage programs

- 3.2.1.3 Increasing pediatric population in developing economies

- 3.2.1.4 Advancements in vaccine formulation and production efficiency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory approval processes

- 3.2.2.2 High cost of storage and transportation of vaccine

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding public-private partnerships for vaccine distribution

- 3.2.3.2 Growing focus on combination vaccines

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Pipeline analysis

- 3.6 Regulatory landscape

- 3.7 Future market trends

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 Expansion plans

Chapter 5 Market Estimates and Forecast, By Vaccine Type, 2021-2034 ($ Mn)

- 5.1 Key trends

- 5.2 Subunit vaccines

- 5.2.1 Recombinant vaccines

- 5.2.2 Conjugate vaccines

- 5.2.3 Polysaccharide vaccines

- 5.3 Toxoid vaccines

- 5.4 Inactivated vaccines

- 5.5 Live attenuated vaccines

- 5.6 Other vaccine types

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021-2034 ($ Mn)

- 6.1 Key trends

- 6.2 Viral diseases

- 6.2.1 Hepatitis

- 6.2.2 Influenza

- 6.2.3 HPV

- 6.2.4 Measles, mumps, and rubella (MMR)

- 6.2.5 Rotavirus

- 6.2.6 Herpes zoster

- 6.2.7 Covid-19

- 6.2.8 Other viral diseases

- 6.3 Bacterial diseases

- 6.3.1 Meningococcal diseases

- 6.3.2 Pneumococcal diseases

- 6.3.3 DPT

- 6.3.4 Other bacterial diseases

Chapter 7 Market Estimates and Forecast, By Age Group, 2021-2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pediatric

- 7.3 Adult

Chapter 8 Market Estimates and Forecast, By End Use, 2021-2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.2.1 Public

- 8.2.2 Private

- 8.3 Specialty clinics

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AstraZeneca

- 10.2 Bharat Biotech

- 10.3 Biofarma

- 10.4 CSL Seqirus

- 10.5 Emergent Biosolutions

- 10.6 GlaxoSmithKline (GSK)

- 10.7 Haffkine Bio-Pharmaceutical

- 10.8 Merck

- 10.9 Moderna

- 10.10 Novavax

- 10.11 Pfizer

- 10.12 Sanofi

- 10.13 Serum Institute of India

- 10.14 Sinovac

- 10.15 Valneva

- 10.16 VBI Vaccines

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 210 Pages

- 納期

- 2~3営業日