物流におけるジェネレーティブAIの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Generative AI in Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1782148

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

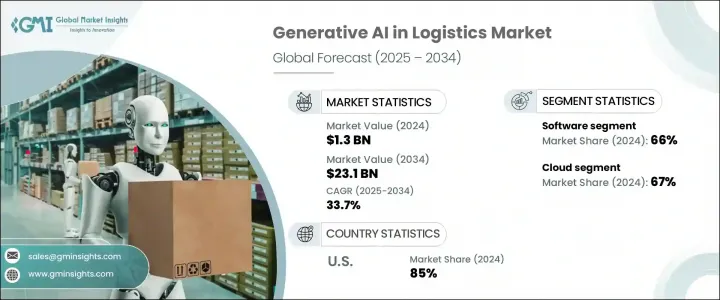

物流におけるジェネレーティブAIの世界市場規模は、2024年に13億米ドルとなり、CAGR 33.7%で成長し、2034年には231億米ドルに達すると予測されています。

このテクノロジーは、リアルタイムのインテリジェンスと長期的な戦略予測の両方を提供することで、サプライチェーンのオペレーションを根本的に変革しています。何千もの配送ルートや輸送シナリオをシミュレートすることで、物流業者は在庫計画を微調整し、運賃を下げ、予期せぬ混乱に備えることができます。また、AIを活用した需要予測はリソースの利用を効率化し、ダイナミックルーティングツールは配送スケジュールを改善します。業務効率とコスト管理がより重要になる中、市場の将来を形作る重要な力として、ジェネレーティブAIの統合が浮上しています。

ジェネレーティブAIは、顧客の行動や嗜好を分析することで、ロジスティクス企業がサービスのパーソナライゼーションを強化することを可能にします。これらのインテリジェント・システムは、リアルタイムの警告を発し、理想的な配達窓口を推奨し、顧客との対話に基づいてサービスを自動的に調整することができます。このレベルのカスタマイズは、顧客の満足度と忠誠心を高めると同時に、企業がプレミアム価格を請求することを可能にします。競争の激しい業界では、AIを活用したパーソナライズされたロジスティクス体験が引き続き勢いを増しています。さらに、燃料コストと排出量を削減する圧力が高まる中、物流車両は、交通パターン、天候予測、過去のデータを使用して最適化されたルートを提案するAIにますます依存するようになり、よりクリーンでスリムなオペレーションが標準となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 13億米ドル |

| 予測金額 | 231億米ドル |

| CAGR | 33.7% |

2024年、ソフトウェア分野のシェアは66%で、2034年までのCAGRは32%で成長します。ロジスティクスチームは、在庫不足、配送の滞り、突然の需要急増など、多数のサプライチェーンの混乱をシミュレートするAI主導の予測ツールを優先しています。これらのツールは、企業が業務をプロアクティブに調整し、効率とコストの両方を改善するのに役立ちます。このような最新のソリューションは、旧来のモデルよりも迅速な結果を提供し、レガシーシステムとの統合も容易であるため、時間のかかるカスタムメイドのオプションよりも魅力的です。

クラウド導入分野は2024年に67%のシェアを占め、2034年までCAGR 32%で力強い成長を維持すると予想されます。ロジスティクス業務が地理的に分散するにつれて、企業は変動するビジネスニーズに基づいて即座に拡張できる柔軟なクラウドベースのAIソリューションを選択するようになっています。従来のサーバーセットアップとは異なり、クラウドプラットフォームは、特に季節的なピーク時や予期せぬ市場シフト時など、需要の急増に合わせてリアルタイムのコンピューティングパワーとデータストレージを提供します。この適応性により、クラウドシステムはグローバルサプライチェーンに不可欠なものとなり、この分野での優位性を高めています。

北米物流におけるジェネレーティブAI市場は85%のシェアを占め、2024年には3億5,520万米ドルを創出しました。同国は、IBM、マイクロソフト、アマゾン、オラクル、パランティア・テクノロジーズ、SAP、エヌビディア、グーグルなどの大手ハイテク企業に支えられ、サプライチェーンにおける高度なAI導入の中心的な拠点として浮上しています。これらの企業はエンタープライズ対応のAIインフラを提供しており、物流プロバイダーはアルゴリズムの開発と展開を加速させる最先端の機能にすぐにアクセスできます。この迅速なイノベーションサイクルにより、米国は世界のロジスティクスAIのフロントランナーとして位置づけられています。

物流におけるジェネレーティブAI市場の主要企業は、戦略的クラウドパートナーシップ、スケーラブルなAIモデル、業界に特化した機械学習ツールを倍増させています。また、地域や分野特有のロジスティクスの課題に迅速に適応するモジュール型AIソリューションにも注力しています。API統合によるユーザーアクセシビリティの向上、プラグアンドプレイプラットフォームの構築、リアルタイムのデータ可視性の実現は、共通の目標です。これらの企業はアジャイル開発環境に投資し、リアルタイムの物流需要に対応する低遅延コンピューティングを提供しています。顧客エンゲージメントを向上させ、オペレーショナルリスクを軽減し、急速に進化する市場情勢の中でブランドが競争優位に立つために、競合情勢分析、持続可能性に焦点を当てたルート最適化、および予測分析機能が優先されています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 強化されたサプライチェーンの最適化

- 反復プロセスの自動化

- 顧客のパーソナライズされた体験

- コスト効率の高い車両およびルート管理

- 業界の潜在的リスク&課題

- データのプライバシーとセキュリティリスク

- レガシーシステムとの統合の複雑さ

- 市場機会

- AIによる需要予測と在庫最適化

- スマート倉庫のためのデジタルツインの作成

- 自律ルート計画と車両管理

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- ケーススタディ

- ユースケース

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 変分オートエンコーダ

- 生成的敵対ネットワーク

- リカレントニューラルネットワーク

- 長期短期記憶ネットワーク

- トランスフォーマー

第6章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソフトウェア

- サービス

第7章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- クラウド

- オンプレミス

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- ルート最適化

- 需要予測

- 倉庫および在庫管理

- サプライチェーンの自動化

- 予測メンテナンス

- リスク管理

- カスタマイズされた物流ソリューション

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- サードパーティロジスティクスプロバイダー

- 貨物運送業者

- eコマース企業

- 製造業者

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Amazon Web Services

- DHL Group

- FedEx

- Flexport

- Four Kites

- IBM

- Locus

- Maersk

- Microsoft

- NVIDIA

- Open AI

- Optimal Dynamics

- Oracle

- Palantir Technologies

- Project44

- Salesforce

- SAP

- UPS

- XPO Logistics

目次

The Global Generative AI in Logistics Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 33.7% to reach USD 23.1 billion by 2034. This technology is fundamentally transforming supply chain operations by delivering both real-time intelligence and long-term strategic forecasting. By simulating thousands of delivery routes and transport scenarios, logistics providers can fine-tune inventory planning, lower freight expenses, and stay prepared for unexpected disruptions. AI-powered demand forecasting also streamlines resource use, while dynamic routing tools improve delivery timelines. As operational efficiency and cost control become more important, the integration of generative AI has emerged as a key force shaping the market's future.

Generative AI enables logistics firms to enhance service personalization by analyzing customer behavior and preferences. These intelligent systems can trigger real-time alerts, recommend ideal delivery windows, and automatically adjust services based on client interactions. This level of customization boosts customer satisfaction and loyalty while allowing businesses to charge premium prices. In a competitive industry, personalized logistics experiences powered by AI continue to drive momentum. Moreover, with growing pressure to reduce fuel costs and emissions, logistics fleets increasingly rely on AI to suggest optimized routes using traffic patterns, weather predictions, and historical data, making cleaner and leaner operations the standard.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $23.1 Billion |

| CAGR | 33.7% |

In 2024, the software segment held a 66% share and is set to grow at a CAGR of 32% through 2034. Logistics teams have prioritized AI-driven predictive tools that simulate numerous supply chain disruptions like stock shortages, delivery hold-ups, or sudden demand spikes. These tools help firms adjust operations proactively, improving both efficiency and cost outcomes. These modern solutions offer faster results than older models and integrate easily with legacy systems, making them more attractive than time-consuming, custom-built options.

The cloud deployment segment held a 67% share in 2024 and is expected to maintain strong growth at a CAGR of 32% through 2034. As logistics operations become more geographically dispersed, firms are choosing flexible, cloud-based AI solutions that scale instantly based on fluctuating business needs. Unlike traditional server setups, cloud platforms provide real-time computing power and data storage as demand surges, especially during seasonal peaks or unexpected market shifts. This adaptability makes cloud systems critical for global supply chains, reinforcing their dominance in the sector.

North America Generative AI In Logistics Market held 85% share and generated USD 355.2 million in 2024. The country has emerged as a central hub for advanced AI adoption in supply chains, backed by major tech firms like IBM, Microsoft, Amazon, Oracle, Palantir Technologies, SAP, NVIDIA, and Google. These companies offer enterprise-ready AI infrastructure, giving logistics providers immediate access to cutting-edge capabilities that accelerate algorithm development and deployment. This rapid innovation cycle positions the U.S. as a frontrunner in logistics AI worldwide.

Leading firms in the Generative AI in Logistics Market are doubling down on strategic cloud partnerships, scalable AI models, and industry-specific machine learning tools. They're also focusing on modular AI solutions that adapt quickly to regional and sector-specific logistics challenges. Enhancing user accessibility through API integration, building plug-and-play platforms, and enabling real-time data visibility are common goals. These companies invest in agile development environments and provide low-latency computing to meet real-time logistics demands. Customization capabilities, sustainability-focused route optimization, and predictive analytics are being prioritized to improve customer engagement and reduce operational risks, giving brands a competitive edge in a fast-evolving market landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Component

- 2.2.4 Deployment mode

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Enhanced supply chain optimization

- 3.2.1.2 Automation of repetitive process

- 3.2.1.3 Personalized experience of the customers

- 3.2.1.4 Cost-efficient fleet & route management

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy and security risks

- 3.2.2.2 Integration complexity with legacy systems

- 3.2.3 Market opportunities

- 3.2.3.1 AI driven demand forecasting and inventory optimization

- 3.2.3.2 Digital twin creation for smart warehousing

- 3.2.3.3 Autonomous route planning and fleet management

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Case studies

- 3.9 Use cases

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Variational autoencoder

- 5.3 Generative adversarial networks

- 5.4 Recurrent neural networks

- 5.5 Long short-term memory networks

- 5.6 Transformers

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Software

- 6.3 Services

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Cloud

- 7.3 On-premises

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Route optimization

- 8.3 Demand forecasting

- 8.4 Warehouse and inventory management

- 8.5 Supply chain automation

- 8.6 Predictive maintenance

- 8.7 Risk management

- 8.8 Customized logistics solution

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021- 2034 (USD Million)

- 9.1 Key trends

- 9.2 Third party logistics providers

- 9.3 Freight forwarders

- 9.4 E-commerce companies

- 9.5 Manufacturers

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Amazon Web Services

- 11.2 DHL Group

- 11.3 FedEx

- 11.4 Flexport

- 11.5 Four Kites

- 11.6 Google

- 11.7 IBM

- 11.8 Locus

- 11.9 Maersk

- 11.10 Microsoft

- 11.11 NVIDIA

- 11.12 Open AI

- 11.13 Optimal Dynamics

- 11.14 Oracle

- 11.15 Palantir Technologies

- 11.16 Project44

- 11.17 Salesforce

- 11.18 SAP

- 11.19 UPS

- 11.20 XPO Logistics

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日