|

市場調査レポート

商品コード

1782128

加工産業用マテリアルハンドリング機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Processing Industry Material Handling Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 加工産業用マテリアルハンドリング機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年07月15日

発行: Global Market Insights Inc.

ページ情報: 英文 210 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

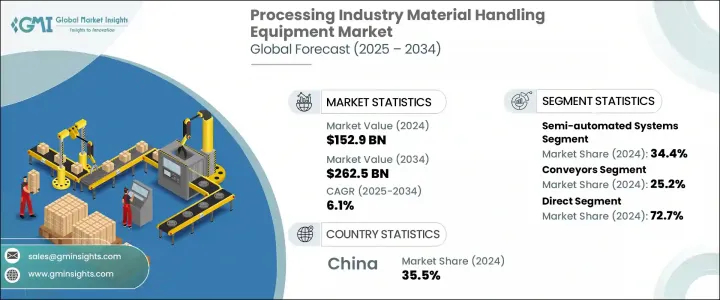

加工産業用マテリアルハンドリング機器の世界市場は、2024年には1,529億米ドルとなり、CAGR 6.1%で成長し、2034年には2,625億米ドルに達すると推定されています。

この着実な上昇は主に、加工部門全体で高度で自動化されたソリューションに対する需要が高まっていることに起因しています。この業界は、材料の移動、保管、管理方法を再構築するインテリジェント技術の統合によって、デジタルトランスフォーメーションをますます受け入れています。自動化はもはや将来の動向ではなく、業務効率、コスト削減、労働者の安全にとって不可欠な要素となっています。

加工業界全体の企業が、ロボット工学、AI、IoTなどのイノベーションを活用してワークフローを合理化し、リアルタイムの可視性を高め、より優れたプロセス制御によって競争力を獲得しています。これらのデジタルシステムは、生産量を向上させるだけでなく、手作業への依存を減らし、操作ミスを最小限に抑え、稼働時間を増やすことで、無駄のない製造をサポートします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,529億米ドル |

| 予測金額 | 2,625億米ドル |

| CAGR | 6.1% |

急速に進化する市場において、企業が生産性を高め、機敏性を維持しなければならないというプレッシャーの高まりに直面する中、最新のマテリアルハンドリング機器へのシフトは加速し続けています。スマートハンドリングソリューションの採用により、企業はダイナミックな生産ニーズに迅速に対応できるようになり、同時にエネルギー効率の高いオペレーションとマテリアルハンドリングの廃棄物の最小化を通じて持続可能性の目標もサポートできるようになりました。さらに、これらの自動化システムはさまざまな産業要件に合わせてカスタマイズできるため、精度、一貫性、適応性が重要な加工アプリケーションに最適です。

飲食品加工から化学、エレクトロニクスに至るまで、企業は流れを強化し、ボトルネックを減らし、施設内のシームレスな移動を保証する機器に投資しています。このような近代化の推進は、大規模な製造オペレーションを変革するだけでなく、完全自律型システムに多額の投資をせずに競争力を維持することを目指す中規模施設にとっても有益であることが証明されています。こうしたシフトの累積効果は、加工環境に特化したマテリアルハンドリング機器に対する力強い需要軌道となっています。

操作モードの観点から、市場は手動システム、半自動システム、完全自動システム、IoT対応スマートハンドリングシステムに分類されます。このうち、半自動化セグメントは2024年の市場リーダーとして浮上し、全体の収益の約34.4%を獲得しました。このセグメントは予測期間を通じてCAGR 4.4%以上で成長すると予測されています。半自動装置は、自動化の利点とオペレーター制御の最適な融合を提供し、柔軟性と精度の両方を必要とするビジネスにとって特に魅力的です。これらのシステムは、ワークフローが多様な施設に特に適しており、オペレーターは反復作業を機械化しながら、カスタマイズされたタスクを効率的に管理することができます。手頃な価格、統合のしやすさ、メンテナンス要件の低さから、自律運転に完全に移行することなく規模拡大を目指す多くの加工企業にとって、実用的な選択肢となっています。

アプリケーション別に見ると、市場はコンベア、クレーンホイスト、フォークリフト産業用トラック、無人搬送車(AGV)、保管・検索システム、ロボットマテリアルハンドリングシステム、バルクマテリアルハンドリング機器、その他に区分されます。コンベア分野は2024年に25.2%の収益シェアで市場をリードし、2025年から2034年にかけて5.5%以上のCAGRを記録すると予測されています。コンベアシステムが広く普及しているのは、加工工場内のさまざまな地点で材料をシームレスに搬送する能力があるためです。その設計の多様性は、軽量なものから大量の荷物に至るまで、幅広い物品の移動をサポートし、それによって処理能力を向上させ、処理時間を最小化します。これらのシステムは、連続的な生産サイクルで稼働する産業にとって不可欠な、中断のない材料フローを確保することで、プロセスの最適化に大きく貢献します。

市場は、流通チャネルに基づいて、直接チャネルと間接チャネルに分けられます。2024年には、直接販売セグメントが72.7%の収益シェアで支配的な地位を占めており、予測期間を通じてCAGR 4.7%以上で成長すると予測されています。直接販売チャネルは、購入者により適したソリューションと技術サポートを提供し、強力なバリュープロポジションを生み出します。しかし、間接部門は引き続き市場拡大において重要な役割を果たしています。間接部門は、顧客により広いリーチを可能にし、カスタマイズ、販売後のサポート、柔軟な資金調達オプションなど、特に中小企業にとって魅力的な追加サービスを提供します。このようなデュアルチャネルアプローチは、メーカーが個別対応サービスと幅広いアクセシビリティのバランスを維持するのに役立っています。

地域別では、中国が2024年のアジア太平洋の加工産業用マテリアルハンドリング機器市場でトップランナーに浮上し、地域シェアの約35.5%を確保しました。同国の市場は2034年までに20億米ドルを超えると予測されています。この優位性は、急速な産業開発、堅牢な製造インフラ、自動化とスマート製造の促進を目的とした政府の強力なイニシアチブによって後押しされています。継続的な都市化と地域の工業化への取り組みが、高度ハンドリングシステムに対する需要をさらに促進し、中国をアジア太平洋地域全体のこのセクターの成長への主要な貢献者にしています。

加工産業用マテリアルハンドリング機器市場の世界情勢を形成している著名な企業には、Daifuku、Crown Equipment Corporation、Dematic Group、GEA、Fives Group、Hyster-Yale Materials Handling、JBT Corporation、Intelligrated、Jungheinrich、Linde Material Handling、KION Group、Mitsubishi Logisnext、Tetra Pak、SSI Schaefer Group、Toyota Industries Corporationなどがあります。これらの企業は、競争力を強化し、インテリジェントで統合されたマテリアルハンドリングソリューションに対するニーズの高まりに対応するため、研究開発、パートナーシップ、世界展開に多額の投資を行っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 技術の進歩と自動化

- eコマースと物流の成長

- 工業および製造業の拡大

- 業界の潜在的リスク&課題

- メンテナンス費用と複雑さ

- 熟練労働力の不足

- 初期投資額が高め

- 機会

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 運用モード別

- 規制の枠組み

- 標準およびコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーターのファイブフォース分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:動作モード別、2021年~2034年

- 主要動向

- 手動ハンドリング装置

- 半自動システム

- 完全自動化システム

- IoT対応スマートハンドリングシステム

第6章 市場推計・予測:機器タイプ別、2021年~2034年

- 主要動向

- コンベア

- クレーンとホイスト

- フォークリフトと産業用トラック

- 無人搬送車(AGV)

- 保管および回収システム

- ロボットによるマテリアルハンドリングシステム

- バルクマテリアルハンドリング機器

- その他

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 効率的な資材移動

- 保管と整理

- 安全性の向上

- 生産性の向上

- その他

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 食品・飲料加工

- 化学・医薬品加工

- 鉱業・金属加工

- 医薬品製造

- 石油・ガス

- ロジスティクス

- 自動車・電子機器製造

- その他

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接

- 間接

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Crown Equipment Corporation

- Daifuku

- Dematic Group

- Fives Group

- GEA

- Hyster-Yale Materials Handling

- Intelligrated(a Honeywell company)

- JBT Corporation

- Jungheinrich

- KION Group

- Linde Material Handling

- Mitsubishi Logisnext

- SSI Schaefer Group

- Tetra Pak

- Toyota Industries Corporation

The Global Processing Industry Material Handling Equipment Market was valued at USD 152.9 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 262.5 billion by 2034. This steady rise is primarily attributed to the growing demand for advanced, automated solutions across processing sectors. The industry is increasingly embracing digital transformation, driven by the integration of intelligent technologies that are reshaping how materials are moved, stored, and managed. Automation is no longer a future trend-it has become an essential element of operational efficiency, cost reduction, and workforce safety.

Companies across processing industries are leveraging innovations such as robotics, AI, and IoT to streamline workflows, enhance real-time visibility, and gain a competitive edge through better process control. These digital systems not only improve production output but also support lean manufacturing by reducing reliance on manual labor, minimizing operational errors, and increasing uptime.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $152.9 Billion |

| Forecast Value | $262.5 Billion |

| CAGR | 6.1% |

As businesses face heightened pressure to boost productivity and maintain agility in rapidly evolving markets, the shift toward modern material handling equipment continues to accelerate. The adoption of smart handling solutions has enabled companies to respond faster to dynamic production needs, while also supporting sustainability goals through energy-efficient operations and minimizing material waste. Furthermore, these automated systems can be tailored for various industrial requirements, making them ideal for processing applications where precision, consistency, and adaptability are critical.

From food and beverage processing to chemicals and electronics, enterprises are investing in equipment that enhances flow, reduces bottlenecks, and ensures seamless intra-facility movement. This push toward modernization is not only transforming large manufacturing operations but is also proving beneficial for mid-sized facilities aiming to stay competitive without investing heavily in fully autonomous systems. The cumulative effect of these shifts is a robust demand trajectory for material handling equipment tailored specifically to processing environments.

In terms of operation mode, the market is categorized into manual systems, semi-automated systems, fully automated systems, and IoT-enabled smart handling systems. Among these, the semi-automated segment emerged as the market leader in 2024, capturing around 34.4% of the overall revenue. This segment is forecasted to grow at a CAGR of over 4.4% through the forecast period. Semi-automated equipment offers an optimal blend of automation benefits and operator control, which is particularly appealing to businesses that require both flexibility and precision. These systems are especially suitable for facilities with varying workflows, enabling operators to manage customized tasks efficiently while mechanizing repetitive activities. Their affordability, ease of integration, and lower maintenance requirements make them a practical choice for many processing firms aiming to scale without transitioning fully to autonomous operations.

On the basis of application, the market is segmented into conveyors, cranes and hoists, forklifts and industrial trucks, automated guided vehicles (AGVs), storage and retrieval systems, robotic material handling systems, bulk material handling equipment, and others. The conveyors segment led the market in 2024 with a revenue share of 25.2%, and it is anticipated to register a CAGR of over 5.5% from 2025 to 2034. The widespread deployment of conveyor systems is due to their ability to transport materials seamlessly across different points within processing plants. Their design versatility supports the movement of a wide range of goods, from lightweight items to bulk loads, thereby improving throughput and minimizing handling times. These systems contribute significantly to process optimization by ensuring uninterrupted material flow, which is essential for industries that operate on continuous production cycles.

The market, based on distribution channel, is divided into direct and indirect channels. In 2024, the direct sales segment held the dominant position with a revenue share of 72.7% and is projected to grow at a CAGR of over 4.7% throughout the forecast period. Direct channels offer buyers better access to tailored solutions and technical support, creating strong value propositions. However, the indirect segment continues to play a critical role in market expansion. It enables broader customer reach and provides additional services such as customization, post-sale assistance, and flexible financing options, which are especially appealing to small and mid-sized enterprises. This dual-channel approach helps manufacturers maintain a balance between personalized service and wide-scale accessibility.

Regionally, China emerged as the front-runner in the Asia-Pacific processing industry material handling equipment market in 2024, securing approximately 35.5% of the regional share. The country's market is projected to exceed USD 2 billion by 2034. This dominance is fueled by rapid industrial development, a robust manufacturing infrastructure, and strong governmental initiatives aimed at boosting automation and smart manufacturing. Continued urbanization and regional industrialization efforts further drive the demand for advanced handling systems, making China a key contributor to the sector's growth across APAC.

Prominent players shaping the global landscape of the processing industry material handling equipment market include Daifuku, Crown Equipment Corporation, Dematic Group, GEA, Fives Group, Hyster-Yale Materials Handling, JBT Corporation, Intelligrated, Jungheinrich, Linde Material Handling, KION Group, Mitsubishi Logisnext, Tetra Pak, SSI Schaefer Group, and Toyota Industries Corporation. These companies are investing heavily in R&D, partnerships, and global expansions to strengthen their competitive positions and cater to the increasing need for intelligent and integrated material handling solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Mode of operation

- 2.2.2 Equipment type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements and automation

- 3.2.1.2 Growth of e-commerce and logistics

- 3.2.1.3 Expansion of industrial and manufacturing sectors

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Maintenance expenses and complexity

- 3.2.2.2 Shortage of skilled workforce

- 3.2.2.3 High initial investment

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By mode of operation

- 3.7 Regulatory framework

- 3.7.1 standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's five forces analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Mode of Operation, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Manual handling equipment

- 5.3 Semi-automated systems

- 5.4 Fully automated systems

- 5.5 IoT-enabled smart handling systems

Chapter 6 Market Estimates & Forecast, By Equipment Type, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Conveyors

- 6.3 Cranes & Hoists

- 6.4 Forklifts & Industrial Trucks

- 6.5 Automated Guided Vehicles (AGVs)

- 6.6 Storage & Retrieval Systems

- 6.7 Robotic Material Handling Systems

- 6.8 Bulk Material Handling Equipment

- 6.9 Other

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Efficient movement of materials

- 7.3 Storage and organization

- 7.4 Improving safety

- 7.5 Increasing productivity

- 7.6 Other

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Food & beverage processing

- 8.3 Chemical and pharmaceutical processing

- 8.4 Mining & metals processing

- 8.5 Pharmaceutical manufacturing

- 8.6 Oil & gas

- 8.7 Logistics

- 8.8 Automotive and electronics manufacturing

- 8.9 Other

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Crown Equipment Corporation

- 11.2 Daifuku

- 11.3 Dematic Group

- 11.4 Fives Group

- 11.5 GEA

- 11.6 Hyster-Yale Materials Handling

- 11.7 Intelligrated (a Honeywell company)

- 11.8 JBT Corporation

- 11.9 Jungheinrich

- 11.10 KION Group

- 11.11 Linde Material Handling

- 11.12 Mitsubishi Logisnext

- 11.13 SSI Schaefer Group

- 11.14 Tetra Pak

- 11.15 Toyota Industries Corporation