|

市場調査レポート

商品コード

1782127

AIハードウェアの市場機会、成長促進要因、産業動向分析、2025年~2034年予測AI Hardware Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| AIハードウェアの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年07月15日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

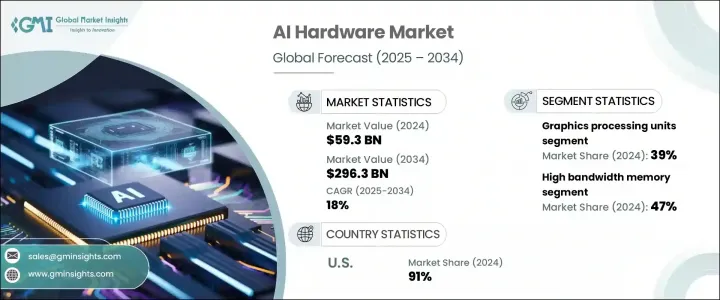

AIハードウェアの世界市場規模は、2024年に593億米ドルとなり、CAGR 18%で成長し、2034年には2,963億米ドルに達すると推定されています。

この力強い成長軌道は、多様な分野で人工知能が広く採用され、ハイパフォーマンス・コンピューティング・インフラの必要性が大幅に高まったことが背景にあります。複雑な計算を必要とするAIモデルの導入が進むにつれ、大規模な処理タスクを処理できる専用のAIハードウェアへの依存度が高まっています。

企業は、より高速なデータ・スループットだけでなく、低レイテンシやエネルギー効率にも対応できるハードウェアへの移行を進めています。この動向はクラウド環境だけにとどまらず、エッジコンピューティング環境全体にもAIが導入され、産業システム、モバイルデバイス、組み込みソリューションにおけるリアルタイムの意思決定を後押ししています。エッジAIの普及は、クラウドサービスに常時依存することなく独立して動作可能なプロセッサとメモリユニットの需要をさらに押し上げています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 593億米ドル |

| 予測金額 | 2,963億米ドル |

| CAGR | 18% |

プロセッサー分野全体では、AIハードウェア市場は、グラフィックス・プロセッシング・ユニット(GPU)、中央演算処理装置(CPU)、テンソル・プロセッシング・ユニット(TPU)、特定用途向け集積回路(ASIC)、フィールド・プログラマブル・ゲート・アレイ(FPGA)、ニューラル・プロセッシング・ユニット(NPU)に区分されます。このうち、GPUは2024年時点で市場全体の約39%を占め、圧倒的なシェアを占めています。2025年から2034年にかけて、このセグメントのCAGRは18%を超える成長が見込まれています。GPUの優位性は、並列コンピューティング、メモリ処理、推論モデルの学習と実行における効率性において比類のない能力を持つことに起因しています。これらの機能により、GPUはエンタープライズグレードのAIプラットフォームにも、複雑なモデル開発にスケーラブルな性能を必要とする研究機関にも不可欠なものとなっています。

メモリとストレージという切り口で見た場合、AIハードウェア市場には、高帯域幅メモリ(HBM)、AIに最適化されたDRAM、不揮発性メモリ、新興メモリ技術が含まれます。2024年には、高帯域幅メモリセグメントが最大シェアを獲得し、市場全体の47%を占める。このセグメントは予測期間中にCAGR 19%以上で拡大すると予測されています。この需要の急増は、AIシステムにおける速度と帯域幅のニーズの高まりが大きく影響しています。AIモデルがより洗練され、データ量が多くなるにつれて、高帯域幅メモリはほぼ瞬時のデータ検索を可能にし、これは特にリアルタイムアプリケーションでシームレスなパフォーマンスを達成するために不可欠です。この機能により、企業は待ち時間を最小限に抑え、応答性を高め、ワークロード処理をより適切に管理できるようになります。

アプリケーション別では、データセンターとクラウド・コンピューティングが引き続き市場収益に最も貢献しています。このセグメントは、スケーラブルで高性能なインフラへのニーズが高まるにつれて急速に拡大し続けています。膨大な学習と推論を必要とするAIモデルの急増は、AIワークロードをサポートするために特別に設計されたデータセンターの構築を企業に促しています。これらのセンターには、AIを効率的に実行するために調整された最先端のアクセラレータとコンポーネントが装備されています。企業は、現在のAIのニーズを満たすだけでなく、将来のモデルの需要も見越した専用インフラへの投資を優先しています。

地域別では、米国が北米のAIハードウェア市場をリードし、地域別収益シェアの約91%を占め、2024年には約198億米ドルを創出しました。この牙城は、技術革新におけるリーダーシップ、強固なサプライチェーン、高度な半導体製造能力へのアクセスによる。米国は、ハードウェア企業、研究機関、クラウドサービスプロバイダーなどの豊富なエコシステムに支えられ、依然としてAIハードウェア開発の世界ハブとなっています。

AIハードウェア市場の主要企業には、NVIDIA、Intel、Qualcomm Technologies、Advanced Micro Devices(AMD)、Apple、Google、Amazon Web Services(AWS)、Microsoft、IBM、Samsung Electronicsなどがあります。これらの企業は、AI搭載システムの進化するニーズをサポートするため、カスタムチップ、高性能プロセッサ、次世代アクセラレータの開発に一貫して投資しています。彼らの努力は、世界のAIハードウェア状況の次の段階を形成する上で極めて重要です。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 生成AIアプリケーションの普及

- エッジAI導入の急速な拡大

- クラウドとデータセンターの導入

- ヘルスケアとライフサイエンスにおけるAI

- 政府のAI投資

- 業界の潜在的リスク&課題

- 高い消費電力と冷却ニーズ

- 世界の半導体供給制約

- 市場機会

- デバイス内AIの需要の高まり

- 政府の半導体インセンティブ

- AIスーパーコンピューティングとハイパースケール拡張

- 業界特化型AIアプリケーションの成長

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 先端プロセスノード開発(3nm、2nm)

- 高帯域幅メモリ(HBM)の進化

- チップレットアーキテクチャとモジュール設計

- 新興技術

- AI向け量子コンピューティングハードウェア

- フォトニックコンピューティングと光AIハードウェア

- ニューロモルフィックコンピューティングアーキテクチャ

- 高度なメモリ技術

- 現在の技術動向

- ケーススタディ

- ユースケース

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:プロセッサー別、2021年~2034年

- 主要動向

- グラフィックス処理装置(GPU)

- トレーニング

- 推論

- エッジ

- データセンター

- 中央処理装置(CPU)

- AI最適化

- AIアクセラレーション搭載サーバーCPU

- エッジコンピューティング

- テンソル処理ユニット(TPU)

- クラウド

- エッジ

- カスタムデザイン

- 特定用途向け集積回路(ASIC)

- AIトレーニング

- AI推論

- カスタムAI

- フィールドプログラマブルゲートアレイ(FPGA)

- AI最適化

- エッジAI

- 再構成可能なコンピューティングプラットフォーム

- ニューラルプロセッシングユニット(NPU)

- スマートフォン

- エッジAI

- IoT

第6章 市場推計・予測:メモリとストレージ別、2021年~2034年

- 主要動向

- 高帯域幅メモリ(HBM)

- AI最適化DRAM

- 不揮発性メモリ

- 新興メモリ技術

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- データセンターとクラウドコンピューティング

- 自動車および輸送

- ヘルスケアとライフサイエンス

- 家電

- 工業および製造業

- 金融サービス

- 通信

第8章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- クラウドベース

- オンプレミス

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ベトナム

- フィリピン

- オーストラリア・ニュージーランド

- シンガポール

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Advanced Micro Devices

- Amazon Web Services(AWS)

- Apple

- ARM

- Broadcom

- Cerebra’s Systems

- Fujitsu

- Graph core

- IBM

- Intel

- Marvell Technology

- Micron Technology

- Microsoft

- NVIDIA

- Qualcomm Technologies

- Samsung Electronics

- SiPearl

- SK Hynix

- Tenstorrent

The Global AI Hardware Market was valued at USD 59.3 billion in 2024 and is estimated to grow at a CAGR of 18% to reach USD 296.3 billion by 2034. This strong growth trajectory is driven by the widespread adoption of artificial intelligence across diverse sectors, which has significantly amplified the need for high-performance computing infrastructure. As organizations increasingly deploy AI models with complex computational demands, there is a growing reliance on dedicated AI hardware capable of handling large-scale processing tasks.

Businesses are transitioning toward hardware that can support not only faster data throughput but also lower latency and greater energy efficiency. This trend is not limited to cloud environments alone; AI is also being implemented across edge computing environments, powering real-time decision-making in industrial systems, mobile devices, and embedded solutions. The proliferation of edge AI is further boosting demand for processors and memory units capable of operating independently without constant reliance on cloud services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $59.3 Billion |

| Forecast Value | $296.3 Billion |

| CAGR | 18% |

Across the processor landscape, the AI hardware market is segmented into graphics processing units (GPUs), central processing units (CPUs), tensor processing units (TPUs), application-specific integrated circuits (ASICs), field-programmable gate arrays (FPGAs), and neural processing units (NPUs). Among these, GPUs held the dominant share of the market in 2024, accounting for approximately 39% of total revenue. From 2025 to 2034, this segment is expected to grow at a CAGR exceeding 18%. The dominance of GPUs can be attributed to their unmatched capabilities in parallel computing, memory handling, and their efficiency in training and running inference models. These features have made GPUs essential to both enterprise-grade AI platforms and research institutions that require scalable performance for complex model development.

When viewed through the lens of memory and storage, the AI hardware market includes high bandwidth memory (HBM), AI-optimized DRAM, non-volatile memory, and emerging memory technologies. In 2024, the high bandwidth memory segment captured the largest share, contributing 47% of the total market. The segment is forecasted to expand at a CAGR of over 19% during the forecast period. This surge in demand is largely influenced by the growing need for speed and bandwidth in AI systems. As AI models become more sophisticated and data-heavy, high bandwidth memory enables near-instant data retrieval, which is critical for achieving seamless performance, particularly in real-time applications. This capability allows enterprises to minimize latency, enhance responsiveness, and better manage workload processing.

On the basis of application, data center and cloud computing remain the largest contributors to market revenue. The segment continues to expand rapidly as the need for scalable, high-performance infrastructure intensifies. The proliferation of AI models with massive training and inference requirements is driving companies to build data centers specifically designed to support AI workloads. These centers are equipped with cutting-edge accelerators and components tailored for efficient AI execution. Organizations are prioritizing investment in purpose-built infrastructure that not only meets current AI needs but also anticipates the demands of future models.

In regional terms, the United States led the AI hardware market in North America, accounting for nearly 91% of the regional revenue share and generating around USD 19.8 billion in 2024. This stronghold is driven by the country's leadership in technology innovation, a robust supply chain, and access to advanced semiconductor manufacturing capabilities. The U.S. remains a global hub for AI hardware development, supported by a rich ecosystem of hardware companies, research institutions, and cloud service providers.

Leading companies in the AI hardware market include NVIDIA, Intel, Qualcomm Technologies, Advanced Micro Devices (AMD), Apple, Google, Amazon Web Services (AWS), Microsoft, IBM, Samsung Electronics, and others. These firms are consistently investing in the development of custom chips, high-performance processors, and next-generation accelerators to support the evolving needs of AI-powered systems. Their efforts are crucial in shaping the next phase of the global AI hardware landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Processor

- 2.2.3 Memory and storage

- 2.2.4 Application

- 2.2.5 Deployment

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Proliferation of generative AI applications

- 3.2.1.2 Rapid expansion of edge AI deployment

- 3.2.1.3 Cloud & data center adoption

- 3.2.1.4 AI in healthcare & life sciences

- 3.2.1.5 Government AI investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High power consumption & cooling needs

- 3.2.2.2 Global chip supply constraints

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for on-device AI

- 3.2.3.2 Government semiconductor incentives

- 3.2.3.3 AI supercomputing & hyperscale expansion

- 3.2.3.4 Growth of industry-specific AI applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Advanced process node development (3nm, 2nm)

- 3.7.1.2 High bandwidth memory (HBM) evolution

- 3.7.1.3 Chiplet architecture and modular design

- 3.7.2 Emerging technologies

- 3.7.2.1 Quantum computing hardware for AI

- 3.7.2.2 Photonic computing and optical AI hardware

- 3.7.2.3 Neuromorphic computing architectures

- 3.7.2.4 Advanced memory technologies

- 3.7.1 Current technological trends

- 3.8 Case studies

- 3.9 Use cases

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Processor, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Graphics processing unit (GPU)

- 5.2.1 Training

- 5.2.2 Inference

- 5.2.3 Edge

- 5.2.4 Data center

- 5.3 Central processing unit (CPU)

- 5.3.1 AI-optimized

- 5.3.2 Server CPU with AI acceleration

- 5.3.3 Edge computing

- 5.4 Tensor processing unit (TPU)

- 5.4.1 Cloud

- 5.4.2 Edge

- 5.4.3 Custom designs

- 5.5 Application-specific integrated circuit (ASIC)

- 5.5.1 AI training

- 5.5.2 AI inference

- 5.5.3 Custom AI

- 5.6 Field-programmable gate arrays (FPGA)

- 5.6.1 AI-optimized

- 5.6.2 Edge AI

- 5.6.3 Reconfigurable computing platforms

- 5.7 Neural processing units (NPU)

- 5.7.1 Smartphone

- 5.7.2 Edge AI

- 5.7.3 IoT

Chapter 6 Market Estimates & Forecast, By Memory & Storage, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 High bandwidth memory (HBM)

- 6.3 AI-optimized DRAM

- 6.4 Non-volatile memory

- 6.5 Emerging memory technologies

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Data center and cloud computing

- 7.3 Automotive and transportation

- 7.4 Healthcare and life sciences

- 7.5 Consumer electronics

- 7.6 Industrial and manufacturing

- 7.7 Financial services

- 7.8 Telecommunications

Chapter 8 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Cloud-Based

- 8.3 On-Premises

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Vietnam

- 9.4.6 Philippines

- 9.4.7 ANZ

- 9.4.8 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Advanced Micro Devices

- 10.2 Amazon Web Services (AWS)

- 10.3 Apple

- 10.4 ARM

- 10.5 Broadcom

- 10.6 Cerebra’s Systems

- 10.7 Fujitsu

- 10.8 Google

- 10.9 Graph core

- 10.10 IBM

- 10.11 Intel

- 10.12 Marvell Technology

- 10.13 Micron Technology

- 10.14 Microsoft

- 10.15 NVIDIA

- 10.16 Qualcomm Technologies

- 10.17 Samsung Electronics

- 10.18 SiPearl

- 10.19 SK Hynix

- 10.20 Tenstorrent