十二指腸潰瘍治療の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Duodenal Ulcer Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1782126

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

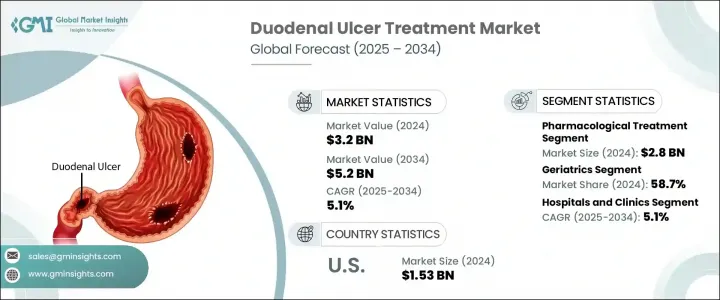

世界の十二指腸潰瘍治療市場は、2024年には32億米ドルと評価され、CAGR 5.1%で成長し、2034年には52億米ドルに達すると推定されています。

この成長には、世界の十二指腸潰瘍患者の増加が大きく寄与しており、多くの場合、栄養不良、アルコール摂取、喫煙習慣が関係しています。高齢者は消化管合併症にかかりやすいため、高齢化も治療ソリューションの需要増に寄与しています。H2受容体拮抗薬やプロトンポンプ阻害薬(PPI)などの薬剤は、その確実な酸抑制能力と良好な安全性プロファイルにより、使用量が増加しています。

多くの治療計画では、十二指腸潰瘍の主な原因であるヘリコバクターピロリ感染を標的とする抗生物質と併用されています。さらに、スクラルファートやミソプロストールのような薬剤は、胃粘膜の保護作用で人気を集めています。AI診断、モバイルヘルスツール、遠隔医療の統合は、アクセシビリティと患者中心の治療に焦点を当て、潰瘍治療の提供方法を再構築しています。デジタルヘルスモデルと予防戦略を採用するヘルスケアシステムが増えるにつれて、信頼性の高い十二指腸潰瘍治療に対する需要はすべての地域で拡大し続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 32億米ドル |

| 予測金額 | 52億米ドル |

| CAGR | 5.1% |

薬理療法セグメントは、2024年に28億米ドルを生み出しました。この優位性は、PPIやH2ブロッカーのような薬剤クラス別が、迅速な症状緩和と一貫した酸コントロールに有効であることに起因します。これらの薬剤は、使いやすさ、経口投与、全体的な利便性から広く好まれており、在宅ケアや患者の長期的なアドヒアランスを支えています。侵襲的な処置なしに効果的に症状を管理できることから、ヘルスケアプロバイダーと患者の両方にとって第一選択となり、この治療カテゴリーの成長を後押ししています。

老年医療分野は2024年に58.7%のシェアを占めました。加齢に伴う消化管保護機能の低下は、高齢者の潰瘍形成に対する脆弱性を増大させ、高齢者を治療オプションの主要な消費者グループにしています。さらに、他の加齢関連疾患の治療のために非ステロイド性抗炎症薬(NSAIDs)を慢性的に使用することは、この層における十二指腸潰瘍のリスクを著しく高める。このように潰瘍形成の誘因に持続的に曝されることから、高齢患者に合わせた長期的かつ予防的なケアアプローチが求められています。

米国の十二指腸潰瘍治療2025年の市場規模は15億3,000万米ドル。米国市場は、ヘリコバクターピロリ感染の有病率の増加、非ステロイド性抗炎症薬(NSAID)の頻繁な使用、食生活の危険因子により成長を続けています。同国では早期発見が重視され、しっかりとした治療プロトコールがタイムリーな診断と介入を支えています。ヘルスケア提供における強力なインフラストラクチャーは、広範な啓発キャンペーンや最先端の診断サービスへのアクセスとともに、高い治療普及率を保証しています。治療研究と技術革新への継続的な投資も、世界の情勢を形成する上で同国の役割を強化しています。

この市場における主要な業界企業には、 Takeda Pharmaceutical, Abbott Laboratories, Boehringer Ingelheim, Cipla, Eisai, GlaxoSmithKline, Pfizer, Merck, Lupin, Novartis, Ferozsons Laboratories, Sun Pharma, Sanofi, and AstraZeneca.などがいます。市場ポジションを強化するため、十二指腸潰瘍治療領域で事業を展開する企業は、様々な戦略的取り組みを実施しています。対症療法とヘリコバクターピロリ菌のような根本原因の両方をターゲットにした先進的な医薬品開発への投資は、重要な焦点となっています。

多くの企業は、パートナーシップ、現地製造、地域マーケティング戦略を通じて世界展開を強化しています。スマートモニタリングや遠隔医療対応治療のようなデジタルヘルス統合は、患者エンゲージメントとアドヒアランスを高めるために検討されています。さらに、企業は有効性とコンプライアンスの向上を目指し、併用療法を含むポートフォリオの多様化を進めています。戦略的な価格設定、患者支援プログラム、医師による教育キャンペーンも、より広範な市場浸透を支えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- ヘリコバクター・ピロリ感染率の上昇

- 遠隔医療とデジタル診断の拡大

- 胃腸の健康に対する意識の高まり

- 制酸療法における技術的進歩

- 業界の潜在的リスク&課題

- 内視鏡検査とpHモニタリング検査の高コスト

- 副作用

- 市場機会

- 発展途上地域におけるヘルスケアの拡大

- 手頃な価格の医薬品アクセスのための官民パートナーシップの拡大

- 促進要因

- 成長可能性分析

- パイプライン分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 規制情勢

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:治療の種類別、2021年~2034年

- 主要動向

- 薬物治療

- 薬物クラス

- プロトンポンプ阻害剤

- H2拮抗薬

- 抗生物質

- その他の薬物クラス

- 薬の種類

- ブランド治療

- ジェネリック医薬品

- 投与経路

- 経口

- 非経口

- 薬物クラス

- 手術

第6章 市場推計・予測:年齢別、2021年~2034年

- 主要動向

- 成人

- 高齢者

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院と診療所

- 在宅ケアの設定

- 外来手術センター

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- AstraZeneca

- Boehringer Ingelheim

- Cipla

- Eisai

- Ferozsons Laboratories

- GlaxoSmithKline

- Lupin

- Merck

- Novartis

- Pfizer

- Sanofi

- Sun Pharma

- Takeda Pharmaceutical

目次

The Global Duodenal Ulcer Treatment Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 5.2 billion by 2034. This growth is largely fueled by rising cases of duodenal ulcers worldwide, often linked to poor nutrition, alcohol intake, and smoking habits. An aging population also contributes to increased demand for treatment solutions, as older individuals are more susceptible to gastrointestinal complications. Medications such as H2 receptor blockers and proton pump inhibitors (PPIs) are seeing heightened usage due to their reliable acid-suppressing abilities and favorable safety profiles.

In many treatment plans, these are now used in conjunction with antibiotics that target Helicobacter pylori infections- a leading cause of duodenal ulcers. Additionally, agents like sucralfate and misoprostol are gaining traction for their protective effects on the gastric lining. The integration of AI diagnostics, mobile health tools, and telemedicine is reshaping how ulcer care is delivered, with a focus on accessibility and patient-centered treatment. As more healthcare systems adopt digital health models and preventive strategies, the demand for reliable duodenal ulcer treatments continues to grow across all regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 5.1% |

The pharmacological therapies segment generated USD 2.8 billion in 2024. This dominance stems from the effectiveness of drug classes like PPIs and H2 blockers in providing quick symptom relief and consistent acid control. These medications are widely preferred for their ease of use, oral delivery, and overall convenience, which support home-based care and long-term patient adherence. Their ability to manage symptoms effectively without invasive procedures makes them the first choice for both healthcare providers and patients, pushing growth in this treatment category.

The geriatrics segment held a 58.7% share in 2024. Age-related declines in gastrointestinal protection increase vulnerability to ulcer formation among older adults, making them the primary consumer group for treatment options. Additionally, chronic use of non-steroidal anti-inflammatory drugs (NSAIDs) to manage other age-related conditions significantly raises the risk of duodenal ulcers in this demographic. This persistent exposure to ulcerogenic triggers calls for long-term and preventive care approaches tailored to senior patients.

United States Duodenal Ulcer Treatment Market was valued at USD 1.53 billion in 2025. The American market continues to grow due to the increasing prevalence of Helicobacter pylori infections, frequent NSAID use, and dietary risk factors. The country's emphasis on early detection and robust treatment protocols supports timely diagnosis and intervention. Strong infrastructure in healthcare delivery, along with extensive awareness campaigns and access to cutting-edge diagnostic services, ensures high treatment adoption. Ongoing investments in therapeutic research and innovation also bolster the country's role in shaping the global duodenal ulcer treatment landscape.

Key industry players in this market include Takeda Pharmaceutical, Abbott Laboratories, Boehringer Ingelheim, Cipla, Eisai, GlaxoSmithKline, Pfizer, Merck, Lupin, Novartis, Ferozsons Laboratories, Sun Pharma, Sanofi, and AstraZeneca. To strengthen their market position, companies operating in the duodenal ulcer treatment space are embracing various strategic initiatives. Investment in advanced drug development targeting both symptom management and root causes, such as Helicobacter pylori, is a key focus.

Many firms are enhancing their global reach through partnerships, local manufacturing, and regional marketing strategies. Digital health integration, such as smart monitoring and telehealth-enabled treatment, is being explored to boost patient engagement and adherence. Additionally, firms are diversifying portfolios to include combination therapies, aiming to improve efficacy and compliance. Strategic pricing, patient assistance programs, and physician education campaigns also support broader market penetration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Treatment type

- 2.2.3 Age group

- 2.2.4 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of helicobacter pylori infections

- 3.2.1.2 Expansion of telemedicine and digital diagnostics

- 3.2.1.3 Growing awareness of gastrointestinal health

- 3.2.1.4 Technological advancements in acid-suppressing therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of endoscopic and pH monitoring procedures

- 3.2.2.2 Adverse effects

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding healthcare in developing regions

- 3.2.3.2 Growing public-private partnerships for affordable drug access

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pipeline analysis

- 3.5 Future market trends

- 3.6 Technology and innovation landscape

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 Middle East and Africa

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pharmacological treatment

- 5.2.1 Drug class

- 5.2.1.1 Proton pump inhibitors

- 5.2.1.2 H2 antagonists

- 5.2.1.3 Antibiotics

- 5.2.1.4 Other drug classes

- 5.2.2 Medication type

- 5.2.2.1 Branded Treatment

- 5.2.2.2 Generics

- 5.2.3 Route of administration

- 5.2.3.1 Oral

- 5.2.3.2 Parenteral

- 5.2.1 Drug class

- 5.3 Surgery

Chapter 6 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Adults

- 6.3 Geriatrics

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Homecare settings

- 7.4 Ambulatory surgical centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AstraZeneca

- 9.3 Boehringer Ingelheim

- 9.4 Cipla

- 9.5 Eisai

- 9.6 Ferozsons Laboratories

- 9.7 GlaxoSmithKline

- 9.8 Lupin

- 9.9 Merck

- 9.10 Novartis

- 9.11 Pfizer

- 9.12 Sanofi

- 9.13 Sun Pharma

- 9.14 Takeda Pharmaceutical

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日