消化性潰瘍治療市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Peptic Ulcers Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773398

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

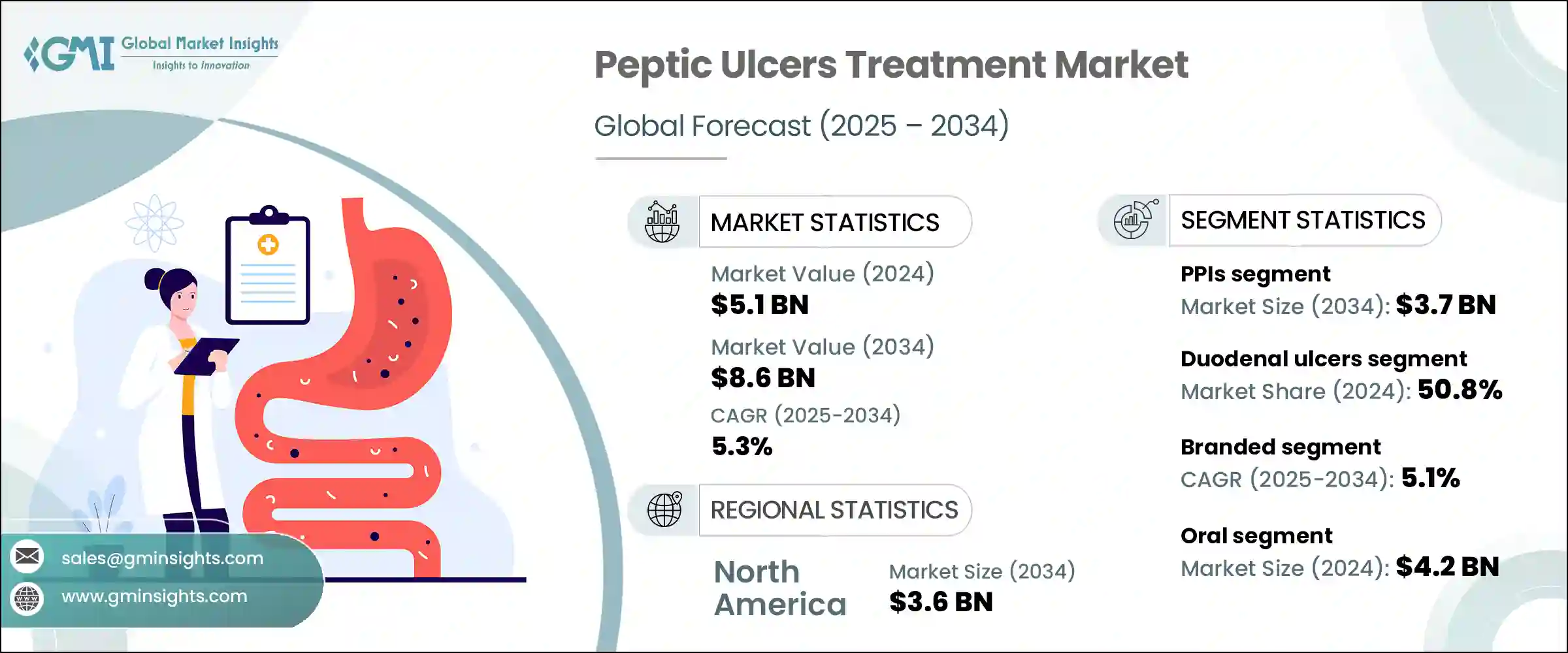

消化性潰瘍治療の世界市場規模は2024年に51億米ドルとなり、CAGR 5.3%で成長し、2034年には86億米ドルに達すると推定されます。

市場成長の主な要因は、成人における消化器疾患の罹患率の上昇と、革新的な医薬品ソリューションの継続的な開発です。この需要に大きく貢献しているのは、ヘリコバクター・ピロリ感染症の蔓延であり、世界的に消化性潰瘍の主要な原因となっています。世界保健機関が指摘するように、この感染症は世界人口の半数以上が罹患しており、特に低・中所得地域での罹患率が高いです。この憂慮すべき蔓延により、消化性潰瘍を管理・除去するためのより効果的な治療オプションに対する需要が加速すると予想されます。

また、非ステロイド性抗炎症薬の誤用が増加していることも、市場拡大を後押しする要因のひとつです。これと並行して、診断法の進歩や、二重・三重併用療法を含む革新的な治療レジメンの採用が増加していることで、患者の回復率が向上し、潰瘍の再発が最小限に抑えられています。これらの要因は、先進国および新興諸国における意識の高まりやヘルスケアへのアクセスの向上と相まって、消化性潰瘍治療ソリューションに対する安定した需要を今後数年間維持すると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 51億米ドル |

| 予測金額 | 86億米ドル |

| CAGR | 5.3% |

プロトンポンプ阻害薬(PPI)分野は、2024年に23億米ドルを売り上げ、2034年にはCAGR 5.1%を記録して37億米ドルに達すると予測されています。PPIは胃酸レベルを下げ、治癒を促進し、痛みを和らげる効果があるため、潰瘍治療の要となっています。その確実な有効性と最小限の副作用により、治療レジメンとして広く好まれています。H.ピロリ除菌のための多剤併用療法への貢献は、市場の支配的地位をさらに強固なものにしています。臨床の現場では、特にPPIを4~8週間の治療期間にわたって投与した場合、高い治癒成功率が常に報告されています。

十二指腸潰瘍は2024年に50.8%のシェアを占め、予測期間を通じて大きな成長を遂げると思われます。十二指腸潰瘍は通常、小腸の上部に形成され、主に細菌感染や非ステロイド性抗炎症薬の長期使用によって引き起こされます。これらの潰瘍は幅広い人口に蔓延しており、明確な症状を呈することが多いため、迅速な診断と迅速な介入が可能となり、高い治療率を支えています。

北米の消化性潰瘍治療市場は2024年に21億米ドルを創出し、2034年にはCAGR 5.5%で成長して36億米ドルに達すると予測されています。この地域の優位性は、NSAID関連の合併症やピロリ菌感染症が多いことに起因しています。ヘルスケアの枠組みが確立していること、先進的な医薬品へのアクセスが向上していること、消化管ケアや予防医療に対する意識が高まっていることなどが、この地域の市場地位の高さに寄与しています。さらに、主要製薬企業の積極的なプレゼンスがこの地域の成長を支え続けています。

消化性潰瘍治療分野の主要企業は、市場での地位を固めるため、さまざまな戦略的取り組みに注力しています。その多くは、より有効性が高く副作用の少ない新しい治療法を開発するため、研究開発に多額の投資を行っています。特に併用療法を中心とした治療法の改善は、治療のアドヒアランスを高め、再発を最小限に抑えることを目的としています。

各社はまた、治療への幅広いアクセスを確保するため、製造能力を拡大し、世界サプライチェーンを強化しています。さらに、企業は戦略的パートナーシップを結び、M&Aを行うことで、自社のポートフォリオと地理的プレゼンスを拡大しようとしています。特に、診断率や治療率が着実に上昇している新興ヘルスケア市場では、ターゲットを絞った啓発キャンペーンや医師教育プログラムによって、製品の認知度やブランドの信頼性がさらに高まっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- ヘリコバクター・ピロリ感染症の罹患率の上昇

- 高齢化人口の増加

- 研究開発資金と活動の拡大

- 業界の潜在的リスク&課題

- PPIの長期使用による副作用

- 市場機会

- 新しい治療法とドラッグデリバリーの革新

- オンライン薬局の拡大

- 促進要因

- 成長可能性分析

- パイプライン分析

- 規制情勢

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 拡張計画

第5章 市場推計・予測:薬剤タイプ別、2021年~2034年

- 主要動向

- プロトンポンプ阻害剤(PPI)

- H2受容体拮抗薬

- 制酸剤

- 抗生物質

- 細胞保護剤

- その他の薬物タイプ

第6章 市場推計・予測:潰瘍タイプ別、2021年~2034年

- 主要動向

- 胃潰瘍

- 十二指腸潰瘍

- 食道潰瘍

第7章 市場推計・予測:医薬品タイプ別、2021年~2034年

- 主要動向

- ブランド

- ジェネリック医薬品

第8章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 経口

- 非経口

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 小売薬局

- オンライン薬局

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- AstraZeneca

- Aurobindo Pharma

- Azurity Pharmaceuticals

- Cadila Healthcare

- Dr. Reddy’s Laboratories

- Eisai

- GlaxoSmithKline

- Granules India

- Pfizer

- Phathom Pharmaceuticals

- Ranbaxy Laboratories

- Strides Pharma

- Sun Pharma

- Takeda

目次

The Global Peptic Ulcers Treatment Market was valued at USD 5.1 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 8.6 billion by 2034. The market growth is largely driven by the rising incidence of gastrointestinal conditions among adults and the continued development of innovative pharmaceutical solutions. A key contributor to this demand is the widespread prevalence of Helicobacter pylori infections, which remain a dominant cause of peptic ulcers globally. As noted by global health bodies, this infection affects more than half the world's population, with particularly high rates in low- and middle-income regions. This alarming prevalence is expected to accelerate the demand for more effective treatment options to manage and eliminate the condition.

Another factor fueling market expansion is the increasing misuse of non-steroidal anti-inflammatory drugs, which often damage the stomach lining and lead to ulcer formation. Alongside this, advancements in diagnostics and the rising adoption of innovative treatment regimens-including dual and triple combination therapies-are improving patient recovery rates and minimizing ulcer recurrence. These factors, combined with rising awareness and enhanced healthcare accessibility in both developed and emerging countries, are expected to sustain steady demand for peptic ulcer treatment solutions in the coming years.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.1 Billion |

| Forecast Value | $8.6 Billion |

| CAGR | 5.3% |

The proton pump inhibitors (PPIs) segment generated USD 2.3 billion in 2024 and is forecasted to hit USD 3.7 billion by 2034, registering a CAGR of 5.1%. PPIs have become the cornerstone of ulcer therapy due to their effectiveness in reducing gastric acid levels, accelerating healing, and relieving pain. Their dependable efficacy and minimal side effects have made them widely preferred in treatment regimens. Their contribution to multi-drug therapy approaches for H. pylori eradication further cements their dominant market position. High healing success rates have been consistently reported in clinical settings, particularly when PPIs are administered over a treatment window of four to eight weeks.

The duodenal ulcers segment held a 50.8% share in 2024 and is set to experience significant growth throughout the forecast period. These ulcers typically form in the upper part of the small intestine and are primarily triggered by bacterial infection and long-term use of NSAIDs. They are prevalent across a broad population and frequently present with distinct symptoms that allow for quicker diagnosis and more immediate intervention, supporting higher treatment rates.

North America Peptic Ulcers Treatment Market generated USD 2.1 billion in 2024 and is expected to reach USD 3.6 billion by 2034, growing at a CAGR of 5.5%. This regional dominance can be attributed to the high burden of NSAID-related complications and H. pylori cases. A well-established healthcare framework, better access to advanced medications, and increasing awareness regarding gastrointestinal care and preventive health all contribute to the region's strong market position. Additionally, the active presence of leading pharmaceutical companies continues to support growth in this region.

Major players in the Global Peptic Ulcers Treatment Industry include Takeda, GlaxoSmithKline, Cadila Healthcare, Aurobindo Pharma, Ranbaxy Laboratories, Pfizer, Dr. Reddy's Laboratories, Strides Pharma, Phathom Pharmaceuticals, Granules India, AstraZeneca, Sun Pharma, Eisai, and Azurity Pharmaceuticals. To solidify their market positions, key players in the peptic ulcer treatment space are focusing on diverse strategic initiatives. Many are investing heavily in R&D to develop new therapies with higher efficacy and lower side effects. Formulation improvements, especially around combination drug regimens, are aimed at increasing treatment adherence and minimizing recurrence.

Companies are also expanding their manufacturing capabilities and strengthening their global supply chains to ensure wider access to treatment. Additionally, firms are entering strategic partnerships and engaging in mergers and acquisitions to broaden their portfolios and geographical presence. Targeted awareness campaigns and physician education programs further enhance product visibility and brand credibility, especially in emerging healthcare markets where diagnostic and treatment rates are steadily climbing.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Drug type

- 2.2.3 Ulcer type

- 2.2.4 Medication type

- 2.2.5 Route of administration

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of Helicobacter pylori Infections

- 3.2.1.2 Growing geriatric population

- 3.2.1.3 Expanding R&D fundings and activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects of long-term PPI use

- 3.2.3 Market opportunities

- 3.2.3.1 Novel therapies & drug delivery innovations

- 3.2.3.2 Expansion of online pharmacies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pipeline analysis

- 3.5 Regulatory landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Proton pump inhibitors (PPIs)

- 5.3 H2-receptor antagonists

- 5.4 Antacids

- 5.5 Antibiotics

- 5.6 Cytoprotective agents

- 5.7 Other drug types

Chapter 6 Market Estimates and Forecast, By Ulcer Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Gastric ulcers

- 6.3 Duodenal ulcers

- 6.4 Esophageal ulcers

Chapter 7 Market Estimates and Forecast, By Medication Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Branded

- 7.3 Generics

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Oral Parenteral

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacies

- 9.3 Retail pharmacies

- 9.4 Online pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AstraZeneca

- 11.2 Aurobindo Pharma

- 11.3 Azurity Pharmaceuticals

- 11.4 Cadila Healthcare

- 11.5 Dr. Reddy’s Laboratories

- 11.6 Eisai

- 11.7 GlaxoSmithKline

- 11.8 Granules India

- 11.9 Pfizer

- 11.10 Phathom Pharmaceuticals

- 11.11 Ranbaxy Laboratories

- 11.12 Strides Pharma

- 11.13 Sun Pharma

- 11.14 Takeda

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日