|

市場調査レポート

商品コード

1782122

人工知能生成コンテンツ(AIGC)の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Artificial Intelligence Generated Content (AIGC) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 人工知能生成コンテンツ(AIGC)の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年07月15日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

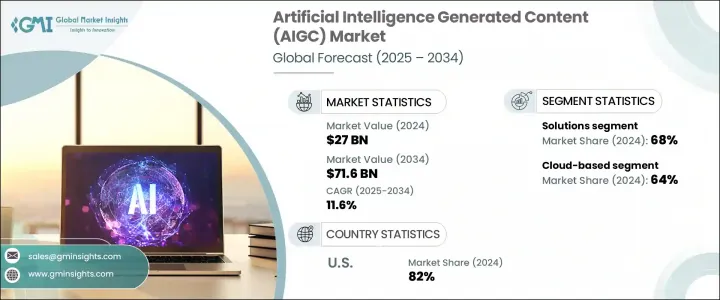

世界の人工知能生成コンテンツ(AIGC)市場は、2024年に270億米ドルと評価され、CAGR 11.6%で成長し、2034年には716億米ドルに達すると推定されています。

かつては労働集約的な作業であった従来のコンテンツ作成は、現在では高度なAI技術を活用した合理的で自動化されたプロセスへと変化しつつあります。AIモデルがより洗練されるにつれ、コンテンツ制作はもはやニッチなクリエイティブチームに限定されるものではなく、企業の中核機能となりつつあります。あらゆる分野の企業が、プロンプトエンジニアリング、倫理的なコンテンツ利用、ワークフローの最適化を効果的に行えるAIリテラシーの高いチームの開発を優先しています。この動向は、AIGCのスキルアップをデジタルトランスフォーメーション戦略の重要な要素に変えつつあります。

市場開発は、公的機関と民間のイノベーターが連携してスキル開発に力を入れるようになったことで、さらに加速しています。様々な機関が協力し、AIを活用したコンテンツ制作の需要に対応できるよう、構造化された学習フレームワークや資格認定システムを構築しています。同時に、AIGCのソリューション・プロバイダーは、トレーニング・モジュールを自社のプラットフォームに統合し、クリエイターから企業のプロフェッショナルまで、ユーザーが拡張可能な教育リソースにアクセスできるようにしています。こうした取り組みにより、マーケティングやエンターテインメントから教育、eコマースまで、さまざまな業界で導入が加速しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 270億米ドル |

| 予測金額 | 716億米ドル |

| CAGR | 11.6% |

市場はコンポーネント別にソリューションとサービスに区分されます。2024年には、ソリューションが最大のシェアを占め、総売上の約68%を占める。このセグメントは、2025年から2034年にかけてCAGR 12%超の成長が見込まれています。AIGCソリューションには、テキスト、画像、動画、音声、さらにはコードを生成するAIベースのプラットフォームが含まれ、企業に動的コンテンツ開発のためのツールを提供します。これらのテクノロジーは、自動化、リアルタイムのパーソナライゼーション、クリエイティブな俊敏性をサポートし、頻繁なコンテンツ更新とブランドエンゲージメントに依存する業界では極めて重要です。マーケティングキャンペーンの合理化、顧客とのコミュニケーションの強化、没入感のあるデジタル体験の構築など、企業はますますこうしたプラットフォームへの依存度を高めています。

AIGC市場は、導入形態別にクラウドベースとオンプレミスに分類されます。クラウドベースのソリューションは2024年に64%のシェアを獲得して市場をリードし、予測期間を通じて13%以上のCAGRを記録すると予測されています。クラウドベースのツールが好まれる背景には、その拡張性、統合の容易さ、リアルタイムのアクセシビリティがあります。クラウドインフラストラクチャにより、ユーザーはAPIやSaaS(Software-as-a-Service)モデルを介してコンテンツを生成することができ、より迅速なイテレーションと継続的なワークフローの改善が促進されます。これらのツールはインフラストラクチャーの制約をなくし、複数のプラットフォームでクリエイティブなアウトプットを展開できるため、デジタルマーケティング、教育、eコマースなどのダイナミックな分野で特に人気があります。

テクノロジー別に見ると、市場は自然言語処理(NLP)、生成的敵対ネットワーク(GAN)、トランスフォーマーモデル、テキストから画像へのモデル、テキストからビデオ/3Dへのモデル、音声からテキストまたはテキストから音声へのシステムなど、いくつかの主要イノベーションに区分されます。このうち、トランスフォーマ・モデルが2024年には支配的な地位を占めています。大規模処理能力で知られるこれらのモデルは、多くの主要なAIGCアプリケーションの基盤となっています。文脈を理解し、人間のような反応を生成し、形式を超えた情報を合成する能力を持つため、マルチモーダルAIプラットフォームの動力源として不可欠です。トランスフォーマーアーキテクチャが進歩し続けるにつれて、ニュアンスがますます豊かになり、適応性の高いコンテンツ作成システムが可能になりつつあります。

地域別では、米国が北米の主要市場として台頭し、地域シェアの約82%を占め、2024年には約76億米ドルの収益を生み出します。同国の優位性は、強力なイノベーションエコシステム、AI研究への旺盛な投資、AI技術の早期企業導入による。デジタル経済が確立され、AIテクノロジープロバイダーが密集していることが、引き続き成長を後押ししています。企業のソフトウェア・スタックへのAIGCツールの統合は、メディア、教育、広告、ビジネスサービスなどのセクターで高い採用を促進しています。

AIGCの状況は競合環境によって形成されており、主要な企業がスケーラブルなコンテンツ生成をサポートするツールを開発しています。これらの企業は、拡大する市場需要に対応するため、プラットフォームの性能向上、ユーザー体験の強化、エンタープライズグレードのアプリケーションのサポートに注力しています。この技術が成熟するにつれて、AIGCは世界なデジタル経済の基盤となる要素になると予想され、コンテンツがどのように想像され、作成され、消費されるかに影響を与えます。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- デジタルコンテンツ需要の爆発的な増加

- AIGCをビジネスアプリに統合

- ファンデーションモデルの進歩

- ローカリゼーションとパーソナライゼーションの必要性

- クリエイター経済の台頭

- クラウドベースの配信モデル

- 業界の潜在的リスク&課題

- 知的財産および著作権リスク

- 非技術系専門家の間での認知度が低い

- 高いコンピューティングリソース要件

- コンテンツの真正性検出の欠如

- 市場機会

- 業界固有のAIGCツール

- 合成データ生成

- 多言語対応・低リソースモデル開発

- AIと人間の協働ワークフロー

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- コスト内訳分析

- ソフトウェア開発およびライセンシング費用

- 導入と統合のコスト

- 保守・サポート費用

- サイバーセキュリティとコンプライアンスのコスト

- トレーニングと変更管理コスト

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

- ユースケース

- 最良のシナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソリューション

- テキスト生成ツール

- 画像生成プラットフォーム

- ビデオおよびアニメーションジェネレーター

- オーディオおよび音声合成ツール

- コード生成プラットフォーム

- サービス

- コンサルティングと戦略

- 統合と展開

- サポートとメンテナンス

- カスタムコンテンツ開発サービス

第6章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- オンプレミス

- クラウドベース

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 自然言語処理(NLP)

- 生成的敵対ネットワーク(GAN)

- トランスフォーマーモデル

- テキストから画像へのモデル

- テキストからビデオ/3D

- テキスト読み上げ(TTS)

- 音声テキスト変換(STT)

第8章 市場推計・予測:コンテンツ別、2021年~2034年

- 主要動向

- テキストコンテンツ

- ブログと記事

- マーケティングコピー(広告、メール)

- 脚本とセリフ

- 製品の説明

- 画像コンテンツ

- デジタルアートとイラスト

- 製品のビジュアル

- マーケティングとソーシャルメディアのグラフィック

- ビデオコンテンツ

- 概要ビデオ

- バーチャルプレゼンター

- 合成俳優/アバター

- オーディオコンテンツ

- ナレーション

- ポッドキャスト

- オーディオブック

- コードの内容

- Web開発スクリプト

- ゲーム開発コード

- 自動化スクリプト

第9章 市場推計・予測:企業規模別、2021年~2034年

- 主要動向

- 中小企業

- 中規模企業

- 大企業

第10章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- マーケティングと広告

- メディア&エンターテイメント

- eコマースと小売

- 教育とトレーニング

- カスタマーサービスとバーチャルアシスタンス

- ソフトウェアとゲーム開発

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- インドネシア

- フィリピン

- シンガポール

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- コロンビア

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- Adobe

- Alibaba Cloud

- Amazon Web Services(AWS)

- Anthropic

- Baidu

- Canva

- Copy.ai

- Descript

- Google DeepMind

- IBM

- Jasper AI

- Meta(Facebook AI)

- Microsoft

- NVIDIA

- OpenAI

- Pika Labs

- Rephrase.ai

- Runway

- Stability AI

- Synthesia

The Global Artificial Intelligence Generated Content Market was valued at USD 27 billion in 2024 and is estimated to grow at a CAGR of 11.6% to reach USD 71.6 billion by 2034. Traditional content creation, once a labor-intensive task, is now transforming into a streamlined, automated process powered by advanced AI technologies. As AI models become more sophisticated, content production is no longer confined to niche creative teams-it is becoming a core enterprise function. Organizations across sectors are prioritizing the development of AI-literate teams that can effectively navigate prompt engineering, ethical content use, and workflow optimization. This trend is turning AIGC upskilling into a critical element of digital transformation strategies.

Market expansion is being further fueled by a growing focus on skill development through collaborations between public agencies and private sector innovators. Various institutions are working together to create structured learning frameworks and credentialing systems to prepare the workforce for the demands of AI-driven content creation. Simultaneously, AIGC solution providers are integrating training modules into their platforms, ensuring users-from creatives to enterprise professionals-have access to scalable education resources. These efforts are accelerating adoption across industries ranging from marketing and entertainment to education and e-commerce.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27 Billion |

| Forecast Value | $71.6 Billion |

| CAGR | 11.6% |

The market is segmented by components into solutions and services. In 2024, solutions represented the largest share, accounting for nearly 68% of total revenue. This segment is expected to grow at a CAGR of over 12% between 2025 and 2034. AIGC solutions include AI-based platforms that generate text, images, videos, audio, and even code, providing businesses with tools for dynamic content development. These technologies support automation, real-time personalization, and creative agility, which are crucial in industries that rely on frequent content updates and brand engagement. Businesses are increasingly relying on these platforms to streamline marketing campaigns, enhance customer communication, and build immersive digital experiences.

By deployment, the AIGC market is categorized into cloud-based and on-premises models. Cloud-based solutions led the market with a 64% share in 2024 and are anticipated to register a CAGR of more than 13% through the forecast period. The preference for cloud-based tools is driven by their scalability, ease of integration, and real-time accessibility. Cloud infrastructure allows users to generate content via APIs and software-as-a-service (SaaS) models, promoting faster iterations and continuous workflow improvements. These tools eliminate infrastructure constraints and allow businesses to expand creative output across multiple platforms, making them especially popular in dynamic sectors like digital marketing, education, and e-commerce.

Based on technology, the market is segmented into several key innovations, including natural language processing (NLP), generative adversarial networks (GANs), transformer models, text-to-image models, text-to-video/3D, and speech-to-text or text-to-speech systems. Among these, transformer models held the dominant position in 2024. These models, known for their large-scale processing capabilities, are the foundation of many leading AIGC applications. Their ability to understand context, generate human-like responses, and synthesize information across formats makes them essential to powering multi-modal AI platforms. As transformer architectures continue to advance, they are enabling increasingly nuanced and adaptable content creation systems.

Regionally, the United States emerged as the leading market within North America, commanding around 82% of the regional share and generating approximately USD 7.6 billion in revenue in 2024. The country's dominance is driven by its strong innovation ecosystem, robust investment in AI research, and early enterprise adoption of AI technologies. A well-established digital economy and a dense concentration of AI technology providers continue to propel growth. The integration of AIGC tools into enterprise software stacks is driving high adoption across sectors such as media, education, advertising, and business services.

The AIGC landscape is shaped by a competitive environment, with key companies developing tools that support scalable content generation. These companies are focused on improving platform performance, enhancing user experiences, and supporting enterprise-grade applications to meet growing market demand. As the technology matures, AIGC is expected to become a foundational element of the global digital economy, influencing how content is imagined, created, and consumed.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment Mode

- 2.2.4 Technology

- 2.2.5 Content

- 2.2.6 Enterprise Size

- 2.2.7 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Explosive growth in digital content demand

- 3.2.1.2 Integration of AIGC into business apps

- 3.2.1.3 Advancements in foundation models

- 3.2.1.4 Need for localization & personalization

- 3.2.1.5 Rise of the creator economy

- 3.2.1.6 Cloud-based delivery models

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Intellectual property & copyright risks

- 3.2.2.2 Limited awareness among non-tech professionals

- 3.2.2.3 High computing resource requirements

- 3.2.2.4 Lack of content authenticity detection

- 3.2.3 Market opportunities

- 3.2.3.1 Industry-specific AIGC tools

- 3.2.3.2 Synthetic data generation

- 3.2.3.3 Multilingual and low-resource model development

- 3.2.3.4 Collaborative AI-human workflows

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Software development & licensing cost

- 3.8.2 Deployment & integration cost

- 3.8.3 Maintenance & support cost

- 3.8.4 Cybersecurity & compliance cost

- 3.8.5 Training & change management cost

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Best-case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solutions

- 5.2.1 Text generation tools

- 5.2.2 Image generation platforms

- 5.2.3 Video and animation generators

- 5.2.4 Audio and speech synthesis tools

- 5.2.5 Code generation platforms

- 5.3 Services

- 5.3.1 Consulting & strategy

- 5.3.2 Integration & deployment

- 5.3.3 Support & maintenance

- 5.3.4 Custom content development services

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud-based

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Natural Language Processing (NLP)

- 7.3 Generative Adversarial Networks (GAN)

- 7.4 Transformer models

- 7.5 Text-to-image models

- 7.6 Text-to-video/3D

- 7.7 Text-to-Speech (TTS)

- 7.8 Speech-to-Text (STT)

Chapter 8 Market Estimates & Forecast, By Content, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Text content

- 8.2.1 Blogs and articles

- 8.2.2 Marketing copy (ads, emails)

- 8.2.3 Scripts and dialogues

- 8.2.4 Product descriptions

- 8.3 Image Content

- 8.3.1 Digital art & illustrations

- 8.3.2 Product visuals

- 8.3.3 Marketing & social media graphics

- 8.4 Video Content

- 8.4.1 Explainer videos

- 8.4.2 Virtual presenters

- 8.4.3 Synthetic actors/avatars

- 8.5 Audio Content

- 8.5.1 Voiceovers

- 8.5.2 Podcasts

- 8.5.3 Audiobooks

- 8.6 Code Content

- 8.6.1 Web development scripts

- 8.6.2 Game development code

- 8.6.3 Automation scripts

Chapter 9 Market Estimates & Forecast, By Enterprise Size, 2021- 2034 ($Bn)

- 9.1 Key trends

- 9.2 Small enterprises

- 9.3 Medium enterprises

- 9.4 Large enterprises

Chapter 10 Market Estimates & Forecast, By Application, 2021- 2034 ($Bn)

- 10.1 Key trends

- 10.2 Marketing & advertising

- 10.3 Media & entertainment

- 10.4 E-commerce & retail

- 10.5 Education & training

- 10.6 Customer service & virtual assistance

- 10.7 Software & game development

- 10.8 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Nordics

- 11.3.7 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Indonesia

- 11.4.7 Philippines

- 11.4.8 Singapore

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Adobe

- 12.2 Alibaba Cloud

- 12.3 Amazon Web Services (AWS)

- 12.4 Anthropic

- 12.5 Baidu

- 12.6 Canva

- 12.7 Copy.ai

- 12.8 Descript

- 12.9 Google DeepMind

- 12.10 IBM

- 12.11 Jasper AI

- 12.12 Meta (Facebook AI)

- 12.13 Microsoft

- 12.14 NVIDIA

- 12.15 OpenAI

- 12.16 Pika Labs

- 12.17 Rephrase.ai

- 12.18 Runway

- 12.19 Stability AI

- 12.20 Synthesia