尿管鏡の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Ureteroscope Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1782109

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

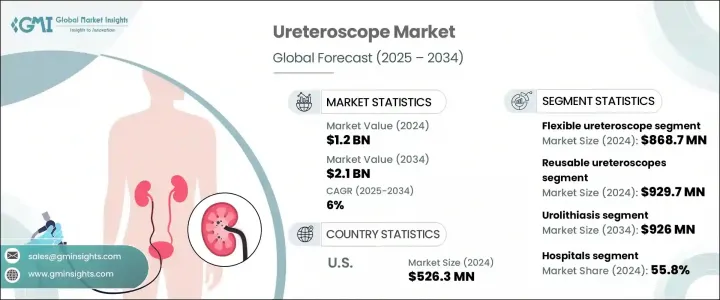

尿管鏡の世界市場は、2024年には12億米ドルと評価され、CAGR 6%で成長し、2034年には21億米ドルに達すると推定されています。

この成長軌道は、主に腎臓結石やその他の尿路関連疾患の世界の発生率の上昇によって牽引されています。これと並行して、より良い臨床結果、術後合併症の減少、入院期間の短縮に後押しされ、低侵襲技術の採用というヘルスケア全体の動向も引き続き加速しています。このような利点により、ヘルスケアプロバイダーも患者も、従来の手術よりも内視鏡的介入を好むようになってきています。尿管内視鏡は、尿管や腎臓の状態を診断・治療するための機器であるが、その設計が進化して柔軟性が向上し、高度な画像診断が可能になったことで、ますます重要性を増しています。これらの技術革新により、患者の快適性と安全性を向上させながら、より精密な治療が可能になり、世界中のヘルスケアシステムで採用が拡大しています。

尿路感染症や腎結石の増加は、現代の生活習慣、肥満率の上昇、遺伝的影響、特定の集団における水分補給不足などが複合的に絡み合っているためと考えられます。これらの健康問題が一般的になるにつれ、医療界は効果的で侵襲性の低い解決策として尿管鏡検査に注目しています。これらのスコープは、狭窄、腫瘍、結石などの幅広い泌尿器科的問題に対処できるように設計されています。最先端の可視化と操作性を備え、尿路全域の徹底的な診断と低侵襲治療を可能にします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 12億米ドル |

| 予測金額 | 21億米ドル |

| CAGR | 6% |

軟性尿管鏡の2024年の市場規模は8億6,870万米ドルでした。適応性が高く、複雑な尿路を容易に通過できるため、複雑な泌尿器科症例の診断や管理に最適です。材料と視覚化における技術的進歩は、これらのデバイスの性能をさらに高め、広く臨床に受け入れられることにつながっています。泌尿器科医がより安全で効率的な手技を可能にする精密機器を求めるようになり、軟性尿管鏡の需要は増加しています。

臨床用途では、尿路結石症分野が2024年に最も高い市場シェアを占め、2034年には9億2,600万米ドルに達すると予測されています。尿路結石症は幅広い層が罹患しており、治療しなければ深刻な合併症を引き起こす可能性があります。尿管鏡の精度と効率は、特に侵襲性の低い外科的手段で結石の除去や破砕が必要な場合に、この疾患の治療に不可欠なツールとなっています。

米国尿管鏡強固なヘルスケアインフラと泌尿器疾患に対する高い認識により、2024年の市場規模は5億2,630万米ドルとなりました。高度な医療技術と腎結石や尿路の問題を抱える患者数の多さが相まって、一貫した需要を牽引しています。さらに、トップクラスの医療機器メーカーが存在し、新しいイメージングツールの導入が急速に進んでいることも、この分野における同国のリーダーシップを確固たるものにしています。

尿管鏡市場の競合情勢に貢献している主要企業は、Boston Scientific、STORZ、Ambu、PUSEN、Coloplast、BD、Stryker、Dornier MedTech、Neoscope、OLYMPUS、OPCOM Medical、RICHARD WOLFなどです。市場ポジションを強化するため、尿管鏡業界の各社は、機器の柔軟性、小型化、光学的透明性の向上に重点を置き、技術革新に多額の投資を行っています。先進国市場と新興国市場の両方の需要に対応するため、戦略的パートナーシップや製品の発売を通じて、製品ポートフォリオを積極的に拡大しています。使い捨てやデジタル尿管鏡技術の継続的な改善もまた、重要な重点分野です。さらに、各社は世界な流通網を強化し、臨床導入を支援するためのトレーニングプログラムに取り組んでおり、これによって長期的な競争力と持続的な市場成長を確保しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 腎臓結石および尿路疾患の罹患率の増加

- 尿管鏡検査における技術的進歩

- 低侵襲デバイスの採用拡大

- 業界の潜在的リスク&課題

- 高度なデジタル尿管鏡の高コスト

- 機会

- 新興市場への進出

- 尿管鏡とロボット手術システムの統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 製品別の価格動向

- 将来の市場動向

- 償還シナリオ

- 消費者行動分析

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 柔軟な尿管鏡

- 堅固な尿管鏡

第6章 市場推計・予測:ユーザビリティ別、2021年~2034年

- 主要動向

- 再利用可能な尿管鏡

- 使い捨て尿管鏡

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 尿路結石症

- 尿道狭窄

- 尿路感染症

- その他の用途

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- その他の最終用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Ambu

- BD

- Boston Scientific

- Coloplast

- Dornier MedTech

- neoscope

- OLYMPUS

- OPCOM Medical

- PUSEN

- RICHARD WOLF

- STORZ

- Stryker

目次

The Global Ureteroscope Market was valued at USD 1.2 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 2.1 billion by 2034. This growth trajectory is primarily being driven by the rising global incidence of kidney stones and other urinary tract-related conditions. Alongside this, the broader healthcare trend of adopting minimally invasive technologies continues to gain pace, fueled by better clinical outcomes, reduced post-operative complications, and shorter hospital stays. These advantages are pushing both healthcare providers and patients to prefer endoscopic interventions over traditional surgery. Ureteroscopes-devices designed to diagnose and treat ureteral and renal conditions-have become increasingly important as their designs evolve to offer improved flexibility and advanced imaging. These innovations allow for more precise treatments with greater patient comfort and enhanced safety, supporting their growing adoption across healthcare systems worldwide.

The increase in urinary tract infections and renal calculi can be attributed to a mix of modern lifestyle habits, rising obesity rates, genetic influences, and poor hydration in certain populations. As these health issues become more common, the medical community is turning to ureteroscopy as an effective and less invasive solution. These scopes are engineered to address a wide range of urological concerns such as strictures, tumors, and calculi. Equipped with cutting-edge visualization and maneuverability, they enable thorough diagnosis and minimally invasive treatment across the urinary tract.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $2.1 Billion |

| CAGR | 6% |

The flexible ureteroscopes segment was valued at USD 868.7 million in 2024. Their adaptability and ease of navigation through the intricate urinary pathways make them ideal for diagnosing and managing complex urological cases. Technological advancements in materials and visualization further enhance the performance of these devices, leading to widespread clinical acceptance. The demand for flexible ureteroscopes is increasing as urologists seek precision instruments that allow for safer and more efficient procedures.

In terms of clinical application, the urolithiasis segment commanded the highest market share in 2024 and is expected to reach USD 926 million by 2034. Urolithiasis affects a broad demographic and can result in serious complications if untreated. The precision and efficiency of ureteroscopes make them essential tools in treating this condition, particularly when stone removal or fragmentation is required through less invasive surgical means.

U.S. Ureteroscope Market was valued at USD 526.3 million in 2024 due to its strong healthcare infrastructure and high awareness of urological disorders. Advanced medical technology, combined with a significant patient population dealing with kidney stones and urinary tract issues, drives consistent demand. Additionally, the presence of top-tier medical device manufacturers and the rapid adoption of newer imaging tools solidify the country's leadership in this space.

Key players contributing to the competitive landscape of the Ureteroscope Market include Boston Scientific, STORZ, Ambu, PUSEN, Coloplast, BD, Stryker, Dornier MedTech, Neoscope, OLYMPUS, OPCOM Medical, and RICHARD WOLF. To strengthen their market position, companies in the ureteroscope industry are investing heavily in innovation, focusing on enhancing device flexibility, miniaturization, and optical clarity. They are actively expanding their product portfolios through strategic partnerships and product launches tailored to meet the demands of both developed and emerging healthcare markets. Continuous improvement in disposable and digital ureteroscope technology is also a key focus area. Additionally, players are ramping up their global distribution networks and engaging in training programs to support clinical adoption, thereby ensuring long-term competitiveness and sustained market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Usability

- 2.2.4 Application

- 2.2.5 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of kidney stones and urinary tract diseases

- 3.2.1.2 Technological advancements in ureteroscopy

- 3.2.1.3 Growing adoption of minimally invasive devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced and digital ureteroscopes

- 3.2.3 Opportunities

- 3.2.3.1 Expansion into emerging markets

- 3.2.3.2 Integration of ureteroscopes with robotic surgical systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends, by product

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.9 Consumer behaviour analysis

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Flexible ureteroscope

- 5.3 Rigid ureteroscope

Chapter 6 Market Estimates and Forecast, By Usability, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Reusable ureteroscopes

- 6.3 Disposable ureteroscopes

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Urolithiasis

- 7.3 Urethral stricture

- 7.4 Urinary tract infections

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Ambu

- 10.2 BD

- 10.3 Boston Scientific

- 10.4 Coloplast

- 10.5 Dornier MedTech

- 10.6 neoscope

- 10.7 OLYMPUS

- 10.8 OPCOM Medical

- 10.9 PUSEN

- 10.10 RICHARD WOLF

- 10.11 STORZ

- 10.12 Stryker

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日