原発性免疫不全症の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Primary Immunodeficiency Disorders Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773467

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

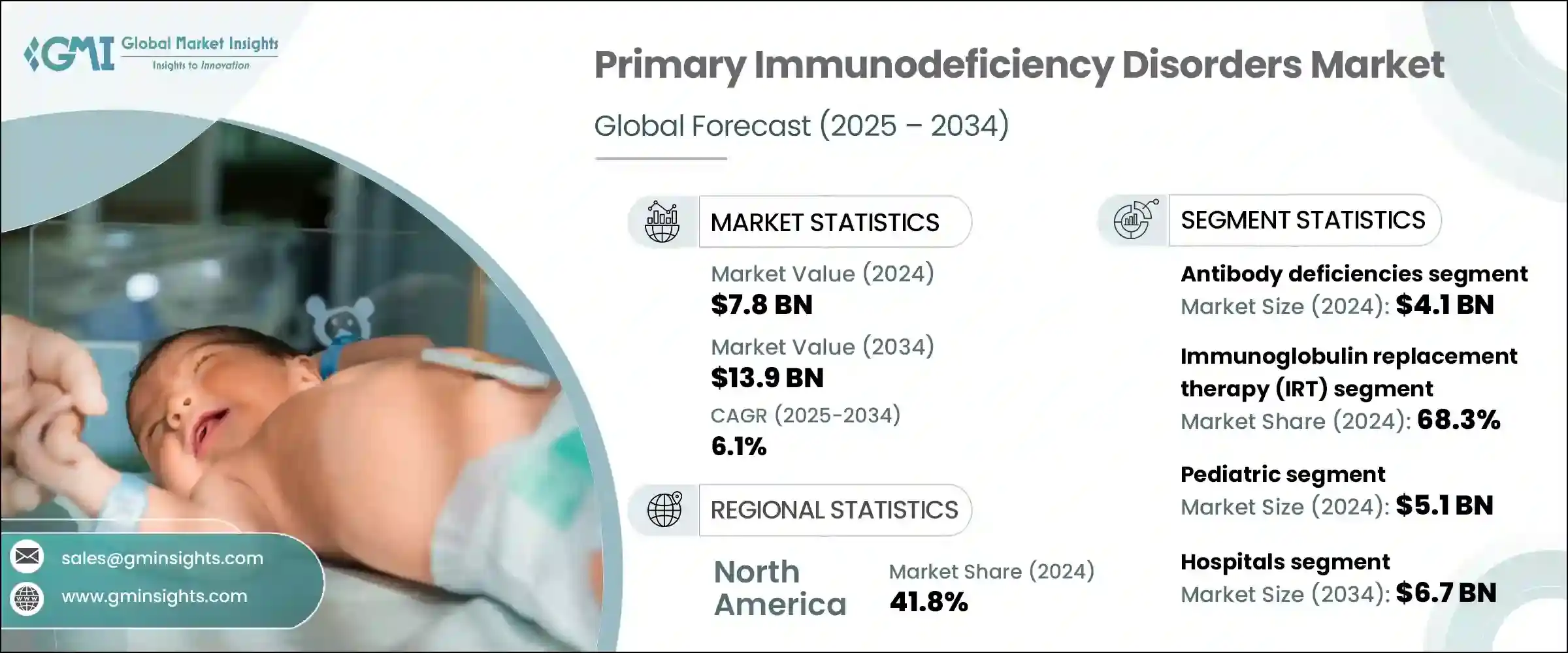

原発性免疫不全症の世界市場は、2024年には78億米ドルと評価され、CAGR 6.1%で成長し、2034年には139億米ドルに達すると予測されています。

この成長の主な要因は、原発性免疫不全症(PIDs)の発生率の上昇と、医療従事者や患者の間でこれらの疾患に対する認識が高まっていることです。診断アプローチと、遺伝子ベースの治療や生物製剤のような治療イノベーションの両方における進歩が、効果的な治療と管理の機会を拡大しています。研究開発への投資が強化され、これらの希少遺伝性疾患に対する認識が高まるにつれて、正確な診断とより的を絞った治療へのアクセスが向上しています。ヘルスケアシステムがより総合的に希少疾患に対応できるように進化するにつれ、早期介入、個別化治療、継続的モニタリングにより、患者はより良い転帰と生活の質の向上という恩恵を受けています。

ヘルスケア提供者の間では免疫学のトレーニングが向上し続けており、免疫不全症が疑われる患者の早期発見と介入が可能となっています。患者支援団体やコミュニティ支援グループは、患者をケアネットワークにつなぎ、ヘルスケア政策の体系的な変更を推進する上で重要な役割を果たしています。このような幅広い関与は、PIDの検出と分類を支援するために世界的に採用されつつある遺伝子配列決定やフローサイトメトリーなどの高度な診断ツールへのアクセスを向上させるのに役立っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 78億米ドル |

| 予測金額 | 139億米ドル |

| CAGR | 6.1% |

南アフリカ、ブラジル、インド、中国などの開発途上地域における可処分所得の増加とともに、都市化が進み、より良い医療サービスを受けられるようになったことで、人々は医療診断を受け、適切な治療を受けるようになっています。原発性免疫不全症は、感染症、慢性疾患、全体的な免疫機能低下に対する脆弱性をもたらす遺伝性免疫系疾患です。治療法の革新は、免疫力を向上させ、症状を緩和し、疾患の再発を最小限に抑えることに重点が置かれています。

2024年には、抗体欠乏症分野が41億米ドルの評価額で最大の市場セグメントを占めました。この優位性は、抗体産生障害に関連する免疫疾患の有病率の高さに起因しています。最も一般的なものは、生涯にわたる治療を必要とする重症感染症を頻繁に引き起こす免疫不全症です。このような患者は通常、静脈内または皮下注射による定期的な免疫グロブリン療法が必要であり、これが製品需要の持続に寄与しています。現在進行中の医療の進歩により、より効率的で患者に優しい投与システムが確保されつつあり、このセグメントの成長可能性が拡大しています。

治療に関しては、免疫グロブリン補充療法(IRT)分野が2024年に68.3%のシェアを占めています。ほとんどの抗体関連免疫不全症に対する標準治療プロトコルとしてIRTへの依存が続いていることが、この分野の市場での存在感を高めています。これらの治療法は、感染症から長期的に保護するものであり、こうした生涯にわたる疾患の管理に不可欠です。半減期の延長やリコンビナント技術など、最近の治療製剤の改良により、治療効果と患者の快適性がさらに向上しています。さらに、認知度と支持の高まりが早期治療開始とアドヒアランスの向上を支えており、これがこの市場の拡大を直接支えています。ヘルスケアプロバイダーは現在、IRTをPID治療の基礎となる治療法として認識しており、IRTがより広く受け入れられ、使用されるようになっています。

米国原発性免疫不全症2024年の市場規模は29億米ドル。同国は、強固なヘルスケアインフラ、先進的診断法の普及、免疫不全症に対する国民的・臨床的意識の高さで世界市場をリードしています。免疫プロファイリング、フローサイトメトリー、高度遺伝子検査などの診断ツールは、特に小児のPID症例の確認と分類に広く使用されています。遺伝子編集技術や幹細胞を用いた治療法といった最先端の治療法が利用できるようになったことで、米国の患者は世界的に最も革新的な治療法のいくつかにアクセスできるようになっています。専門クリニック、免疫学に特化した病院、在宅医療提供モデルなどが市場の成熟に貢献しています。標的生物製剤、次世代免疫グロブリン、希少疾患の新規治療に対する強力な研究投資が、市場の進化を形成し続けています。

原発性免疫不全症市場の主要企業には、Orchard Therapeutics、Miltenyi Biotec、CSL Behring、Baxter International、Medac、Octapharma、ADMA Biologics、武田薬品工業、F. Hoffmann La Roche、Bluebird Bio、Biotest(Grifol Group)、Avanos、Leadiant Biosciencesなどがあります。原発性免疫不全症市場で事業を展開する企業は、市場での存在感を高めるためにいくつかの戦略を追求しています。

その一つが、標的生物製剤、遺伝子治療薬、バイオアベイラビリティを高め投与回数を減らす次世代免疫グロブリン治療薬のための先進的研究開発パイプラインへの投資です。各社はまた、生涯にわたる免疫グロブリン補充療法の需要の高まりに対応するため、製造能力の拡大も進めています。学術機関や研究センターとの戦略的提携により、新たな技術や新たな適応症へのアクセスが可能となっています。各社は、特に診断に対する意識が高まっている新興国地域での地理的拡大を通じて、市場への浸透を図っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 原発性免疫不全症の普及率が高め

- 小児人口の増加

- 診断と治療における技術の進歩

- 免疫グロブリン補充療法(IRT)の需要増加

- 業界の潜在的リスク&課題

- 治療費が高め

- 血漿由来製品の不足

- 市場機会

- 免疫グロブリン療法の適応拡大

- 遺伝子治療および生物製剤のパイプライン拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- テクノロジーの情勢

- 将来の市場動向

- パイプライン分析

- 消費者行動分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

第5章 市場推計・予測:病気の種類別、2021 –2034

- 主要動向

- 抗体欠損

- 複合免疫不全症

- 補体欠損症

- 貪食障害

- その他の病気の種類

第6章 市場推計・予測:治療の種類別、2021 –2034

- 主要動向

- 免疫グロブリン補充療法(IRT)

- 造血幹細胞移植(HSCT)

- 遺伝子治療

- その他の治療の種類

第7章 市場推計・予測:年齢別、2021 –2034

- 主要動向

- 小児科

- 成人用

第8章 市場推計・予測:最終用途別、2021 –2034

- 主要動向

- 病院

- 専門クリニック

- 在宅ケア設定

- その他の用途

第9章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- ADMA Biologics

- Baxter International

- Biotest(Grifol Group)

- Bluebird Bio

- CSL Behring

- F. Hoffmann La Roche

- Leadiant Biosciences

- Medac

- Miltenyi Biotec

- Takeda Pharmaceutical

- Octapharma

- Orchard Therapeutics

目次

The Global Primary Immunodeficiency Disorders Market was valued at USD 7.8 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 13.9 billion by 2034. This growth is primarily driven by the rising incidence of primary immunodeficiency disorders (PIDs) and the increasing recognition of these conditions among medical professionals and patients. Advancements in both diagnostic approaches and therapeutic innovations, such as gene-based therapies and biologics, are creating expanded opportunities for effective treatment and management. Enhanced investment in research and development, coupled with growing awareness of these rare genetic disorders, is improving access to accurate diagnoses and more targeted care. As healthcare systems evolve to address rare conditions more holistically, patients are benefiting from better outcomes and improved quality of life through early intervention, personalized therapies, and continuous monitoring.

Training in immunology continues to improve among healthcare providers, allowing earlier identification and intervention for patients with suspected immunodeficiency disorders. Patient advocacy organizations and community support groups are playing a crucial role in connecting individuals to care networks and pushing for systemic changes in healthcare policy. This broader engagement is helping increase access to advanced diagnostic tools, such as genetic sequencing and flow cytometry, which are being adopted globally to aid in detecting and classifying PIDs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.8 Billion |

| Forecast Value | $13.9 Billion |

| CAGR | 6.1% |

The rise of urbanization and access to better healthcare services, along with increasing disposable incomes in developing regions such as South Africa, Brazil, India, and China, is encouraging people to seek medical evaluations and pursue proper treatment. Primary immunodeficiency disorders are inherited immune system conditions that lead to higher vulnerability to infections, chronic illnesses, and overall weakened immune function. Treatment innovations are focused on improving immunity, alleviating symptoms, and minimizing disease recurrence.

The antibody deficiencies segment represented the largest market segment in 2024, with a valuation of USD 4.1 billion. This dominance stems from the high prevalence of immune disorders linked to impaired antibody production. Among the most common are immunodeficiencies that result in frequent, severe infections requiring lifelong therapy. Patients with these conditions typically need regular immunoglobulin therapy administered through intravenous or subcutaneous methods, which contributes to sustained product demand. Ongoing medical advancements are ensuring more efficient and patient-friendly delivery systems, expanding this segment's growth potential.

In terms of treatment, the immunoglobulin replacement therapy (IRT) segment held a 68.3% share in 2024. The continued reliance on IRT as a standard care protocol for most antibody-related immunodeficiencies reinforces its strong market presence. These therapies offer long-term protection from infections, which is essential in managing these lifelong conditions. Recent improvements in treatment formulations, including options with extended half-lives and recombinant technology, are further increasing therapy effectiveness and patient comfort. Additionally, greater awareness and advocacy support early treatment initiation and improved adherence, which directly supports this market's expansion. Healthcare providers now recognize IRT as a cornerstone therapy in PID treatment, prompting its broader acceptance and usage.

U.S. Primary Immunodeficiency Disorders Market was valued at USD 2.9 billion in 2024. The country leads the global market with a robust healthcare infrastructure, widespread adoption of advanced diagnostics, and strong public and clinical awareness of immunodeficiency disorders. Diagnostic tools, including immune profiling, flow cytometry, and advanced genetic testing, are widely used to confirm and classify PID cases, especially among children. The availability of cutting-edge therapies such as gene editing technologies and stem cell-based interventions is giving U.S. patients access to some of the most innovative treatments globally. Specialized clinics, immunology-focused hospitals, and home-based care delivery models have all contributed to market maturity. Strong research investments in targeted biologics, next-generation immunoglobulins, and novel therapies for rare diseases continue to shape the market's evolution.

Leading companies in the Primary Immunodeficiency Disorders Market include Orchard Therapeutics, Miltenyi Biotec, CSL Behring, Baxter International, Medac, Octapharma, ADMA Biologics, Takeda Pharmaceutical, F. Hoffmann La Roche, Bluebird Bio, Biotest (Grifol Group), Avanos, and Leadiant Biosciences. Companies operating in the primary immunodeficiency disorders market are pursuing several strategies to enhance their market presence.

One major focus is investing in advanced R&D pipelines for targeted biologics, gene therapies, and next-gen immunoglobulin therapies with enhanced bioavailability and reduced administration frequency. Firms are also expanding manufacturing capabilities to meet the growing demand for lifelong immunoglobulin replacement therapies. Strategic collaborations with academic institutions and research centers allow access to emerging technologies and new indications. Companies are increasing market penetration through geographic expansion, especially in developing regions with rising diagnostic awareness.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Disease type

- 2.2.3 Treatment type

- 2.2.4 Age group

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High prevalence of primary immunodeficiency disorders

- 3.2.1.2 Rising pediatric population

- 3.2.1.3 Technological advancement in diagnostics and treatment

- 3.2.1.4 Growing demand for immunoglobulin replacement therapy (IRT)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Shortage of plasma-derived products

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding indications for immunoglobulin therapy

- 3.2.3.2 Pipeline expansion in gene therapy and biologics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Pipeline analysis

- 3.8 Consumer behaviour analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Disease Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Antibody deficiencies

- 5.3 Combined immunodeficiencies

- 5.4 Complement deficiencies

- 5.5 Phagocytic disorders

- 5.6 Other disease types

Chapter 6 Market Estimates and Forecast, By Treatment Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Immunoglobulin replacement therapy (IRT)

- 6.3 Hematopoietic stem cell transplantation (HSCT)

- 6.4 Gene therapy

- 6.5 Other treatment types

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pediatric

- 7.3 Adult

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty Clinics

- 8.4 Homecare Settings

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ADMA Biologics

- 10.2 Baxter International

- 10.3 Biotest (Grifol Group)

- 10.4 Bluebird Bio

- 10.5 CSL Behring

- 10.6 F. Hoffmann La Roche

- 10.7 Leadiant Biosciences

- 10.8 Medac

- 10.9 Miltenyi Biotec

- 10.10 Takeda Pharmaceutical

- 10.11 Octapharma

- 10.12 Orchard Therapeutics

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日