RFテスト装置の市場機会、成長促進要因、産業動向分析、2025~2034年予測

RF Test Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773458

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

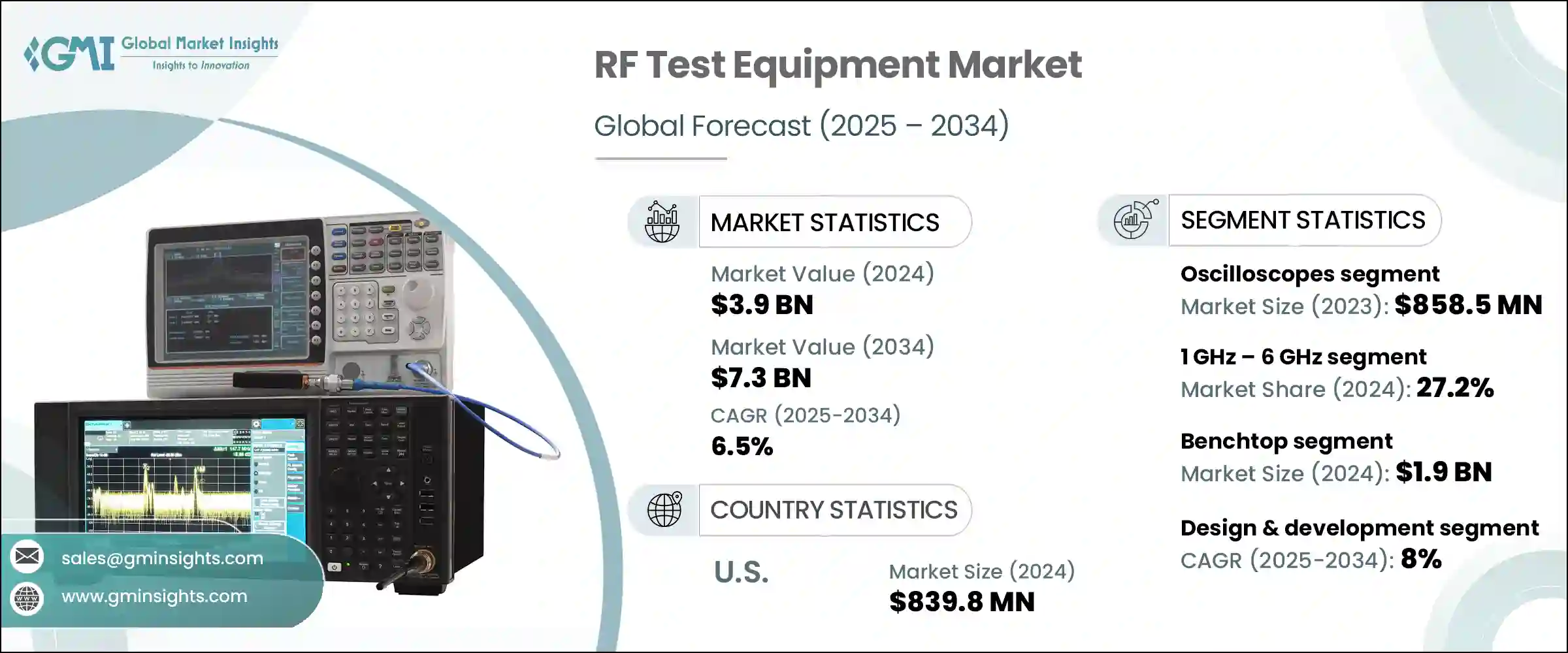

RFテスト装置の世界市場規模は、2024年に39億米ドルとなり、CAGR 6.5%で成長し、2034年には73億米ドルに達すると予測されています。

この分野の成長は、最新の無線通信技術の複雑性の高まりに大きく影響されています。産業界が5G、ミリ波アプリケーション、モノのインターネット(IoT)への移行を進める中、正確なマルチバンド・テスト・ソリューションの需要は急増し続けています。規制コンプライアンス、性能検証、相互運用性検証は、通信、防衛、自動車、産業オートメーションなどの分野で、今や譲れない要件と考えられています。

より多くのデバイスがワイヤレスで接続され、混雑したRF環境で動作するようになるにつれて、精密なテスト機器が品質保証、スペクトラム効率、安全性コンプライアンスに不可欠となっています。RFテストソリューションも超高周波テストに対応できるように進化しており、研究開発ラボやミッションクリティカルなエンジニアリング環境での需要を促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 39億米ドル |

| 予測金額 | 73億米ドル |

| CAGR | 6.5% |

地政学的な情勢は、世界のRFテスト装置を形成する上で重要な役割を果たしてきました。貿易政策と関税、特に最近の米国政権下で課された関税は、主要コンポーネントと機器の輸入コストを増加させることにより、生産コストと世界サプライチェーンに大きな影響を与えています。

5Gインフラの急速な進歩は、RFテスト装置の需要を最も強力に加速する要因の一つとなっています。これらの次世代通信システムは、ビームフォーミング、マッシブMIMO、mmWave伝送などの非常に複雑な技術を利用しており、そのすべてに緻密な検証が必要です。正確なRF試験は、性能指標の測定、標準準拠の検証、世界な帯域と機器サプライヤー間の互換性の保証に必要です。

さらに、5Gエコシステムがスマートシティ、自律型モビリティ、遠隔医療などの新たな領域に拡大する中、RFテスト装置は、ますます高密度化する無線環境での機能性を確保するための基盤であり続けます。ヘルスケア、製造、自動車、スマートホームにおけるIoTソリューションの普及は、RFテストに新たな複雑なレイヤーを追加しました。Wi-Fi、LoRa、Zigbee、Bluetoothで動作するデバイスは、プロトコルのコンプライアンスだけでなく、帯域幅が混雑する環境での共存や干渉への耐性についても検証する必要があります。

2023年、オシロスコープ分野の売上高は8億5,850万米ドルでした。オシロスコープは、電気信号をリアルタイムで可視化し、分析するために不可欠な機器です。デジタル回路、高周波システム、パワーエレクトロニクスの複雑化により、オシロスコープは微細な時間領域計測を必要とするアプリケーションに不可欠となっています。研究開発、自動車設計、無線通信などの業界では、電気的動作の診断、システムのトラブルシューティング、設計の完全性を高い精度で検証するために、これらのツールが頼りにされています。

40GHz以上の周波数向けに設計されたテスト機器は、2024年に24.8%のシェアを占めると予測されています。これらの超高周波ツールは、主に5G mmWaveネットワーク、先進レーダーシステム、宇宙探査、初期段階のテラヘルツ実験などの最先端領域で使用されます。重要度の高い研究開発環境のエンジニアは、次世代のコネクティビティやセンシング・アプリケーションをサポートできる低ノイズ、高解像度の計測器を求めています。まだ新しい分野ではあるが、このカテゴリーは、高周波技術の最前線を押し進める研究機関やイノベーション・ラボの強い牽引力となっています。

ドイツRFテスト装置市場は2034年までに3億5,290万米ドルに達すると予測されています。卓越したエンジニアリングと産業精度の高さで定評のあるドイツでは、先進的なテストツールの需要が高まっています。精密ロボットやスマート工場を含むインダストリー4.0の台頭により、シームレスな自動化のための信頼性の高いRFテストが必要とされています。ドイツの厳格な製造規制は、高効率エレクトロニクスへの注力と相まって、RF試験インフラへの継続的な投資にとって理想的な拠点となっています。強力な国内メーカーの存在と広範な研究開発事業が、世界の試験機器業界におけるドイツの重要性をさらに高めています。

RFテスト装置市場の主要企業には、B&K Precision Corporation、アンリツ株式会社、AR RF/Microwave Instrumentationなどがあり、いずれもRF検証技術の将来を積極的に形成しています。RFテスト装置市場の各社は、市場力を高め、進化する業界ニーズに適応するためにいくつかの戦略を採用しています。主要な焦点は、5G、衛星、IoTの進歩に対応するため、より高い周波数、より広い帯域幅、マルチプロトコル環境のサポートを統合して製品ポートフォリオを強化することです。

戦略的な研究開発投資により、AIを活用したテスト、自動化、クラウド統合のイノベーションが推進されています。開発企業はまた、通信・航空宇宙メーカーとのパートナーシップを強化し、新たなアプリケーションに合わせたソリューションを共同開発しています。高成長地域への地理的拡大と生産の現地化は、関税の影響とサプライチェーンのリスクを軽減するために進められています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 5Gネットワークの展開

- IoTデバイスの普及

- 自動車および航空宇宙技術の進歩

- AIと機械学習の統合

- ソフトウェア定義テスト機器の出現

- 業界の潜在的リスク&課題

- 高度なRFテスト装置の高コスト

- 複雑性と急速な技術変化

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- オシロスコープ

- 信号発生器

- スペクトラムアナライザー

- ネットワークアナライザー

- RFパワーメーター

- RFシンセサイザー

- その他

第6章 市場推計・予測:周波数範囲別、2021-2034

- 主要動向

- 1GHz未満

- 1GHz~6GHz

- 6GHz~18GHz

- 18GHz~40GHz

- 40GHz以上

第7章 市場推計・予測:フォームファクター別、2021-2034

- 主要動向

- ベンチトップ

- ポータブル/ハンドヘルド

- モジュラー

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- 設計・開発

- 製造業

- 設置とメンテナンス

- その他

第9章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 通信

- 家電

- 自動車・輸送

- 航空宇宙および防衛

- 産業

- 医学

- その他

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Anritsu Corporation

- AR RF/Microwave Instrumentation

- B&K Precision Corporation

- Berkeley Nucleonics Corporation

- Bird Technologies

- Copper Mountain Technologies

- Giga-tronics Incorporated

- Keysight Technologies

- National Instruments(NI)

- Qorvo

- Rigol Technologies

- Rohde &Schwarz

- Saelig Company, Inc.

- Signal Hound

- Teledyne LeCroy

- Teledyne Technologies Incorporated

- Thorlabs, Inc.

- Vaunix Technology Corporation

- Yokogawa Electric Corporation

目次

The Global RF Test Equipment Market was valued at USD 3.9 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 7.3 billion by 2034. Growth in this sector is being heavily influenced by the rising complexity of modern wireless communication technologies. As industries increasingly shift to 5G, mmWave applications, and the Internet of Things (IoT), the demand for accurate, multi-band testing solutions continues to surge. Regulatory compliance, performance validation, and interoperability verification are now considered non-negotiable requirements across telecommunications, defense, automotive, and industrial automation sectors.

As more devices become wirelessly connected and operate across crowded RF environments, the need for precise test equipment becomes essential for quality assurance, spectrum efficiency, and safety compliance. RF test solutions are also evolving to accommodate ultrahigh-frequency testing, driving demand across R&D labs and mission-critical engineering environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $7.3 Billion |

| CAGR | 6.5% |

Geopolitical developments have played a notable role in shaping the global RF test equipment landscape. Trade policies and tariffs, particularly those imposed during recent US administrations, have significantly impacted production costs and global supply chains by increasing import costs on key components and equipment.

The rapid advancement of 5G infrastructure has become one of the most powerful accelerators for RF test equipment demand. These next-generation communication systems utilize highly complex technologies like beamforming, massive MIMO, and mmWave transmissions, all of which require intricate validation. Precise RF testing is necessary to measure performance metrics, verify standard compliance, and guarantee compatibility across global bands and equipment suppliers.

Furthermore, as the 5G ecosystem expands into new domains like smart cities, autonomous mobility, and telemedicine, RF test equipment remains foundational to ensuring functionality across increasingly dense wireless environments. The proliferation of IoT solutions across healthcare, manufacturing, automotive, and smart homes has added another layer of complexity to RF testing. Devices operating on Wi-Fi, LoRa, Zigbee, and Bluetooth need to be validated not only for protocol compliance but also for coexistence and interference resilience in bandwidth-congested environments.

In 2023, the oscilloscope segment generated USD 858.5 million. These instruments are essential for visualizing and analyzing electrical signals in real-time. The rising intricacy of digital circuits, radio-frequency systems, and power electronics has made oscilloscopes indispensable in applications that require fine time-domain measurement. Industries such as R&D, automotive design, and wireless communication rely on these tools for diagnosing electrical behavior, troubleshooting systems, and validating design integrity with high levels of precision.

Test equipment designed for frequencies above the 40 GHz segment is anticipated to contribute a 24.8% share in 2024. These ultrahigh-frequency tools are primarily used in cutting-edge domains including 5G mmWave networks, advanced radar systems, space exploration, and early-stage terahertz experimentation. Engineers in high-stakes R&D environments demand low-noise, high-resolution instrumentation that can support next-generation connectivity and sensing applications. Though still an emerging segment, this category is gaining strong traction with research institutions and innovation labs pushing the frontiers of high-frequency technology.

Germany RF Test Equipment Market is forecasted to hit USD 352.9 million by 2034. The country's reputation for engineering excellence and industrial precision fuels the demand for advanced testing tools. The rise of Industry 4.0, including precision robotics and smart factories, requires reliable RF testing for seamless automation. Germany's rigorous manufacturing regulations, coupled with its focus on high-efficiency electronics, make it an ideal hub for continuous investment in RF testing infrastructure. The presence of strong domestic manufacturers and extensive R&D operations further reinforces Germany's importance in the global testing equipment landscape.

Key players in the RF Test Equipment Market include B&K Precision Corporation, Anritsu Corporation, and AR RF/Microwave Instrumentation, all of whom are actively shaping the future of RF validation technologies. Companies in the RF test equipment market are adopting several strategies to build market strength and adapt to evolving industry needs. A major focus has been on enhancing product portfolios by integrating support for higher frequencies, wider bandwidths, and multi-protocol environments to keep pace with 5G, satellite, and IoT advancements.

Strategic R&D investments are driving innovation in AI-enabled testing, automation, and cloud integration. Companies are also strengthening partnerships with telecom and aerospace manufacturers to co-develop solutions tailored to emerging applications. Geographic expansion into high-growth regions and localization of production are being pursued to reduce tariff impacts and supply chain risks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 5G network deployment

- 3.7.1.2 Proliferation of IoT devices

- 3.7.1.3 Advancements in automotive and aerospace technologies

- 3.7.1.4 Integration of AI and machine learning

- 3.7.1.5 Emergence of software-defined test equipment

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High cost of advanced RF test equipment

- 3.7.2.2 Complexity and rapid technological changes

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Oscilloscopes

- 5.3 Signal generators

- 5.4 Spectrum analyzers

- 5.5 Network analyzers

- 5.6 RF power meters

- 5.7 RF synthesizers

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Frequency Range, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Less than 1 GHz

- 6.3 1 GHz – 6 GHz

- 6.4 6 GHz – 18 GHz

- 6.5 18 GHz – 40 GHz

- 6.6 Above 40 GHz

Chapter 7 Market Estimates & Forecast, By Form Factor, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Benchtop

- 7.3 Portable/Handheld

- 7.4 Modular

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Design & development

- 8.3 Manufacturing

- 8.4 Installation & maintenance

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 Telecommunications

- 9.3 Consumer electronics

- 9.4 Automotive & transportation

- 9.5 Aerospace & defense

- 9.6 Industrial

- 9.7 Medical

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Anritsu Corporation

- 11.2 AR RF/Microwave Instrumentation

- 11.3 B&K Precision Corporation

- 11.4 Berkeley Nucleonics Corporation

- 11.5 Bird Technologies

- 11.6 Copper Mountain Technologies

- 11.7 Giga-tronics Incorporated

- 11.8 Keysight Technologies

- 11.9 National Instruments (NI)

- 11.10 Qorvo

- 11.11 Rigol Technologies

- 11.12 Rohde & Schwarz

- 11.13 Saelig Company, Inc.

- 11.14 Signal Hound

- 11.15 Teledyne LeCroy

- 11.16 Teledyne Technologies Incorporated

- 11.17 Thorlabs, Inc.

- 11.18 Vaunix Technology Corporation

- 11.19 Yokogawa Electric Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日