自動車用圧電燃料インジェクターの市場機会と成長促進要因、産業動向分析、2025~2034年予測

Automotive Piezoelectric Fuel Injectors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773453

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

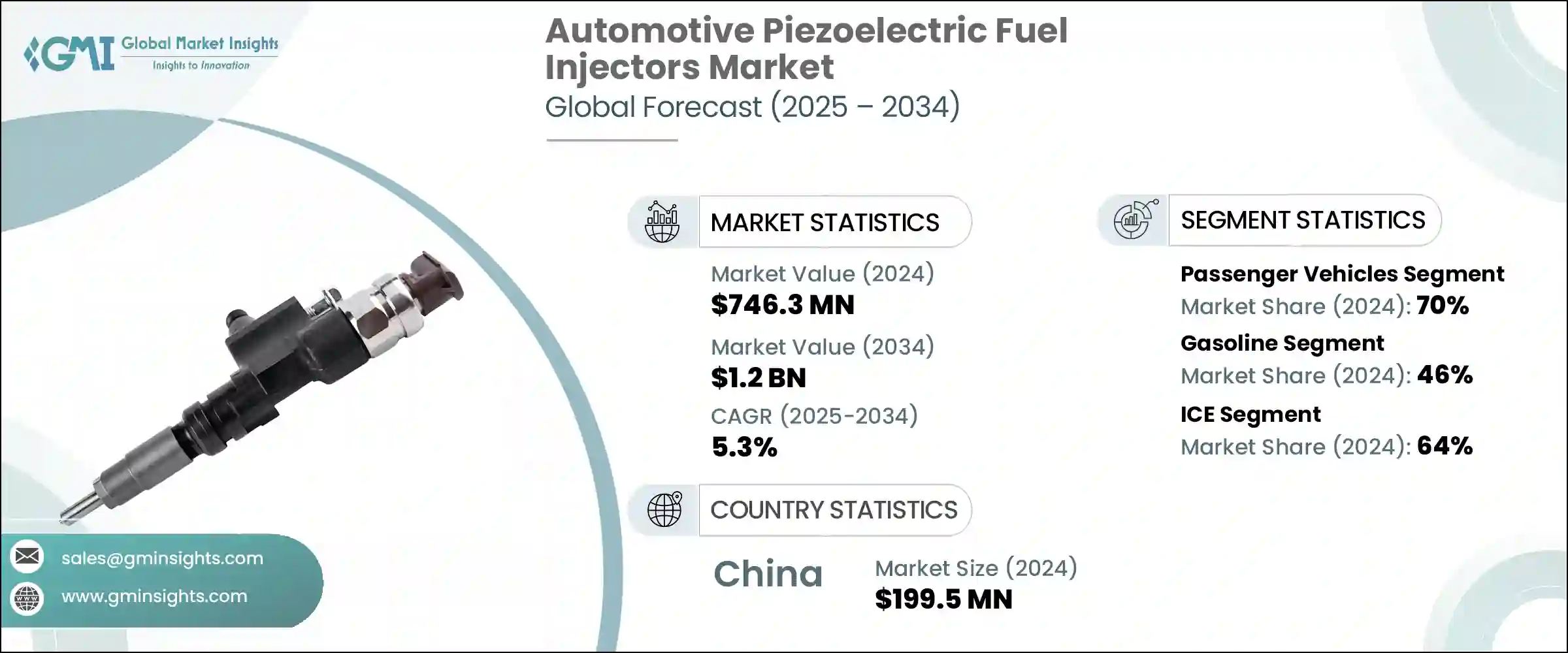

自動車用圧電燃料インジェクターの世界市場は、2024年には7億4,630万米ドルとなり、CAGR 5.3%で成長し、2034年には12億米ドルに達すると予測されています。

この市場の成長は、CRDIやGDIなどの先進エンジン技術の導入が進むとともに、自動車の排ガスに関する世界の規制が厳しくなっていることが背景にあります。これらのインジェクターは、迅速かつ極めて正確な燃料供給を可能にし、燃焼効率の向上と汚染物質の削減に大きく貢献します。

圧電インジェクターは、積極的な環境基準を持つ地域において、従来のソレノイド式に着実に取って代わりつつあります。スマートな電子制御ユニットや高度な診断機能との統合により、燃料流量をリアルタイムで調整できるようになり、エンジン性能の最適化と粒子状物質の排出量の低減が可能になります。また、よりクリーンなモビリティ・ソリューションへのシフトは、あらゆるタイプの車両プラットフォームにおける内燃アプリケーションの制御と効率を高めるため、こうした高精度部品の必要性を加速させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 7億4,630万米ドル |

| 予測金額 | 12億米ドル |

| CAGR | 5.3% |

圧電インジェクターは、単一の燃焼サイクル内で複数の超高速燃料噴射を可能にすることで、エンジン管理を再定義しています。この制御レベルは、エンジニアが比類のない精度で空気と燃料の混合気を微調整し、燃費を向上させ、排出ガスを大幅に削減するのに役立ちます。ユーロ7、BS-VIステージII、EPA第3次規制など、各国がより厳しい規制を導入するにつれて、これらの特性はますます重要になってきています。自動車分野は急速に進化しており、ピエゾベースのシステムは、特に、より速い応答時間とより高い噴射精度が要求されるシナリオにおいて、ソレノイドインジェクターの限界に対処するものと位置づけられています。

乗用車セグメントは2024年に市場をリードし、70%のシェアを占め、2034年までCAGR 5.5%で成長すると予測されています。この優位性は、乗用車、小型トラック、実用車の世界の生産・販売台数の多さに起因しています。アジア、欧州、北米のような地域における厳しい排ガス規制は、これらの車両クラスに高度な燃料噴射システムを組み込むことをメーカーに促しています。圧電燃料インジェクターは、性能と経済性を向上させながら規制基準を満たすのに役立ち、パワーと環境意識の両方に対する消費者の期待に応えます。その用途はハイブリッドやプラグインハイブリッドのプラットフォームで拡大しており、そこでは急速なオンオフサイクルとスタート・ストップ操作が、迅速かつ効率的に反応するインジェクタを要求しています。

ガソリン車セグメントは46%のシェアを占め、2025年から2034年にかけてCAGR 5.7%で成長すると予測されています。複数の大陸の規制機関が小型車の排ガス規制を進める中、ディーゼルに比べて粒子状物質や窒素酸化物の排出量が比較的少ないガソリンエンジンが魅力的になっています。自動車メーカーは、性能目標と排ガスベンチマークの両方を満たすために、圧電インジェクターで強化されたガソリン直噴システムに傾倒しています。ガソリンエンジンは、軽量、静粛性、生産コストの低さで支持されており、圧電インジェクターは、これらのエンジンの燃焼改善とスロットルレスポンスの向上に役立ち、ガソリンセグメントの重要なコンポーネントとしての地位を確保しています。

アジア太平洋自動車用圧電燃料インジェクター市場は67%のシェアを占め、1億9,950万米ドルを生み出しました。内燃自動車の大量生産と環境規制の強化が、高精度噴射技術の普及を後押ししています。中国の先進的な排ガス規制の採用は、よりクリーンな燃焼へのフォーカスを強め、圧電インジェクターシステムへの強い需要を生み出しています。さらに、Infineon、京セラ、Aptiv、シーメンスなどのTier-1部品メーカーは、地域市場のニーズに合わせたソリューションを提供するために国内企業と提携し、この地域での取り組みを強化しています。これらのパートナーシップは、商業用と旅客用の両方の用途にインジェクターの性能を最適化することに重点を置いており、競争力のあるコストを維持しながら、高い圧力しきい値での耐久性と効率を確保しています。

世界の自動車用圧電燃料インジェクター市場を積極的に形成している注目すべき企業には、京セラ、コンチネンタル、シーメンス、インフィニオン、日立アステモ・インディアナ、アプティブ、ロバート・ボッシュ、デンソー、日本特殊陶業、村田製作所などがあります。これらのメーカーは、燃料供給要件や排ガス規制の進化に対応するため、技術革新と投資を行っています。

自動車用圧電燃料インジェクター市場の主要メーカーは、強力な競争力を築くためにいくつかの戦略的分野に注力しています。第一に、インジェクターの速度、応答精度、燃料噴霧を改良し、より優れた排出ガス制御と燃焼効率を実現するための研究開発に多額の投資を行っています。第二に、ガソリン直噴システムやハイブリッドシステムに最適化された用途別インジェクターを開発するため、自動車OEMとの共同開発が行われています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- GDIおよびCRDIエンジンの採用増加

- 圧電材料の技術的進歩

- プレミアムおよび高級車セグメントの成長

- より厳しい排出規制

- OEMおよびTier 1サプライヤーによる研究開発投資の増加

- 業界の潜在的リスク&課題

- 圧電インジェクターの高コスト

- 改良型ソレノイドインジェクターとの競合

- 市場機会

- ハイブリッドパワートレインの採用増加

- 商用車におけるディーゼルエンジンの最適化

- ガソリン直噴(GDI)エンジンへの広範な移行

- デジタルエンジン管理とAI統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:車両別、2021~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第6章 市場推計・予測:燃料別、2021~2034年

- 主要動向

- ガソリン

- ディーゼル

- その他

第7章 市場推計・予測:販売チャネル別、2021~2034年

- 主要動向

- OEM

- アフターマーケット

第8章 市場推計・予測:推進力別、2021~2034年

- 主要動向

- ICE

- ハイブリッド

第9章 市場推計・予測:技術別、2021~2034年

- 主要動向

- 直噴(DI)

- コモンレール直噴(CRDI)

- ガソリン直噴(GDI)

- ポート燃料噴射(PFI)

第10章 市場推計・予測:動作圧力範囲別、2021~2034年

- 主要動向

- 低圧(200バール未満)

- 中圧(200~1000バール)

- 高圧(1000バール超)

第11章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第12章 企業プロファイル

- Aptiv

- Continental

- Delphi Technologies

- Denso Corporation

- Edelbrock LLC

- Fuzhou Ruida Machinery

- GB Remanufacturing

- Hitachi Astemo Indiana

- Infineon

- Keihin

- KYOCERA

- Magneti Marelli Parts and Services.

- Mikuni American

- Murata Manufacturing

- Robert Bosch

- Siemens

- Stanadyne

- Valley Fuel Injection &Turbo

- Woodward

- WUZETEM

目次

The Global Automotive Piezoelectric Fuel Injectors Market was valued at USD 746.3 million in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 1.2 billion by 2034. Growth in this market is being fueled by the increasing implementation of advanced engine technologies such as CRDI and GDI, alongside stricter global regulations around vehicle emissions. These injectors allow for rapid and extremely precise fuel delivery, which contributes significantly to enhanced combustion efficiency and reduced pollutants.

Piezoelectric injectors are steadily replacing traditional solenoid types in regions with aggressive environmental standards. Their integration with smart electronic control units and advanced diagnostics enables real-time adjustment of fuel flow, allowing for optimized engine performance and fewer particulate emissions. The shift toward cleaner mobility solutions is also accelerating the need for these high-precision components, as they offer greater control and efficiency in internal combustion applications across all types of vehicle platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $746.3 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 5.3% |

Piezoelectric injectors are redefining engine management by enabling multiple ultra-fast fuel injections within a single combustion cycle. This level of control helps engineers fine-tune the air-fuel mixture with unmatched accuracy, boosting fuel efficiency and significantly lowering emissions. These attributes are becoming increasingly important as countries implement tighter regulations like Euro 7, BS-VI Stage II, and EPA Tier 3. The automotive sector is evolving rapidly, with piezo-based systems positioned to address the limitations of solenoid injectors, especially in scenarios demanding faster response times and higher injection precision.

The passenger vehicles segment led the market in 2024, contributing 70% share, and is projected to grow at a CAGR of 5.5% through 2034. This dominance stems from the high global production and sales volumes of cars, light trucks, and utility vehicles. Stringent emission controls in regions like Asia, Europe, and North America are pushing manufacturers toward incorporating advanced fuel injection systems in these vehicle classes. Piezoelectric fuel injectors help meet regulatory thresholds while improving performance and economy, aligning with consumer expectations for both power and environmental consciousness. Their application is expanding in hybrid and plug-in hybrid platforms, where rapid on-off cycles and start-stop operation demand injectors that respond quickly and efficiently-qualities that piezo technology delivers consistently.

The gasoline vehicle segment held a 46% share, and it is projected to grow at a CAGR of 5.7% between 2025 and 2034. As regulatory bodies across multiple continents move to restrict emissions from light-duty vehicles, gasoline engines are becoming more attractive due to their relatively lower particulate and nitrogen oxide output compared to diesel. Automotive manufacturers are leaning into gasoline direct injection systems, enhanced with piezoelectric injectors, to meet both performance goals and emission benchmarks. With gasoline engines favored for their lighter weight, quieter operation, and lower cost of production, piezo injectors help these engines deliver improved combustion and better throttle response, securing their position as a key component in the gasoline segment.

Asia Pacific Automotive Piezoelectric Fuel Injectors Market held a 67% share, generating USD 199.5 million. The country's massive internal combustion vehicle output and increasingly rigorous environmental mandates are driving the widespread integration of high-precision injection technology. China's adoption of advanced emission standards has intensified the focus on cleaner combustion, creating a strong demand for piezoelectric injector systems. Additionally, Tier-1 component manufacturers such as Infineon, KYOCERA, Aptiv, and Siemens are intensifying their efforts in the region by collaborating with domestic firms to tailor solutions for regional market needs. These partnerships focus on optimizing injector performance for both commercial and passenger applications, ensuring durability and efficiency at elevated pressure thresholds while maintaining competitive costs.

Notable companies actively shaping the Global Automotive Piezoelectric Fuel Injectors Market include KYOCERA, Continental, Siemens, Infineon, Hitachi Astemo Indiana, Aptiv, Robert Bosch, Denso, NGK Spark Plug Co, and Murata Manufacturing. These players are innovating and investing to keep pace with the industry's evolving fuel delivery requirements and emissions legislation.

Major manufacturers in the automotive piezoelectric fuel injectors market are focusing on several strategic areas to build a strong competitive position. First, they are investing heavily in research and development to refine injector speed, response precision, and fuel atomization, enabling better emissions control and combustion efficiency. Second, collaborations with vehicle OEMs are being formed to develop application-specific injectors optimized for gasoline direct injection and hybrid systems.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Fuel type

- 2.2.4 Sales channel

- 2.2.5 Propulsions

- 2.2.6 Technology

- 2.2.7 Operating pressure range

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of GDI and CRDI engines

- 3.2.1.2 Technological advancements in Piezo materials

- 3.2.1.3 Growth of premium and luxury vehicle segments

- 3.2.1.4 Stricter emission regulations

- 3.2.1.5 Increased R&D investments by OEMs and Tier-1 suppliers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of piezoelectric injectors

- 3.2.2.2 Competition from improved solenoid injectors

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of hybrid powertrains

- 3.2.3.2 Diesel engine optimization in commercial vehicles

- 3.2.3.3 The widespread shift to gasoline direct injection (GDI) engines

- 3.2.3.4 Digital engine management and AI integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($ Mn, units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchbacks

- 5.2.2 Sedans

- 5.2.3 SUVs

- 5.3 Commercial vehicles

- 5.3.1 Light commercial vehicles (LCV)

- 5.3.2 Medium commercial vehicles (MCV)

- 5.3.3 Heavy commercial vehicles (HCV)

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.1.1 Gasoline

- 6.1.2 Diesel

- 6.1.3 Others

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 ICE

- 8.3 Hybrid

Chapter 9 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Direct injection (DI)

- 9.3 Common rail direct injection (CRDI)

- 9.4 Gasoline direct injection (GDI)

- 9.5 Port fuel injection (PFI)

Chapter 10 Market Estimates & Forecast, By Operating Pressure Range, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 Low pressure (<200 bar)

- 10.3 Medium pressure (200–1000 bar)

- 10.4 High pressure (>1000 bar)

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Aptiv

- 12.2 Continental

- 12.3 Delphi Technologies

- 12.4 Denso Corporation

- 12.5 Edelbrock LLC

- 12.6 Fuzhou Ruida Machinery

- 12.7 GB Remanufacturing

- 12.8 Hitachi Astemo Indiana

- 12.9 Infineon

- 12.10 Keihin

- 12.11 KYOCERA

- 12.12 Magneti Marelli Parts and Services.

- 12.13 Mikuni American

- 12.14 Murata Manufacturing

- 12.15 Robert Bosch

- 12.16 Siemens

- 12.17 Stanadyne

- 12.18 Valley Fuel Injection & Turbo

- 12.19 Woodward

- 12.20 WUZETEM

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日