|

市場調査レポート

商品コード

1773440

切削工具市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Cutting Tools Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 切削工具市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月24日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

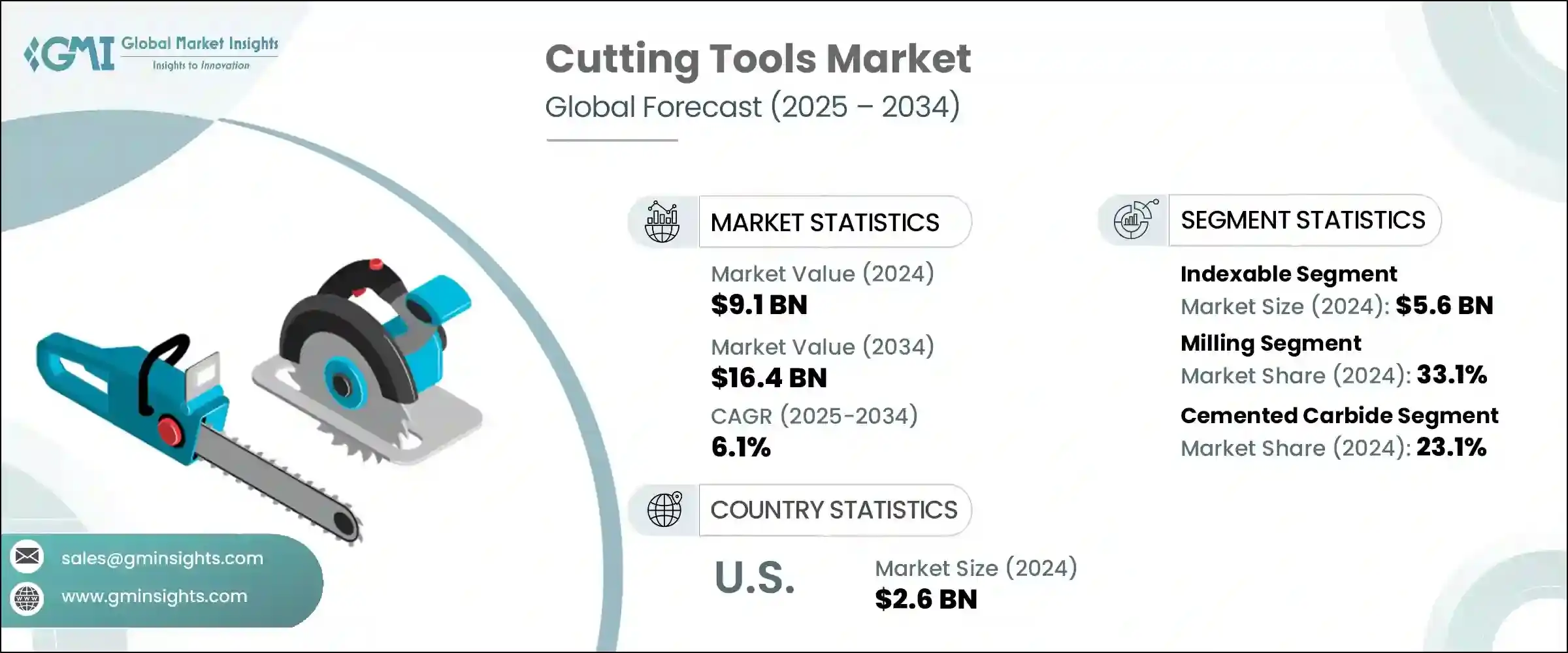

切削工具の世界市場規模は、2024年に91億米ドルとなり、CAGR 6.1%で成長し、2034年には164億米ドルに達すると予測されています。

この市場は、製造方法の進歩によって大きく成長しています。自動化とインダストリー4.0実践の台頭により、欠陥のない部品を製造できる精密工具への需要が高まっています。自動車、航空宇宙、エレクトロニクスなどの産業は、特にこのような精度から恩恵を受けています。

さらに、複合材料や高強度合金など、より軽量で強度の高い材料を使用する方向にシフトしているため、これらの強靭な材料を扱うことができる、より高度な切削工具が必要とされています。また、特に新興経済諸国ではインフラ・ブームが続いており、大型機械や現場設備に適した工具のニーズが高まっていることも重要な推進力となっています。また、原材料の使用量を最適化し、廃棄物を最小限に抑えることが重視されているため、耐久性が高く、コスト効率の高い切削工具が求められています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 91億米ドル |

| 予測金額 | 164億米ドル |

| CAGR | 6.1% |

さらに、切削工具業界では、より環境に優しい生産方法を求める動きが加速しており、企業は性能とともに持続可能性を優先するようになっています。メーカーは、原材料の調達から製造工程におけるエネルギー効率の改善まで、あらゆる段階で環境に優しい手法を採用しています。切削工具のコーティングや材料の進歩により、工具寿命の延長や廃棄物の削減が可能になり、切削効率も向上しています。さらに、リサイクルや再利用を重視する傾向が強まり、環境フットプリント全体が削減されています。また、多くの企業が、製造工程における有害排出物の削減と有害化学物質の使用の最小化に注力しています。

2024年には、刃先交換式工具セグメントは56億米ドルを生み出しました。この分野は、費用対効果と汎用性により人気が高まっています。刃先交換式工具は、工具全体を廃棄する代わりに、摩耗したチップを交換することができるため、運用コストの削減に貢献し、自動車や航空宇宙などの精密駆動産業において非常に魅力的です。また、これらの工具は高速加工をサポートし、メーカーにとって重要な効率性と耐久性を向上させる。交換可能なチップを使用することで、スクラップ金属の発生が少なくなり、廃棄物も削減されるため、環境に優しい製造プロセスに対する需要の高まりと一致し、持続可能性へのシフトがさらに魅力を高めています。

フライス工具セグメントは、2024年に33.1%のシェアを占めました。このセグメントの急拡大は、フライス工具が複数の産業において幅広い作業に対応できることに起因しています。これらの工具は、複雑なプロファイルを高精度で製造するために不可欠であり、自動車、航空宇宙、エレクトロニクスで一般的に使用されています。製品設計において、より軽量で耐久性のある部品が求められる中、フライス工具は、先端材料を切削する能力により、人気を集めています。多目的設計や改良されたコーティングなどの技術革新も、工具寿命の延長や運用コストの削減によって、このセグメントの成長に貢献しています。

米国の切削工具2024年の市場規模は26億米ドルで、世界市場をリードしています。米国の製造業は幅広い産業にまたがっており、この優位性を支える重要な要因となっています。自動車産業と航空宇宙産業が、厳しい品質基準を満たす高精度の工具の需要に拍車をかけています。さらに、製造業におけるロボット工学、センサー、クラウド分析の統合は、業務効率を高めることで市場の成長をさらに後押ししています。

大手企業は、工具の性能を向上させ、寿命を延ばすために研究開発に多額の投資を行っています。また、環境規制やより環境に優しい製品を求める消費者の需要に応えるため、持続可能な製造技術を積極的に模索しています。さらに、戦略的パートナーシップ、合併、買収を活用して、製品提供の拡大とサプライチェーンの強化を図っています。企業はまた、スマートセンサーやIoT対応デバイスなどのデジタルツールを取り入れて、製造の精度と業務効率を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 機会

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- ツールの種類別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ航空

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:ツールタイプ別、2021年~2034年

- 主要動向

- インデックス可能

- ソリッドラウンド

第6章 市場推計・予測:工程別、2021年~2034年

- 主要動向

- フライス加工

- 掘削

- 穿孔

- 旋回

- 研削

- その他

第7章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 超硬合金

- 高速度鋼(HSS)

- セラミックス

- 立方晶窒化ホウ素(CBN)

- 多結晶ダイヤモンド(PCD)

- エキゾチック材料

- ステンレス鋼

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 自動車

- 航空宇宙および防衛

- 建設

- エレクトロニクス

- 発電

- 石油・ガス

- 木工

- 金型製造

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接

- 間接

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- マレーシア

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Ceratizit S.A.

- Cougar Cutting Tools

- Emuge Corporation

- Greenleaf Corporation

- Ingersoll Cutting Tools

- Iscar Ltd.

- Kennametal Inc.

- Mapal Inc.

- Mitsubishi Materials Corporation

- Mohawk Special Cutting Tools

- OSG Corporation

- Sandvik Coromant

- Seco Tools AB

- Tungaloy Corporation

- Walter Technologies

The Global Cutting Tools Market was valued at USD 9.1 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 16.4 billion by 2034. This market is experiencing significant growth, driven largely by advancements in manufacturing methods. With the rise of automation and Industry 4.0 practices, there is an increasing demand for precision tools that can produce defect-free parts. Industries like automotive, aerospace, and electronics particularly benefit from such accuracy.

Additionally, the shift toward using lighter and stronger materials, including composites and high strength alloys, necessitates more advanced cutting tools that can handle these tough materials. Another key driver is the ongoing infrastructure boom, especially in rapidly developing economies, which raises the need for tools suitable for large machines and site equipment. Along with this, the focus on optimizing raw material use and minimizing waste continues to push manufacturers toward more durable, cost-effective cutting tools.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.1 Billion |

| Forecast Value | $16.4 Billion |

| CAGR | 6.1% |

Furthermore, the drive for greener production methods is accelerating within the cutting tools industry, as companies increasingly prioritize sustainability alongside performance. Manufacturers are adopting eco-friendly practices at every stage, from sourcing raw materials to improving energy efficiency during the manufacturing process. Advances in cutting tool coatings and materials are enabling longer tool lifespans and reduced waste, while also enhancing cutting efficiency. Additionally, there is a growing emphasis on recycling and reusing cutting tools, reducing the overall environmental footprint. Many companies are also focusing on reducing hazardous emissions and minimizing the use of harmful chemicals during the production process.

In 2024, the indexable tools segment generated USD 5.6 billion. This segment is growing in popularity due to its cost-effectiveness and versatility. Indexable tools allow users to replace worn-out inserts instead of discarding the entire tool, which helps lower operational costs, making them highly attractive in precision-driven industries like automotive and aerospace. These tools also support high-speed machining, enhancing efficiency and durability, which are crucial for manufacturers. The shift toward sustainability further adds to their appeal, as using replaceable inserts generates less scrap metal and reduces waste, aligning with the growing demand for greener manufacturing processes.

The milling tools segment accounted for a 33.1% share in 2024. The rapid expansion of this segment can be attributed to the wide range of tasks milling tools are capable of handling in multiple industries. These tools are essential for producing complex profiles with high precision, and they are commonly used in automotive, aerospace, and electronics. As product designs demand lighter yet more durable parts, milling tools are gaining popularity due to their ability to cut through advanced materials. Innovations, such as multi-purpose designs and improved coatings, have also contributed to the segment's growth by extending tool life and reducing operational costs.

United States Cutting Tools Market was valued at USD 2.6 billion in 2024, leading the global market. The U.S. manufacturing sector, which spans a wide range of industries, is a key factor driving this dominance. The automotive and aerospace sectors fuel the demand for highly accurate tools that meet stringent quality standards. Additionally, the integration of robotics, sensors, and cloud analytics in manufacturing further boosts market growth by enhancing operational efficiency.

Key companies in the Cutting Tools Industry include Ceratizit S.A., Cougar Cutting Tools, Emuge Corporation, Greenleaf Corporation, Ingersoll Cutting Tools, Iscar Ltd., Kennametal Inc., Mapal Inc., Mitsubishi Materials Corporation, Mohawk Special Cutting Tools, OSG Corporation, Sandvik Coromant, Seco Tools AB, Tungaloy Corporation, and Walter Technologies. In response to the increasing demand for cutting-edge products, companies in the cutting tools market are focusing on technological advancements to enhance their market position.

Leading players are investing heavily in research and development to improve the performance of their tools and increase their lifespan. They are also actively exploring sustainable manufacturing techniques to meet environmental regulations and consumer demands for greener products. Additionally, strategic partnerships, mergers, and acquisitions are being utilized to expand product offerings and strengthen supply chains. Companies are also incorporating digital tools, such as smart sensors and IoT-enabled devices, to enhance precision and operational efficiency in manufacturing.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Tool type

- 2.2.3 Process

- 2.2.4 Material Type

- 2.2.5 End Use

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By tool type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 MEA

- 4.2.1.5 LATAM

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Tool Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Indexable

- 5.3 Solid Round

Chapter 6 Market Estimates & Forecast, By Process, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Milling

- 6.3 Drilling

- 6.4 Boring

- 6.5 Turning

- 6.6 Grinding

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Material Type, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Cemented Carbide

- 7.3 High-Speed Steel (HSS)

- 7.4 Ceramics

- 7.5 Cubic Boron Nitride (CBN)

- 7.6 Polycrystalline Diamond (PCD)

- 7.7 Exotic Materials

- 7.8 Stainless Steel

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Aerospace & Defense

- 8.4 Construction

- 8.5 Electronics

- 8.6 Power Generation

- 8.7 Oil & Gas

- 8.8 Woodworking

- 8.9 Die and Mold Manufacturing

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Ceratizit S.A.

- 11.2 Cougar Cutting Tools

- 11.3 Emuge Corporation

- 11.4 Greenleaf Corporation

- 11.5 Ingersoll Cutting Tools

- 11.6 Iscar Ltd.

- 11.7 Kennametal Inc.

- 11.8 Mapal Inc.

- 11.9 Mitsubishi Materials Corporation

- 11.10 Mohawk Special Cutting Tools

- 11.11 OSG Corporation

- 11.12 Sandvik Coromant

- 11.13 Seco Tools AB

- 11.14 Tungaloy Corporation

- 11.15 Walter Technologies