|

|

市場調査レポート

商品コード

1773434

ギアボックスおよびギアモーター市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Gearbox and Gear Motors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ギアボックスおよびギアモーター市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月19日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

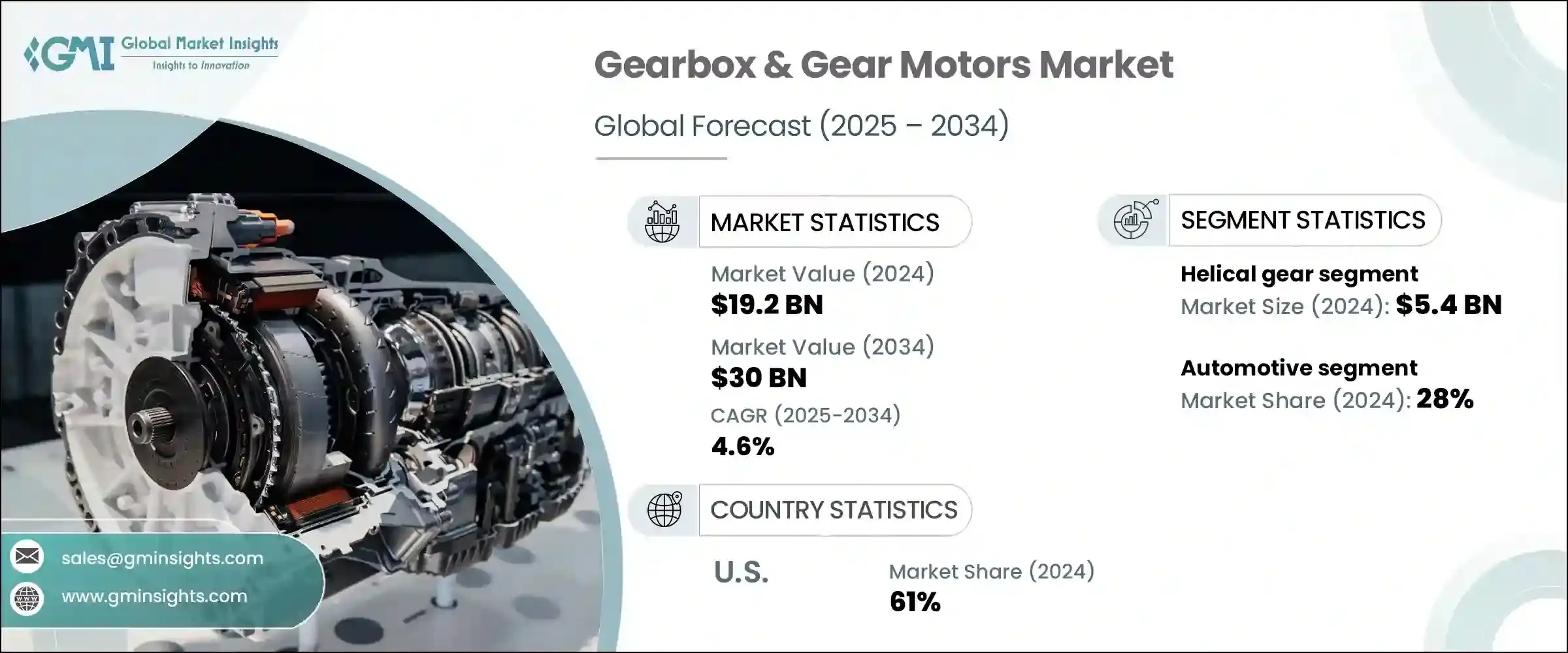

ギアボックスおよびギアモーターの世界市場は、2024年に192億米ドルと評価され、CAGR 4.6%で成長し、2034年には300億米ドルに達すると推定されています。

電気自動車の人気が高まっていることに加え、産業オートメーションの拡大やロボット工学の進歩が引き続き市場の需要を牽引しています。クリーンエネルギー源、特に風力エネルギーへの投資の増加は、様々な動力用途における信頼性が高く高性能なギアモーターの必要性をさらに高めています。世界中の産業がインフラの近代化とエネルギー効率の改善に重点を置いているため、革新的なギアボックス技術に対する需要が急増しています。

特にエネルギー分野では、エネルギー捕捉を強化し、回転効率を最適化するギアモーターの重要性が高まっています。その結果、市場は自動車、製造、発電を含むいくつかの最終用途の垂直分野で力強い成長を目の当たりにしています。しかし、このような拡大にもかかわらず、高い維持費が依然として顕著な障壁となっています。ギヤアセンブリ、モーター、制御システムが一体化されているため複雑さが増し、専門的なサービスが必要になることが多いです。また、部品価格の変動や専門家によるメンテナンスの必要性も、運用コストの上昇の一因となっており、コストに敏感な市場での幅広い採用を妨げる要因となっています。とはいえ、現在進行中の研究開発と製品の改良は、長期的なメンテナンスの懸念の軽減に役立っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 192億米ドル |

| 予測金額 | 300億米ドル |

| CAGR | 4.6% |

ヘリカルギア分野は、2024年に54億米ドルを生み出しました。これらのモーターは、角度のついた歯で設計されており、振動や作動音を最小限に抑え、効率を高めています。ヘリカルギアは、クレーン、ホイストシステム、コンベア機械、重工業用工具など、滑らかな動きと負荷容量を必要とする産業でよく見られます。これらのギアソリューションは、製造業、オートメーションシステム、医療機器などの高精度アプリケーションを含む、静かな動作とトルク性能が重要な環境に適しています。また、大きな負荷を管理し、高トルクを提供する能力により、マテリアルハンドリング、鉱業、インフラストラクチャなどの分野にも適しています。

2024年には、自動車分野が28%のシェアを占めています。様々なカテゴリーで毎年何百万台もの自動車が生産されているため、この分野ではギア駆動システムに対する大規模かつ安定した需要が生まれ続けています。電気、ハイブリッド、または従来の内燃エンジンのいずれの構成であっても、ギアボックスは最適な動力伝達のために不可欠であり続けています。自動車産業における急速な技術革新は、燃費の向上、高度な安全技術、シームレスな運転体験をサポートするギアコンポーネントへのニーズをさらに高めています。現代の自動車は、進化する排ガス規制や性能要件に合わせて、多段変速システムやスマートギア機構を搭載しています。

米国のギアボックスおよびギアモーター市場は、2024年に61%のシェアを占めました。この市場の成長を支えているのは、産業オートメーションとスマート製造コンセプトの広範な導入です。建設、包装、食品製造、製薬など複数の分野で、効率的な動力伝達技術の採用が進んでいます。さらに、産業用ロボットやエネルギー・インフラへの投資の増加が新たな機会を生み出しています。効率、信頼性、コンパクト設計を重視する米国メーカーは、カスタマイズ可能な製品ライン、メンテナンス軽減設計、状態監視と予知保全が可能なインテリジェントシステムを提供することで技術革新を推進しています。

ギアボックスおよびギアモーターの世界市場を形成する主要企業には、Bonfiglioli S.p.A.、Elecon Engineering Co.Ltd.、Portescap、NORD Drivesystems Group、Shanthi Gears Limited、Nidec Corporation、Top Gear Transmissions、Dunkermotoren、SEW-EURODRIVE GmbH &Co.KG、Regal Rexnord Corporation、Siemens AG、Flender International GmbH、ABB、住友重機械工業株式会社、NGL。市場での地位を強化するために、主要なギアボックス、ギアモーターメーカーは様々な積極的な戦略を採用しています。

その多くは、製品開発に多額の投資を行い、寿命が長くメンテナンスの必要性が少ない、高効率で低騒音のソリューションを開発しています。各社はまた、世界サプライチェーンを強化し、各地域の需要への対応力を高めるために現地生産施設を設立しています。戦略的パートナーシップや買収は、企業が新市場を開拓し、製品ポートフォリオを拡大するのに役立っています。さらに、いくつかのメーカーは、インダストリー4.0へのシフトに合わせて、リアルタイムの診断と予知保全のためのスマートモニタリングシステムを組み込んでいます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 電気自動車の需要増加

- 再生可能エネルギー部門の成長

- 産業オートメーションとロボット工学の進歩

- 業界の潜在的リスク&課題

- 高いメンテナンスコスト

- 原材料費の変動

- 機会

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- ヘリカルギア

- 遊星歯車

- ベベルギア

- ウォームギア

- その他

第6章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ギアボックス

- ギアモーターユニット

第7章 市場推計・予測:定格出力別、2021年~2034年

- 主要動向

- 7.5kW未満

- 7.5kW~75kW

- 75kW以上

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- マテリアルハンドリング

- 自動車

- 飲食品

- 医療

- 風力

- 金属および鉱業

- その他

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接

- 間接

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- ABB

- Bonfiglioli S.p.A.

- Dunkermotoren

- Elecon Engineering Co. Ltd.

- Flender International GmbH

- NGL

- Nidec Corporation

- NORD Drivesystems Group

- Portescap

- Regal Rexnord Corporation

- SEW-EURODRIVE GmbH &Co. KG

- Shanthi Gears Limited

- Siemens AG

- Sumitomo Heavy Industries Ltd.

- Top Gear Transmissions

The Global Gearbox & Gear Motors Market was valued at USD 19.2 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 30 billion by 2034. The rising popularity of electric vehicles, along with expanding industrial automation and advancements in robotics, continues to drive market demand. Growing investments in clean energy sources, particularly wind energy, are further boosting the need for dependable and high-performing gear motors across various power applications. As industries worldwide focus on modernizing infrastructure and improving energy efficiency, the demand for innovative gearbox technologies is surging.

Gear motors, especially in energy sectors, are becoming increasingly critical due to their ability to enhance energy capture and optimize rotational efficiency. As a result, the market is witnessing strong growth in several end-use verticals, including automotive, manufacturing, and power generation. However, despite this expansion, high upkeep expenses remain a notable barrier. The integrated nature of gear assemblies, motors, and control systems increases complexity, often requiring specialized servicing. Variability in component prices and the need for expert maintenance also contribute to elevated operational costs, which can deter broader adoption in cost-sensitive markets. Nevertheless, ongoing R&D and product enhancements are helping reduce long-term maintenance concerns.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $19.2 Billion |

| Forecast Value | $30 Billion |

| CAGR | 4.6% |

The helical gear segment generated USD 5.4 billion in 2024. These motors are designed with angled teeth, minimizing vibration and operating noise and boosting efficiency. They're commonly found in industries requiring smooth motion and load capacity, such as cranes, hoisting systems, conveyor machinery, and heavy industrial tools. These gear solutions are well-suited for environments where quiet operation and torque performance are vital, including high-precision applications in manufacturing, automation systems, and medical devices. Their capacity to manage significant loads and deliver high torque also makes them favorable for sectors such as material handling, mining, and infrastructure.

In 2024, the automotive segment accounted for a 28% share. With millions of vehicles produced each year across various categories, the sector continues to generate a massive and consistent demand for gear-driven systems. Whether in electric, hybrid, or traditional internal combustion engine configurations, gearboxes remain essential for optimal power delivery. Rapid innovation within the automotive industry is further increasing the need for gear components that support enhanced fuel efficiency, advanced safety technologies, and seamless driving experiences. Modern vehicles are being equipped with multi-speed systems and smart gear mechanisms tailored for evolving emission regulations and performance requirements.

United States Gearbox & Gear Motors Market held a 61% share in 2024. Growth in this market is supported by the widespread implementation of industrial automation and smart manufacturing concepts. Multiple sectors-including construction, packaging, food production, and pharmaceuticals-are increasingly adopting efficient power transmission technologies. Additionally, rising investments in industrial robotics and energy infrastructure are creating new opportunities. With an emphasis on efficiency, reliability, and compact design, US manufacturers push innovation by offering customizable product lines, reduced-maintenance designs, and intelligent systems capable of condition monitoring and predictive maintenance.

Key companies shaping the Global Gearbox & Gear Motors Market include Bonfiglioli S.p.A., Elecon Engineering Co. Ltd., Portescap, NORD Drivesystems Group, Shanthi Gears Limited, Nidec Corporation, Top Gear Transmissions, Dunkermotoren, SEW-EURODRIVE GmbH & Co. KG, Regal Rexnord Corporation, Siemens AG, Flender International GmbH, ABB, Sumitomo Heavy Industries Ltd., and NGL. To strengthen their market standing, leading gearbox, and gear motor manufacturers are adopting a range of proactive strategies.

Many are investing significantly in product development to create high-efficiency and low-noise solutions with longer lifespans and reduced maintenance needs. Companies are also enhancing their global supply chains and establishing local production facilities to ensure better responsiveness to regional demands. Strategic partnerships and acquisitions are helping firms tap into new markets and extend product portfolios. Additionally, several manufacturers are incorporating smart monitoring systems for real-time diagnostics and predictive maintenance, aligning with the shift toward Industry 4.0.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Product Type

- 2.2.4 Rated Power

- 2.2.5 End use Industry

- 2.2.6 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for electrical vehicles

- 3.2.1.2 Growth in renewable energy sector

- 3.2.1.3 Advancements in industrial automation and robotics

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High maintenance costs

- 3.2.2.2 Fluctuations in raw material costs

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Helical gear

- 5.3 Planetary gear

- 5.4 Bevel gear

- 5.5 Worm gear

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Gearbox

- 6.3 Gear motor unit

Chapter 7 Market Estimates and Forecast, By Rated Power, 2021 - 2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Up to 7.5 kW

- 7.3 7.5 kW to 75 kW

- 7.4 Above 75 kW

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Material handling

- 8.3 Automotive

- 8.4 Food and beverages

- 8.5 Medical

- 8.6 Wind power

- 8.7 Metals and mining

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 Bonfiglioli S.p.A.

- 11.3 Dunkermotoren

- 11.4 Elecon Engineering Co. Ltd.

- 11.5 Flender International GmbH

- 11.6 NGL

- 11.7 Nidec Corporation

- 11.8 NORD Drivesystems Group

- 11.9 Portescap

- 11.10 Regal Rexnord Corporation

- 11.11 SEW-EURODRIVE GmbH & Co. KG

- 11.12 Shanthi Gears Limited

- 11.13 Siemens AG

- 11.14 Sumitomo Heavy Industries Ltd.

- 11.15 Top Gear Transmissions