|

市場調査レポート

商品コード

1773421

動物用除細動器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Veterinary Defibrillators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 動物用除細動器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月16日

発行: Global Market Insights Inc.

ページ情報: 英文 142 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

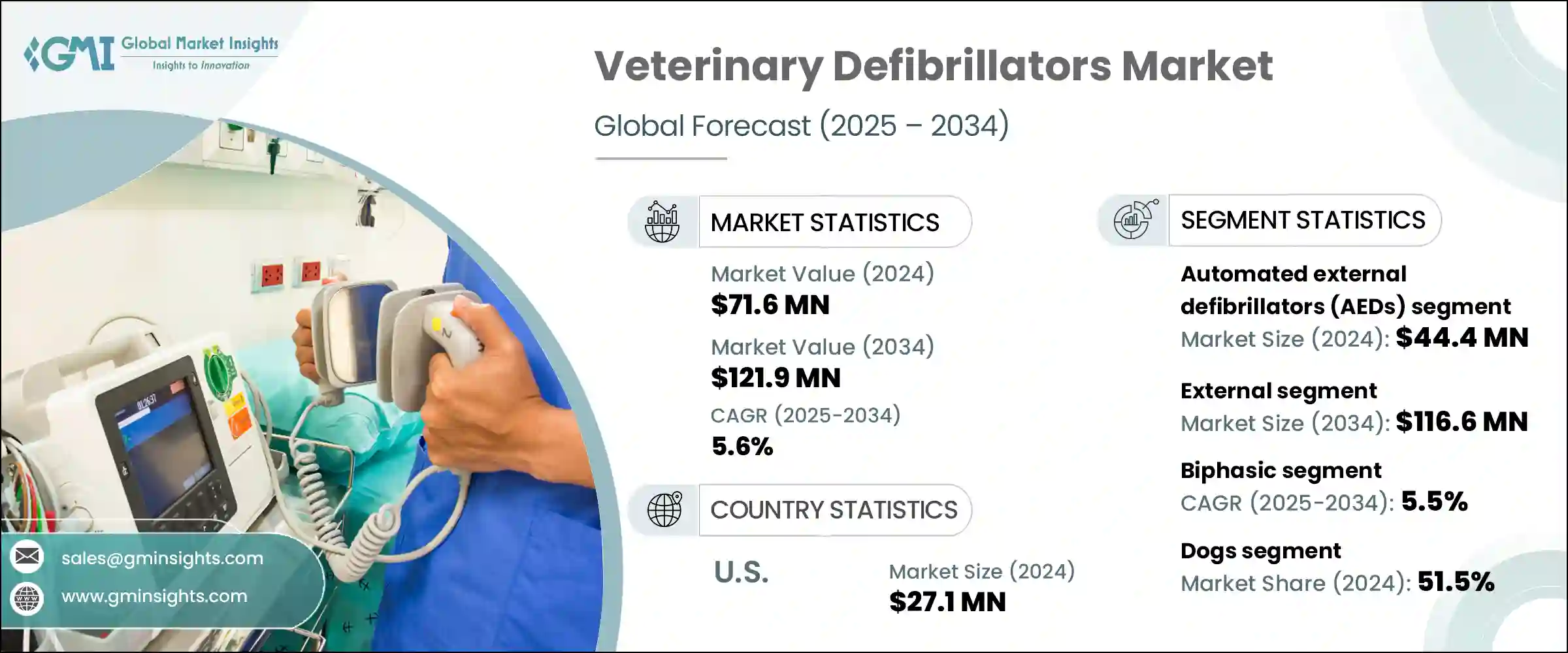

動物用除細動器の世界市場は、2024年には7,160万米ドルと評価され、CAGR 5.6%で成長し、2034年には1億2,190万米ドルに達すると予測されています。

動物における心血管系の問題の発生が増加していることが、市場の需要を煽る主な要因となっています。この成長は、動物病院、診療所、救急医療施設の数の増加によってさらに支えられています。24時間体制の動物救急サービスや専門的な心臓治療により、除細動器、特にマルチパラメーター機能を備えた除細動器のニーズが高まっています。小型で持ち運びができ、使いやすい自動体外式除細動器(AED)の最近の進歩により、小規模な診療所や移動診療所にも普及し、救命技術をより広く利用できるようになっています。

アクセシビリティの向上は、操作性の改善や最新のモニタリング・ツールとの統合と相まって、より幅広い獣医学的用途での採用を後押ししています。心臓の健康を優先する飼い主が増え、緊急時に適時に除細動を行うことの利点に関する認識が広まるにつれて、動物病院はこうした救命機器の重要性を認識しつつあります。ペットの飼育率の上昇と動物ケアの水準の向上は、特にインフラが確立され継続的に拡大している新興国市場において、手動および自動の両ソリューションに対する長期的な需要に寄与しています。動物用除細動器は、不整脈や突然の心停止の際に動物に治療用の電気ショックを与えます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7,160万米ドル |

| 予測金額 | 1億2,190万米ドル |

| CAGR | 5.6% |

2024年、自動体外式除細動器(AED)分野の売上高は4,440万米ドルでした。AEDの高い普及率は、その直感的なデザインとユーザーガイド機能によるところが大きいです。除細動プロセスを通じて獣医師を支援する内蔵アルゴリズムが、中小規模の診療所や移動ユニットでの使用を促進しています。心臓のリズムを瞬時に評価し、必要なショックを与えることができるため、迅速な対応シナリオに不可欠です。コンパクトな形状、充電式電源、統合されたモニタリング機能などが、AEDの多用途性を支えています。AEDは、従来の診療所だけでなく、移動獣医サービス、救助活動、遠隔地の動物保健施設などでも使用されるようになってきており、このセグメントの継続的な拡大に大きく貢献しています。

二相式除細動器セグメントは、2034年までCAGR 5.5%で成長すると予測されています。これらの装置は二相のショック伝達を利用し、より効率的かつ制御された電流の流れを心臓に流すことができるため、特に心臓血管系に敏感な動物に有益です。必要なエネルギーが低いため、組織損傷のリスクが軽減され、これは小型のペットを治療する際には極めて重要です。二相性技術の強化された安全性と有効性は、獣医師の間で好ましい選択肢として位置づけられています。このセグメントの成長は、最新のマルチパラメーターモニターとの高い互換性と、ICUや外科病棟のようなクリティカルケア環境への統合によっても推進されています。高度なショック・アルゴリズムと高負荷の医療現場での適応性により、獣医の専門医や教育病院はますますこれらのシステムを好むようになっています。

米国の動物用除細動器市場は2024年に2,710万米ドルに達しました。この一貫した増加は、ペット飼育の増加、獣医インフラの改善、動物の救急医療への注目の高まりを反映しています。ペット保険の普及もハイエンド技術へのアクセスを支えており、より多くの飼い主が二相性除細動器やAEDのような機器を購入できるようになっています。ペットの心臓ケアをより充実させようという動きが、動物病院におけるより強固で技術的な設備を備えた緊急対応システムを育んでいます。

世界の動物用除細動器市場を形成している主要企業は、Mindray Medical International Limited、Avante Animal Health、Wuhan Union Medical Technology、New Gen Medical Systems、Shinova Medical、ARI Medical Technology、Infinium Medical、Shenzhen Comen Medical Instruments、Promed Technology、Chongqing Vision Star Optical、Kalstein、Digicare Biomedical、Meditech Equipment、Hefei Eur Vet Technology、Zucami Medicalなどです。市場での地位を確保・強化するため、新興国市場の大手動物用除細動器メーカーは、使いやすさと高度な臨床機能を兼ね備えたコンパクトなポータブル機器の開発に積極的に投資しています。インテリジェントショックアルゴリズムとマルチパラメータモニタリングを手動式とAEDシステムの両方に統合することで、製品価値を高めています。動物病院や救急医療プロバイダーとの戦略的パートナーシップにより、各ブランドは実世界のニーズを理解し、それに応じてソリューションを調整することができます。さらに、各社は世界の販売網を拡大し、動物医療のインフラがまだ発展途上にある未開拓地域に参入しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- ペット飼育の増加とペットの人間化

- ペットの心臓疾患の発生率増加

- 獣医学技術の進歩

- 業界の潜在的リスク&課題

- 除細動器の高コスト

- 意識と訓練の欠如

- 機会

- 救急・重篤医療サービスの需要増加

- 発展途上地域における獣医インフラへの投資増加

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- 消費者行動分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 自動体外除細動器(AED)

- 手動式除細動器

第6章 市場推計・予測:モダリティ別、2021年~2034年

- 主要動向

- 外部

- 内部

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 二相性

- 単相性

第8章 市場推計・予測:動物タイプ別、2021年~2034年

- 主要動向

- 犬

- 猫

- 馬

- その他の動物タイプ

第9章 市場推計・予測:機能別、2021年~2034年

- 主要動向

- 標準

- マルチパラメータ機能

第10章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 動物病院および診療所

- 獣医研究機関

- その他の用途

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- ARI Medical Technology

- Avante Animal Health

- Chongqing Vision Star Optical

- Digicare Biomedical

- Hefei Eur Vet Technology

- Infinium Medical

- Kalstein

- Meditech Equipment

- Mindray Medical International Limited

- New Gen Medical Systems

- Promed Technology

- Shenzhen Comen Medical Instruments

- Shinova Medical

- Wuhan Union Medical Technology

The Global Veterinary Defibrillators Market was valued at USD 71.6 million in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 121.9 million by 2034. Increasing occurrences of cardiovascular issues in animals are a major driver fueling market demand. The growth is further supported by the rising number of veterinary hospitals, clinics, and emergency care facilities. Around-the-clock animal emergency services and specialized cardiac care are increasing the need for defibrillators, particularly those equipped with multiparameter functionalities. Recent advancements in compact, portable, and easy-to-use automated external defibrillators (AEDs) are extending their reach to smaller clinics and mobile practices, enabling broader access to life-saving technologies.

Enhanced accessibility, combined with improvements in ease of operation and integration with modern monitoring tools, is helping drive adoption across a wider range of veterinary applications. As more pet owners prioritize cardiac health, and as awareness spreads regarding the benefits of timely defibrillation during emergencies, veterinary practices are recognizing the importance of these life-saving devices. Increased pet adoption rates and the rising standards of animal care are contributing to long-term demand for both manual and automated solutions, particularly in developed markets where infrastructure is well-established and continually expanding. Veterinary defibrillators deliver therapeutic electrical shocks to animals in cases of cardiac arrhythmia or sudden cardiac arrest.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $71.6 Million |

| Forecast Value | $121.9 Million |

| CAGR | 5.6% |

In 2024, the automated external defibrillators (AEDs) segment generated USD 44.4 million. The high adoption rate of AEDs is largely due to their intuitive design and user-guided functionality. Built-in algorithms that assist veterinarians through the defibrillation process are encouraging their use in small and mid-size practices, as well as in mobile units. Their ability to instantly assess heart rhythms and deliver the necessary shock makes them essential for rapid-response scenarios. Compact form, rechargeable power, and integrated monitoring capabilities support their versatility. AEDs are being increasingly used beyond traditional clinics, in mobile veterinary services, rescue operations, and animal health facilities in remote areas, which contributes significantly to the segment's ongoing expansion.

The biphasic defibrillators segment is projected to grow at a CAGR of 5.5% through 2034. These devices utilize dual-phase shock delivery, allowing more efficient and controlled current flow through the heart, which is particularly beneficial for animals with sensitive cardiovascular systems. Lower energy requirements reduce tissue damage risks, which is crucial when treating small pets. The enhanced safety and effectiveness of biphasic technology are positioning it as a preferred option among veterinarians. The segment's growth is also driven by its high compatibility with contemporary multiparameter monitors and integration into critical care environments like ICUs and surgical units. Veterinary specialists and teaching hospitals increasingly favor these systems due to their advanced shock algorithms and adaptability in high-intensity medical settings.

United States Veterinary Defibrillators Market reached USD 27.1 million in 2024. This consistent increase reflects growing pet ownership, improvements in veterinary infrastructure, and a heightened focus on emergency animal care. Pet insurance adoption is also supporting access to high-end technologies, enabling more pet owners to afford devices like biphasic defibrillators and AEDs. The push for better cardiac care in pets is fostering a more robust and technologically equipped emergency response system in veterinary practices.

Key players shaping the Global Veterinary Defibrillators Market include Mindray Medical International Limited, Avante Animal Health, Wuhan Union Medical Technology, New Gen Medical Systems, Shinova Medical, ARI Medical Technology, Infinium Medical, Shenzhen Comen Medical Instruments, Promed Technology, Chongqing Vision Star Optical, Kalstein, Digicare Biomedical, Meditech Equipment, Hefei Eur Vet Technology, and Zucami Medical. To secure and strengthen their market position, leading veterinary defibrillator manufacturers are actively investing in the development of compact, portable devices that combine ease of use with sophisticated clinical features. Integration of intelligent shock algorithms and multiparameter monitoring into both manual and AED systems is helping enhance product value. Strategic partnerships with veterinary hospitals and emergency care providers allow brands to understand real-world needs and tailor solutions accordingly. Additionally, companies are broadening their global distribution networks and entering underserved regions where veterinary care infrastructure is still evolving.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Modality

- 2.2.4 Technology

- 2.2.5 Animal type

- 2.2.6 Functionality

- 2.2.7 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership and humanization of pets

- 3.2.1.2 Increasing incidence of cardiac disorders in pets

- 3.2.1.3 Advancements in veterinary medical technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of defibrillators

- 3.2.2.2 Lack of awareness and training

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for emergency and critical care services

- 3.2.3.2 Growing investments in veterinary infrastructure in developing regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Consumer behaviour analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Automated external defibrillators (AEDs)

- 5.3 Manual defibrillators

Chapter 6 Market Estimates and Forecast, By Modality, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 External

- 6.3 Internal

Chapter 7 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Biphasic

- 7.3 Monophasic

Chapter 8 Market Estimates and Forecast, By Animal Type, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Dogs

- 8.3 Cats

- 8.4 Horses

- 8.5 Other animal types

Chapter 9 Market Estimates and Forecast, By Functionality, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Standard

- 9.3 Multiparameter-capability

Chapter 10 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Veterinary hospitals and clinics

- 10.3 Veterinary research institutes

- 10.4 Other end use

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 ARI Medical Technology

- 12.2 Avante Animal Health

- 12.3 Chongqing Vision Star Optical

- 12.4 Digicare Biomedical

- 12.5 Hefei Eur Vet Technology

- 12.6 Infinium Medical

- 12.7 Kalstein

- 12.8 Meditech Equipment

- 12.9 Mindray Medical International Limited

- 12.10 New Gen Medical Systems

- 12.11 Promed Technology

- 12.12 Shenzhen Comen Medical Instruments

- 12.13 Shinova Medical

- 12.14 Wuhan Union Medical Technology