|

市場調査レポート

商品コード

1773336

加硫ソリッドゴムの市場機会と促進要因、業界動向分析、2025~2034年予測Vulcanised Solid Rubber Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 加硫ソリッドゴムの市場機会と促進要因、業界動向分析、2025~2034年予測 |

|

出版日: 2025年06月27日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

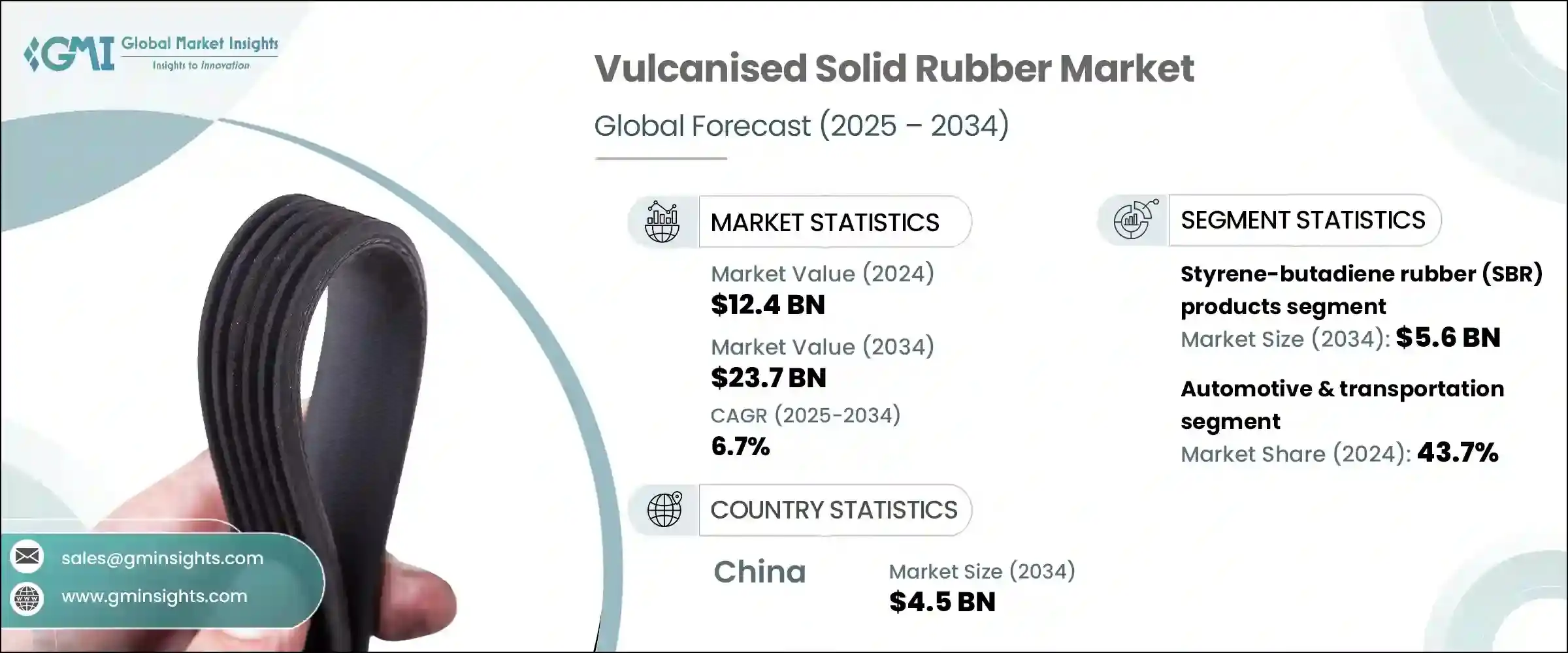

加硫ソリッドゴムの世界市場規模は、2024年に124億米ドルとなり、CAGR 6.7%で成長し、2034年には237億米ドルに達すると予測されています。

この増加傾向は、特に欧州のような既に確立された地域や中国のような急速に経済が発展している地域における、自動車産業や建設産業全体での消費の増加によって大きく後押しされています。加硫ソリッドゴムは、その優れた耐候性、高い耐久性、弾力性により、さまざまな産業用途に不可欠な材料として支持され続けています。シーリング、振動減衰、保護パッド、耐久性のある床材システムなど、その性能は世界中の産業でますます信頼されています。機械的ストレスが高く、さまざまな環境要因にさらされる環境下でも優れた性能を発揮するため、成熟市場と新興市場の両方で安定した需要があります。

温度変動に耐え、信頼性の高い断熱性を発揮するこの素材は、長寿命と弾力性を必要とする製造環境において好ましい選択肢となっています。世界的に、特に東南アジアや中東の一部でインフラ投資が回復するなか、長期的な効率性を求めて工業用ゴムソリューションに注目するプロジェクトが増えています。一方、自動車セクターの変革、特に電気自動車やハイブリッド車へのシフトが進行していることから、防音、防振、温度管理の強化を実現する素材への需要がさらに高まると予想されます。その結果、加硫ソリッドゴムは先進的な自動車設計に採用されることが増え、業界内の技術革新と部品統合の急増を支えています。こうした要求の進化により、サプライヤーはより持続可能で、性能志向で、用途に特化した次世代ゴム配合を提供することで適応を促し、市場の勢いをさらに加速させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 124億米ドル |

| 予測金額 | 237億米ドル |

| CAGR | 6.7% |

製品タイプ別では、スチレンブタジエンゴム(SBR)が引き続き世界市場を独占しています。この分野は2024年に29億米ドルの収益を上げ、2034年には56億米ドルに成長すると予測され、この期間のCAGRは6.9%です。SBRの人気は、特に高摩擦・摩耗の激しい用途において、そのコスト効率と卓越した機械的性能によって牽引されています。耐摩耗性と経時安定性により、ガスケット、シール、ベルト、工業用パッドなどの部品に非常に適しています。さらに、この素材は天然ゴムとよくなじむため、自動車、履物、建築などさまざまな産業への適応性が向上します。この相溶性は物理的特性を高めるだけでなく、使用事例の幅を広げ、市場での優位性を強めています。

用途別に分類すると、2024年の世界の加硫ソリッドゴム市場では自動車・運輸部門が43.7%の収益貢献で最大のシェアを占めています。同部門のリーダーシップは、耐熱性、耐油性、応力耐久性が要求される自動車部品に加硫ゴム部品が幅広く使用されていることに支えられています。これらの特性により、加硫ゴムはエンジンマウント、アンダーボディシールド、フロアライナー、騒音防止システムなどに適しています。電気自動車が勢いを増すなか、騒音・振動・ハーシュネス(NVH)低減システムなど、非構造的でありながら重要な部品におけるゴムへの依存は、業界でますます顕著になっています。EVの静かな車内や断熱に対するニーズは、ゴム配合の技術革新に拍車をかけ、新たなモビリティ・プラットフォーム全体にその関連性を広げています。

地域別では、中国が主要な貢献国に浮上し、2024年には23億米ドルの売上を上げ、2034年にはCAGR 6.9%の成長率で45億米ドルに達すると予想されます。同国の強力な地位は、その膨大な生産能力と、イノベーション主導の製造業への継続的なシフトによって支えられています。原材料費の高騰にもかかわらず、国内メーカーは世界市場の期待に応える高性能ゴムコンパウンドを開発する努力を強めています。自立と技術進歩を重視する中国は、付加価値の高いゴム製品の採用を促進し、国際舞台での競争力を高めています。さらに、国内消費は着実に増加し続けており、内需を支え、長期的な成長機会をもたらしています。

世界の加硫ソリッドゴム業界は依然として高度に統合されており、主要企業5社が市場全体の40%以上のシェアを占めています。これらの企業は、垂直統合、包括的な製品提供、広範な製造ネットワークを通じて競争力を維持しています。大手企業は、バイオベースで揮発性有機化合物(VOC)が少なく、厳しい条件下でも長いライフサイクルに耐えられる高度なゴムコンパウンドを開発するため、研究開発に多額の投資を行っています。戦略的買収も市場形成に重要な役割を果たしており、大手企業はニッチコンパウンドメーカーの買収や地域メーカーとの合弁事業を通じて、その勢力を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品タイプ別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021~2034年

- 主要動向

- 天然ゴム(NR)製品

- スチレンブタジエンゴム(SBR)製品

- ブタジエンゴム(BR)製品

- エチレンプロピレンジエンモノマー(EPDM)製品

- ニトリルゴム(NBR)製品

- クロロプレンゴム(CR)製品

- シリコーンゴム製品

- その他の特殊ゴム製品

第6章 市場推計・予測:硬度別、2021~2034年

- 主要動向

- 軟質(ショアA 30-50)

- 中質(ショアA 50-70)

- 硬質(ショアA 70-90)

- 超硬質(ショアA 90以上)

第7章 市場推計・予測:製造工程別、2021~2034年

- 主要動向

- 圧縮成形

- トランスファー成形

- 射出成形

- 押し出し

- カレンダー加工

- その他

第8章 市場推計・予測:用途別、2021~2034年

- 主要動向

- 自動車・輸送

- タイヤとタイヤ部品

- シールとガスケット

- 振動アイソレータとマウント

- ホースとベルト

- その他の自動車部品

- 産業機械および装置

- 工業用シールとガスケット

- コンベアベルトとコンポーネント

- ローラーとホイール

- 振動絶縁システム

- その他の産業用途

- 建設・インフラ

- 橋梁支承と伸縮継手

- 免震システム

- 防水・シーリング製品

- 床材・舗装材

- その他の建設用途

- 電気・電子工学

- 絶縁材およびケーブル部品

- コネクタとシール

- その他の電気用途

- ヘルスケアおよび医療機器

- 医療用チューブおよび部品

- ストッパーとシール

- その他の医療用途

- 消費財

- 履物部品

- スポーツ用品

- 家庭用品

- その他の消費者向け用途

- その他

第9章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- Arlanxeo

- Bridgestone Corporation

- Continental AG

- Dow Inc.

- ExxonMobil Corporation

- Freudenberg Group

- Gates Corporation

- Goodyear Tire &Rubber Company

- JSR Corporation

- Kumho Petrochemical

- LANXESS AG

- Michelin

- Momentive Performance Materials Inc.

- NOK Corporation

- Parker Hannifin Corporation

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Rubber Industries, Ltd.

- Trelleborg AB

- Wacker Chemie AG

- Zeon Corporation

The Global Vulcanised Solid Rubber Market was valued at USD 12.4 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 23.7 billion by 2034. This upward trend is largely fueled by rising consumption across the automotive and construction industries, particularly in well-established regions like Europe and rapidly advancing economies such as China. Vulcanised solid rubber continues to gain traction due to its impressive resistance to weathering, high durability, and elasticity, making it an essential material in a wide variety of industrial applications. Industries across the globe increasingly rely on it for its performance in sealing, vibration dampening, protective padding, and durable flooring systems. Its robust performance under high mechanical stress and exposure to various environmental factors ensures consistent demand across both mature and emerging industrial markets.

The material's ability to withstand temperature fluctuations and provide reliable insulation positions it as a preferred choice in manufacturing environments that require longevity and resilience. As infrastructure spending rebounds globally, especially across Southeast Asia and parts of the Middle East, more projects are turning to industrial-grade rubber solutions for long-term efficiency. Meanwhile, the ongoing transformation of the automotive sector-particularly the shift toward electric and hybrid mobility-is expected to further strengthen demand for materials that deliver noise insulation, vibration control, and enhanced thermal management. As a result, vulcanized solid rubber is increasingly being adopted in advanced vehicle designs, supporting a surge in innovation and component integration within the industry. These evolving requirements are prompting suppliers to adapt by offering next-generation rubber formulations that are more sustainable, performance-oriented, and application-specific, further driving the market's momentum.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.4 Billion |

| Forecast Value | $23.7 Billion |

| CAGR | 6.7% |

In terms of product types, styrene-butadiene rubber (SBR) continues to dominate the global market landscape. This segment generated a revenue of USD 2.9 billion in 2024 and is forecasted to grow to USD 5.6 billion by 2034, registering a CAGR of 6.9% over the period. SBR's popularity is driven by its cost-efficiency and exceptional mechanical performance, especially in high-friction and wear-intensive applications. Its abrasion resistance and aging stability make it highly suitable for use in components such as gaskets, seals, belts, and industrial pads. Additionally, the material blends well with natural rubber, improving its adaptability across different industries like automotive, footwear, and construction. This compatibility not only enhances its physical properties but also broadens its range of use cases, reinforcing its dominance in the market.

When segmented by application, the automotive and transportation sector accounted for the largest share of the global vulcanized solid rubber market in 2024, with a revenue contribution of 43.7%. The sector's leadership is underpinned by the broad use of vulcanized rubber parts in vehicle components that demand heat resistance, oil tolerance, and stress durability. These characteristics make the material well-suited for use in engine mounts, underbody shields, floor liners, and noise-control systems. With electric vehicles gaining momentum, the industry's reliance on rubber for non-structural yet critical components such as noise, vibration, and harshness (NVH) reduction systems is becoming more pronounced. The need for quieter cabins and thermal insulation in EVs is fueling innovation in rubber formulations and expanding their relevance across new mobility platforms.

Regionally, China emerged as a leading contributor, generating USD 2.3 billion in revenue in 2024 and is expected to reach USD 4.5 billion by 2034, growing at a CAGR of 6.9%. The country's strong position is supported by its massive production capacity and ongoing shift towards innovation-led manufacturing. Despite rising raw material costs, local producers are ramping up efforts to develop high-performance rubber compounds that meet the quality expectations of global markets. China's emphasis on self-reliance and technological advancement is fostering greater adoption of value-added rubber products, enhancing its competitiveness on the international stage. Additionally, domestic consumption continues to rise steadily, supporting internal demand and driving long-term growth opportunities.

The global vulcanized solid rubber industry remains highly consolidated, with the top five market players accounting for over 40% of the total share. These companies maintain a competitive edge through vertical integration, comprehensive product offerings, and expansive manufacturing networks. Leading players are investing heavily in research and development to engineer advanced rubber compounds that are bio-based, low in volatile organic compounds (VOCs), and capable of withstanding longer life cycles under demanding conditions. Strategic acquisitions are also playing a significant role in shaping the market, with major companies expanding their footprint through targeted takeovers of niche compounders and joint ventures with regional producers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only )

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.7 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Natural rubber (NR) products

- 5.3 Styrene-butadiene rubber (SBR) products

- 5.4 Butadiene rubber (BR) products

- 5.5 Ethylene propylene diene monomer (EPDM) products

- 5.6 Nitrile rubber (NBR) products

- 5.7 Chloroprene rubber (CR) products

- 5.8 Silicone rubber products

- 5.9 Other specialty rubber products

Chapter 6 Market Estimates and Forecast, By Hardness Grade, 2021 - 2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Soft (shore a 30-50)

- 6.3 Medium (shore a 50-70)

- 6.4 Hard (shore a 70-90)

- 6.5 Extra hard (shore a 90+)

Chapter 7 Market Estimates and Forecast, By Manufacturing Process, 2021 - 2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Compression molding

- 7.3 Transfer molding

- 7.4 Injection molding

- 7.5 Extrusion

- 7.6 Calendering

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 Automotive & transportation

- 8.2.1 Tires & tire components

- 8.2.2 Seals & gaskets

- 8.2.3 Vibration isolators & mounts

- 8.2.4 Hoses & belts

- 8.2.5 Other automotive components

- 8.3 Industrial machinery & equipment

- 8.3.1 Industrial seals & gaskets

- 8.3.2 Conveyor belts & components

- 8.3.3 Rollers & wheels

- 8.3.4 Vibration isolation systems

- 8.3.5 Other industrial applications

- 8.4 Construction & infrastructure

- 8.4.1 Bridge bearings & expansion joints

- 8.4.2 Seismic isolation systems

- 8.4.3 Waterproofing & sealing products

- 8.4.4 Flooring & paving materials

- 8.4.5 Other construction applications

- 8.5 Electrical & electronics

- 8.5.1 Insulation & cable components

- 8.5.2 Connectors & seals

- 8.5.3 Other electrical applications

- 8.6 Healthcare & medical devices

- 8.6.1 Medical tubing & components

- 8.6.2 Stoppers & seals

- 8.6.3 Other medical applications

- 8.7 Consumer goods

- 8.7.1 Footwear components

- 8.7.2 Sporting goods

- 8.7.3 Household products

- 8.7.4 Other consumer applications

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arlanxeo

- 10.2 Bridgestone Corporation

- 10.3 Continental AG

- 10.4 Dow Inc.

- 10.5 ExxonMobil Corporation

- 10.6 Freudenberg Group

- 10.7 Gates Corporation

- 10.8 Goodyear Tire & Rubber Company

- 10.9 JSR Corporation

- 10.10 Kumho Petrochemical

- 10.11 LANXESS AG

- 10.12 Michelin

- 10.13 Momentive Performance Materials Inc.

- 10.14 NOK Corporation

- 10.15 Parker Hannifin Corporation

- 10.16 Shin-Etsu Chemical Co., Ltd.

- 10.17 Sumitomo Rubber Industries, Ltd.

- 10.18 Trelleborg AB

- 10.19 Wacker Chemie AG

- 10.20 Zeon Corporation