|

市場調査レポート

商品コード

1773412

コールドミックスアスファルト市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Cold Mix Asphalt Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| コールドミックスアスファルト市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月26日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

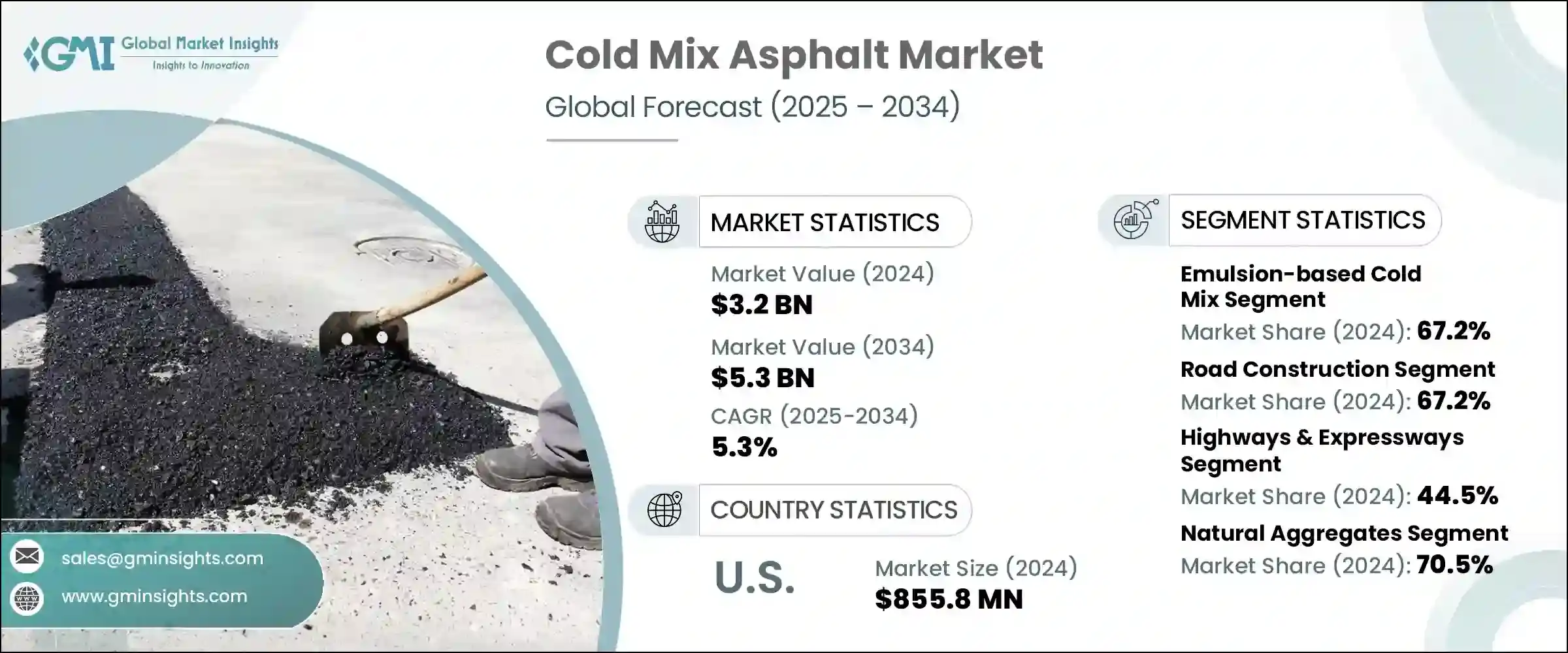

コールドミックスアスファルトの世界市場規模は、2024年に32億米ドルとなり、CAGR 5.3%で成長し、2034年には53億米ドルに達すると予測されています。

この成長の原動力となっているのは、継続的なインフラ投資、低排出建設資材の需要増加、世界の道路維持・復旧プロジェクトに対する注目の高まりです。コールドミックスアスファルトは、使いやすさ、最小限の設備要件、事実上どのような気象条件でも適用できる能力により、従来のホットミックスに代わるものとして着実に支持を集めています。開発途上地域および先進地域の政府は、特にホットミックス工場へのアクセスが制限されている、あるいは存在しない地域において、道路の接続および保全プログラムを推進しています。その結果、コールドミックスの代替は、地方の道路開発やスポット補修プロジェクトに不可欠なものとなりつつあります。

このアスファルトタイプは、温室効果ガス排出量の削減にも貢献するため、持続可能なインフラ整備を好む規制状況において、魅力的な選択肢となっています。一時的な補修、ユーティリティ・カットの復旧、および交通量の少ない道路の維持管理におけるその使用は、コストに敏感で、ロジスティクス的に困難なシナリオにおいて、不可欠なものとなっています。さらに、国の政策支援と配合技術の進歩により、その信頼性、保存性、最新の舗装基準への準拠が向上しています。コールドミックスアスファルトは、人件費やエネルギーコストを削減するだけでなく、長期保存も可能であるため、分散型建設や緊急補修に最適なソリューションとなっています。このような利便性と性能効率の高さにより、コールドミックスは公共事業部門や民間請負業者から支持され続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 32億米ドル |

| 予測金額 | 53億米ドル |

| CAGR | 5.3% |

製品セグメント別では、エマルジョンベースのコールドミックスが2024年の市場全体の67.2%を占め、市場を独占しています。この優位性は、製造時のエネルギー消費量が少なく、塗布時の取り扱いがより安全であることから、世界の安全性と持続可能性の目標に合致していることに起因しています。エマルジョンベースの混合物は、さまざまな骨材との適合性が高く、パッチワークや一般的な路面維持に適しているため、広く使用されています。この製剤の採用が増加している背景には、湿った状態でも塗布できることがあり、さまざまな気候や環境での実用性がさらに高まっています。

道路建設分野は2024年に67.2%の市場シェアを占め、最大の用途分野となりました。特に半都市部や農村部における道路開発プロジェクトでは、効率的で費用対効果の高いソリューションが重視されるようになっており、引き続きコールドミックスアスファルトの需要を押し上げています。この材料は、輸送が容易で現場での加熱が不要といった物流上の利点があるため、アクセス道路や脇道、交通量の少ない通路の建設に最適です。また、最小限の資源で迅速な展開が可能なため、インフラ拡張プロジェクトにおける初期表面治療や舗装に適した材料となっています。

最終用途産業の観点から見ると、2024年の市場シェアの44.5%は高速道路と高速道路が占めています。国道や地方道への投資が活発化する中、交通の混乱を最小限に抑えつつ、頻繁な車両荷重に耐えることができる、硬化が早く耐候性に優れた材料へのニーズが高まっています。コールドミックスアスファルトは、特に連続補修、路肩補強、路面安定化が必要な地域で、この要件を十分に満たします。迅速な展開が可能なため、ダウンタイムを最小限に抑えることができ、交通量の多い路線や交通量の多い高速道路では非常に重要です。

2024年のコールドミックスアスファルト世界市場は米国が8億5,580万米ドルの評価額でリードしました。インフラの近代化に重点を置いた連邦政府の資金援助と、環境に配慮した材料への幅広いシフトが、市場の成長を支える極めて重要な役割を果たしています。特に、緊急補修や季節的な補修、天候の変動が激しい地域での長期的な路面治療に適しており、その汎用性の高さから、州や自治体の道路保全活動におけるコールドミックスの採用が増加しています。

競合情勢を形成している主要企業には、オールステーツ・マテリアル・グループ、マーティン・マリエッタ・マテリアルズ、レイクサイド・インダストリーズ、UNIQUE Paving Materials、カーギルなどがあります。これらの企業は、地域の専門知識と高度な研究開発能力を活用し、多様な地域のニーズに合わせた高性能製品を提供しています。信頼性、耐久性、環境効率に重点を置き、持続可能な道路建設の進化する要求をサポートするために、提供する製品を改良し続けています。また、ポリマー改質コールドパッチ・ソリューションと顧客中心のサポート・システムを重視するブランドも、現代のインフラの優先事項に沿った、すぐに使えるオールシーズン舗装ソリューションに対する消費者の嗜好の高まりに後押しされ、その勢力を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- インフラ開発の拡大

- 費用対効果とエネルギー効率

- 環境持続可能性への重点

- 塗布と保管の容易さ

- 業界の潜在的リスク&課題

- 品質の一貫性の問題

- 発展途上地域での認識の低さ

- ホットミックスアスファルトとの競合

- 標準化の課題

- 市場機会

- 新興市場のインフラ成長

- 技術的進歩

- 持続可能な建設の動向

- 遠隔地アプリケーション

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- エマルジョンベースのコールドミックス

- カチオンエマルジョンコールドミックス

- アニオン性エマルジョンコールドミックス

- 非イオン性エマルジョンコールドミックス

- アスファルトの削減

- 急速硬化(RC)カットバック

- 中速硬化(MC)カットバック

- 低速硬化(SC)カットバック

- 発泡アスファルト

- コールドリサイクルミックス

- コールドリサイクル

- 中央プラントのコールドリサイクル

- その他のタイプ

- ポリマー改質コールドミックス

- 繊維強化コールドミックス

- 添加剤強化コールドミックス

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 道路建設

- 新しい道路建設

- 道路拡幅

- 仮設道路

- 道路の保守と修理

- 道路の穴の補修

- クラックシーリング

- 表面処理

- 緊急修理

- 舗装の改修

- 全深度埋め立て

- コールドインプレースリサイクル

- 路盤安定化

- その他の用途

- 路肩工事

- 公共事業の復旧を削減

- 自転車道と歩道

第7章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 高速道路

- 州間高速道路

- 州道

- 高速道路

- 市道

- 都市道路

- 郊外の道路

- 田舎道

- 空港

- 滑走路

- 誘導路

- エプロン

- 駐車場

- 商業用駐車場

- 住宅駐車場

- 工業用駐車場

- その他

- 港湾

- 工業地域

- レクリエーションエリア

第8章 市場推計・予測:骨材タイプ別、2021年~2034年

- 主要動向

- 天然骨材

- 砕石

- 砂利

- 砂

- リサイクル骨材

- 再生アスファルト舗装(RAP)

- リサイクルコンクリート骨材(RCA)

- その他のリサイクル材料

- 合成骨材

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- ExxonMobil Corporation

- BASF

- Total Energies SE

- All States Materials Group.

- Martin Marietta Materials

- Asphalt Materials

- UNIQUE Paving Materials

- Arkema Group

- Kao Corporation

- Ingevity Corporation

- Colas SA

- Aggregate Industries

- Cargill

- HEI-Way Premium Asphalt

- Simon Team

- Heidelberg Materials AG

- Reeves Construction Company

- Tarmac(CRH Company)

- Lakeside Industries

The Global Cold Mix Asphalt Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 5.3 billion by 2034. This growth is being driven by ongoing infrastructure investments, a rising demand for low-emission construction materials, and increasing attention toward road maintenance and rehabilitation projects worldwide. Cold mix asphalt is steadily gaining traction as an alternative to traditional hot mix due to its ease of use, minimal equipment requirements, and ability to be applied in virtually any weather condition. Governments across developing and developed regions are pushing for road connectivity and preservation programs, especially in areas where access to hot mix plants is limited or non-existent. As a result, the cold mix alternative is becoming integral to rural road development and spot repair projects.

This asphalt type also contributes to lower greenhouse gas emissions, making it an attractive option in a regulatory landscape that favors sustainable infrastructure practices. Its use in temporary repairs, utility cut reinstatements, and maintenance of low-traffic roads has made it indispensable in cost-sensitive and logistically challenged scenarios. Furthermore, national policy support and technological advancements in formulation have enhanced its reliability, shelf life, and adherence to modern paving standards. Cold mix asphalt not only reduces labor and energy costs but also enables longer storage, making it a go-to solution for decentralized construction and emergency repairs. This convenience, coupled with its performance efficiency, ensures that cold mix continues to gain preference among public works departments and private contractors alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 5.3% |

In terms of product segmentation, emulsion-based cold mix dominated the market in 2024, accounting for 67.2% of the total revenue share. This dominance stems from its lower energy consumption during production and safer handling during application, which aligns well with global safety and sustainability goals. Emulsion-based mixes are widely used due to their compatibility with various aggregates and suitability for patchwork and general road surface maintenance. The rising adoption of this formulation is also supported by its ability to be applied in damp conditions, further enhancing its practicality in a range of climates and environments.

The road construction segment represented the largest application area in 2024, holding a market share of 67.2%. The increasing emphasis on efficient, cost-effective solutions for road development projects, particularly in semi-urban and rural regions, continues to boost demand for cold mix asphalt. This material offers logistical advantages, such as easier transport and no need for onsite heating, making it ideal for building access roads, byways, and low-volume traffic corridors. Its capacity to be deployed quickly with minimal resources has also made it a preferred material for initial surface treatments and paving in infrastructure expansion projects.

From an end-use industry perspective, highways and expressways contributed to 44.5% of the market share in 2024. As investments in national and regional roadways intensify, there is a growing need for quick-setting and weather-resistant materials that can withstand frequent vehicle loads while minimizing traffic disruptions. Cold mix asphalt fulfills this requirement well, particularly in areas where continuous repairs, shoulder reinforcement, and surface stabilization are needed. Its rapid deployability ensures minimal downtime, which is critical for busy routes and high-traffic expressways.

The United States led the global cold mix asphalt market in 2024, with a valuation of USD 855.8 million. Federal funding focused on infrastructure modernization, along with a broader shift toward environmentally conscious materials, has played a pivotal role in supporting market growth. The adoption of cold mix in road preservation efforts across state and municipal agencies is increasing, particularly due to its versatility and suitability for emergency repairs, seasonal patching, and long-term surface treatments in areas with extreme weather fluctuations.

Key players shaping the competitive landscape include All States Materials Group, Martin Marietta Materials, Lakeside Industries, UNIQUE Paving Materials, and Cargill. These companies leverage regional expertise and advanced R&D capabilities to offer high-performance products tailored to diverse geographic needs. With a strong focus on reliability, durability, and eco-efficiency, they continue to refine their offerings to support the evolving demands of sustainable road construction. Brands that emphasize polymer-modified cold patch solutions and customer-centric support systems are also expanding their footprint, driven by increasing consumer preference for ready-to-use, all-season pavement solutions that align with modern infrastructure priorities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.2.5 Manufacturing process

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing infrastructure development

- 3.2.1.2 Cost-effectiveness & energy efficiency

- 3.2.1.3 Environmental sustainability focus

- 3.2.1.4 Ease of application & storage

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Quality consistency issues

- 3.2.2.2 Limited awareness in developing regions

- 3.2.2.3 Competition from hot mix asphalt

- 3.2.2.4 Standardization challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging markets infrastructure growth

- 3.2.3.2 Technological advancements

- 3.2.3.3 Sustainable construction trends

- 3.2.3.4 Remote area applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Emulsion-based cold mix

- 5.2.1 Cationic emulsion cold mix

- 5.2.2 Anionic emulsion cold mix

- 5.2.3 Non-ionic emulsion cold mix

- 5.3 Cutback asphalt

- 5.3.1 Rapid curing (RC) cutback

- 5.3.2 Medium curing (mc) cutback

- 5.3.3 Slow curing (SC) cutback

- 5.4 Foamed asphalt

- 5.5 Cold recycled mix

- 5.5.1 Place cold recycling

- 5.5.2 Central plant cold recycling

- 5.6 Other types

- 5.6.1 Polymer modified cold mix

- 5.6.2 Fiber reinforced cold mix

- 5.6.3 Additive enhanced cold mix

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Road construction

- 6.2.1 New road construction

- 6.2.2 Road widening

- 6.2.3 Temporary roads

- 6.3 Road maintenance & repair

- 6.3.1 Pothole patching

- 6.3.2 Crack sealing

- 6.3.3 Surface treatment

- 6.3.4 Emergency repairs

- 6.4 Pavement rehabilitation

- 6.4.1 Full depth reclamation

- 6.4.2 Cold in-place recycling

- 6.4.3 Base course stabilization

- 6.5 Other applications

- 6.5.1 Shoulder construction

- 6.5.2 Utility cuts restoration

- 6.5.3 Bike paths & walkways

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Highways & expressways

- 7.2.1 Interstate highways

- 7.2.2 State highways

- 7.2.3 Expressways

- 7.3 Municipal roads

- 7.3.1 Urban roads

- 7.3.2 Suburban roads

- 7.3.3 Rural roads

- 7.4 Airports

- 7.4.1 Runways

- 7.4.2 Taxiways

- 7.4.3 Aprons

- 7.5 Parking areas

- 7.5.1 Commercial parking lots

- 7.5.2 Residential parking

- 7.5.3 Industrial parking

- 7.6 Others

- 7.6.1 Ports & harbors

- 7.6.2 Industrial areas

- 7.6.3 Recreational areas

Chapter 8 Market Estimates and Forecast, By Aggregate Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Natural aggregates

- 8.2.1 Crushed stone

- 8.2.2 Gravel

- 8.2.3 Sand

- 8.3 Recycled aggregates

- 8.3.1 Reclaimed asphalt pavement (RAP)

- 8.3.2 Recycled concrete aggregate (RCA)

- 8.3.3 Other recycled materials

- 8.4 Synthetic aggregates

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 ExxonMobil Corporation

- 10.2 BASF

- 10.3 Total Energies SE

- 10.4 All States Materials Group.

- 10.5 Martin Marietta Materials

- 10.6 Asphalt Materials

- 10.7 UNIQUE Paving Materials

- 10.8 Arkema Group

- 10.9 Kao Corporation

- 10.10 Ingevity Corporation

- 10.11 Colas SA

- 10.12 Aggregate Industries

- 10.13 Cargill

- 10.14 HEI-Way Premium Asphalt

- 10.15 Simon Team

- 10.16 Heidelberg Materials AG

- 10.17 Reeves Construction Company

- 10.18 Tarmac (CRH Company)

- 10.19 Lakeside Industries