|

市場調査レポート

商品コード

1773400

先進自動車用照明市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Advanced Vehicle Lighting Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 先進自動車用照明市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月17日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

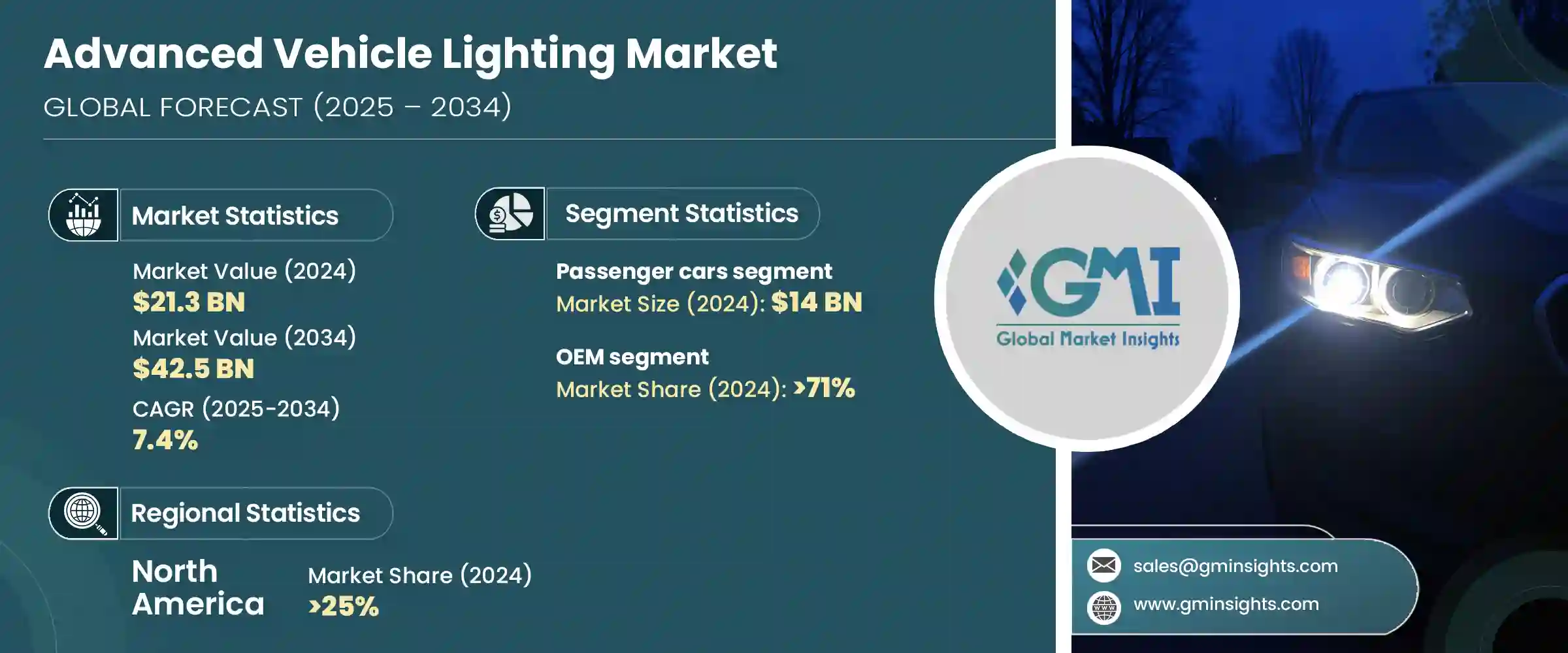

先進自動車用照明の世界市場規模は、2024年に213億米ドルとなり、CAGR 7.4%で成長し、2034年には425億米ドルに達すると推定されています。

この成長は、ADAS(先進運転支援システム)と自律走行技術の統合が進み、最新の自動車の照明要件が変化していることが主な要因です。マトリックスLEDやレーザーヘッドランプのようなインテリジェント照明ソリューションは、センサー機能をサポートし、グレアを低減するためにリアルタイムでビームパターンを調整できるため、ますます需要が高まっています。

自動車メーカーは、特に視界が限られた状況で歩行者や他の車両と通信できる動的照明システムに多額の投資を行っています。自動車分野での競争が激化する中、メーカーは複雑な照明デザインをブランドの特徴として活用しています。特に電気自動車や高級車では、ダイナミックターンシグナル、3Dテールライト、室内アンビエント照明などの機能が、今や不可欠なスタイリング要素となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 213億米ドル |

| 予測金額 | 425億米ドル |

| CAGR | 7.4% |

フレキシブルLEDとOLED技術により、自動車メーカーは高度にカスタマイズ可能でアニメーション化された照明効果を作り出すことができ、自動車のアイデンティティと視覚的魅力を大幅に高めることができます。このような適応性の高い照明ソリューションは、車両のさまざまな部分に形を変えて組み込むことができるため、デザイナーは競争市場で各モデルを際立たせる独自のシグネチャーを自由に開発できます。順次点灯する方向指示器、歓迎のライトショー、ムードを高める室内照明など、ダイナミックなアニメーションをプログラムできる能力は、未来的で個性的な機能を求める消費者に強く響く洗練されたレイヤーを追加します。

2024年、乗用車部門の市場規模は140億米ドルに達します。デイタイム・ランニング・ライト(DRL)やアダプティブ・ドライビング・ビーム(ADB)システムの採用など、世界の規制強化により、相手先商標製品メーカー(OEM)は先進照明技術の統合を余儀なくされています。これらの機能は、昼夜を問わず視認性を向上させるだけでなく、国際的な安全基準への適合を確実にします。各国政府がより厳格な照明規制を実施する中、乗用車の主流はますますこのようなシステムを搭載するようになっており、先進自動車用照明の需要を押し上げています。さらに、プレミアムで没入感のあるインテリアに対する消費者の関心は、自動車メーカーが洗練された車内体験を作り出すために、マルチカラーLEDストリップ、シンクロナイズされたムード照明、カスタマイズ可能なライトテーマを取り付けることを後押ししています。

OEMセグメントは2024年に71%のシェアを占める。先進的な照明システムは、車両デザインを定義し、メーカーのブランドアイデンティティを強化する上で極めて重要になっています。特徴的なLED DRL、アニメーション化されたウェルカムライト、設定可能なテールライトのデザインは、イノベーションとラグジュアリーに焦点を当てたマーケティングキャンペーンをサポートしながら、自動車を即座に認識させることに貢献しています。混雑したマーケットプレースで際立つために、OEMは照明の研究開発に多大なリソースを割いており、消費者を魅了し、自社の製品を差別化する印象的で特徴的なデザインの創造を目指しています。

北米先進自動車用照明2024年のシェアは25%。米国高速道路交通安全局(NHTSA)は、アダプティブ・ドライビング・ビーム(ADB)ヘッドライトやその他のインテリジェント照明技術を許可する規制への支持を強めています。このような政策転換により、自動車メーカーは、路上走行時の安全性を高め、まぶしさを低減し、進化する連邦安全基準に適合する先進照明システムを採用するようになり、高品質照明ソリューションの市場機会が拡大しています。さらに、米国では電気自動車(EV)と自律走行車の急速な普及が、政府のインセンティブと消費者の強い関心に後押しされ、LEDマトリックス、LiDAR内蔵ヘッドランプ、通信に特化した照明機能など、次世代の自動車の安全性と性能に不可欠な洗練された照明技術に対する需要を促進しています。

先進自動車用照明世界市場の主要企業は、オスラム、ZKW、小糸製作所、ルミレッズ、フォービア、スタンレー、ヴァレオなどです。これらの企業は、技術革新と戦略的ポジショニングによって激しい競争を繰り広げ、世界市場シェアの大部分を占めています。先進自動車用照明分野の企業は、その存在感を確固たるものにし市場ポジションを強化するため、自律走行車や電気自動車の動向に合わせた適応型、スマート、コネクテッド照明システムの開発など、照明技術の継続的イノベーションに注力しています。研究開発に多額の投資を行い、機能性、エネルギー効率、デザインの特徴を強化した新製品を投入しています。自動車OEMとの戦略的パートナーシップや協力関係により、これらの企業は自社の照明ソリューションを車両プラットフォームにシームレスに統合し、早期採用と長期契約を確保しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 車両におけるアダプティブ照明の採用拡大

- 車両の電動化とEV生産率の上昇

- 道路と乗客の安全への重点化

- 効率的な照明システムに関する政府の義務

- 業界の潜在的リスク&課題

- 高度な照明部品の高コスト

- 車載電子機器とのシステム統合の複雑さ

- 市場機会

- 自動運転用スマート照明の開発

- EVおよび高級車セグメントの成長

- 新興自動車製造市場における拡大

- 照明と車両通信システムの統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- ハロゲン

- キセノン/HID

- LED

- レーザ

- 有機EL

- マトリックスLED

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- フロントライティング

- リアライト

- 室内照明

- サイド&コーナー照明

- フォグランプと補助灯

- コミュニケーション照明

第7章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- ライトデューティ

- ミディアムデューティ

- ヘビーデューティ

第8章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:推進別、2021年~2034年

- 主要動向

- ICE

- 電気自動車

- ハイブリッド車

- PHEV

- 燃料電池自動車

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 東南アジア

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Koito Manufacturing Co., Ltd.

- Valeo S.A.

- Hella GmbH &Co. KGaA(FORVIA Group)

- Marelli Automotive Lighting

- Stanley Electric Co., Ltd.

- ZKW Group GmbH

- OSRAM Continental GmbH

- Hyundai Mobis Co., Ltd.

- Lumileds Holding B.V.

- Nichia Corporation

- Bosch Mobility Solutions

- TYC Brother Industrial Co., Ltd.

- Texas Instruments

- Denso Corporation

- GE Lighting(Savant Systems Inc.)

- Varroc Engineering Ltd.

- Bosla Lighting

- SL Corporation

- Ichikoh Industries, Ltd.

- J.W. Speaker Corporation

The Global Advanced Vehicle Lighting Market was valued at USD 21.3 billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 42.5 billion by 2034. This growth is driven largely by the rising integration of advanced driver assistance systems (ADAS) and autonomous driving technologies, which are transforming the lighting requirements of modern vehicles. Intelligent lighting solutions, such as matrix LED and laser headlamps, are increasingly in demand because they can adjust beam patterns in real-time to support sensor functions and reduce glare.

Automakers are heavily investing in dynamic lighting systems that can communicate with pedestrians and other vehicles, especially in conditions with limited visibility. As competition intensifies in the automotive sector, manufacturers are leveraging complex lighting designs as a distinctive brand signature. Features like dynamic turn signals, 3D taillights, and interior ambient lighting are now essential styling elements, particularly in electric and luxury vehicles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.3 Billion |

| Forecast Value | $42.5 Billion |

| CAGR | 7.4% |

Flexible LED and OLED technologies allow automakers to create highly customizable and animated lighting effects that significantly boost a vehicle's identity and visual appeal. These adaptable lighting solutions can be shaped and integrated into various parts of the vehicle, offering designers the freedom to develop unique signatures that set each model apart in a competitive market. The ability to program dynamic animations-such as sequential turn signals, welcoming light shows, or mood-enhancing interior lighting-adds a layer of sophistication that resonates strongly with consumers seeking futuristic and personalized features.

In 2024, the passenger cars segment held USD 14 billion. Regulatory mandates worldwide, such as the adoption of daytime running lights (DRLs) and adaptive driving beam (ADB) systems, are compelling original equipment manufacturers (OEMs) to integrate advanced lighting technologies. These features not only improve visibility during both day and night but also ensure compliance with international safety standards. As governments enforce stricter lighting regulations, mainstream passenger cars are increasingly outfitted with such systems, pushing demand for advanced vehicle lighting higher. Furthermore, consumer interest in premium, immersive interiors is driving automakers to install multi-color LED strips, synchronized mood lighting, and customizable light themes to create a sophisticated in-car experience.

The OEM segment held a 71% share in 2024. Advanced lighting systems have become crucial in defining vehicle design and reinforcing brand identity for manufacturers. Signature LED DRLs, animated welcome lights, and configurable taillight designs contribute to making vehicles instantly recognizable while supporting marketing campaigns focused on innovation and luxury. To stand out in a crowded marketplace, OEMs are dedicating significant resources to lighting research and development, aiming to create striking, distinctive designs that attract consumers and differentiate their offerings.

North America Advanced Vehicle Lighting Market held a 25% share in 2024. The U.S. National Highway Traffic Safety Administration (NHTSA) is increasingly supporting regulations that permit adaptive driving beam (ADB) headlights and other intelligent lighting technologies. These policy shifts encourage automakers to adopt advanced lighting systems that enhance on-road safety, reduce glare, and comply with evolving federal safety standards, generating greater market opportunities for high-quality lighting solutions. Additionally, the rapid growth of electric vehicles (EVs) and autonomous cars in the U.S., spurred by government incentives and strong consumer interest, fuels demand for sophisticated lighting technologies such as LED matrices, LiDAR-integrated headlamps, and communication-focused lighting features that are critical for next-generation vehicle safety and performance.

Leading players in the Global Advanced Vehicle Lighting Market include OSRAM, ZKW, Koito, Lumileds, Forvia, STANLEY, and Valeo. Together, these companies hold a significant portion of the global market share, competing vigorously through innovation and strategic positioning. To solidify their presence and strengthen market positions, companies in the advanced vehicle lighting space are focusing on continuous innovation in lighting technologies, such as the development of adaptive, smart, and connected lighting systems that align with autonomous and electric vehicle trends. They are investing heavily in research and development to introduce new products that offer enhanced functionality, energy efficiency, and distinctive design features. Strategic partnerships and collaborations with automotive OEMs allow these companies to integrate their lighting solutions seamlessly into vehicle platforms, ensuring early adoption and long-term contracts.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicle

- 2.2.4 Propulsion

- 2.2.5 Sales Channel

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of adaptive lighting in vehicles

- 3.2.1.2 Rising vehicle electrification and EV production rates

- 3.2.1.3 Increasing emphasis on road and passenger safety

- 3.2.1.4 Government mandates for efficient lighting systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced lighting components

- 3.2.2.2 Complexity in system integration with vehicle electronics

- 3.2.3 Market opportunities

- 3.2.3.1 Development of smart lighting for autonomous driving

- 3.2.3.2 Growth in EV and luxury vehicle segments

- 3.2.3.3 Expansion in emerging automotive manufacturing markets

- 3.2.3.4 Integration of lighting with vehicle communication systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn & Units)

- 5.1 Key trends

- 5.2 Halogen

- 5.3 Xenon/HID

- 5.4 LED

- 5.5 Laser

- 5.6 OLED

- 5.7 Matrix LED

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn & Units)

- 6.1 Key trends

- 6.2 Front Lighting

- 6.3 Rear Lighting

- 6.4 Interior Lighting

- 6.5 Side & Corner Lighting

- 6.6 Fog and Auxiliary Lights

- 6.7 Communication Lighting

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn & Units)

- 7.1 Key trends

- 7.2 Passenger Car

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial Vehicle

- 7.3.1 Light-duty

- 7.3.2 Medium-duty

- 7.3.3 Heavy-duty

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn & Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn & Units)

- 9.1 Key trends

- 9.2 ICE

- 9.3 BEV

- 9.4 HEV

- 9.5 PHEV

- 9.6 FCEV

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Koito Manufacturing Co., Ltd.

- 11.2 Valeo S.A.

- 11.3 Hella GmbH & Co. KGaA (FORVIA Group)

- 11.4 Marelli Automotive Lighting

- 11.5 Stanley Electric Co., Ltd.

- 11.6 ZKW Group GmbH

- 11.7 OSRAM Continental GmbH

- 11.8 Hyundai Mobis Co., Ltd.

- 11.9 Lumileds Holding B.V.

- 11.10 Nichia Corporation

- 11.11 Bosch Mobility Solutions

- 11.12 TYC Brother Industrial Co., Ltd.

- 11.13 Texas Instruments

- 11.14 Denso Corporation

- 11.15 GE Lighting (Savant Systems Inc.)

- 11.16 Varroc Engineering Ltd.

- 11.17 Bosla Lighting

- 11.18 SL Corporation

- 11.19 Ichikoh Industries, Ltd.

- 11.20 J.W. Speaker Corporation