再生アスファルト舗装市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Recycled Asphalt Pavement (RAP) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773394

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

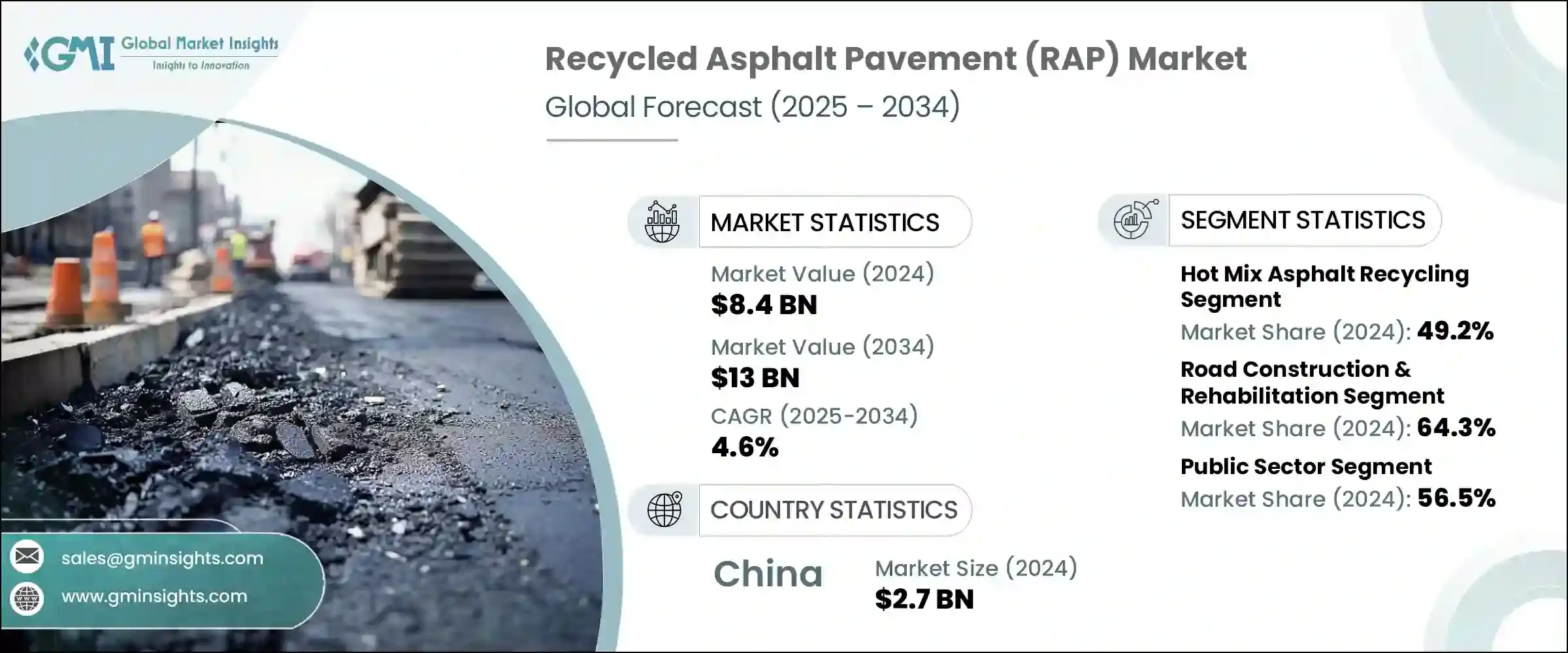

世界の再生アスファルト舗装市場は、2024年に84億米ドルと評価され、CAGR 4.6%で成長し、2034年には130億米ドルに達すると推定されています。

費用対効果が高く持続可能な建設資材への需要が高まるにつれ、RAP産業は様々なインフラ分野で大きな牽引力を獲得しています。政府や請負業者は、バージン原料への依存を減らし、プロジェクトコストを下げ、環境への影響を最小限に抑えるために、アスファルトリサイクルをますます受け入れています。この動向は、埋立廃棄物の削減、エネルギー効率の改善、既存の道路材料の再利用による温室効果ガス排出の抑制に、ますます焦点が当てられていることが背景にあります。規制機関は、持続可能な道路建設慣行による環境保全を引き続き重視しており、これは世界のインフラ部門におけるRAPの地位をさらに強固なものにしています。

より持続可能な道路復旧ソリューションの追求において、RAPは経済的にも生態学的にもかなりの利点を示しています。再生アスファルトは、性能を損なうことなく舗装プロジェクトに組み込むことができ、従来のアスファルトに代わる耐久性を提供します。既存のバッチおよびドラムミックス技術との互換性は、それが大規模な道路建設のための実用的な選択肢となっています。近年では、インフラ・プロジェクトのライフサイクル排出量削減への注目が高まっていることも、RAPの人気上昇に寄与しています。再生材料を建設ワークフローに組み込むことで、請負業者は高い構造的完全性を維持しながら二酸化炭素排出量を削減することができます。さらに、移動式リサイクル機器を使って現場で処理できるなど、RAPの運用上の柔軟性が、その効率性と普及に拍車をかけています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 84億米ドル |

| 予測金額 | 130億米ドル |

| CAGR | 4.6% |

リサイクル手法の中で、ホットミックスアスファルト(HMA)リサイクルは、2024年の市場シェア全体の49.2%を占め、主要なプロセスとして浮上しています。HMAリサイクルは、材料コストと二酸化炭素排出量の両方を大幅に削減しながら、バージンアスファルトに近い性能を提供する能力によって際立っています。RAP含有率の高い混合物への適応性により、高速道路の再舗装や道路の改良に好まれる方法となっています。さらに、技術の進歩により、HMAリサイクル工程の一貫性と品質が改善され、構造的に要求の厳しい道路層での使用が可能になりました。

用途別では、道路建設と復旧が市場を独占し、2024年の総需要の64.3%を占めました。持続可能な都市開発と費用対効果の高い道路改良に対するニーズの高まりが、この分野でのRAP使用の急増につながっています。リサイクル材料は現在、幹線道路や地方道路に広く取り入れられており、自治体や民間業者が資源利用を最適化しながら環境目標を達成するのに役立っています。高い割合の再生材料を使用して舗装性能を維持できることから、RAPは公共および民間のインフラ・プロジェクトにおける重要な構成要素となっています。長期的な持続可能性目標との整合性を求める管轄区域が増えるにつれ、道路工事へのRAPの統合はより戦略的になっています。

エンドユーザー別に見ると、2024年のRAP市場では公共部門が56.5%を占め、最大のシェアを占めています。政府が支援するインフラ構想や持続可能性の義務化によって、RAPは公共事業の標準的な構成要素となっています。国や地域レベルの当局は、特に高速道路や地方自治体の再開発プロジェクトにおいて、入札仕様書にリサイクル材料の使用を求めるようになっています。公共機関はまた、環境認証や長期的性能に貢献する材料を優先的に使用するようになっており、それによって調達戦略におけるRAPの価値が強化されています。

地域別では中国が世界のRAP市場をリードし、2024年の評価額は27億米ドルに達しました。インフラ接続、都市再生、環境責任を重視する同国は、各省で再生アスファルトの大規模な採用を推進しています。リサイクル建設資材を支援する政策的枠組みは、近代的なリサイクル工場の成長と相まって、様々なプロジェクトにおけるRAPの展開を支え続けています。国道開拓にRAPを統合する中国の構造的アプローチは、この地域の圧倒的な市場シェアに大きく貢献しています。

再生アスファルト舗装業界の競合情勢は、主要なインフラ企業が持続可能性の証明書を強化するにつれて進化しています。市場のリーダーは、アスファルトのリサイクルを中核事業に組み込んでおり、サプライチェーン全体の品質管理を確実にするために垂直統合に焦点を当てています。骨材生産ユニットの所有から、アスファルト混合プラントや舗装サービスの運営に至るまで、これらの企業は、再生アスファルトを効率的に回収し、再利用するための合理化されたプロセスを確立しています。

多くは、専用施設を設置し、ドラムミキサーをアップグレードし、高RAP用途のために移動ユニットを利用することによって、リサイクル能力を拡大しています。技術的な統合も顕著になってきており、低炭素建設基準への準拠をサポートするために、正確なRAP投与、温度調節、排出監視のためのデジタルツールを導入しています。さらに、業界参加者は、再生アスファルトの使用に関する仕様を強化し、完全深度でのリサイクル技術を最適化することを目的とした調査やパイロットプロジェクトにおいて、公的機関と協力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 道路補修とインフラ改修の需要増加

- バージンアスファルトに比べて材料費と生産コストが低い

- リサイクル材料を促進する厳しい環境規制

- 業界の潜在的リスク&課題

- 特殊なリサイクル設備とプラントの改造にかかる初期投資費用

- 再生アスファルト材の品質と性能の一貫性がない

- 市場機会

- RAP統合を促進する政府資金による持続可能なインフラプログラムの拡大

- 道路建設におけるコールドインプレイス工法およびフルデプス埋立工法の採用増加

- 高性能RAP混合物の品質を向上させる性能向上添加剤の開発

- 商業プロジェクトにおけるグリーン建設資材への民間部門の関心の高まり

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:リサイクルプロセス別、2021年~2034年

- 主要動向

- ホットミックスアスファルトリサイクル

- バッチプラント

- ドラムプラント

- コールドミックスアスファルトリサイクル

- インプレースコールドリサイクル

- 中央プラントのコールドリサイクル

- インプレースリサイクル

- コールドインプレースリサイクル(CIR)

- 全深度埋め立て(FDR)

- ホットインプレースリサイクル(HIR)

- 中央プラントのリサイクル

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 道路建設と改修

- 高速道路と高速道路

- 都市の道路や街路

- 田舎道

- 駐車場と歩道

- 空港の滑走路と誘導路

- 歩道、自転車レーン、レクリエーション用地

- その他のインフラ(港湾、工業団地)

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 公共部門

- 運輸省(DOT)

- 市町村および地方自治体

- 空港および港湾当局

- 民間部門

- 建設・エンジニアリング会社

- 不動産開発業者

- 工業および商業の最終用途

- 請負業者と下請業者

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- Colas S.A.

- Eurovia(VINCI Group)

- Granite Construction Inc.

- Oldcastle Materials(CRH)

- LafargeHolcim Ltd.

- CEMEX S.A.B. de C.V.

- Vulcan Materials Company

- Road Science

- The Lane Construction Corporation

- GreenRap

- Downer Group(Reconophalt)

- Gencor Industries

- Phoenix Industries

- Atmos Technologies

目次

The Global Recycled Asphalt Pavement Market was valued at USD 8.4 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 13 billion by 2034. As demand for cost-effective and sustainable construction materials increases, the RAP industry is gaining significant traction across various infrastructure segments. Governments and contractors are increasingly embracing asphalt recycling to reduce dependence on virgin raw materials, lower project costs, and minimize environmental impact. The trend is driven by a growing focus on reducing landfill waste, improving energy efficiency, and limiting greenhouse gas emissions through the reuse of existing road materials. Regulatory bodies continue to emphasize environmental preservation through sustainable road construction practices, which has further solidified RAP's position in the global infrastructure sector.

In the pursuit of more sustainable road rehabilitation solutions, RAP presents considerable economic and ecological advantages. Recycled asphalt can be integrated into paving projects without compromising performance, offering a durable alternative to conventional asphalt. Its compatibility with existing batch and drum mix technologies makes it a practical choice for large-scale road construction. In recent years, the increased focus on reducing lifecycle emissions from infrastructure projects has also contributed to RAP's rising popularity. By incorporating reclaimed materials into construction workflows, contractors are able to lower their carbon footprints while maintaining high structural integrity. Moreover, the operational flexibility of RAP, such as its ability to be processed on-site using mobile recycling equipment, adds to its efficiency and widespread adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $13 Billion |

| CAGR | 4.6% |

Among recycling methods, hot mix asphalt (HMA) recycling has emerged as the leading process, accounting for 49.2% of the overall market share in 2024. HMA recycling stands out due to its ability to deliver near-virgin performance while significantly cutting down on both material costs and carbon emissions. Its adaptability to high-RAP-content mixes has made it the preferred method for highway resurfacing and road upgrades. Additionally, advances in technology have improved the consistency and quality of HMA recycling processes, making it feasible for use in structurally demanding road layers.

In terms of application, road construction and rehabilitation dominated the market, representing 64.3% of total demand in 2024. The increasing need for sustainable urban development and cost-effective roadway upgrades has led to a surge in RAP usage within this segment. Recycled materials are now widely incorporated into arterial and local roads, helping municipalities and private contractors meet environmental goals while optimizing resource use. The ability to maintain pavement performance using high percentages of recycled content has made RAP a key component in public and private infrastructure projects. Its integration into roadworks has become more strategic as more jurisdictions seek to align with long-term sustainability targets.

When segmented by end user, the public sector held the largest share of the RAP market in 2024, accounting for 56.5%. Government-backed infrastructure initiatives and sustainability mandates have made RAP a standard component in public works. Authorities at national and regional levels increasingly require the use of recycled materials in tender specifications, particularly for highways and municipal redevelopment projects. Public agencies are also prioritizing materials that contribute to environmental certifications and long-term performance, thereby reinforcing the value of RAP in procurement strategies.

Regionally, China led the global RAP market, with a valuation of USD 2.7 billion in 2024. The country's strong emphasis on infrastructure connectivity, urban renewal, and environmental responsibility has driven large-scale adoption of recycled asphalt across its provinces. Policy frameworks supporting recycled construction materials, coupled with the growth of modern recycling plants, continue to support RAP deployment in various projects. China's structured approach to integrating RAP in national highway development has contributed significantly to the region's dominant market share.

The competitive landscape of the recycled asphalt pavement industry is evolving as major infrastructure companies enhance their sustainability credentials. Market leaders are incorporating asphalt recycling into core operations, focusing on vertical integration to ensure quality control across the supply chain. From owning aggregate production units to operating asphalt mix plants and paving services, these companies have established streamlined processes to recover and reuse reclaimed asphalt efficiently.

Many are expanding their recycling capacity by setting up dedicated facilities, upgrading drum mixers, and utilizing mobile units for high-RAP applications. Technological integration is also becoming more prominent, with firms deploying digital tools for precise RAP dosing, temperature regulation, and emissions monitoring to support compliance with low-carbon construction standards. In addition, industry participants are collaborating with public agencies on research and pilot projects aimed at enhancing specifications for recycled asphalt use and optimizing full-depth recycling techniques.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Recycling Process

- 2.2.3 Application

- 2.2.4 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for road repair and infrastructure rehabilitation

- 3.2.1.2 Lower material and production costs compared to virgin asphalt

- 3.2.1.3 Stringent environmental regulations promoting recycled materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Initial investment costs for specialized recycling equipment and plant modifications

- 3.2.2.2 Inconsistent quality and performance of reclaimed asphalt material

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of government-funded sustainable infrastructure programs encouraging RAP integration

- 3.2.3.2 Rising adoption of cold-in-place and full-depth reclamation techniques in road construction

- 3.2.3.3 Development of performance-enhancing additives to improve high RAP mix quality

- 3.2.3.4 Increasing private sector interest in green construction materials for commercial projects

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Recycling Process, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Hot mix asphalt recycling

- 5.2.1 Batch plant

- 5.2.2 Drum plant

- 5.3 Cold mix asphalt recycling

- 5.3.1 In-place cold recycling

- 5.3.2 Central plant cold recycling

- 5.4 In-place recycling

- 5.4.1 Cold in-place recycling (CIR)

- 5.4.2 Full depth reclamation (FDR)

- 5.4.3 Hot in-place recycling (HIR)

- 5.5 Central plant recycling

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Road construction & rehabilitation

- 6.2.1 Highways and expressways

- 6.2.2 Urban roads and streets

- 6.2.3 Rural roads

- 6.3 Parking lots and pavements

- 6.4 Airport runways and taxiways

- 6.5 Pathways, bike lanes, and recreational surfaces

- 6.6 Other infrastructure (ports, industrial sites)

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Public sector

- 7.2.1 Departments of transportation (DOTs)

- 7.2.2 Municipalities and local governments

- 7.2.3 Airports and ports authorities

- 7.3 Private sector

- 7.3.1 Construction and engineering firms

- 7.3.2 Real estate developers

- 7.3.3 Industrial and commercial end use

- 7.4 Contractors and subcontractors

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Colas S.A.

- 9.2 Eurovia (VINCI Group)

- 9.3 Granite Construction Inc.

- 9.4 Oldcastle Materials (CRH)

- 9.5 LafargeHolcim Ltd.

- 9.6 CEMEX S.A.B. de C.V.

- 9.7 Vulcan Materials Company

- 9.8 Road Science

- 9.9 The Lane Construction Corporation

- 9.10 GreenRap

- 9.11 Downer Group (Reconophalt)

- 9.12 Gencor Industries

- 9.13 Phoenix Industries

- 9.14 Atmos Technologies

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日