構造用接着剤市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Structural Bonding Agents Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773391

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

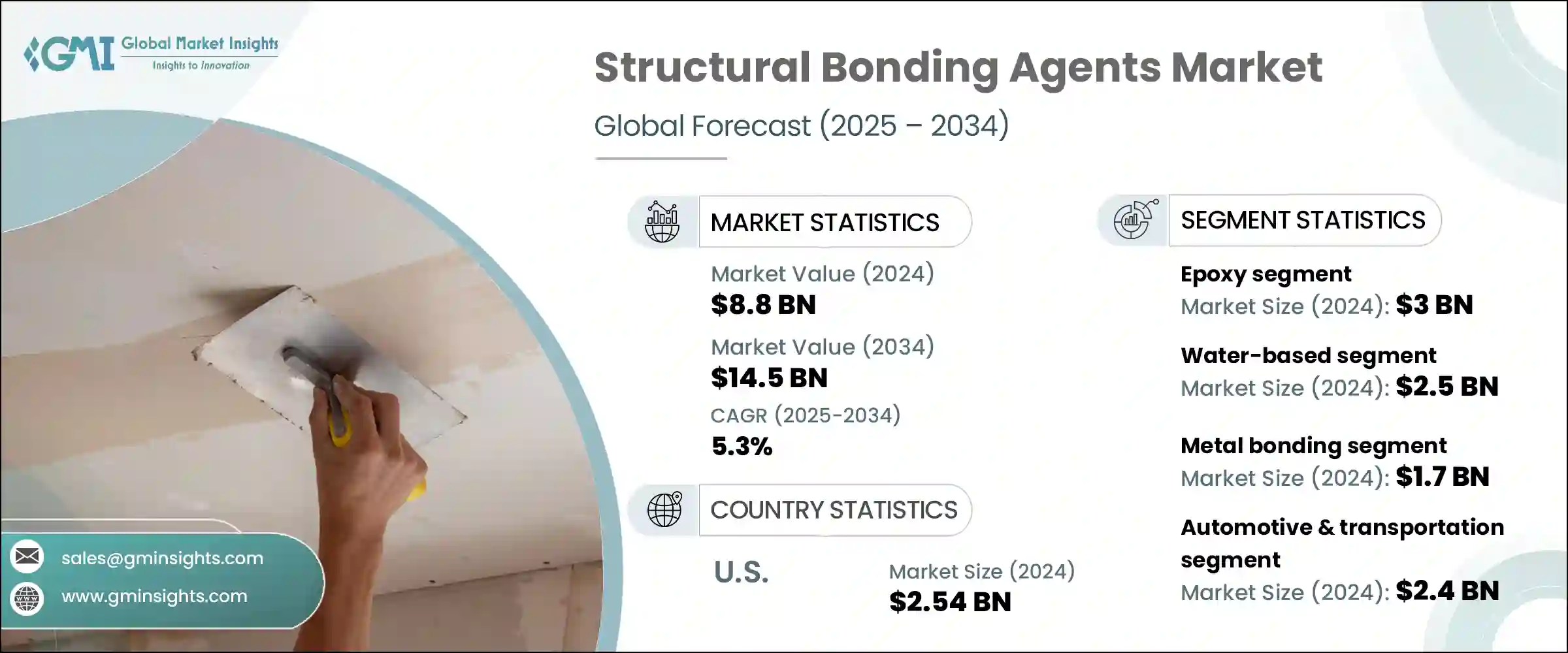

構造用接着剤の世界市場規模は2024年に88億米ドルとなり、CAGR 5.3%で成長し、2034年には145億米ドルに達すると予測されています。

市場拡大の要因はいくつかあるが、中でも自動車産業と航空宇宙産業における軽量材料の需要の高まりが大きいです。これらの分野では、構造強度を犠牲にすることなく燃費を向上させ、排出ガスを削減するのに役立つ、より軽量な複合材料をサポートするために接合剤を取り入れる傾向が強まっています。

また、さまざまな用途で複合材料の採用が拡大していることも、その優れた強度対重量比と耐久性により、市場の成長を後押ししています。構造用接着剤は、厳しい環境におけるこれらの材料の性能と受容性を高めることにより、重要な役割を果たしています。さらに、現在進行中の世界の建設プロジェクトは、需要に大きく寄与しています。接着剤は、荷重分散、美観、環境ストレス要因への耐性という点で、従来のメカニカルファスナーよりも優れているからです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 88億米ドル |

| 予測金額 | 145億米ドル |

| CAGR | 5.3% |

新たな動向は持続可能性にも向けられており、メーカーはより厳しい規制や消費者の嗜好に応えるため、環境に優しく、低VOC、無溶剤の接着剤に注力しています。このシフトは、環境コンプライアンスだけでなく、より健康的な室内空気の質と生態系への影響の低減に対する需要の増加によっても推進されています。グリーンビルディングの認証や排出基準が厳しくなるにつれ、企業は進化する世界・ベンチマークに合わせて接着剤を積極的に改良しています。市場は、特に建設、包装、輸送などの分野で、持続可能性が設計の中心的な考慮事項となっている水性およびバイオベースの構造用接着剤への嗜好の高まりを目の当たりにしています。

エポキシセグメントは2024年に30億米ドルの市場価値を持ち、2034年まで5%のCAGRで成長すると予想されます。エポキシ接着剤は、航空宇宙、自動車、建築、エレクトロニクスなどの産業における幅広い用途により、市場をリードしています。これらの接着剤は、優れた機械的強度、耐薬品性、金属と軽量複合材料の両方を接着する能力を提供し、高成長分野で不可欠なものとなっています。また、荷重を効果的に分散し、見た目に美しい仕上がりを実現する能力も、その需要に拍車をかけています。

水性構造用接着剤分野は2024年に25億米ドルを占め、2034年までCAGR 5.8%で成長すると予測されています。厳しい環境規制と低VOC処方へのシフトに後押しされ、水性接着剤は特に建設業界や包装業界で支持を集めています。これらの接着剤は、接着強度や性能を損なうことなく、より安全で環境に優しい代替品を提供します。

米国構造用接着剤2024年の市場規模は25億4,000万米ドルで、2025年から2034年にかけてCAGR 4.8%で成長すると予測されています。米国の成長は、インフラや建設プロジェクトに対する多額の投資と並んで、航空宇宙や自動車セクターにおける高性能で軽量な接着ソリューションに対する需要が大きな原動力となっています。接着技術の革新と有利な政府政策が引き続き市場拡大を後押ししています。

世界構造用接着剤市場の主要企業であるArkema Group、Henkel AG &Co.KGaA、3M Company、Sika AG、H.B. Fuller Companyなど、世界の構造用接着剤市場の大手企業は、いくつかの戦略的次元で活発に競争しています。構造用接着剤市場の企業は、技術革新に注力し、特に軽量で環境に優しい接着剤など、新たな産業ニーズに合わせた製品ポートフォリオを拡大することで、その地位を強化しています。各社は研究開発に多額の投資を行い、性能を向上させながら環境規制に適合する配合を開発しています。自動車、航空宇宙、建設セクターの主要企業との戦略的提携やパートナーシップは、市場へのリーチと信頼性の拡大に役立っています。さらに、急成長地域への地理的拡大が収益の伸びを支えています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- エポキシ

- 1成分エポキシ

- 2成分エポキシ

- 改質エポキシ

- ポリウレタン

- 1成分ポリウレタン

- 2成分ポリウレタン

- アクリル

- シアノアクリレート

- 改質アクリル

- メチルメタクリレート(MMA)

- シリコーン

- その他

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 水性

- 溶剤ベース

- ホットメルト

- 反応的

- その他

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 金属接合

- 鋼鉄

- アルミニウム

- その他の金属

- 複合接合

- 炭素繊維複合材

- ガラス繊維複合材

- その他の複合材料

- プラスチック接合

- 熱可塑性プラスチック

- 熱硬化性樹脂

- 木材接着

- ガラス接着

- コンクリートと石の接着

- 多材料接合

- その他

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 自動車・輸送

- 乗用車

- 商用車

- 電気自動車

- 鉄道

- その他

- 航空宇宙

- 商用機

- 軍用機

- 一般航空

- 宇宙用途

- 建築・建設

- 住宅

- 商業

- 産業

- インフラストラクチャー

- 風力エネルギー

- 陸上風力

- 洋上風力

- 海洋

- 造船

- ボート建造

- 海洋構造物

- エレクトロニクス

- コンシューマーエレクトロニクス

- 産業用電子機器

- 医療

- 工業組立

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東およびアフリカ

第10章 企業プロファイル

- Henkel AG &Co. KGaA

- 3M Company

- Sika AG

- H.B. Fuller Company

- Huntsman Corporation

- Arkema Group

- Lord Corporation(Parker Hannifin Corporation)

- Ashland Global Holdings Inc.

- Illinois Tool Works Inc.

- Dow Inc.

- Mapei S.p.A.

- RPM International Inc.

- Permabond LLC

- Master Bond Inc.

- Dymax Corporation

- Jowat SE

- Delo Industrial Adhesives

- Pidilite Industries Ltd.

- Parson Adhesives, Inc.

- Hernon Manufacturing, Inc.

目次

The Global Structural Bonding Agents Market was valued at USD 8.8 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 14.5 billion by 2034. The market expansion is driven by several factors, most notably the rising demand for lightweight materials in the automotive and aerospace industries. These sectors are increasingly incorporating bonding agents to support lighter composite materials, which help boost fuel efficiency and reduce emissions without sacrificing structural strength.

The growing adoption of composite materials across various applications also fuels market growth, thanks to their superior strength-to-weight ratio and durability. Structural bonding agents play a crucial role by enhancing the performance and acceptance of these materials in challenging environments. Additionally, ongoing global construction projects contribute significantly to demand, as bonding agents offer advantages over traditional mechanical fasteners in terms of load distribution, aesthetics, and resistance to environmental stressors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.8 Billion |

| Forecast Value | $14.5 Billion |

| CAGR | 5.3% |

Emerging trends also point toward sustainability, with manufacturers focusing on eco-friendly, low-VOC, and solvent-free adhesives to meet stricter regulations and consumer preferences. This shift is not only driven by environmental compliance but also by the increasing demand for healthier indoor air quality and reduced ecological impact. As green building certifications and emissions standards become more stringent, companies are proactively reformulating their bonding agents to align with evolving global benchmarks. The market is witnessing a growing preference for water-based and bio-based structural adhesives, particularly in sectors like construction, packaging, and transportation, where sustainability has become a core design consideration.

The epoxy segment held a market value of USD 3 billion in 2024 and is expected to grow at a 5% CAGR through 2034. Epoxy adhesives lead the market due to their wide-ranging applications in industries like aerospace, automotive, construction, and electronics. These adhesives provide excellent mechanical strength, chemical resistance, and the ability to bond both metals and lightweight composites, making them indispensable in high-growth sectors. Their ability to distribute loads effectively and deliver visually appealing finishes adds to their demand.

The water-based structural bonding agents segment accounted for USD 2.5 billion in 2024 and is anticipated to grow at a CAGR of 5.8% through 2034. Driven by stringent environmental regulations and a shift toward low-VOC formulations, water-borne adhesives are gaining traction, especially in the construction and packaging industries. These adhesives provide a safer, more environmentally friendly alternative without compromising bond strength or performance.

U.S. Structural Bonding Agents Market was valued at USD 2.54 billion in 2024 and is forecasted to grow at a CAGR of 4.8% from 2025 to 2034. Growth in the U.S. is largely fueled by the demand for high-performance, lightweight bonding solutions in the aerospace and automotive sectors, alongside substantial investments in infrastructure and construction projects. Innovation in adhesive technology and favorable government policies continue to bolster market expansion.

Leading players in the Global Structural Bonding Agents Market, such as Arkema Group, Henkel AG & Co. KGaA, 3M Company, Sika AG, and H.B. Fuller Company, are actively competing across several strategic dimensions. Companies in the structural bonding agents market strengthen their position by focusing on innovation and expanding product portfolios tailored to emerging industry needs, particularly lightweight and eco-friendly adhesives. They invest heavily in R&D to develop formulations that comply with environmental regulations while enhancing performance. Strategic collaborations and partnerships with key players in the automotive, aerospace, and construction sectors help expand market reach and credibility. Additionally, geographic expansion into fast-growing regions supports revenue growth.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Technology

- 2.2.4 Application

- 2.2.5 End Use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Epoxy

- 5.2.1 One-component epoxy

- 5.2.2 Two-component epoxy

- 5.2.3 Modified epoxy

- 5.3 Polyurethane

- 5.3.1 One-component polyurethane

- 5.3.2 Two-component polyurethane

- 5.4 Acrylic

- 5.4.1 Cyanoacrylates

- 5.4.2 Modified acrylics

- 5.5 Methyl methacrylate (MMA)

- 5.6 Silicone

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Water-based

- 6.3 Solvent-based

- 6.4 Hot melt

- 6.5 Reactive

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Metal Bonding

- 7.2.1 Steel

- 7.2.2 Aluminum

- 7.2.3 Other metals

- 7.3 Composite bonding

- 7.3.1 Carbon fiber composites

- 7.3.2 Glass fiber composites

- 7.3.3 Other composites

- 7.4 Plastic bonding

- 7.4.1 Thermoplastics

- 7.4.2 Thermosets

- 7.5 Wood bonding

- 7.6 Glass bonding

- 7.7 Concrete and stone bonding

- 7.8 Multi-material bonding

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Automotive & transportation

- 8.2.1 Passenger vehicles

- 8.2.2 Commercial vehicles

- 8.2.3 Electric vehicles

- 8.2.4 Rail

- 8.2.5 Others

- 8.3 Aerospace

- 8.3.1 Commercial aircraft

- 8.3.2 Military aircraft

- 8.3.3 General aviation

- 8.3.4 Space applications

- 8.4 Building & construction

- 8.4.1 Residential

- 8.4.2 Commercial

- 8.4.3 Industrial

- 8.4.4 Infrastructure

- 8.5 Wind Energy

- 8.5.1 Onshore wind

- 8.5.2 Offshore wind

- 8.6 Marine

- 8.6.1 Shipbuilding

- 8.6.2 Boat Building

- 8.6.3 Offshore structures

- 8.7 Electronics

- 8.7.1 Consumer electronics

- 8.7.2 Industrial electronics

- 8.8 Medical

- 8.9 Industrial assembly

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Henkel AG & Co. KGaA

- 10.2 3M Company

- 10.3 Sika AG

- 10.4 H.B. Fuller Company

- 10.5 Huntsman Corporation

- 10.6 Arkema Group

- 10.7 Lord Corporation (Parker Hannifin Corporation)

- 10.8 Ashland Global Holdings Inc.

- 10.9 Illinois Tool Works Inc.

- 10.10 Dow Inc.

- 10.11 Mapei S.p.A.

- 10.12 RPM International Inc.

- 10.13 Permabond LLC

- 10.14 Master Bond Inc.

- 10.15 Dymax Corporation

- 10.16 Jowat SE

- 10.17 Delo Industrial Adhesives

- 10.18 Pidilite Industries Ltd.

- 10.19 Parson Adhesives, Inc.

- 10.20 Hernon Manufacturing, Inc.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日