|

市場調査レポート

商品コード

1773388

口腔内センサー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Intra-Oral Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 口腔内センサー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月24日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

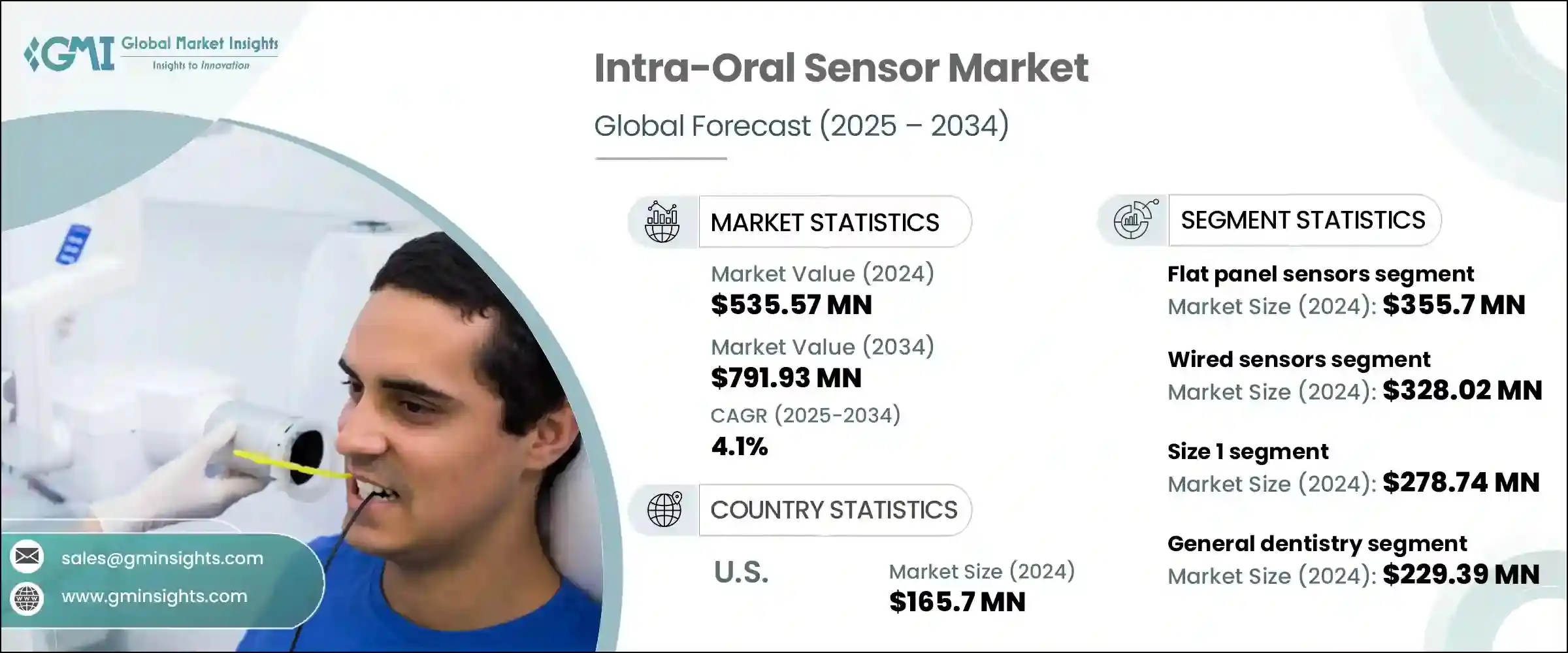

口腔内センサーの世界市場は、2024年に5億3,557万米ドルと評価され、CAGR 4.1%で成長し、2034年には7億9,193万米ドルに達すると予測されています。

この市場拡大の背景には、歯科疾患の罹患率の上昇と、早期かつ正確な診断に対する需要の高まりがあります。口腔内センサーは、歯とその周辺構造の高解像度デジタル画像を取り込むのに不可欠な役割を果たし、診断精度の向上、より正確な治療計画の立案、患者の治療成績の向上を可能にします。歯科医療従事者がより優れた診断ツール、特に加齢に関連する疾患の発見を求める中、高度な画像処理システムは不可欠なものとなっています。AI統合3DイメージングやコーンビームCT(CBCT)などの技術は、画像の忠実度と診断速度を向上させ、患者の不快感を軽減し、歯科ワークフローを合理化しています。

AIを搭載した口腔内センサーの急速な普及は、診断精度を高め、患者ケア全体を改善することで、世界中の歯科クリニックを変革しています。これらの先進的なシステムは、人工知能を活用して自動的に異常を検出し、画像分析を合理化し、人的ミスを減らすことで、開業医がより迅速で正確な診断を提供できるようにします。AIが進化を続ける中、機械学習アルゴリズムを搭載したセンサーは、最小限の手動入力で虫歯、歯周病、骨量減少の初期兆候を特定できるようになりました。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 5億3,557万米ドル |

| 予測金額 | 7億9,193万米ドル |

| CAGR | 4.1% |

口腔内センサー市場のフラットパネルセンサーセグメントは、2024年に3億5,570万米ドルを創出しました。フラットパネルセンサーの人気の高まりは、高精細画像出力によるところが大きいです。これらのセンサは、デジタルワークフローにシームレスに統合され、精度、スピード、診療管理システムとの相互運用性が不可欠な現代の歯科医療環境において不可欠なものとなっています。歯科医療従事者は、特に治療計画中や診察中の診断精度と患者とのコミュニケーションを改善する能力により、これらのセンサーをますます好むようになっています。さらに、人間工学に基づいたデザインとリアルタイム画像配信により、患者にもオペレーターにも優しい製品となっています。

有線センサー部門は、2024年に3億2,802万米ドルの評価額を確保し、強力な市場ポジションを維持しています。耐久性、信頼できる画像の一貫性、既存の歯科ソフトウェアエコシステムへの統合の容易さで知られる有線センサーは、ワイヤレスの柔軟性よりも信頼性を優先する開業医の間で最有力な選択肢であり続けています。これらのシステムは、継続的な電力供給とリアルタイムのデータ転送で動作し、処置中の中断を最小限に抑えます。費用対効果、メンテナンスの必要性の少なさ、実績があることから、特に予算に見合った拡張性の高い画像ソリューションを必要とするクリニックでは、有線センサーが選ばれています。

ドイツ口腔内センサー2024年の市場規模は3,027万米ドルであり、先進的なヘルスケアシステムと強固な歯科医療機器生産基盤に支えられています。強力な保険制度と国のデジタル化戦略に支えられ、最先端の歯科医療技術の採用が増え続けています。デジタル・ヘルス・ソリューションを奨励する政府の政策により、従来のイメージング・ツールからデジタル・センサーへの置き換えが着実に増加しています。さらに、歯科医療における厳格な臨床ガイドラインと厳格なトレーニング基準が、診断の卓越性と進化する医療規制へのコンプライアンスの両方を確保するため、診療所に頻繁に画像処理機能をアップグレードするよう促しています。

同市場の主なプレーヤーには、FONA srl、Carestream Dental LLC、Acteon Group、Dexis LLC、Genoray Co.メーカーはAIとCBCT技術の統合に注力し、診断精度の向上と迅速なイメージングを提供しています。歯科用ソフトウェア・プロバイダーや画像処理OEMとの提携により、包括的で統合が容易な画像処理ソリューションが生み出されています。増大する需要に対応するため、各社は製品ポートフォリオを拡大し、患者の快適性と診療効率を優先した小型のワイヤレス口腔内センサーを含めるようになっています。また、センサーの解像度を向上させ、放射線被ばくを低減するための研究開発にも投資しています。歯科医療従事者向けの教育イニシアティブやトレーニングプログラムは、導入率の向上と効果的な活用の確保に役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 歯科疾患の発生率の上昇

- デジタル歯科の導入拡大

- 画像センサーの技術的進歩

- 高齢化人口の増加

- 新興市場における歯科医療インフラの拡大

- 業界の潜在的リスク&課題

- 高度な口腔内センサーの高コスト

- デジタルインフラの不足により発展途上地域での導入が限られている

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- フラットパネルセンサー

- CCD(電荷結合素子)センサー

- CMOS(相補型金属酸化膜半導体)センサー

- 蛍光体蓄光板(PSP)

- その他

第6章 市場推計・予測:接続性別、2021年~2034年

- 主要動向

- 有線センサー

- ワイヤレスセンサー

第7章 市場推計・予測:センサーサイズ別、2021年~2034年

- 主要動向

- サイズ0

- サイズ1

- サイズ2

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 一般歯科

- 歯内療法

- 歯列矯正

- 歯周病

- インプラント

- その他

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売(バイヤーへのOEM)

- 販売代理店

- オンライン小売プラットフォーム

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Acteon Group

- Carestream Dental LLC.

- Dentsply Sirona Inc.

- Dexis LLC.

- FONA srl

- Genoray Co., Ltd.

- Hamamatsu Photonics K.K.

- ImageWorks Corporation

- Midmark Corporation

- MyRay

- Owandy Radiology

- Planmeca Oy

- Trident S.r.l.

- Vatech Co., Ltd.

- XDR Radiology

The Global Intra-Oral Sensor Market was valued at USD 535.57 million in 2024 and is estimated to grow at a CAGR of 4.1% to reach USD 791.93 million by 2034. This expansion is driven by a rising incidence of dental disorders and a growing demand for early and accurate diagnosis. Intra-oral sensors play an essential role in capturing high-resolution digital images of teeth and surrounding structures, enabling improved diagnostic accuracy, more precise treatment planning, and enhanced patient outcomes. As dental professionals seek better diagnostic tools-especially in detecting age-related conditions-advanced imaging systems are becoming indispensable. Technologies such as AI-integrated 3D imaging and Cone Beam Computed Tomography (CBCT) have improved image fidelity and diagnostic speed, reducing patient discomfort and streamlining dental workflows.

The rapid adoption of AI-powered intra-oral sensors is transforming dental clinics worldwide by elevating diagnostic precision and improving overall patient care. These advanced systems leverage artificial intelligence to automatically detect anomalies, streamline image analysis, and reduce human error, allowing practitioners to deliver faster and more accurate diagnoses. As AI continues to evolve, sensors equipped with machine learning algorithms can now identify early signs of cavities, gum disease, and bone loss with minimal manual input.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $535.57 million |

| Forecast Value | $791.93 million |

| CAGR | 4.1% |

The flat panel sensors segment in the intra-oral sensor market generated USD 355.7 million in 2024. Their rise in popularity is largely driven by high-definition image output, which allows for enhanced visualization of fine dental structures. These sensors integrate seamlessly into digital workflows, making them indispensable in modern dental environments where precision, speed, and interoperability with practice management systems are essential. Dental professionals increasingly favor these sensors due to their ability to improve diagnostic accuracy and patient communication, especially during treatment planning and consultations. Additionally, their ergonomic design and real-time image delivery make them both patient- and operator-friendly.

The wired sensors segment secured a valuation of USD 328.02 million in 2024 and continues to hold a strong market position. Known for their durability, dependable image consistency, and ease of integration into existing dental software ecosystems, wired sensors remain a top choice among practitioners who prioritize reliability over wireless flexibility. These systems operate with continuous power and real-time data transfer, minimizing disruptions during procedures. Their cost-effectiveness, minimal maintenance needs, and proven track record further reinforce their preference, especially in clinics that require budget-friendly, scalable imaging solutions.

Germany Intra-Oral Sensor Market was valued at USD 30.27 million in 2024, propelled by the nation's advanced healthcare system and robust dental equipment production base. Backed by strong insurance frameworks and national digitization strategies, the adoption of cutting-edge dental technologies continues to rise. Government policies encouraging digital health solutions have led to a steady increase in the replacement of traditional imaging tools with digital sensors. Additionally, stringent clinical guidelines and rigorous training standards in dentistry push clinics to frequently upgrade their imaging capabilities, ensuring both diagnostic excellence and compliance with evolving health regulations.

Prominent players in the market include FONA srl, Carestream Dental LLC., Acteon Group, Dexis LLC., Genoray Co., Ltd., Dentsply Sirona Inc. Manufacturers are focusing on integrating AI and CBCT technologies to offer enhanced diagnostic accuracy and faster imaging. Partnerships with dental software providers and imaging OEMs are creating comprehensive, easy-to-integrate imaging solutions. To meet growing demand, companies are expanding their product portfolios to include compact, wireless intra-oral sensors that prioritize patient comfort and clinic efficiency. They are also investing in R&D to improve sensor resolution and reduce radiation exposure. Educational initiatives and training programs for dental professionals help improve adoption rates and ensure effective utilization.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of dental disorders

- 3.2.1.2 Increasing adoption of digital dentistry

- 3.2.1.3 Technological advancements in imaging sensors

- 3.2.1.4 Growing geriatric population

- 3.2.1.5 Expanding dental care infrastructure in emerging markets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced intraoral sensors

- 3.2.2.2 Limited adoption in developing regions due to lack of digital infrastructure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Flat panel sensors

- 5.2.1 CCD (charge-coupled device) sensors

- 5.2.2 CMOS (complementary metal-oxide semiconductor) sensors

- 5.3 Phosphor storage plate (PSP)

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Connectivity, 2021 - 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Wired sensors

- 6.3 Wireless sensors

Chapter 7 Market Estimates and Forecast, By Sensor Size, 2021 - 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Size 0

- 7.3 Size 1

- 7.4 Size 2

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 General dentistry

- 8.3 Endodontics

- 8.4 Orthodontics

- 8.5 Periodontics

- 8.6 Implantology

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Million & Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales (OEM to Buyer)

- 9.3 Distributors

- 9.4 Online retail platforms

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Acteon Group

- 11.2 Carestream Dental LLC.

- 11.3 Dentsply Sirona Inc.

- 11.4 Dexis LLC.

- 11.5 FONA srl

- 11.6 Genoray Co., Ltd.

- 11.7 Hamamatsu Photonics K.K.

- 11.8 ImageWorks Corporation

- 11.9 Midmark Corporation

- 11.10 MyRay

- 11.11 Owandy Radiology

- 11.12 Planmeca Oy

- 11.13 Trident S.r.l.

- 11.14 Vatech Co., Ltd.

- 11.15 XDR Radiology