|

市場調査レポート

商品コード

1773375

乗用車キャビンモニタリングシステム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Passenger Vehicle Cabin Monitoring System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 乗用車キャビンモニタリングシステム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月24日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

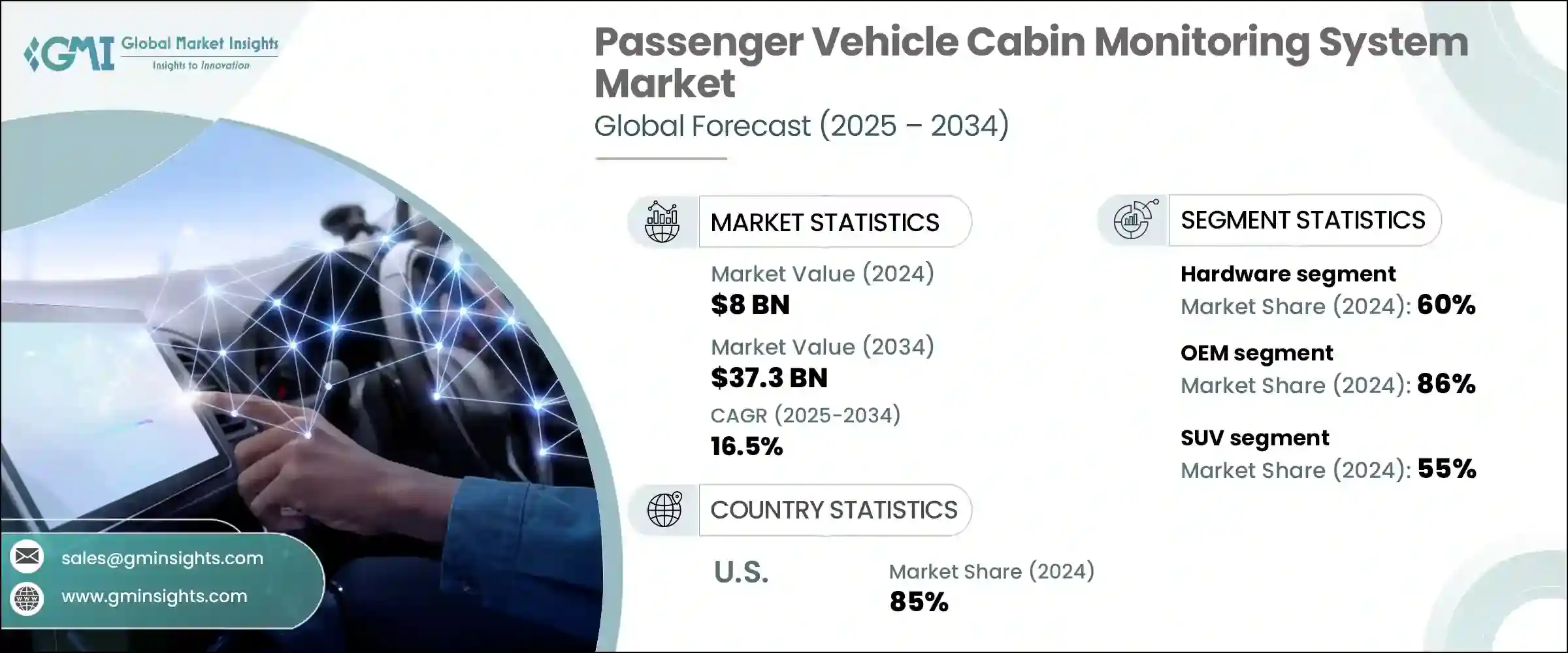

乗用車キャビンモニタリングシステムの世界市場規模は、2024年に80億米ドルとなり、CAGR16.5%で成長し、2034年には373億米ドルに達すると予測されています。

自動車メーカーと消費者の双方による、乗員の安全性、快適性、スマートな車内技術への注目の高まりが、この成長の主要な推進力となっています。自動車の自律化が進むにつれて、バイタルサイン検出、乗員識別、ドライバー監視を含むキャビン・モニタリング・システムの統合が最新の自動車設計の標準になりつつあります。

これらのシステムは、センサーとAIを活用したアルゴリズムの組み合わせに依存しており、ドライバーの覚醒度を監視し、同乗者を検出し、さらには生体データを分析して、眠気警告、適応型エアバッグの展開、緊急介入などの機能をサポートします。主要な自動車市場の規制機関が高度な安全機能を義務付け、購入者がパーソナライズされたプロアクティブなキャビン体験を強く求めていることから、インテリジェント・キャビン・モニタリング・ソリューション市場は急成長の態勢を整えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 80億米ドル |

| 予測金額 | 373億米ドル |

| CAGR | 16.5% |

これらのシステムはコンセプトの段階を超え、乗員の識別、ドライバーの注意力評価、子供の安全確保に不可欠なものとなり、日常的な自動車における役割を確固たるものにしています。かつてはプレミアムまたは未来的な機能と見なされていたものが、規制上の義務付けと消費者の期待の変化の両方によって、今や標準的な要件になりつつあります。先進的なキャビン・モニタリング・システムは、バイタルサインの検出、疲労レベルのモニター、緊急事態へのリアルタイム対応など、利便性と車内セキュリティの両方を高めるために統合されるようになりました。また、居住状況に基づく自動空調調整や生体認証に基づくパーソナライゼーションなどのインテリジェント機能もサポートします。

2024年には、ハードウェア分野が60%のシェアを占め、2025~2034年のCAGRは16%と予測されています。ハードウェアは、カメラ、レーダーセンサー、赤外線モジュール、組み込みエレクトロニクスで構成され、依然として乗用車のキャビン・モニタリング・システムの要となっています。自動車メーカーが車内のスマート化に注力する中、堅牢で応答性の高いハードウェアの必要性は極めて重要です。これらのコンポーネントは、ドライバーの警戒、乗客の存在、生体指標を追跡するAIアルゴリズムに燃料を供給するのに必要なリアルタイムデータを提供し、システム性能に不可欠なものとなっています。

OEMセグメントは2024年に86%のシェアを占め、自動車業界がセンサー対応の工場設置型安全ソリューションを推進していることが背景にあります。自動車メーカーは、生産時にキャビンとドライバー・モニタリング・システムを直接統合することを選択するようになっており、空調制御、ADAS、インフォテインメント・システムなどの他の車載技術とのシームレスな互換性を確保しています。OEMによる取り付けは、システムの精度、信頼性、消費者の信頼を高めるため、この市場で好まれる提供方法となっています。

北米乗用車キャビンモニタリングシステム市場は85%のシェアを占め、2024年には24億米ドルを創出しました。成熟した自動車部門、厳格な安全基準、技術革新への強い意欲により、同国が採用をリードしています。自動車メーカーは、生体追跡、乗員検知、疲労モニタリングなどの機能を新車モデルに標準装備することに積極的です。こうした需要と規制当局のサポートが相まって、米国はこの分野で圧倒的な強さを誇っています。

乗用車キャビンモニタリングシステム業界の有力企業には、Magna International Inc.、Panasonic Corporation、Robert Bosch GmbH、Continental AG、Valeo S.A.、Denso Corporation、Visteon Corporationなどがあります。乗用車キャビンモニタリングシステム市場における足場を固めるため、企業はいくつかの重要な戦略を採用しています。イノベーションが最前線にあり、センサーの精度、AI機能、車両アーキテクチャとのシステム統合を進めるための研究開発に多額の投資を行っています。自動車メーカーとの協業や戦略的パートナーシップは、新技術の採用を加速し、特定のOEMニーズに合わせたソリューションの提供を支援します。各社はまた、多様な市場に対応するため、現地生産とカスタマーサポートを通じた世界展開の拡大にも注力しています。サイバーセキュリティ機能の強化とシステムの信頼性向上は、安全システムに対する消費者の信頼を高めるために優先されます。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 政府の支援を受けて電気自動車の世界の普及が進む

- 軽量でスマートなベアリング技術の進歩により、効率と耐久性が向上します

- 新興市場におけるEV製造の拡大

- センサー対応ベアリングによる予知保全の統合

- 業界の潜在的リスク&課題

- 初期費用が高め

- 複雑な設置とメンテナンス

- 市場機会

- 世界のEV生産の急増

- OEMとの研究開発および共同開発

- 促進要因

- 成長可能性分析

- 規制情勢

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許分析

- 価格動向

- 地域別

- コンポーネント別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- カメラ

- センサー

- 表示単位

- 制御ユニット

- ソフトウェア

- サービス

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- ハッチバック

- セダン

- SUV

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 促進要因ー監視システム

- 視線追跡

- 顔認識

- 頭位モニタリング

- 眠気検知

- 注意散漫検出

- 乗員監視システム(OMS)

- 乗員存在検知

- シートベルト監視

- 子供の検出

- 乗客行動分析

- その他

第8章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- カメラベース

- センサーベース

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

第11章 企業プロファイル

- Aptiv

- Autoliv

- Caaresys

- Continental

- Denso

- Faurecia S.A.

- Gentex

- Harman International Industries, Inc.

- Hyundai Mobis

- Magna International

- Omron

- Panasonic

- Robert Bosch

- Seeing Machines

- Smart Eye AB

- Tobii

- Valeo S.A.

- Vayyar Imaging

- Visteon

- ZF Friedrichshafen

The Global Passenger Vehicle Cabin Monitoring System Market was valued at USD 8 billion in 2024 and is estimated to grow at a CAGR of 16.5% to reach USD 37.3 billion by 2034. The rising focus on occupant safety, comfort, and smart in-cabin technology by both car manufacturers and consumers is a key driver of this growth. As vehicles become increasingly autonomous, the integration of cabin monitoring systems-including vital sign detection, occupant identification, and driver monitoring-is becoming standard in modern car designs.

These systems rely on a mix of sensors and AI-powered algorithms to monitor driver alertness, detect passengers, and even analyze biometric data, supporting functions such as drowsiness alerts, adaptive airbag deployment, and emergency interventions. With regulatory agencies in major automotive markets mandating advanced safety features and buyers showing strong demand for personalized and proactive cabin experiences, the market for intelligent cabin monitoring solutions is poised for rapid growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8 Billion |

| Forecast Value | $37.3 Billion |

| CAGR | 16.5% |

These systems have moved beyond the concept stage to become essential in identifying occupants, assessing driver attention, and ensuring child safety, solidifying their role in everyday vehicles. What was once viewed as a premium or futuristic feature is now becoming a standard requirement, driven by both regulatory mandates and shifting consumer expectations. Advanced cabin monitoring systems are now integrated to detect vital signs, monitor fatigue levels, and respond to emergencies in real-time, enhancing both convenience and in-vehicle security. They also support intelligent functions like automatic climate adjustment based on occupancy and biometric-based personalization.

In 2024, the hardware segment held a 60% share and is forecasted to grow at a CAGR of 16% during 2025-2034. Hardware remains the cornerstone of cabin monitoring systems in passenger vehicles, consisting of cameras, radar sensors, infrared modules, and embedded electronics. As automakers focus on smarter interiors, the need for robust and responsive hardware is critical. These components provide the real-time data necessary to fuel AI algorithms that track driver vigilance, passenger presence, and biometric indicators, making them indispensable for system performance.

The OEM segment held an 86% share in 2024, driven by the automotive industry's push toward sensor-enabled, factory-installed safety solutions. Vehicle manufacturers increasingly opt to integrate cabin and driver monitoring systems directly during production, ensuring seamless compatibility with other in-car technologies like climate control, ADAS, and infotainment systems. OEM installation enhances system accuracy, reliability, and consumer trust, making it the preferred method of delivery in this market.

North America Passenger Vehicle Cabin Monitoring System Market held an 85% share and generated USD 2.4 billion in 2024. The country leads adoption due to a mature automotive sector, stringent safety standards, and a strong appetite for innovation. Automakers are proactively incorporating features such as biometric tracking, occupant detection, and fatigue monitoring as standard across new vehicle models. This demand, combined with regulatory support, positions the U.S. as a dominant force in this segment.

Prominent companies in the Passenger Vehicle Cabin Monitoring System Industry include Magna International Inc., Panasonic Corporation, Robert Bosch GmbH, Continental AG, Valeo S.A., Denso Corporation, and Visteon Corporation. To strengthen their foothold in the passenger vehicle cabin monitoring system market, companies are adopting several key strategies. Innovation is at the forefront, with significant investment in research and development to advance sensor accuracy, AI capabilities, and system integration with vehicle architectures. Collaborations and strategic partnerships with automakers accelerate the adoption of new technologies and help tailor solutions to specific OEM needs. Companies are also focusing on expanding their global reach through localized production and customer support to serve diverse markets. Enhancing cybersecurity features and improving system reliability are prioritized to build consumer confidence in safety systems.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Technology

- 2.2.5 Sales channel

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing global adoption of electric vehicles supported by government incentives

- 3.2.1.2 Advancements in lightweight and smart bearing technologies improve efficiency and durability

- 3.2.1.3 Expansion of EV manufacturing in emerging markets

- 3.2.1.4 Integration of predictive maintenance through sensor-enabled bearings

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial costs

- 3.2.2.2 Complex installation and maintenance

- 3.2.3 Market opportunities

- 3.2.3.1 Surging global EV production

- 3.2.3.2 R&D and co-development with OEMs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By component

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Cost breakdown analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Cameras

- 5.2.2 Sensors

- 5.2.3 Display Units

- 5.2.4 Control Units

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Hatchback

- 6.3 Sedan

- 6.4 SUV

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Driver monitoring system

- 7.2.1 Eye-Tracking

- 7.2.2 Facial recognition

- 7.2.3 Head position monitoring

- 7.2.4 Drowsiness detection

- 7.2.5 Distraction detection

- 7.3 Occupant Monitoring System (OMS)

- 7.3.1 Occupant presence detection

- 7.3.2 Seat belt monitoring

- 7.3.3 Child detection

- 7.3.4 Passenger behavior analysis

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEMs

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Camera based

- 9.3 Sensor based

- 9.4 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aptiv

- 11.2 Autoliv

- 11.3 Caaresys

- 11.4 Continental

- 11.5 Denso

- 11.6 Faurecia S.A.

- 11.7 Gentex

- 11.8 Harman International Industries, Inc.

- 11.9 Hyundai Mobis

- 11.10 Magna International

- 11.11 Omron

- 11.12 Panasonic

- 11.13 Robert Bosch

- 11.14 Seeing Machines

- 11.15 Smart Eye AB

- 11.16 Tobii

- 11.17 Valeo S.A.

- 11.18 Vayyar Imaging

- 11.19 Visteon

- 11.20 ZF Friedrichshafen