ペット用治療食の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Pet Therapeutic Diet Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773356

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

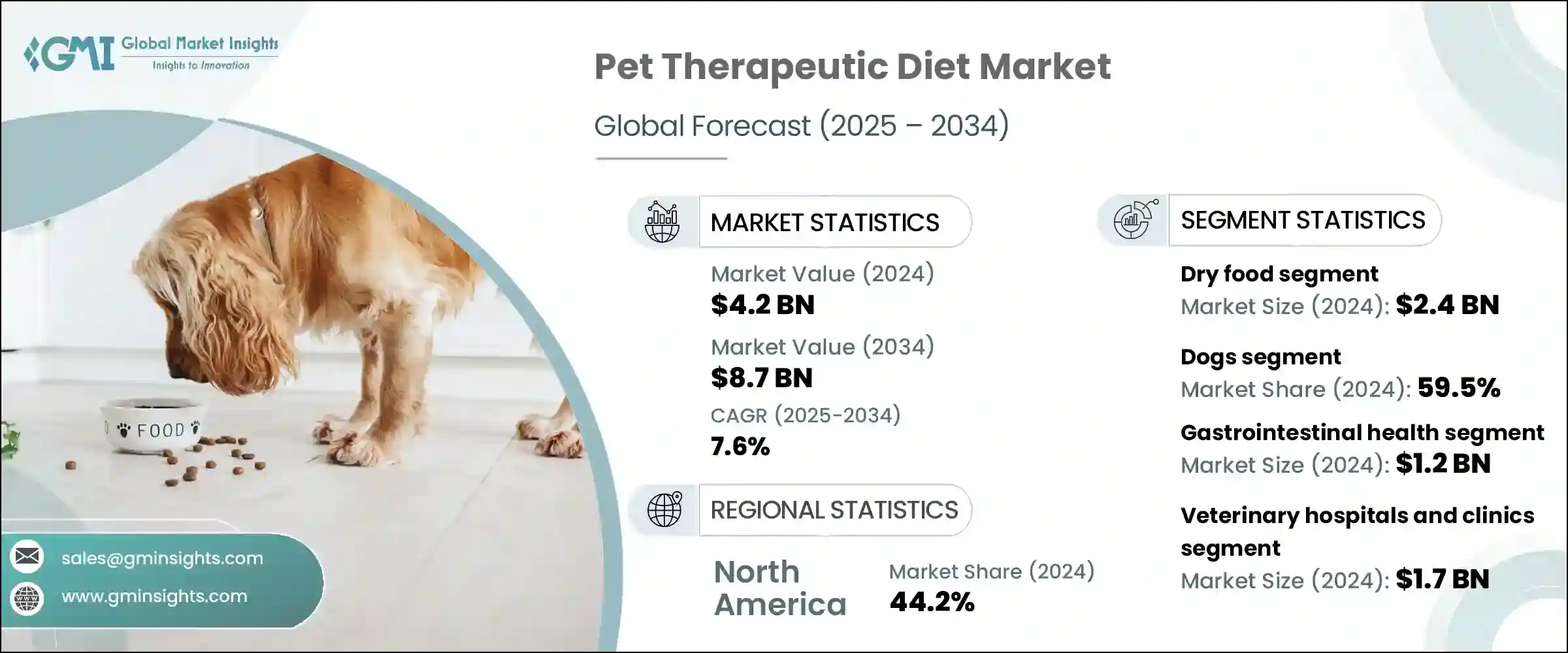

世界のペット用治療食市場は、2024年には42億米ドルと評価され、CAGR7.6%で成長し、2034年までには87億米ドルに達すると推定されています。

コンパニオンアニマルにおける慢性的な健康問題-肥満、糖尿病、腎臓病、胃腸障害など-の増加は、的を絞った栄養ソリューションの需要を促進しています。ペットの飼い主がますます家族中心のペットの世話をするようになっているため、予防と治療の両方のメリットを提供する特殊な食事に投資する意欲が高まっています。責任あるペットの飼い方に対する意識の高まりと、積極的な健康管理へのシフトがこの動向を後押ししています。

治療食の普及は、獣医師による指導の増加や、よりホリスティックなケアオプションへの需要によって、さらに拍車がかかっています。現在、多くのペットの飼い主は、栄養を病態を管理し、動物の長期的な健康を確保するための不可欠なツールと見なしています。ペットの人間化の動向は、ペットフードの品質と臨床効果への期待を高めています。その結果、より多くの消費者が、回復と継続的な健康をサポートするために、病態に特化した食事を選ぶようになり、新興国市場と開拓市場の両方において、治療食はコンパニオンアニマルヘルスケア戦略の中核をなすものと位置づけられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 42億米ドル |

| 予測金額 | 87億米ドル |

| CAGR | 7.6% |

ペット用治療食は、ペットの特定の病状の治療、管理、予防に役立つよう調整された、動物栄養分野の中でも特殊なセグメントです。これらの製剤は獣医学的ケアにおいて重要な役割を果たし、回復をサポートし、症状を軽減し、全体的な健康を促進するように設計された栄養上の利点を提供します。

ドライフードカテゴリーのセグメントは2024年に市場をリードし、評価額は24億米ドルに達しました。ペットの飼い主や獣医師がドライフードを好むのは、費用対効果が高く、保存期間が長く、保管が容易なためです。これらの製品は確実な分量管理が可能で、一貫した治療用栄養を必要とするペット、特に慢性疾患を管理するペットに理想的です。肥満、腎臓病、胃腸のアンバランスといった健康問題に対応するよう設計されたドライフードは、毎日の給餌を容易にすると同時に、ペットの継続的なケアに必要な栄養素を確実に摂取できます。

犬用セグメントは2024年に59.5%のシェアを占めました。犬の健康懸念、特に不活発なライフスタイルや人工的な成分を多く含む食事によって悪化する肥満の増加が、治療食製品に対する需要を煽っています。犬の自然な傾向として、頻繁に食べ物を摂取するため、バランスのとれた健康志向の食事を与えることの重要性が高まっています。犬の食習慣と栄養ニーズはペットフードの選択にますます影響を与えるようになっており、飼い主は長期的な健康維持のために専門的な治療食を選ぶようになっています。

米国のペット用治療食市場は2024年に17億米ドルに達しました。ペットの飼育頭数の増加と高齢化人口の増加が市場拡大の主な要因です。現在、多くのペットが心血管疾患、関節疾患、その他の慢性疾患を管理するために特殊な食事を必要としています。ペットの予防的健康対策への注目の高まりも、治療食の需要を押し上げています。高度に発達した米国の獣医療ネットワークは、こうした治療食を長期的な治療計画に組み込んでおり、疾病管理や日常的な動物ケアの標準的な一部となっています。また、ペット保険に対する認識が高まり、ペット保険を利用できるようになったことで、より多くの飼い主がプレミアム治療食を検討するようになっています。

世界市場をリードする企業には、Veterinary Nutrition Group、JustFoodForDogs、Open Farm、Diamond Pet Foods、Mars Petcare、Hill's Pet Nutrition、EmerAid、Stella and Chewy's、United PetFood、Eden Holistic Pet Foods、Blue Buffalo(General Mills)、Virbac、Ziwi、Nestle、iVet.comなどがあります。市場での存在感を高めるため、ペット用治療食分野の企業は、科学的裏付けのある特定の症状に特化した食事を処方するための研究開発に多額の投資を行っています。多くの企業は、腎臓サポート、消化器ケア、代謝の健康、関節の健康など、より幅広い健康問題をカバーするために製品ラインを拡大しています。獣医師や動物病院との提携は、製品の信頼性とリーチを高めています。戦略的なマーケティング活動により、臨床的効能と高品質の原材料を強調し、消費者の信頼を築いています。また、健康意識の高い飼い主の期待に応えるため、透明性の高い表示やクリーンな処方を採用しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- ペットの高齢化

- ペット飼育の増加とペットの人間化

- ペット動物における慢性疾患の増加

- 製品の革新とカスタマイズ

- 業界の潜在的リスク・課題

- 規制上の課題と信頼性の懸念

- 認識と教育の不足

- 市場機会

- 発展途上地域におけるペット飼育の増加と都市化

- クリーンラベル、オーガニック、植物ベースの治療食の需要増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- 技術的情勢

- 価格分析

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な開発

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ドライフード

- ウェットフード/缶詰

- その他の製品タイプ

第6章 市場推計・予測:動物タイプ別、2021年~2034年

- 主要動向

- 猫

- 犬

- その他の動物

第7章 市場推計・予測:健康状態別、2021年~2034年

- 主要動向

- 腎臓の健康

- 胃腸の健康

- 心臓血管の健康

- 体重管理

- 関節ケア

- その他の健康状態

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 動物病院・診療所

- eコマース

- 小売薬局

- その他の流通チャネル

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Blue Buffalo(General Mills)

- Diamond Pet Foods

- Eden Holistic Pet Foods

- EmerAid

- Hill's Pet Nutrition

- iVet.com

- JustFoodForDogs

- Mars Petcare

- Nestle

- Open Farm

- Stella and Chewy's

- United PetFood

- Veterinary Nutrition Group

- Virbac

- Ziwi

目次

The Global Pet Therapeutic Diet Market was valued at USD 4.2 billion in 2024 and is estimated to grow at a CAGR of 7.6% to reach USD 8.7 billion by 2034. Increasing chronic health issues in companion animals-such as obesity, diabetes, kidney disease, and gastrointestinal disorders-are driving the demand for targeted nutritional solutions. As pet owners increasingly adopt a family-centric approach to pet care, they're more willing to invest in specialized diets that offer both preventive and therapeutic benefits. Rising awareness about responsible pet ownership and a shift toward proactive health management are reinforcing this trend.

The broader adoption of therapeutic nutrition is further fueled by growing veterinary guidance and a demand for more holistic care options. Many pet parents now view nutrition as an essential tool for managing conditions and ensuring the long-term wellness of their animals. The trend toward pet humanization has elevated expectations for quality and clinical efficacy in pet food. As a result, more consumers are turning to condition-specific diets to support recovery and ongoing health, positioning therapeutic diets as a core component of companion animal healthcare strategies in both emerging and developed markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $8.7 Billion |

| CAGR | 7.6% |

Pet therapeutic diets represent a specialized segment within the animal nutrition sector, tailored to help treat, manage, or prevent specific medical conditions in pets. These formulations play a key role in veterinary care, delivering nutritional benefits designed to support recovery, reduce symptoms, and promote overall well-being.

The dry food category segment led the market in 2024, reaching a valuation of USD 2.4 billion. Pet owners and veterinarians prefer dry food due to its cost-effectiveness, long shelf life, and ease of storage. These products offer reliable portion control and are ideal for pets requiring consistent therapeutic nutrition, especially those managing chronic conditions. Designed to address health issues like obesity, kidney disease, or gastrointestinal imbalances, dry formulations make daily feeding routines easier while ensuring pets receive the necessary nutrients for ongoing care.

The dogs segment held a 59.5% share in 2024. A growing number of health concerns in dogs-particularly obesity, which is exacerbated by inactive lifestyles and diets high in artificial ingredients-are fueling demand for therapeutic food products. The natural tendency of dogs to consume food frequently increases the importance of feeding them balanced, health-oriented diets. Their dietary habits and nutritional needs are increasingly influencing pet food choices, encouraging owners to turn to specialized therapeutic options to maintain long-term health.

United States Pet Therapeutic Diet Market reached USD 1.7 billion in 2024. Rising pet adoption and the growing population of aging animals are major contributors to market expansion. Many pets now require specialized diets to manage cardiovascular conditions, joint problems, and other chronic illnesses. An increased focus on preventive health measures for pets is also boosting demand for therapeutic diets. The highly developed veterinary network in the U.S. incorporates these diets into long-term treatment plans, making them a standard part of disease management and routine animal care. Greater awareness and access to pet insurance are also enabling more owners to explore premium dietary solutions.

Companies leading the global market include Veterinary Nutrition Group, JustFoodForDogs, Open Farm, Diamond Pet Foods, Mars Petcare, Hill's Pet Nutrition, EmerAid, Stella and Chewy's, United PetFood, Eden Holistic Pet Foods, Blue Buffalo (General Mills), Virbac, Ziwi, Nestle, and iVet.com. To strengthen their market presence, companies in the pet therapeutic diet space are investing heavily in research and development to formulate science-backed, condition-specific diets. Many firms are expanding product lines to cover a wider range of health issues, including renal support, digestive care, metabolic health, and joint wellness. Collaborations with veterinarians and veterinary clinics are enhancing product credibility and reach. Strategic marketing efforts emphasize clinical efficacy and quality ingredients to build trust among consumers. Players are also adopting transparent labeling and clean formulations to align with the expectations of health-conscious pet owners.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Animal type

- 2.2.4 Health condition

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Aging pet population

- 3.2.1.2 Rising pet ownership and pet humanization

- 3.2.1.3 Growing prevalence of chronic disease in companion animals

- 3.2.1.4 Product innovation and customization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory challenges and reliability concerns

- 3.2.2.2 Limited awareness and education

- 3.2.3 Market opportunities

- 3.2.3.1 Rising pet ownership and urbanization in developing regions

- 3.2.3.2 Growing demand for clean-label, organic and plant-based therapeutic diets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological landscape

- 3.6 Pricing analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key development

- 4.6.1 Mergers and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dry food

- 5.3 Wet/ canned food

- 5.4 Other product types

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cats

- 6.3 Dogs

- 6.4 Other animals

Chapter 7 Market Estimates and Forecast, By Health Condition, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Renal health

- 7.3 Gastrointestinal health

- 7.4 Cardiovascular health

- 7.5 Weight management

- 7.6 Joint care

- 7.7 Other health conditions

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospitals and clinics

- 8.3 E-commerce

- 8.4 Retail pharmacies

- 8.5 Other distribution channels

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Blue Buffalo (General Mills)

- 10.2 Diamond Pet Foods

- 10.3 Eden Holistic Pet Foods

- 10.4 EmerAid

- 10.5 Hill's Pet Nutrition

- 10.6 iVet.com

- 10.7 JustFoodForDogs

- 10.8 Mars Petcare

- 10.9 Nestle

- 10.10 Open Farm

- 10.11 Stella and Chewy's

- 10.12 United PetFood

- 10.13 Veterinary Nutrition Group

- 10.14 Virbac

- 10.15 Ziwi

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日