|

市場調査レポート

商品コード

1773341

産業用インクジェットプリンターの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Industrial Inkjet Printers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 産業用インクジェットプリンターの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月23日

発行: Global Market Insights Inc.

ページ情報: 英文 225 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

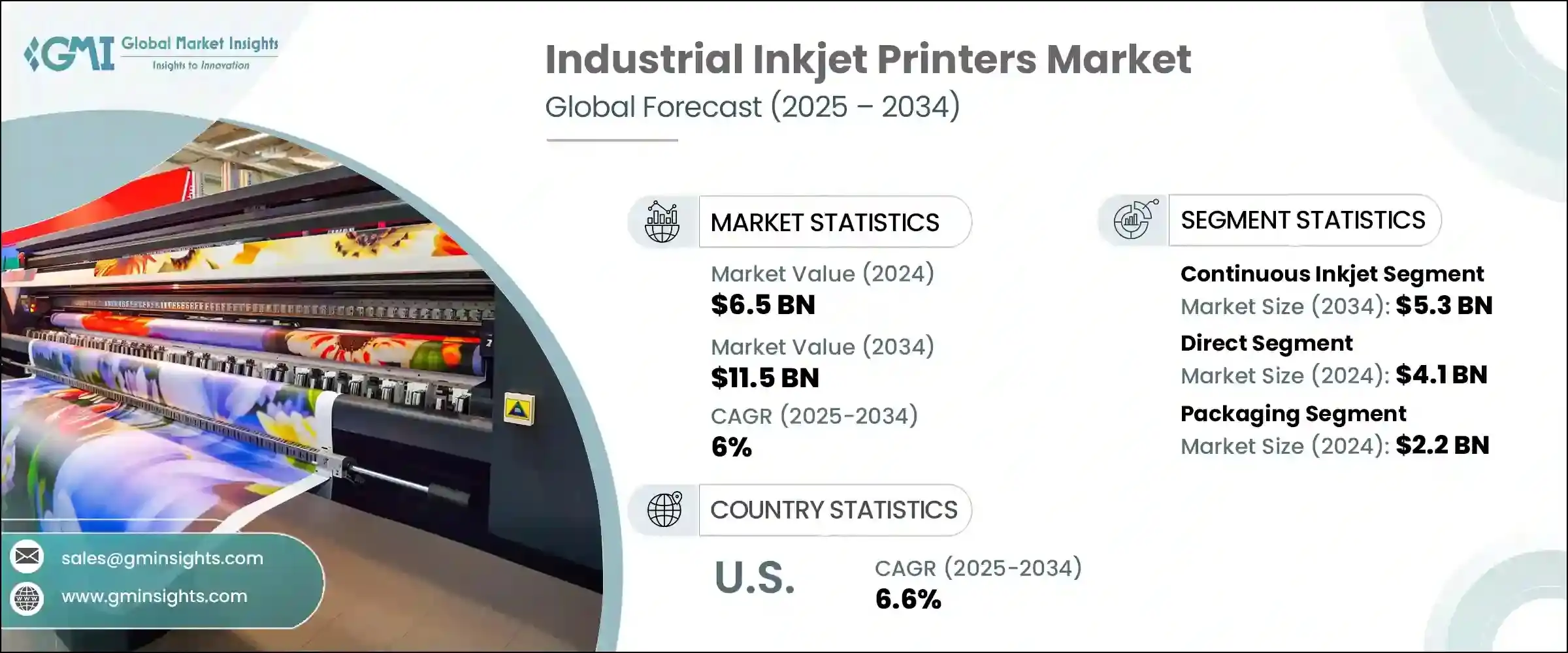

産業用インクジェットプリンターの世界市場規模は、2024年に65億米ドルとなり、CAGR6%で成長し、2034年までには115億米ドルに達すると予測されています。

医薬品、テキスタイル、パッケージングなどの業界では、バリアブルデータ印刷、特にバーコード、日付、シリアル番号、バッチコードなどを多様な素材にリアルタイムでラベリングする需要が大幅に高まっています。この成長は、製品のパーソナライゼーション、規制基準の厳格化、競争市場におけるブランドの差別化に対する消費者の期待によって後押しされています。

インクジェットシステムは、高解像度の印刷を小ロットで行うための柔軟で費用対効果の高いソリューションであり、コストのかかる段取り替えを必要としないため、エンドユーザーの間で採用が拡大しています。さらに、特に米国環境保護庁(EPA)が廃棄物の削減とエネルギー効率の改善に重点を置いていることから、持続可能性は勢いを増しています。その結果、環境に配慮した生産性の高い代替手段としてインクジェット印刷を採用する企業が増えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 65億米ドル |

| 予測金額 | 115億米ドル |

| CAGR | 6% |

技術の進歩、特に印字ヘッド設計、デジタルインク処方、インダストリー4.0プラットフォームとの統合により、インクジェットプリンターの性能は大幅に向上しています。これらの改良により、超高解像度の出力が可能になり、微小液滴の制御やピクセル精度の向上などの機能を活用することで、装飾パッケージング、フィルムラベリング、カスタム素材などの特殊用途に恩恵をもたらしています。さらに、産業用インクジェット技術は、付加製造、特にバインダージェッティングに活路を見いだし、バイオメディカル、航空宇宙、自動車など、さまざまな分野の3Dプリンティングで実行可能な方法であることが証明されつつあります。これらのマシンが進化するにつれて、潜在的な投資収益率は増加し続け、現代の生産環境における役割を確固たるものにしています。

コンティニュアスインクジェット(CIJ)セグメントは2024年に29億米ドルを占め、2034年には53億米ドルに増加すると予想されています。このセグメントが市場をリードしているのは、メンテナンスの必要性を最小限に抑えながら高速で非接触印刷を実行できるためです。耐久性に優れ、要求の厳しい環境でも安定した出力が可能なため、さまざまな基材に有効期限や追跡コードなどの可変情報を印刷するビジネスに人気があります。強力な粘着特性と、厳しい産業条件下でもシームレスな操作性により、CIJシステムは引き続き市場で高い地位を維持しています。

直販セグメントは2024年に41億米ドルを占め、2025年から2034年のCAGRは6.1%と予想されています。高度なカスタマイズと技術的複雑さを要求する産業用途が、主にこのセグメントを牽引しています。Epson、Markem-Imaje、Domino Printing Sciences、Videojetなどの大手メーカーは、顧客との直接的な関係を構築することで、市場へのアプローチを強化しています。これらの企業は、システムのセットアップ、リアルタイムのテクニカルサポート、保守契約、既存のワークフローとの完全な統合など、顧客に合わせたサービスを提供し、長期的な顧客の維持と満足を確保しています。

北米の産業用インクジェットプリンター市場は、2024年に9億米ドルと評価され、2025年から2034年にかけてCAGR6.6%で成長すると予測されています。米国の優位性は、その確立された技術的に高度な製造エコシステムに起因します。インクジェットシステムは、電子機器、食品製造、医薬品など様々な分野におけるマーキング、コーディング、ラベリング工程に広く採用されています。これらのシステムは、既存のオートメーションセットアップに効率的に統合され、ダウンタイムを最小限に抑えながらスループットを大幅に向上させます。業界リーダーによる継続的な研究開発努力は、産業用インクジェット技術の性能、耐久性、運用効率の向上を続けています。

産業用インクジェットプリンター業界の競合状況を形成している主要企業には、Canon、Fujifilm、Durst Phototechnik、HP、Brother Industries、Konica Minolta、Epson、itachi Industrial Equipment Systems、Mitsubishi Heavy Industries Printing & Packaging Machinery、Electronics For Imaging、Keyence、Leibinger Group、Domino Printing Sciencesなどがあります。

産業用インクジェットプリンター業界の主要企業は、市場での地位を強化するため、顧客との直接取引に重点を置き、オーダーメードのソリューションを可能にし、メンテナンス、トレーニング、インテグレーションを含むフルサービスのパッケージを提供しています。多くの企業は、規制要件や顧客の期待に沿うよう、プリントヘッド技術、インク化学、持続可能な実践を進歩させるための研究開発に多額の投資を行っています。戦略的な提携や買収も一般的で、製品ポートフォリオを拡大し、新しい地域市場にアクセスするのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク・課題

- 機会

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 規制の枠組み

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- ポーターのファイブフォース分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ航空

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 常用インクジェット

- オンデマンドドロップ

- UVインクジェット

- その他

第6章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 食品・飲料

- 化学薬品

- 医薬品

- パッケージ

- パーソナルケア・化粧品

- その他

第7章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 間接販売

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第9章 企業プロファイル

- Brother Industries

- Canon

- Domino Printing Sciences

- Durst Phototechnik

- Electronics For Imaging

- Epson

- Fujifilm

- Hitachi Industrial Equipment Systems

- HP

- Keyence

- Konica Minolta

- Leibinger Group

- Markem-Imaje

- Mitsubishi Heavy Industries Printing &Packaging Machinery

- Videojet

The Global Industrial Inkjet Printers Market was valued at USD 6.5 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 11.5 billion by 2034. Industries such as pharmaceuticals, textiles, and packaging are significantly boosting the demand for variable data printing, particularly for real-time labeling with barcodes, dates, serial numbers, and batch codes across diverse materials. This growth is fueled by consumer expectations for product personalization, stricter regulatory standards, and brand differentiation in competitive markets.

Inkjet systems offer a flexible and cost-effective solution for high-resolution printing on short-run jobs without the need for costly retooling, which is attracting growing adoption among end-users. Furthermore, sustainability is gaining momentum, especially with the emphasis from the U.S. Environmental Protection Agency (EPA) on reducing waste and improving energy efficiency. As a result, more companies are turning to inkjet printing as an environmentally responsible and productive alternative.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 6% |

Technological advancements, especially in printhead design, digital ink formulations, and integration with Industry 4.0 platforms, are significantly enhancing the performance of inkjet printers. These improvements allow for ultra-high-resolution outputs, benefiting specialized applications like decorative packaging, film labeling, and custom materials by leveraging features such as micro-droplet control and increased pixel accuracy. Additionally, industrial inkjet technology has found a place in additive manufacturing, particularly binder jetting, which is proving to be a viable method in 3D printing across various sectors, including biomedical, aerospace, and automotive. The potential return on investment continues to increase as these machines evolve, solidifying their role in modern production environments.

The continuous inkjet (CIJ) segment accounted for USD 2.9 billion in 2024 and is expected to rise to USD 5.3 billion by 2034. This segment leads the market due to its ability to perform high-speed, non-contact printing with minimal maintenance requirements. Its durability and ability to deliver consistent output in demanding settings make it a popular choice for businesses that rely on printing variable information such as expiration dates and tracking codes on a variety of substrates. With strong adhesion properties and seamless operation even under challenging industrial conditions, CIJ systems continue to maintain a strong market position.

The direct sales segment accounted for USD 4.1 billion in 2024 and is anticipated to grow at a CAGR of 6.1% during 2025-2034. Industrial applications that demand a high degree of customization and technical complexity primarily drive this segment. Leading manufacturers such as Epson, Markem-Imaje, Domino Printing Sciences, and Videojet have strengthened their market approach by building direct relationships with clients. These companies provide personalized services, including system setup, real-time technical support, maintenance agreements, and full integration with existing workflows, ensuring long-term client retention and satisfaction.

North America Industrial Inkjet Printers Market was valued at USD 900 million in 2024 and is projected to grow at a CAGR of 6.6% between 2025 and 2034. The dominance of the U.S. stems from its well-established and technologically advanced manufacturing ecosystem. Inkjet systems are widely adopted for marking, coding, and labeling processes within various sectors such as electronics, food production, and pharmaceuticals. These systems integrate efficiently into existing automation setups, significantly boosting throughput while minimizing downtime. Ongoing research and development efforts by industry leaders continue to enhance the performance, durability, and operational efficiency of industrial inkjet technologies.

Key players shaping the competitive landscape of the Industrial Inkjet Printer Industry include Canon, Fujifilm, Durst Phototechnik, HP, Brother Industries, Konica Minolta, Epson, Hitachi Industrial Equipment Systems, Mitsubishi Heavy Industries Printing & Packaging Machinery, Electronics For Imaging, Keyence, Leibinger Group, and Domino Printing Sciences.

To strengthen their market position, leading companies in the industrial inkjet printers industry are focusing on direct client engagement, enabling tailored solutions, and offering full-service packages including maintenance, training, and integration. Many are investing heavily in R&D to advance printhead technology, ink chemistry, and sustainable practices to align with regulatory requirements and customer expectations. Strategic collaborations and acquisitions are also common, helping to expand product portfolios and access new regional markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 End use industry

- 2.2.4 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory framework

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's five forces analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 MEA

- 4.2.1.5 LATAM

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Technology, 2021-2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Continuous inkjet

- 5.3 Drop on demand

- 5.4 UV inkjet

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By End Use Industry, 2021-2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Food & beverage

- 6.3 Chemical

- 6.4 Pharmaceutical

- 6.5 Packaging

- 6.6 Personal care & cosmetics

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021-2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Direct sales

- 7.3 Indirect sales

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034, ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 The U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 South Africa

Chapter 9 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 9.1 Brother Industries

- 9.2 Canon

- 9.3 Domino Printing Sciences

- 9.4 Durst Phototechnik

- 9.5 Electronics For Imaging

- 9.6 Epson

- 9.7 Fujifilm

- 9.8 Hitachi Industrial Equipment Systems

- 9.9 HP

- 9.10 Keyence

- 9.11 Konica Minolta

- 9.12 Leibinger Group

- 9.13 Markem-Imaje

- 9.14 Mitsubishi Heavy Industries Printing & Packaging Machinery

- 9.15 Videojet