新エネルギー自動車用スタビライザーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

New Energy Vehicle Stabilizer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773335

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

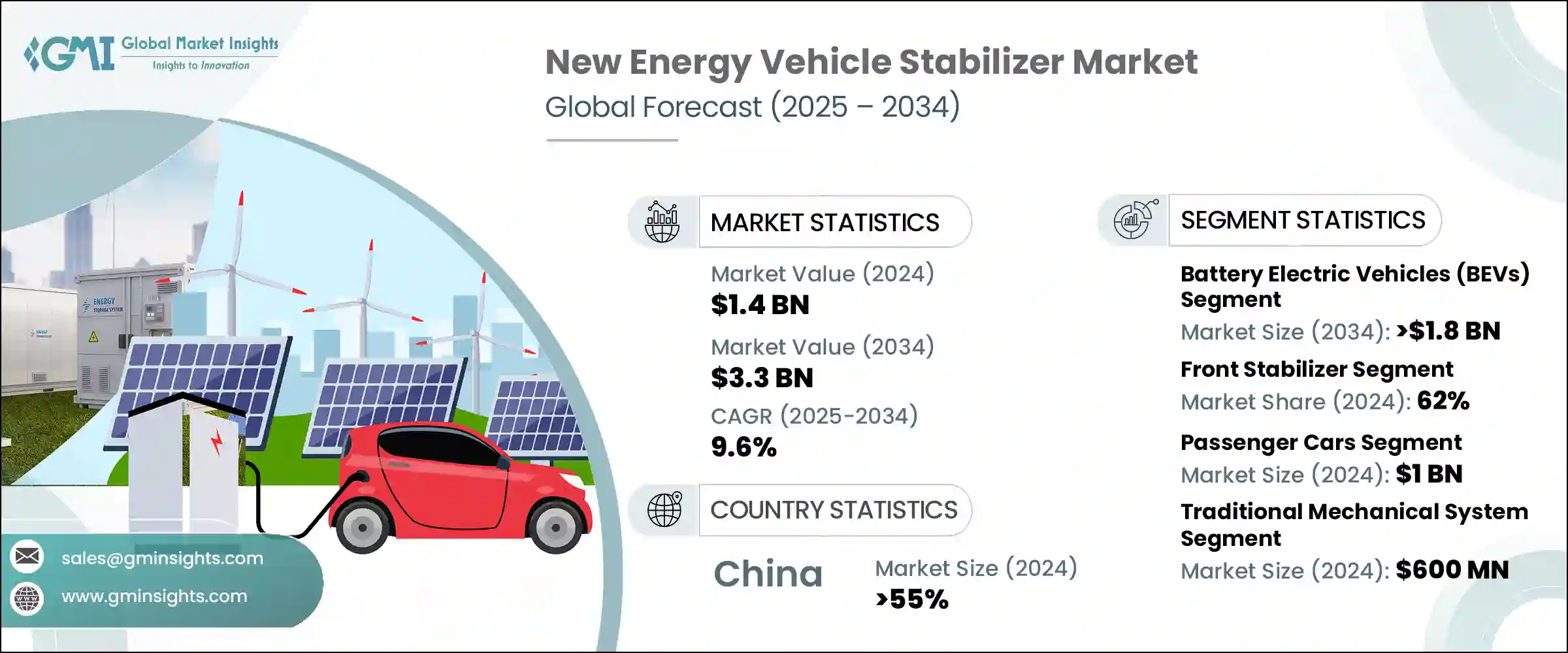

新エネルギー自動車用スタビライザーの世界市場は、2024年には14億米ドルと評価され、CAGR9.6%で成長し、2034年までには33億米ドルに達すると推定されています。

この成長は、世界の主要市場で電気自動車、ハイブリッド車、水素自動車の採用が増加していることが大きな要因となっています。メーカーが代替ドライブトレインに移行するにつれて、車両ダイナミクスと全体的な乗り心地が重視されるようになり、これが先進スタビライザー技術の需要を直接後押ししています。電気機械式スタビライザーとアクティブスタビライザーは、サスペンション性能を強化し、ボディロールを低減し、乗客とドライバーの両方にスムーズなハンドリングを提供する能力により、広く採用されるようになってきています。これは、高レベルの安全性と快適性を実現しようとするEV分野の幅広い動向を反映しています。

スタビライザー(スタビライザーバーまたはアンチロールバーと呼ばれることが多い)は、特にバッテリーの搭載によって重量配分が変化するNEVのサスペンションシステムを支える上で重要な役割を果たします。従来の内燃機関(ICE)車とは異なり、NEVはバッテリーパックを車両フロアに搭載する傾向があるため、重心が移動し、スタビライザーシステムの見直しが必要となります。これらのシステムは、特に高速走行時や急激な方向転換時に、最適な性能とコーナリング安定性を確保するように設計されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 14億米ドル |

| 予測金額 | 33億米ドル |

| CAGR | 9.6% |

バッテリー電気自動車(BEV)は、2024年に46%のシェアを占め、2034年までには18億米ドルの市場規模になると予測されています。スタビライザー市場におけるBEVの足場固めの背景には、オール電化プラットフォームに対する生産と消費者の需要の急増があります。この増加は、支持的な政策環境、充電インフラの拡大、Hyundai、Volkswagen、Tesla、BYDのような世界OEMの多額の投資によるものです。BEVのバッテリー重量が重くなると、特別に設計されたサスペンションシステムが必要となり、先進スタビライザー部品への依存度が高まります。

2024年には、フロントスタビライザーバーセグメントが世界の新エネルギー自動車用スタビライザー市場をリードし、62%のシェアを占め、2034年までのCAGRは8.2%と予測されています。この優位性は、フロントアクスルの安定性を管理し、車両バランスを維持するという重要な役割に起因しています。電気自動車は前輪駆動方式を採用することが多く、バッテリーの質量が前車軸に集中するため、フロントスタビライザーは、リアルタイムの運転状況で正確なハンドリングを確保し、車体の動きを抑えるために不可欠なものとなっています。

アジア太平洋の新エネルギー自動車用スタビライザー市場は55%のシェアを占め、2024年には3億米ドルを創出しました。NEV製造の急速な加速による持続的な規制支援と国内需要の増加が、この成長の主な促進要因です。中国は世界最大のNEV市場としての地位を確立しており、その地位は積極的な国家戦略と投資によって強化されています。NIO、XPeng、BYD、Geelyなどの地元ブランドや、Tesla、Volkswagenなどの世界自動車メーカーは、急増する需要に対応するため、この地域での生産拠点を拡大し続けています。

新エネルギー自動車用スタビライザー市場で事業を展開している主要企業には、Sogefi Group、Thyssenkrupp、DAEWON、ZF、Dongfeng、NHK International、SwayTec、Hendrickson、Kongsberg Automotive、Mubeaなどがあります。NEV用スタビライザーセグメントに属する企業は、次世代EVプラットフォームの革新と統合を積極的に追求しています。その多くは、進化する電動ドライブトレインのダイナミクスに適合する、より軽量で高強度のスタビライザー部品を開発するための研究開発に投資しています。EVメーカーと協力して初期段階から設計に関与することで、カスタマイズされたサスペンションシステムが可能になります。企業はまた、オンボードのセンサーや制御ユニットと連動してリアルタイムで性能を発揮する適応技術や電気機械技術も取り入れています。地域に根ざした生産拠点やOEMとの長期的なサプライヤー契約を通じて世界に展開することで、これらのプレーヤーは市場への参入を強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 原材料サプライヤー

- 部品メーカー

- テクノロジープロバイダー

- アフターマーケットサプライヤー

- システムインテグレーター

- コスト構造

- 利益率

- 各段階での付加価値

- サプライチェーンに影響を与える要因

- 破壊者

- サプライヤーの情勢

- 影響要因

- 促進要因

- 電気自動車とハイブリッド車に対する政府の義務と消費者の需要の増加

- NEVにおける乗り心地制御とハンドリング性能の向上に対する需要

- 機械式スタビライザーからインテリジェントなセンサー統合型スタビライザーへの移行

- 適応型および切断型スタビライザーシステムの必要性の増加

- 業界の潜在的リスク・課題

- 特に電気機械および能動システム

- スペースの制約によるパッケージングの課題

- 市場機会

- 電動オフロード車におけるパフォーマンスパーツとカスタマイズの成長

- 無線(OTA)スタビライザーのチューニングと制御ソリューションへの扉を開く

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術

- 新興技術

- 特許分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 持続可能性分析

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- バッテリー電気自動車(BEV)

- プラグインハイブリッド電気自動車(PHEV)

- ハイブリッド電気自動車(HEV)

- 燃料電池電気自動車(FCEV)

第6章 市場推計・予測:スタビライザー、2021年~2034年

- 主要動向

- フロントスタビライザー

- リアスタビライザー

第7章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 油圧スタビライザーシステム

- 電気機械式スタビライザーシステム

- 電子制御スタビライザーバー

- 伝統的な機械システム

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV

- MUV

- 商用車

- 小型商用車

- 中型商用車

- 大型商用車

第9章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ウクライナ

- ロシア

- ノルディック

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- チリ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- AAM

- ADDCO

- Chuo Spring

- DAEWON

- Dongfeng

- JAMNA AUTO INDUSTRIES LIMITED

- Sogefi Group

- Kongsberg Automotive

- Mubea

- NHK International

- Hendrickson

- Sogefi

- SwayTec

- Tata

- Thyssenkrupp

- Tinsley Bridge

- TMT(CSR)

- Tower

- Wanxiang

- Yangzhou Dongsheng

- ZF

目次

The Global New Energy Vehicle Stabilizer Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 9.6% to reach USD 3.3 billion by 2034. This growth is largely fueled by the increasing adoption of electric, hybrid, and hydrogen-powered vehicles across major global markets. As manufacturers shift to alternative drivetrains, there is a rising emphasis on vehicle dynamics and overall ride quality, which directly boosts the demand for advanced stabilizer technologies. Electromechanical and active stabilizers are becoming more widely adopted due to their ability to enhance suspension performance, reduce body roll, and provide smoother handling for both passengers and drivers. This reflects a broader trend in the EV sector to deliver high levels of safety and comfort.

Stabilizers-often called sway or anti-roll bars-play a crucial role in supporting the suspension systems of NEVs, especially given the altered weight distribution brought on by battery placement. Unlike conventional internal combustion engine (ICE) vehicles, NEVs tend to house battery packs on the vehicle floor, shifting the center of gravity and requiring reimagined stabilizer systems. These systems are designed to ensure optimal performance and cornering stability, particularly during high-speed maneuvers or rapid direction changes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 9.6% |

Battery Electric Vehicles (BEVs) commanded a 46% share in 2024, and the segment is anticipated to generate USD 1.8 billion by 2034. The strong foothold of BEVs in the stabilizer market is backed by surging production and consumer demand for all-electric platforms. This increase is due to supportive policy environments, expanded charging infrastructure, and significant investment from global OEMs like Hyundai, Volkswagen, Tesla, and BYD. Heavier battery weights in BEVs necessitate specially engineered suspension systems, increasing the reliance on advanced stabilizer components.

In 2024, the front stabilizer bars segment led the global new energy vehicle stabilizer market, accounting for 62% share, and is forecasted to grow at a CAGR of 8.2% through 2034. This dominance stems from their critical role in managing front-axle stability and maintaining vehicle balance. As electric vehicles frequently adopt front-wheel drive configurations and concentrate battery mass on the front axle, front stabilizers have become indispensable in ensuring precise handling and reduced body movement in real-time driving conditions.

Asia Pacific New Energy Vehicle Stabilizer Market held a 55% share and generated USD 300 million in 2024. The rapid acceleration of NEV manufacturing sustained regulatory support, and increasing domestic demand are key drivers of this growth. China has established itself as the largest NEV market worldwide, a position reinforced by aggressive national strategies and investment. Local brands like NIO, XPeng, BYD, and Geely, as well as global automakers such as Tesla and Volkswagen, have continued to expand their production footprints in the region to meet this surging demand.

Leading players operating in the New Energy Vehicle Stabilizer Market include Sogefi Group, Thyssenkrupp, DAEWON, ZF, Dongfeng, NHK International, SwayTec, Hendrickson, Kongsberg Automotive, and Mubea. Companies in the NEV stabilizer segment are aggressively pursuing innovation and integration with next-gen EV platforms. Most are investing in R&D to develop lighter, high-strength stabilizer components that match the evolving dynamics of electric drivetrains. Collaborations with EV manufacturers for early-stage design involvement allow for customized suspension systems. Firms are also incorporating adaptive and electromechanical technologies that work with onboard sensors and control units for real-time performance. Global expansion through localized production hubs and long-term supplier agreements with OEMs helps these players strengthen their market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Stabilizer

- 2.2.4 Technology

- 2.2.5 Application

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component manufacturers

- 3.1.1.3 Technology providers

- 3.1.1.4 Aftermarket suppliers

- 3.1.1.5 System integrators

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing government mandates and consumer demand for electric and hybrid vehicles

- 3.2.1.2 Demand for enhanced ride control and handling performance in NEVs

- 3.2.1.3 Shift from mechanical to intelligent, sensor-integrated stabilizers

- 3.2.1.4 Increased need for adaptive and disconnecting stabilizer systems

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Especially electromechanical and active systems

- 3.2.2.2 Packaging challenges due to space constraints

- 3.2.3 Market Opportunities

- 3.2.3.1 Growth in performance parts and customization in electric off-road vehicles

- 3.2.3.2 Opens door for over-the-air (OTA) stabilizer tuning and control solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology & innovation landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.8.1 North America

- 3.8.2 Europe

- 3.8.3 Asia Pacific

- 3.8.4 Latin America

- 3.8.5 Middle East & Africa

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Sustainability analysis

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Battery Electric Vehicles (BEVs)

- 5.3 Plug-in Hybrid Electric Vehicles (PHEVs)

- 5.4 Hybrid Electric Vehicles (HEVs)

- 5.5 Fuel Cell Electric Vehicles (FCEVs)

Chapter 6 Market Estimates & Forecast, By Stabilizer, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Front Stabilizer

- 6.3 Rear Stabilizer

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Hydraulic stabilizer system

- 7.3 Electromechanical stabilizer system

- 7.4 Electronically controlled stabilizer bar

- 7.5 Traditional mechanical system

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.1.1 Passenger Car

- 8.1.2 Sedan

- 8.1.3 Hatchback

- 8.1.4 SUV

- 8.1.5 MUV

- 8.2 Commercial Vehicle

- 8.2.1 Light Commercial Vehicle

- 8.2.2 Medium Commercial Vehicle

- 8.2.3 Heavy Commercial Vehicle

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 North America

- 10.1.1 U.S.

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Ukraine

- 10.2.7 Russia

- 10.2.8 Nordic

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 South Korea

- 10.3.6 Southeast Asia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.4.4 Chile

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 AAM

- 11.2 ADDCO

- 11.3 Chuo Spring

- 11.4 DAEWON

- 11.5 Dongfeng

- 11.6 JAMNA AUTO INDUSTRIES LIMITED

- 11.7 Sogefi Group

- 11.8 Kongsberg Automotive

- 11.9 Mubea

- 11.10 NHK International

- 11.11 Hendrickson

- 11.12 Sogefi

- 11.13 SwayTec

- 11.14 Tata

- 11.15 Thyssenkrupp

- 11.16 Tinsley Bridge

- 11.17 TMT(CSR)

- 11.18 Tower

- 11.19 Wanxiang

- 11.20 Yangzhou Dongsheng

- 11.21 ZF

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日