|

市場調査レポート

商品コード

1773329

自動車用電動油圧式パワーステアリングポンプの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Automotive Electro-Hydraulic Power Steering Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用電動油圧式パワーステアリングポンプの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月16日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

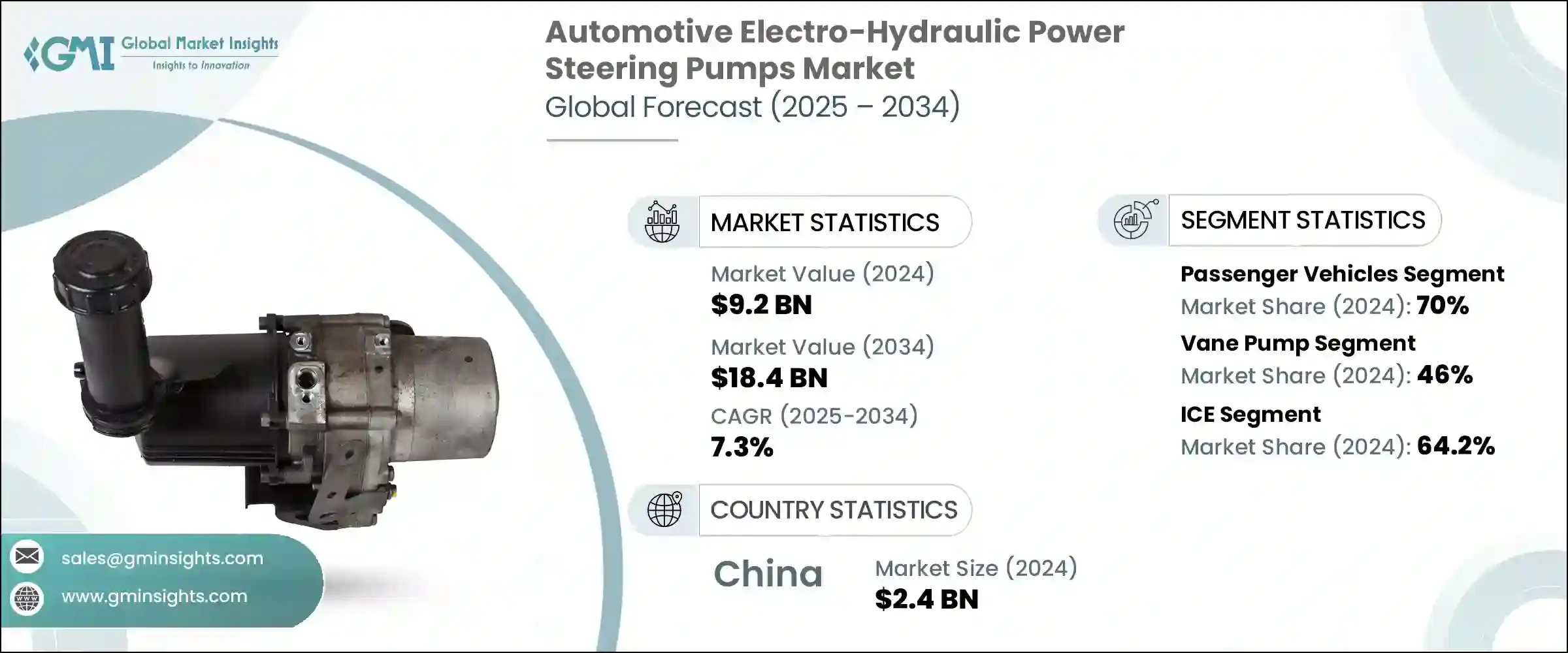

自動車用電動油圧式パワーステアリングポンプの世界市場規模は、2024年に92億米ドルとなり、CAGR7.3%で成長し、2034年までには184億米ドルに達すると予測されています。

この力強い成長は、世界の省燃費・低排出ガス車へのシフトによって推進されています。自動車メーカーが北米、欧州、中国などの地域でますます厳しくなる環境規制に対応することを目指しているため、EHPSシステムは不可欠なものとなりつつあります。従来の油圧ステアリングとは異なり、EHPSテクノロジーはエンジンから独立して作動し、必要なときだけ作動します。そのため、エンジン抵抗が大幅に削減され、燃料使用量も少なくなります。その適応性の高い構造により、ハイブリッド車やマイルドハイブリッド車に強く適合します。このシステムは、ハイブリッド運転で一般的な内燃エンジン停止時でも完全なステアリング機能を維持するため、完全な電動ステアリングシステムに代わる費用対効果の高いシステムとなっています。

自動車メーカーが高度な運転支援機能を自動車に搭載するようになるにつれ、より応答性の高い、電子制御されたステアリング入力が求められるようになっています。EHPSシステムは、代替パワートレインを搭載した車両であっても、安全性と精度を確保しながらこのニーズに応えます。車線中央維持や衝突回避のような自動化技術をサポートするEHPSの能力は、自動車カテゴリー全体へのEHPSの普及を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 92億米ドル |

| 予測金額 | 184億米ドル |

| CAGR | 7.3% |

乗用車セグメントが70%のシェアを占め、2034年までのCAGRは7.5%と予想されます。このセグメントは生産と需要の両面で規模が大きいため、EHPSの成長に大きく寄与しています。より良いハンドリング、洗練された乗り心地、安全な運転体験に対する消費者の期待の高まりが、自動車メーカーがEHPSシステムをより広範囲に統合する動機となっています。特にハイブリッド車や電気乗用車は、システムの互換性と省エネルギーの可能性から恩恵を受けており、メーカーが幅広いモデルでEHPSを使用することを後押ししています。

ベーンポンプ技術セグメントは2024年に46%のシェアを占め、2034年までCAGR8%で成長すると予測されています。これらのポンプは、作動油の流れを一定に保ち、安定した正確なステアリングフィードバックを保証する能力で好まれています。その設計は、ポンプハウジングと常に接触しているスライディングベーンを特徴としており、スムーズな性能と優れたドライバーコントロールを実現しています。ベーンポンプはまた、静かな作動音と低い脈動が評価され、車内の快適性と洗練された音響を重視する車両設計に適しています。

中国の自動車用電動油圧式パワーステアリングポンプ市場は2024年に24億米ドルと評価され、シェアは67%を占めました。同国では、ハイブリッドシステムやエネルギー意識の高い自動車技術の導入が加速しており、国内外の自動車ブランドでEHPSシステムの需要が高まっています。48Vハイブリッドプラットフォームの普及に伴い、EHPSソリューションの統合が広がっています。グローバルTier-1サプライヤーと地元企業の両方が研究開発および地域化された製造に多額の投資を行っているため、重要な生産および技術革新のハブとしての中国の地位はさらに強化されています。ADASの採用とインテリジェントステアリング技術の急増も、プレミアム車と中級車のカテゴリーにおけるEHPSの導入を後押ししています。

世界の自動車用電動油圧式パワーステアリングポンプ市場に積極的に参入している主要企業には、Delphi Technologies、ZF Friedrichshafen、Robert Bosch、Nexteer Automotive、Mitsubishi Electric、GKN Automotive、JTEKT、NSK Ltd.、Hyundai Mobis、Tennecoなどがあります。自動車用EHPS市場における競争力を強化するため、各企業はイノベーション主導の成長と戦略的パートナーシップを追求しています。その多くは、OEMの要件を満たすEHPSユニットのエネルギー効率、サイズ、統合の柔軟性を高めるため、研究開発に多額の投資を行っています。また、中国のような急成長経済圏での市場参入を最適化するため、現地企業と合弁会社を設立している企業もあります。現地生産とコスト削減のために製造工程を合理化することも顕著な戦略です。各社はまた、48Vプラットフォームなどの高電圧アーキテクチャをサポートするシステムで製品ポートフォリオを拡大しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 燃費効率の高いステアリングシステムの需要増加

- パワートレインアーキテクチャの電動化の急増

- 先進運転支援システム(ADAS)との統合の進展

- 小型商用車(LCV)の販売増加

- 新興市場における自動車生産の拡大

- 業界の潜在的リスク・課題

- 従来の油圧ポンプに比べてシステムコストが高め

- 限定的な完全電気自動車アーキテクチャとの互換性

- 市場機会

- ハイブリッド車とマイルドハイブリッド車の普及増加

- 小型商用車(LCV)セグメントの拡大

- 現地生産と地域生産の拡大

- 戦略的パートナーシップと合弁事業による成長

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第6章 市場推計・予測:ポンプ別、2021年~2034年

- 主要動向

- ベーンポンプ

- ギアポンプ

- ピストンポンプ

- その他

第7章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第8章 市場推計・予測:推進力別、2021年~2034年

- 主要動向

- ICE

- 電気自動車(EV)

- ハイブリッド

第9章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ポンプユニット

- 貯水池

- パワーステアリングフルード

- 制御ユニット

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Alltech Automotive

- Cardone Industries

- Delphi Technologies

- GDST Auto Parts

- GKN Automotive

- Hitachi Astemo

- Hyundai Mobis

- JTEKT

- Kartek

- MAPCO Autotechnik

- Maval Manufacturing

- Mitsubishi Electric

- Nexteer Automotive

- NSK Ltd.

- Robert Bosch

- SEAT

- Sheppard Steering

- Tenneco

- Turn One Steering

- ZF Friedrichshafen

The Global Automotive Electro-Hydraulic Power Steering Pumps Market was valued at USD 9.2 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 18.4 billion by 2034. This strong growth is being propelled by the worldwide shift toward fuel-saving and low-emission vehicles. As vehicle manufacturers aim to meet increasingly strict environmental mandates in regions like North America, Europe, and China, EHPS systems are becoming essential. Unlike conventional hydraulic steering, EHPS technology operates independently from the engine, turning on only when needed. This significantly cuts engine drag and lowers fuel use. Its adaptable structure makes it a strong fit for hybrid and mild hybrid vehicles. The system retains full steering capability even when the internal combustion engine is turned off-a common condition in hybrid operations, making it a cost-effective alternative to full electric steering systems.

As automakers increasingly build advanced driver assistance features into vehicles, they require more responsive and electronically controlled steering inputs. EHPS systems meet this need while ensuring safety and precision, even in vehicles with alternative powertrains. Their ability to support automated technologies such as lane centering and collision avoidance is driving their widespread adoption across vehicle categories.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.2 Billion |

| Forecast Value | $18.4 Billion |

| CAGR | 7.3% |

The passenger vehicles segment held a 70% share and is expected to grow at a CAGR of 7.5% through 2034. The segment's scale in both production and demand makes it a major contributor to EHPS growth. Rising consumer expectations for better handling, refined ride quality, and safe driving experiences are motivating automakers to integrate EHPS systems more extensively. Hybrid and electric passenger vehicles, in particular, benefit from the system's compatibility and energy-saving potential, encouraging manufacturers to use EHPS across a wide spectrum of models.

The vane pump technology segment accounted for 46% share in 2024 and is projected to grow at a CAGR of 8% through 2034. These pumps are preferred for their ability to maintain a consistent flow of hydraulic fluid, ensuring steady and precise steering feedback. Their design features sliding vanes that stay in constant contact with the pump housing, delivering smooth performance and superior driver control. Vane pumps are also valued for their quiet operation and low pulsation, making them a preferred choice in vehicle designs that emphasize cabin comfort and acoustic refinement.

China Automotive Electro-Hydraulic Power Steering Pumps Market generated USD 2.4 billion in 2024 and held a 67% share. The country's accelerated adoption of hybrid systems and energy-conscious automotive technologies has pushed demand for EHPS systems across both domestic and international car brands. With a growing push for 48V hybrid platforms, EHPS solutions are seeing widespread integration. China's position as a key production and innovation hub is further reinforced by heavy investments from both global Tier-1 suppliers and local companies in research, development, and regionalized manufacturing. The surge in ADAS adoption and intelligent steering technologies is also bolstering EHPS implementation across premium and mid-tier vehicle categories.

Major companies actively participating in the Global Automotive Electro-Hydraulic Power Steering Pumps Market include Delphi Technologies, ZF Friedrichshafen, Robert Bosch, Nexteer Automotive, Mitsubishi Electric, GKN Automotive, JTEKT, NSK Ltd., Hyundai Mobis, and Tenneco. To strengthen their competitive edge in the automotive EHPS market, companies are pursuing innovation-led growth and strategic partnerships. Many are investing heavily in R&D to enhance the energy efficiency, size, and integration flexibility of EHPS units meeting OEM requirements. Others are forming joint ventures with local players to optimize market reach in fast-growing economies like China. Streamlining manufacturing processes to localize production and reduce costs is another prominent strategy. Companies are also expanding their product portfolios with systems that support higher-voltage architectures like 48V platforms.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Technology

- 2.2.4 Suspension

- 2.2.5 Sales channel

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for fuel-efficient steering systems

- 3.2.1.2 Surge in electrification of powertrain architectures

- 3.2.1.3 Rising integration with advanced driver-assistance systems (ADAS)

- 3.2.1.4 Increasing sales of light commercial vehicles (LCVs)

- 3.2.1.5 Expansion of vehicle production in emerging markets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system cost compared to traditional hydraulic pumps

- 3.2.2.2 Limited compatibility with fully electric vehicle architectures

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of hybrid and mild-hybrid vehicles

- 3.2.3.2 Expansion of the light commercial vehicle (LCV) segment

- 3.2.3.3 Localized manufacturing and regional production expansion

- 3.2.3.4 Growth through strategic partnerships and joint ventures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchbacks

- 5.2.2 Sedans

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light commercial vehicles (LCV)

- 5.3.2 Medium commercial vehicles (MCV)

- 5.3.3 Heavy commercial vehicles (HCV)

Chapter 6 Market Estimates & Forecast, By Pump, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Vane pump

- 6.3 Gear pump

- 6.4 Piston pump

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Sales channel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 OEMs

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Propulsions, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 ICE

- 8.3 Electric Vehicles (EVs)

- 8.4 Hybrid

Chapter 9 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Pump unit

- 9.3 Reservoir

- 9.4 Power steering fluid

- 9.5 Control unit

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Alltech Automotive

- 11.2 Cardone Industries

- 11.3 Delphi Technologies

- 11.4 GDST Auto Parts

- 11.5 GKN Automotive

- 11.6 Hitachi Astemo

- 11.7 Hyundai Mobis

- 11.8 JTEKT

- 11.9 Kartek

- 11.10 MAPCO Autotechnik

- 11.11 Maval Manufacturing

- 11.12 Mitsubishi Electric

- 11.13 Nexteer Automotive

- 11.14 NSK Ltd.

- 11.15 Robert Bosch

- 11.16 SEAT

- 11.17 Sheppard Steering

- 11.18 Tenneco

- 11.19 Turn One Steering

- 11.20 ZF Friedrichshafen