光ファイバージャイロスコープの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Fiber Optics Gyroscope Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773318

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

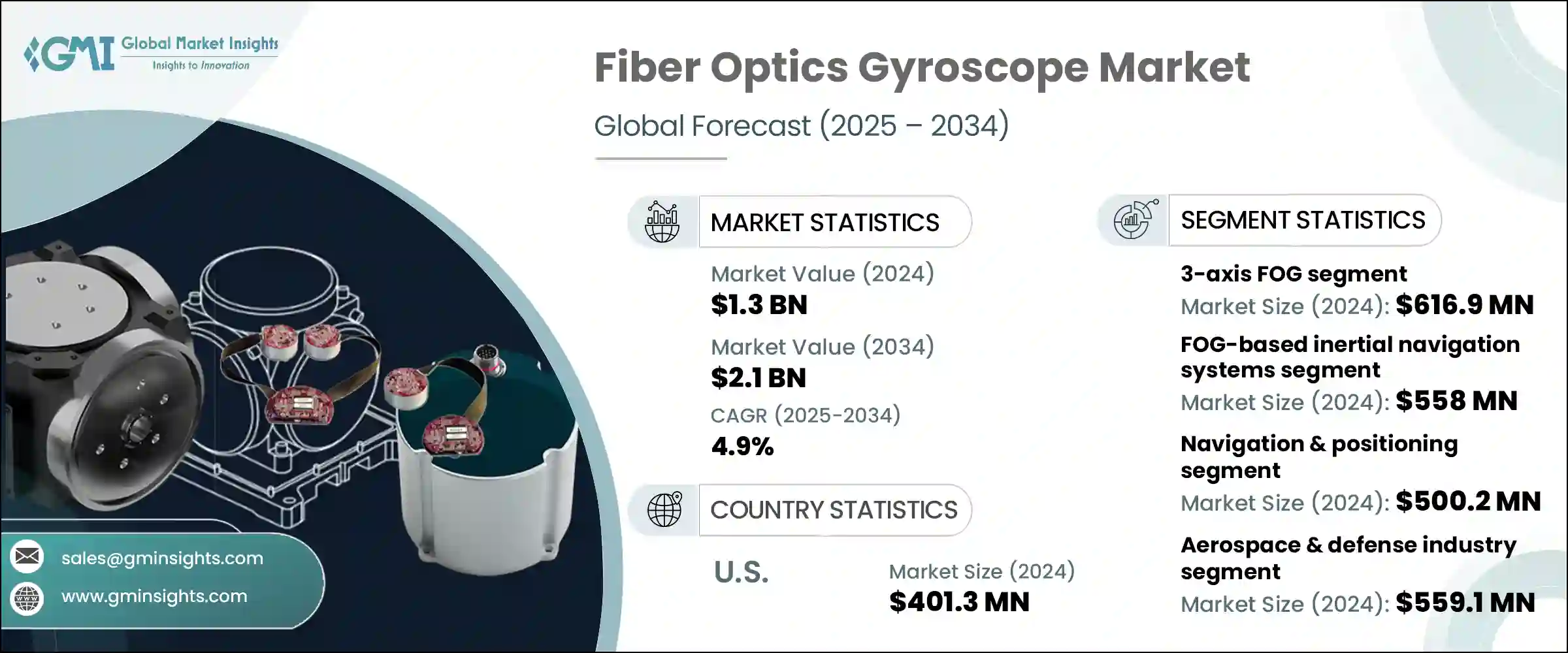

光ファイバージャイロスコープの世界市場規模は、2024年に13億米ドルとなり、CAGR4.9%で成長し、2034年までには21億米ドルに達すると予測されています。

この成長は、自律移動の急速な進展とともに、防衛および航空宇宙アプリケーションからの需要増加の影響を強く受けています。光ファイバジャイロ(FOGs)は、リングレーザやMEMSジャイロのような代替品に比べ、特に繊細な防衛環境において明確な利点を提供します。可動部品なしで動作し、電磁干渉の影響を受けず、より高い精度と長期的な安定性を実現するため、ミッションクリティカルなシステムに理想的であり、市場の持続的な需要を確実なものにしています。

成長に大きく寄与しているのは、自動運転車や無人航空機を含む自律走行車の拡大です。これらのプラットフォームでは、GPS信号が故障する可能性がある状況でも、信頼性の高い方位とナビゲーションのデータが必要です。FOGの耐振動性、高精度、フェイルセーフ設計は、このような使用事例に不可欠です。MEMSジャイロスコープは低コストのニーズに応えることが多いですが、FOGは信頼性と冗長性を必要とするアプリケーションのプレミアムスタンダードであり続けています。企業は、拡張性のある全天候型機能をサポートし、セーフティクリティカルなシステムのリスクを低減するために、FOGアシストナビゲーションへの投資を増やしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 13億米ドル |

| 予測金額 | 21億米ドル |

| CAGR | 4.9% |

2024年には、3軸FOGセグメントは6億1,690万米ドルを生み出しました。これらのシステムは、重量とサイズを削減するコンパクトな設計で、X、Y、Z軸センシングを統合しています。これは、ミサイル、UAV、自律走行車、次世代飛行システムへの展開に有利です。防衛組織が極超音速および先進航空宇宙プラットフォームで多軸ナビゲーションを優先するにつれ、3軸FOGはより不可欠になっています。電動垂直離着陸機や自律型ドローンの台頭も、その高度安定性と精密な制御により、これらのソリューションへの需要を加速させています。初期コストはかかるものの、複数の単軸ジャイロに比べて長期的なメンテナンスコストの削減が可能なため、引き続き採用が進んでいます。

FOGベースの慣性航法システムセグメントは、2024年に5億5,800万米ドルを生み出しました。これらのシステムは、GPSが信頼できなかったり、危うかったりする環境では重要です。軍用機、水中船舶、ミサイルシステムは、妨害に強く長時間航行できるFOGベースのINSに依存しています。この需要は商業分野にも及んでおり、都市型自律走行車、ロジスティクスドローン、スマートエアモビリティソリューションでは、トンネルや街並みのような障害物環境での測位にFOGが使用されています。

ドイツの光ファイバージャイロスコープ市場は2024年に7,340万米ドルと評価されました。堅調な自動車製造業と産業オートメーション部門が主要な牽引役となっています。FOGは高精度のモーションセンシングが可能なため、ADAS開発や自律走行車の研究開発プログラムに採用されています。さらに、航空宇宙・防衛製造におけるドイツの強い存在感と、先進ナビゲーション技術の開発に注力する国内企業が、この市場におけるドイツの足跡拡大を支えています。

主な市場プレーヤーは、iMAR Navigation、KVH Industries、SkyMEMS、Optolink、Tamagawa Seiki、Advanced Navigation、Emcore、Exail、Safran、Mostatech、Northrop Grumman Litef、Cielo Inertial Solutions、Honeywell International、Nedaero Componentsなどです。光ファイバージャイロスコープ市場の主要企業は、技術革新、製品の差別化、長期防衛契約の融合に注力し、市場での存在感を高めています。多くの企業が研究開発に多額の投資を行い、安定性と精度を高めた、より軽量でコンパクトな多軸FOGユニットを開発しています。政府機関や民間の防衛請負業者との戦略的パートナーシップは、リピートビジネスの確保に役立っています。また、防衛予算が増加している地域で製造拠点を拡大している企業もあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 防衛・航空宇宙分野の需要増加

- 自動運転車の拡大

- 石油・ガス探査の成長

- FOG技術の進歩

- 宇宙探査活動の増加

- 業界の潜在的リスク・課題

- 高い製造コスト

- 代替技術からの競合

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 将来の市場動向

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新たなビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 消費者感情分析

- 特許および知的財産分析

- 地政学と貿易のダイナミクス

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- 市場集中分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- チャレンジャー

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展、2021年~2024年

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:軸タイプ別、2021年~2034年

- 主要動向

- 1軸FOG

- 2軸FOG

- 3軸FOG

第6章 市場推計・予測:デバイス別、2021年~2034年

- 主要動向

- FOGベースのジャイロコンパス

- FOGベースの慣性計測ユニット

- FOGベースの慣性航法システム

- FOGベースの姿勢方位基準システム

- その他

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- ナビゲーションとポジショニング

- 安定化システム

- ロボット工学と自動化

- 誘導システム

- その他

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 航空宇宙・防衛

- 自動車

- 海洋・海中

- 石油・ガス

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Advanced Navigation

- Cielo Inertial Solutions

- Emcore

- Exail

- Honeywell International

- iMAR Navigation

- KVH Industries

- Mostatech

- Nedaero Components

- Northrop Grumman Litef

- Optolink

- Safran

- SkyMEMS

- Tamagawa Seiki

目次

The Global Fiber Optics Gyroscope Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 2.1 billion by 2034. This growth is strongly influenced by increased demand from defense and aerospace applications, along with rapid strides being made in autonomous mobility. Fiber optics gyroscopes (FOGs) offer distinct advantages over alternatives like ring laser and MEMS gyroscopes, particularly in sensitive defense environments. They operate without moving parts, are immune to electromagnetic interference, and deliver greater accuracy and long-term stability-making them ideal for mission-critical systems and ensuring sustained market demand.

A significant contributor to growth is the expanding autonomous vehicle landscape, including self-driving cars and unmanned aerial vehicles. These platforms require dependable orientation and navigation data in conditions where GPS signals may fail. The vibration resistance, high accuracy, and fail-safe design of FOGs make them indispensable in such use cases. While MEMS gyroscopes often serve low-cost needs, FOGs remain the premium standard for applications requiring reliability and redundancy. Companies are increasingly investing in FOG-assisted navigation to support scalable, all-weather functionality and to reduce risk in safety-critical systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.1 Billion |

| CAGR | 4.9% |

In 2024, the 3-axis FOG segment generated USD 616.9 million. These systems offer integrated X, Y, and Z-axis sensing within a compact design that reduces weight and size. This benefits deployment in missiles, UAVs, autonomous vehicles, and next-gen flight systems. As defense organizations prioritize multi-axis navigation in hypersonic and advanced aerospace platforms, 3-axis FOGs are becoming more essential. The rise of electric vertical takeoff and landing aircraft and autonomous drones is also accelerating demand for these solutions, due to their altitude stability and precise control. Despite their upfront cost, the long-term reduction in maintenance costs compared to multiple single-axis gyros continues to drive adoption.

The FOG-based inertial navigation systems segment generated USD 558 million in 2024. These systems are critical in environments where GPS is unreliable or compromised. Military-grade aircraft, underwater vessels, and missile systems rely on FOG-based INS for jam-resistant and long-duration navigation performance. This demand also extends to the commercial sector, where urban autonomous vehicles, logistics drones, and smart air mobility solutions use FOGs for positioning in obstructed environments like tunnels or cityscapes.

Germany Fiber Optics Gyroscope Market was valued at USD 73.4 million in 2024. The nation's robust automotive manufacturing and industrial automation sectors are key drivers. FOGs are being adopted in ADAS development and autonomous vehicle R&D programs for their high-precision motion sensing. Additionally, Germany's strong presence in aerospace and defense manufacturing, along with domestic companies focused on developing advanced navigation technologies, supports the country's expanding footprint in this market.

Prominent market players include iMAR Navigation, KVH Industries, SkyMEMS, Optolink, Tamagawa Seiki, Advanced Navigation, Emcore, Exail, Safran, Mostatech, Northrop Grumman Litef, Cielo Inertial Solutions, Honeywell International, and Nedaero Components. Leading companies in the fiber optics gyroscope market focus on a blend of innovation, product differentiation, and long-term defense contracts to build their market presence. Many invest heavily in R&D to develop lighter, more compact multi-axis FOG units with enhanced stability and precision, making them suitable for integration into advanced aerospace, naval, and autonomous platforms. Strategic partnerships with government agencies and private defense contractors help secure repeat business. Some firms are also expanding their manufacturing footprint in regions with rising defense budgets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Axis type trends

- 2.2.2 Device trends

- 2.2.3 Application trends

- 2.2.4 End use Industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO Perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical Success Factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand in defense & aerospace

- 3.2.1.2 Expansion of autonomous vehicles

- 3.2.1.3 Growth in oil & gas exploration

- 3.2.1.4 Advancements in FOG technology

- 3.2.1.5 Rising space exploration activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing costs

- 3.2.2.2 Competition from alternative technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Pricing strategies

- 3.11 Emerging business models

- 3.12 Compliance requirements

- 3.13 Sustainability measures

- 3.14 Consumer sentiment analysis

- 3.15 Patent and IP analysis

- 3.16 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Axis Type, 2021 – 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 1-Axis FOG

- 5.3 2-Axis FOG

- 5.4 3-Axis FOG

Chapter 6 Market Estimates and Forecast, By Device, 2021 – 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 FOG-based gyrocompass

- 6.3 FOG-based inertial measurement unit

- 6.4 FOG-based inertial navigation system

- 6.5 FOG-based attitude heading reference system

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Navigation & positioning

- 7.3 Stabilization systems

- 7.4 Robotics & automation

- 7.5 Guidance system

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 Aerospace & defense

- 8.3 Automotive

- 8.4 Marine & subsea

- 8.5 Oil & gas

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Advanced Navigation

- 10.2 Cielo Inertial Solutions

- 10.3 Emcore

- 10.4 Exail

- 10.5 Honeywell International

- 10.6 iMAR Navigation

- 10.7 KVH Industries

- 10.8 Mostatech

- 10.9 Nedaero Components

- 10.10 Northrop Grumman Litef

- 10.11 Optolink

- 10.12 Safran

- 10.13 SkyMEMS

- 10.14 Tamagawa Seiki

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日