アルミハニカムパネルの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Aluminum Honeycomb Panels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773313

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

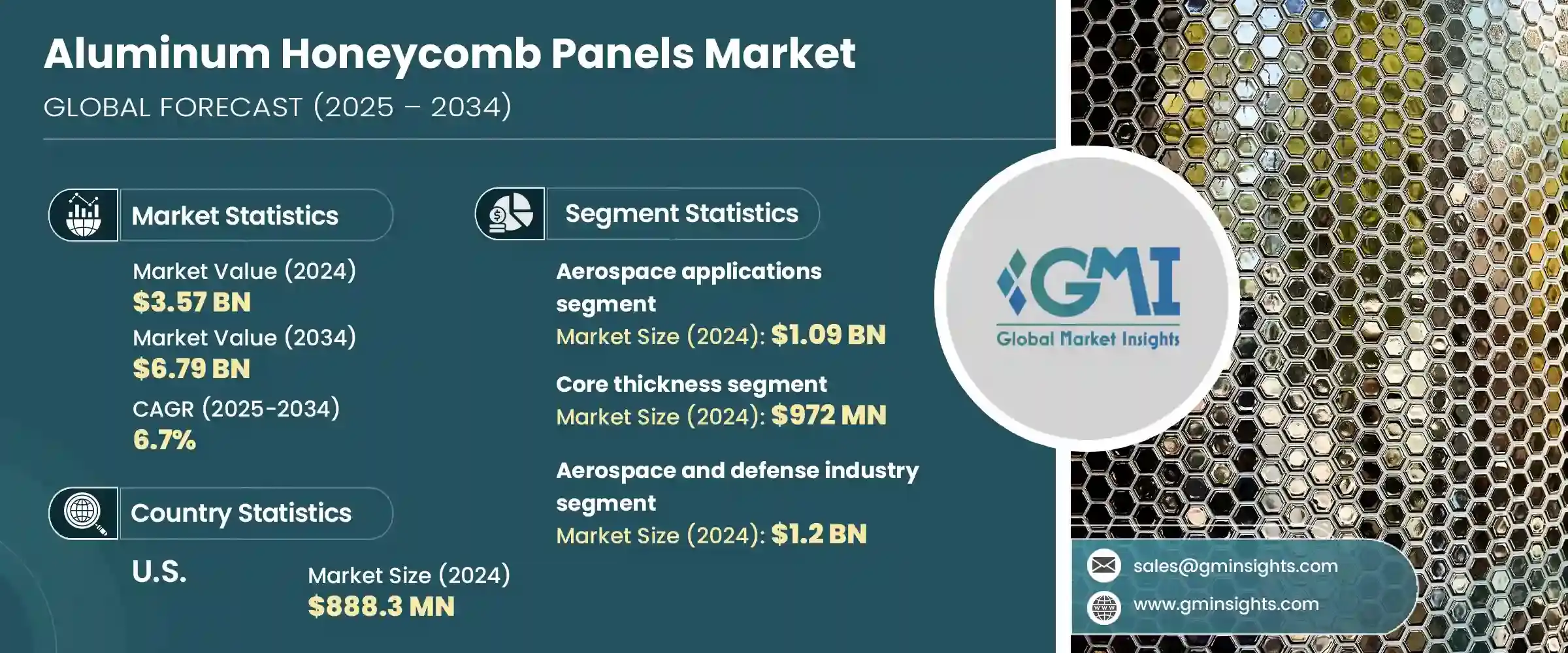

アルミハニカムパネルの世界市場規模は2024年に35億7,000万米ドルとなり、CAGR6.7%で成長し、2034年までには67億9,000万米ドルに達すると予測されています。

この成長は主に、強度と低重量を組み合わせた材料を必要とする複数の高性能産業にわたる用途の増加によってもたらされます。この需要は、航空宇宙、自動車、建設、工業製造など、性能効率と構造的完全性が鍵となる分野で特に顕著です。これらのパネルは、構造物の重量を大幅に増加させることなく、エネルギー吸収、耐久性、様々な応力に対する耐性に関する厳しい要件を満たす能力が広く認められています。

産業界が省エネルギーと持続可能性の目標を追求し続ける中、軽量でありながら堅牢な素材への需要が高まっており、アルミハニカムパネルは理想的なソリューションとなっています。近代的なインフラ、輸送システム、特殊機器のハウジングにこれらの素材を使用する傾向が高まっていることも、世界の市場におけるアルミハニカムパネルの重要性の高まりを裏付けています。リサイクル性、耐火性、断熱性によりその魅力はさらに増し、機能性と環境への配慮の両方が求められる幅広い用途に適しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 35億7,000万米ドル |

| 予測金額 | 67億9,000万米ドル |

| CAGR | 6.7% |

航空宇宙分野では、アルミハニカムパネルは軽量で高強度といった必須条件を満たすため、急速に普及しています。航空宇宙用途分野だけで、2024年には10億9,000万米ドルと評価され、2025年から2034年までのCAGRは7.5%を記録すると予測されています。これらのパネルは、燃費効率を高め、航空製造において重要な設計の柔軟性を向上させるのに役立ちます。その用途は、性能を損なうことなく軽量化を図ることが重要な、内装仕切り、床システム、構造要素にまで及びます。航空機メーカーがコスト効率と燃料節約技術に重点を置くようになるにつれ、アルミハニカム構造への好みは強まり続けています。

これらの材料はまた、建築・建設業界でも受け入れられつつあります。軽量で剛性が高いため、設置が容易で寿命が長く、構造的役割において優れた性能を発揮します。耐火性と遮音性という特性は、特に商業施設や公共施設での被覆システム、天井、間仕切りでの使用に貢献しています。グリーン建築基準や持続可能なアーキテクチャへのシフトは、特に新興経済諸国において、建築慣行におけるアルミハニカムパネルの採用率向上につながりました。

製品仕様の観点からは、コア厚さ、合金タイプ、セル構成の革新を通じて市場が進展しています。2024年に9億7,200万米ドルと評価されたコア厚セグメントは、予測期間中にCAGR7%で成長すると予想されています。コアの寸法を変化させることで、用途に応じて耐荷重性能をカスタマイズできる一方、特定の合金は耐食性を高め、構造性能を最適化します。また、特定の合金は耐食性を高め、構造性能を最適化します。開発メーカーは、特定の設計要件や技術要件に対応するため、オーダーメイドのパネル形状やサイズも開発しています。このような技術革新により、アルミハニカムパネルは多業種にわたる複雑な環境への適応性を高めています。

最終用途別では、航空宇宙・防衛産業が2024年の市場で最大のシェアを占め、市場規模は12億米ドル、市場シェアは32.4%です。この分野は2034年までCAGR7.2%で拡大すると予想されています。成長の原動力となっているのは、国防計画への投資の増加と、先進防衛システム向けの軽量材料への重点化の高まりです。自動車産業、特に電気自動車分野では、パネルは車両全体の重量を減らすことで航続距離の延長と性能向上に貢献しています。

さらに、海洋、鉄道、ロジスティクスなどの分野でも、耐腐食性、熱安定性、加工のしやすさの必要性から、パネルの利用が拡大しています。これらの特性により、パネルは船舶の内装、列車のコンパートメント、貨物システムでの使用に適しています。また、産業機器メーカーも、機密機器の構造フレームやエンクロージャーの製造にこのパネルを使用しており、その汎用性と性能の一貫性が浮き彫りになっています。

米国のアルミハニカムパネル市場は、2024年には8億8,830万米ドルとなり、2025年から2034年にかけてCAGR6.5%で成長すると予測されています。同国は航空機生産の世界のハブとしての地位に加え、電気自動車や軍用アップグレードへの投資が増加しており、市場拡大に有利な条件が整いつつあります。環境に配慮した建設慣行や商業ビルにおけるエネルギー効率の重視が、国内需要をさらに後押ししています。

競合情勢には、先進的な製造、多様な製品ポートフォリオ、サプライチェーンにわたる戦略的パートナーシップの組み合わせによって市場を独占している主要な複合材料メーカーや素材メーカーが名を連ねています。これらの企業は、製品の強度、耐火性、進化する工業規格への適合性を向上させるため、継続的に研究開発に投資しています。世界の規制基準や持続可能性目標に合わせて生産することで、これらの企業は競争力を維持し、大量生産とハイスペック市場の両方の需要に対応しています。OEMや請負業者との確立された関係は、長期的な事業の継続性を保証し、自動化と品質管理への取り組みは、重要な最終用途分野でのリーダーシップを強化しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク・課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測、用途、2021年~2034年

- 主要動向

- 航空宇宙用途

- 商用航空

- 航空機の床システム

- 内装パネルとコンポーネント

- 構造アプリケーション

- 軍事および防衛航空

- 宇宙および衛星アプリケーション

- 商用航空

- 自動車用途

- 電気自動車部品

- 衝突吸収システム

- 構造補強

- 内装および外装パネル

- 建設とアーキテクチャ

- カーテンウォールシステム

- ファサードクラッディング

- インテリアデザインアプリケーション

- 屋根と構造要素

- 海洋用途

- 造船および海軍用途

- ヨットおよびレジャーボートの製造

- 海洋プラットフォーム建設

- 産業用途

- 機械設備製造

- 工具と治具

- クリーンルームおよび実験室アプリケーション

- 交通と鉄道

- 高速鉄道アプリケーション

- 都市交通システム

- 商用車アプリケーション

- その他

- 家具とデザイン

- 再生可能エネルギーの応用

- スポーツ・レクリエーション用品

第6章 市場推計・予測:コアタイプと仕様別、2021年~2034年

- 主要動向

- コアの厚さ

- 超薄(5mm~10mm)

- 標準(11mm~25mm)

- 中厚(26mm~50mm)

- 厚手(51mm~100mm)

- 重厚(100mm以上)

- アルミニウム合金タイプ

- 3003合金(商用グレード)

- 5052合金(航空宇宙グレード)

- 5056合金(高性能用途)

- その他の特殊合金

- セルのサイズと構成

- 標準的な六角形セル

- マイクロセル構成

- カスタムセルジオメトリ

- フェイスシート素材

- アルミニウム表面シート

- 複合表面シート

- ハイブリッド構成

- パネルのサイズと寸法

- 標準パネル

- 大型パネル

- カスタムサイズのアプリケーション

第7章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 航空宇宙・防衛産業

- 自動車産業

- 建築・建設業界

- 商業建設

- 住宅用途

- インフラ開発

- 海洋・造船業

- 商業輸送

- 海軍・防衛用途

- レクリエーション用マリンマーケット

- オフショアエネルギー部門

- 運輸・物流

- 鉄道輸送

- 商用車

- 公共交通機関

- 工業製造業

- 機械設備

- クリーンルームアプリケーション

- 特殊な産業用途

- その他

- エネルギーと発電

- スポーツとレクリエーション

- 家具とインテリアデザイン

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ

第9章 企業プロファイル

- 3A Composites Holding AG

- Hexcel Corporation

- Plascore Inc.

- Alcoa Corporation

- Novelis Inc.

- Hunter Douglas N.V.

- Toray Advanced Composites

- Euro-Composites S.A.

- Collins Aerospace(Raytheon Technologies)

- Argosy International Inc.

- Alucoil S.L.

- Pacific Panels Inc.

- Benecor Inc.

- Liming Honeycomb Composites Co., Ltd.

- KUMZ(Kamensk-Uralsky Metallurgical Works)

- Eco Earth Solutions

- Renoxbell Group

- Foshan Alucrown Building Materials Co., Ltd.

- Mass Transit Equipment LLP

- UACJ Corporation

- Schweiter Technologies AG

- Shinko-North Co., Ltd.

- Guangzhou Aloya Renoxbell Aluminum Co., Ltd.

- Advanced Custom Manufacturing

- Zodiac Aerospace(Safran)

- B/E Aerospace

- Triumph Group Inc.

- The NORDAM Group LLC

- Flatiron Panel Products

- Corex-Honeycomb

- 3M Company

- Armacell International S.A.

- MC Gill Corporation

- TenCate Advanced Composites

- Oerlikon Metco

- Boeing Encore Interiors LLC

- Safran S.A.

- Rockwell Collins(Collins Aerospace)

- Avcorp Industries Inc.

- Yamaton Corporation

- Shuangdie Group

- SPEE3D

- Zimmermann Group

- BoDo Plastics

- Duramax

- LIDA PLASTIC INDUSTRY

- Gayatri Corporation

- Viva Composite Panel Pvt Ltd

- Go Alubuild Pvt Ltd

- Kukreja Brothers

- Uniwell International Enterprises Corp.

- Prance Building Materials

- DJ Aluminum

- Alumetal

- TOPCOMB

- Chaluminium

- Jixiang Aluminum

目次

The Global Aluminum Honeycomb Panels Market was valued at USD 3.57 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 6.79 billion by 2034. This growth is primarily driven by increasing applications across multiple high-performance industries that require materials combining strength with low weight. The demand is particularly pronounced in sectors where performance efficiency and structural integrity are key, such as aerospace, automotive, construction, and industrial manufacturing. These panels are widely recognized for their ability to meet stringent requirements related to energy absorption, durability, and resistance to various stresses without significantly increasing the weight of structures.

As industries continue to pursue energy-saving and sustainability goals, the demand for lightweight yet robust materials is rising, which makes aluminum honeycomb panels an ideal solution. The rising trend of using these materials in modern infrastructure, transportation systems, and specialized equipment housing further supports their growing relevance in global markets. Their appeal is enhanced by their recyclability, fire resistance, and thermal insulation properties, making them suitable for a wide range of applications that require both functionality and environmental responsibility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.57 billion |

| Forecast Value | $6.79 billion |

| CAGR | 6.7% |

In the aerospace segment, aluminum honeycomb panels are gaining rapid traction as they fulfill essential criteria such as lightweight and high strength. The aerospace applications segment alone was valued at USD 1.09 billion in 2024 and is projected to register a CAGR of 7.5% from 2025 to 2034. These panels help enhance fuel efficiency and enable improved design flexibility, which is critical in aviation manufacturing. Their usage extends to interior partitions, flooring systems, and structural elements, where weight reduction is crucial without compromising performance. As aircraft manufacturers increase focus on cost-efficient and fuel-saving technologies, the preference for aluminum honeycomb structures continues to strengthen.

These materials are also finding growing acceptance in the building and construction industry. Their combination of low weight and high rigidity allows for easier installation, longer lifespan, and superior performance in structural roles. Their fire-resistant and sound-insulating features further contribute to their use in cladding systems, ceilings, and partitions, particularly in commercial and institutional buildings. The shift toward green building codes and sustainable architecture has led to higher adoption of aluminum honeycomb panels in construction practices, especially in developed economies.

From a product specification standpoint, the market is advancing through innovations in core thickness, alloy types, and cell configurations. The core thickness segment, which was valued at USD 972 million in 2024, is expected to grow at a CAGR of 7% over the forecast period. Varying core dimensions offer customized load-bearing capabilities across applications, while specific alloys enhance corrosion resistance and optimize structural performance. Manufacturers are also developing tailored panel shapes and sizes to cater to specific design or technical requirements. These innovations are making aluminum honeycomb panels more adaptable to complex environments across multiple industries.

In terms of end-use, the aerospace and defense industry accounted for the largest share of the market in 2024, valued at USD 1.2 billion and holding a 32.4% market share. This segment is expected to expand at a CAGR of 7.2% through 2034. The growth is fueled by increased investment in national defense programs and a growing emphasis on lightweight materials for advanced defense systems. In the automotive industry, particularly in the electric vehicle segment, the panels contribute to extended range and better performance by reducing overall vehicle weight.

Additionally, their growing usage in sectors like marine, rail, and logistics is driven by the need for corrosion resistance, thermal stability, and ease of fabrication. These characteristics make the panels well-suited for use in ship interiors, train compartments, and cargo systems. Industrial manufacturers also rely on these panels to build structural frames and enclosures for sensitive equipment, which highlights their versatility and performance consistency.

In the United States, the aluminum honeycomb panels market was valued at USD 888.3 million in 2024 and is projected to grow at a CAGR of 6.5% from 2025 to 2034. The country's position as a global hub for aircraft production, along with rising investments in electric vehicles and military upgrades, is creating favorable conditions for market expansion. The emphasis on environmentally friendly construction practices and energy efficiency in commercial buildings further supports domestic demand.

The competitive landscape features major composite and material producers who dominate the market through a combination of advanced manufacturing, diverse product portfolios, and strategic partnerships across supply chains. These companies continuously invest in research and development to improve product strength, fire resistance, and adaptability to meet evolving industrial standards. By aligning production with global regulatory norms and sustainability targets, these firms maintain their competitive edge and cater to both high-volume and high-specification market demands. Their established relationships with OEMs and contractors ensure long-term business continuity, while their commitment to automation and quality control reinforces their leadership in critical end-use segments.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Application

- 2.2.3 Core Type and Specifications

- 2.2.4 End use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, Application, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Aerospace applications

- 5.2.1 Commercial aviation

- 5.2.1.1 Aircraft flooring systems

- 5.2.1.2 Interior panels and components

- 5.2.1.3 Structural applications

- 5.2.2 Military and defense aviation

- 5.2.3 Space and satellite applications

- 5.2.1 Commercial aviation

- 5.3 Automotive applications

- 5.3.1 Electric vehicle components

- 5.3.2 Crash absorption systems

- 5.3.3 Structural reinforcements

- 5.3.4 Interior and exterior panels

- 5.4 Construction and architecture

- 5.4.1 Curtain wall systems

- 5.4.2 Facade cladding

- 5.4.3 Interior design applications

- 5.4.4 Roofing and structural elements

- 5.5 Marine applications

- 5.5.1 Ship building and naval applications

- 5.5.2 Yacht and recreational boat manufacturing

- 5.5.3 Offshore platform construction

- 5.6 Industrial applications

- 5.6.1 Machinery and equipment manufacturing

- 5.6.2 Tooling and fixtures

- 5.6.3 Clean room and laboratory applications

- 5.7 Transportation and rail

- 5.7.1 High-speed rail applications

- 5.7.2 Urban transit systems

- 5.7.3 Commercial vehicle applications

- 5.8 Others

- 5.8.1 Furniture and design

- 5.8.2 Renewable energy applications

- 5.8.3 Sports and recreation equipment

Chapter 6 Market Estimates & Forecast, By Core Type and Specifications, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Core thickness

- 6.2.1 Ultra-thin (5mm-10mm)

- 6.2.2 Standard (11mm-25mm)

- 6.2.3 Medium (26mm-50mm)

- 6.2.4 Thick (51mm-100mm)

- 6.2.5 Heavy-duty (above 100mm)

- 6.3 Aluminum alloy type

- 6.3.1 3003 alloy (commercial grade)

- 6.3.2 5052 alloy (aerospace grade)

- 6.3.3 5056 alloy (high-performance applications)

- 6.3.4 Other specialized alloys

- 6.4 Cell size and configuration

- 6.4.1 Standard hexagonal cells

- 6.4.2 Micro-cell configurations

- 6.4.3 Custom cell geometries

- 6.5 Face sheet material

- 6.5.1 Aluminum face sheets

- 6.5.2 Composite face sheets

- 6.5.3 Hybrid configurations

- 6.6 Panel size and dimensions

- 6.6.1 Standard panels

- 6.6.2 Large format panels

- 6.6.3 Custom-sized applications

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Aerospace and defense industry

- 7.3 Automotive industry

- 7.4 Building and construction industry

- 7.4.1 Commercial construction

- 7.4.2 Residential applications

- 7.4.3 Infrastructure development

- 7.5 Marine and shipbuilding industry

- 7.5.1 Commercial shipping

- 7.5.2 Naval and defense applications

- 7.5.3 Recreational marine market

- 7.5.4 Offshore energy sector

- 7.6 Transportation and logistics

- 7.6.1 Rail transportation

- 7.6.2 Commercial vehicles

- 7.6.3 Public transportation systems

- 7.7 Industrial manufacturing

- 7.7.1 Machinery and equipment

- 7.7.2 Clean room applications

- 7.7.3 Specialized industrial uses

- 7.8 Others

- 7.8.1 Energy and power generation

- 7.8.2 Sports and recreation

- 7.9 Furniture and interior design

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 3A Composites Holding AG

- 9.2 Hexcel Corporation

- 9.3 Plascore Inc.

- 9.4 Alcoa Corporation

- 9.5 Novelis Inc.

- 9.6 Hunter Douglas N.V.

- 9.7 Toray Advanced Composites

- 9.8 Euro-Composites S.A.

- 9.9 Collins Aerospace (Raytheon Technologies)

- 9.10 Argosy International Inc.

- 9.11 Alucoil S.L.

- 9.12 Pacific Panels Inc.

- 9.13 Benecor Inc.

- 9.14 Liming Honeycomb Composites Co., Ltd.

- 9.15 KUMZ (Kamensk-Uralsky Metallurgical Works)

- 9.16 Eco Earth Solutions

- 9.17 Renoxbell Group

- 9.18 Foshan Alucrown Building Materials Co., Ltd.

- 9.19 Mass Transit Equipment LLP

- 9.20 UACJ Corporation

- 9.21 Schweiter Technologies AG

- 9.22 Shinko-North Co., Ltd.

- 9.23 Guangzhou Aloya Renoxbell Aluminum Co., Ltd.

- 9.24 Advanced Custom Manufacturing

- 9.25 Zodiac Aerospace (Safran)

- 9.26 B/E Aerospace

- 9.27 Triumph Group Inc.

- 9.28 The NORDAM Group LLC

- 9.29 Flatiron Panel Products

- 9.30 Corex-Honeycomb

- 9.31 3M Company

- 9.32 Armacell International S.A.

- 9.33 MC Gill Corporation

- 9.34 TenCate Advanced Composites

- 9.35 Oerlikon Metco

- 9.36 Boeing Encore Interiors LLC

- 9.37 Safran S.A.

- 9.38 Rockwell Collins (Collins Aerospace)

- 9.39 Avcorp Industries Inc.

- 9.40 Yamaton Corporation

- 9.41 Shuangdie Group

- 9.42 SPEE3D

- 9.43 Zimmermann Group

- 9.44 BoDo Plastics

- 9.45 Duramax

- 9.46 LIDA PLASTIC INDUSTRY

- 9.47 Gayatri Corporation

- 9.48 Viva Composite Panel Pvt Ltd

- 9.49 Go Alubuild Pvt Ltd

- 9.50 Kukreja Brothers

- 9.51 Uniwell International Enterprises Corp.

- 9.52 Prance Building Materials

- 9.53 DJ Aluminum

- 9.54 Alumetal

- 9.55 TOPCOMB

- 9.56 Chaluminium

- 9.57 Jixiang Aluminum

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日