|

市場調査レポート

商品コード

1773262

ボール盤の市場機会、成長促進要因、産業動向分析、2025~2034年予測Drilling Machines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ボール盤の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年06月16日

発行: Global Market Insights Inc.

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

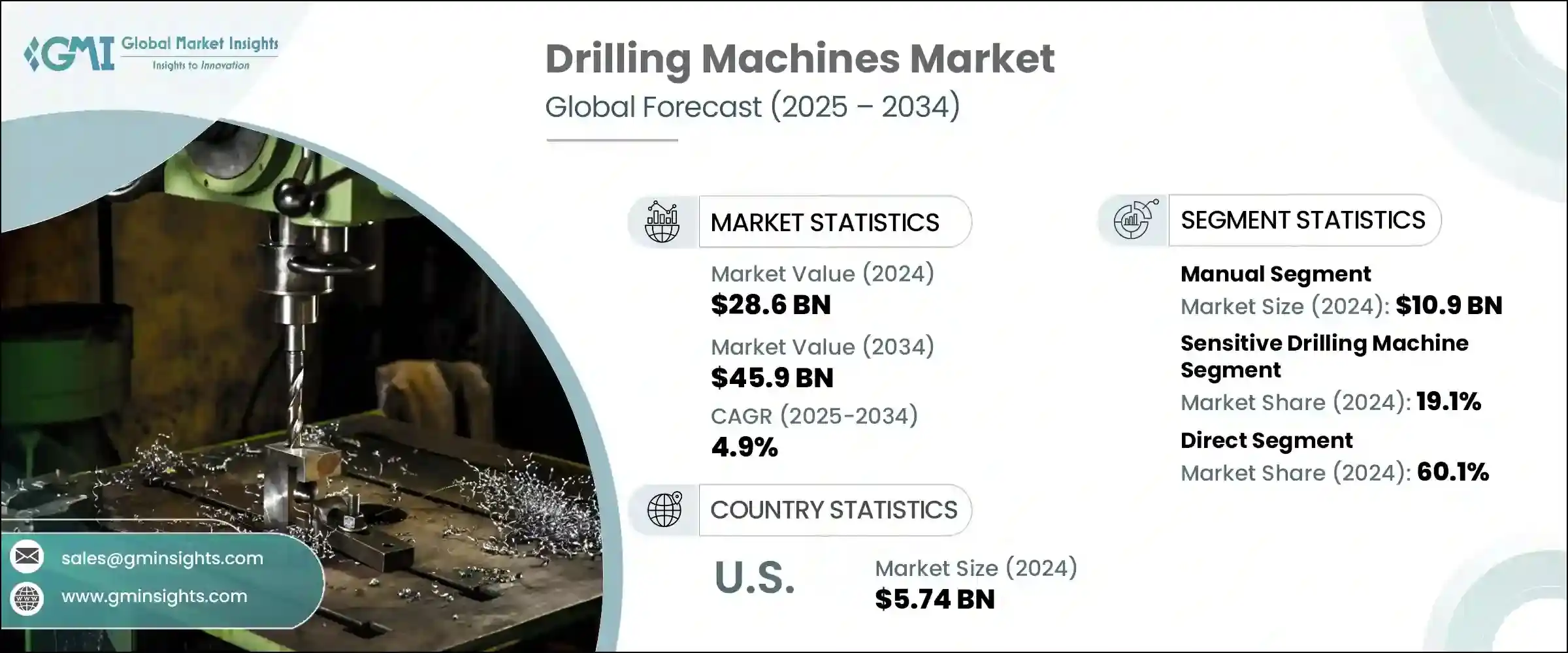

ボール盤の世界市場は、2024年には286億米ドルとなり、CAGR 4.9%で成長し、2034年には459億米ドルに達すると予測されています。

スマート製造の進展と産業自動化の急成長が市場拡大に拍車をかけています。精度と安定した出力で知られるCNCボール盤は、スマート工場環境において不可欠なコンポーネントとなりつつあります。インダストリー4.0やIoTを駆使したシステムが製造業全体で勢いを増す中、ボール盤は、リアルタイム性能監視、遠隔システム診断、予知保全などのインテリジェント機能で強化されており、これらすべてが効率改善やダウンタイム削減に貢献しています。

また、特に新興経済諸国におけるインフラ整備や都市の拡大により、建設が盛んな地域でも需要が伸びています。こうした動向は、新興市場特有のニーズを満たす、よりコンパクトでコスト効率の高い機械を生産するよう、現地メーカーに影響を与えています。業界の成長をさらに支えているのは、分野を超えた用途基盤の拡大、先端技術へのアクセスの改善、デジタル製造エコシステムへの投資の増加です。これらの原動力が相まって、ボール盤の世界的な産業サプライチェーンにおける使用方法が再構築され、この分野の着実な上昇軌道に寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 286億米ドル |

| 予測金額 | 459億米ドル |

| CAGR | 4.9% |

建設活動が勢いを増す中、大規模な作業に対応できる大型掘削ソリューションへのニーズが高まっています。多くの新興国市場では、インフラのアップグレードが急増しており、頑丈で効率的な機械に対する安定した需要が生まれています。これに対応するため、メーカーは耐久性だけでなく、さまざまな作業条件に適応できる機器の製造に注力しています。

2024年、手動ボール盤は109億米ドルを生み出し、2034年までCAGR 3.8%で成長すると予想されています。自動化が急進しているにもかかわらず、手動ボール盤は、その低コスト、柔軟性、使いやすさから、多くの産業で依然として不可欠です。これらの機械は、エネルギーへのアクセスが限られている地域や、熟練労働者の人件費が低い地域で頻繁に利用されています。基本的な掘削作業で十分であり、高度なシステムがまだ実現できない中小企業、移動式作業場、遠隔地の作業現場では、しばしば第一の選択肢となります。多機能であり、基本的な作業への適応性が高いため、開発が遅れていたり、インフラが整っていない環境での日常的な産業作業や建設作業にとって、実用的なソリューションとなっています。

高感度ボール盤は2024年に19.1%のシェアを占め、2034年までのCAGRは4.2%と予測されています。これらの機械は、その精度、信頼性、高い精度を必要とする軽負荷用途に適していることから支持されています。スペースが限られ、デリケートな取り扱いが重要な作業で広く使用されています。コンパクトな構造でメンテナンスが容易なため、緻密な穴あけや細部の仕上げが必要な分野で広く採用されています。新興国では精密加工への投資が進んでおり、教育現場や小規模な加工工場など、低価格で高性能な工具が求められる分野でニーズが高まっています。

米国の2024年の市場規模は57億4,000万米ドルで、2025~2034年にかけてCAGR 4.7%で成長すると予測されています。同国では近代的な製造手法への継続的な投資とインダストリー4.0技術の採用により、自動化されたインテリジェントなボール盤の需要が大きく伸びています。国内生産能力の復活は、拡大する再生可能エネルギーへの取り組みや老朽化したインフラをアップグレードする努力と相まって、さまざまな掘削システムに対する安定した需要に拍車をかけています。米国はまた、強固なサプライチェーン、強力な研究開発投資、新技術の早期導入の恩恵を受けており、製造、エネルギー、産業の各分野における高度で革新的な機器の統合を支えています。

ボール盤市場で競合している主要企業には、Cheto Corporation SA、Soilmec S.p.A.、Minitool、Hitachi Construction Machinery Ltd、Mitsubishi Heavy Industries Ltd.、Ingersoll Rand、Sandvik AB、Epiroc AB、KURAKI Co Ltd、SMTCL、Beretta S.r.l. P、ERLO Group、Bauer Maschinen GmbH、Robert Bosch GmbH、Caterpillar、Liebherr Group、Dezhou Hongxin Machine Tool Co Ltd、Shenyang Machine Tool Co Ltd、Atlas Copco、Boart Longyearなどです。市場ポジションを強化するため、ボール盤業界の主要企業は、AI統合、IoT接続、自動化に適した設計を特徴とする次世代機械で製品ラインを拡大するなどの戦略を追求しています。また、新たな地域へのアクセスや流通能力を強化するために、パートナーシップや合弁事業が設立されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 産業自動化とスマート製造

- インフラと建設プロジェクトの増加

- 新興経済における都市化と工業化

- 業界の潜在的リスク・課題

- 特定の最終用途産業における導入の遅れ

- 安全性と運用上の危険性

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 技術・イノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- タイプ別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- 貿易統計

- 主要輸入国

- 主要輸出国

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:タイプ別、2021~2034年

- 主要動向

- 高感度ボール盤

- 直立型ボール盤

- ラジアルボール盤

- ギャングボール盤

- 深穴ボール盤

- CNCボール盤

- 多軸ボール盤

- その他(磁気ボール盤)

第6章 市場推計・予測:自動化レベル別、2021~2034年

- 主要動向

- 手動

- 半自動

- 完全自動

第7章 市場推計・予測:操作別、2021~2034年

- 主要動向

- 穴あけ加工

- タッピング加工

- 座ぐり加工

- リーミング加工

- スポットフェーシング加工

- その他(ボーリング、ペック、コア)

第8章 市場推計・予測:構造別、2021~2034年

- 主要動向

- 固定式

- ポータブル

第9章 市場推計・予測:電源別、2021~2034年

- 主要動向

- 電池駆動

- コード付き

第10章 市場推計・予測:用途別、2021~2034年

- 主要動向

- 金属の穴あけ

- 木材の穴あけ

- 繊維・プラスチックの穴あけ

- 複合材料の穴あけ

- ガラス・セラミックの穴あけ

- その他(医療用インプラント・手術器具、PCBドリリング(マイクロドリリング)など)

第11章 市場推計・予測:最終用途別、2021~2034年

- 主要動向

- 航空宇宙

- 重機

- 自動車

- エネルギー業界

- 軍事・防衛

- その他

第12章 市場推計・予測:流通チャネル別、2021~2034年

- 主要動向

- 直接

- 間接

第13章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- インドネシア

- マレーシア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第14章 企業プロファイル

- Atlas Copco

- Bauer Maschinen GmbH

- Beretta S.r.l. P

- Boart Longyear

- Caterpillar

- Cheto Corporation SA

- Dezhou Hongxin Machine Tool Co Ltd

- Epiroc AB

- ERLO Group

- Hitachi Construction Machinery Ltd

- Ingersoll Rand

- KURAKI Co Ltd

- Liebherr Group

- Minitool

- Mitsubishi Heavy Industries ltd.

- Robert Bosch GmbH

- Sandvik AB

- Shenyang Machine Tool Co Ltd

- SMTCL

- Soilmec S.p.A.

The Global Drilling Machines Market was valued at USD 28.6 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 45.9 billion by 2034. The ongoing evolution of smart manufacturing and rapid growth in industrial automation are fueling market expansion. CNC drilling machines, known for their precision and consistent output, are becoming essential components in smart factory environments. As Industry 4.0 and IoT-driven systems gain momentum across manufacturing industries, drilling machines are being enhanced with intelligent features such as real-time performance monitoring, remote system diagnostics, and predictive maintenance, all of which contribute to improved efficiency and reduced downtime.

Demand is also growing in construction-heavy regions, particularly due to robust infrastructure development and urban expansion in industrializing economies. These trends are influencing local manufacturers to produce more compact and cost-efficient machines that meet the unique needs of emerging markets. The industry's growth is further supported by the widening application base across sectors, improved access to advanced technology, and rising investment in digital manufacturing ecosystems. Combined, these dynamics are reshaping how drilling machines are used across global industrial supply chains and contributing to the sector's steady upward trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $28.6 Billion |

| Forecast Value | $45.9 Billion |

| CAGR | 4.9% |

With construction activities gaining momentum, there is a growing need for heavy-duty drilling solutions that can keep up with large-scale operations. Many developing markets are experiencing a surge in infrastructure upgrades, which is creating consistent demand for rugged, efficient machines. In response, manufacturers are focusing on building equipment that is not only durable but also adaptable to varying working conditions.

In 2024, manual drilling machines generated USD 10.9 billion and are expected to grow at a CAGR of 3.8% through 2034. Despite the surge in automation, manual drilling equipment remains essential in many industries due to its lower cost, flexibility, and ease of use. These machines are frequently utilized in regions with limited access to energy or where skilled labor costs remain low. They are often the first choice for smaller businesses, mobile workshops, and remote worksites where basic drilling operations are sufficient and advanced systems are not yet feasible. Their multifunctional nature and adaptability for basic operations make them a practical solution for everyday industrial and construction tasks in less-developed or infrastructure-poor environments.

The sensitive drilling machines segment accounted for a 19.1% share in 2024 and is forecasted to grow at a CAGR of 4.2% through 2034. These machines are favored for their precision, reliability, and suitability for light-duty applications requiring high levels of accuracy. They are extensively used in operations where space is limited and delicate handling is crucial. Because of their compact structure and straightforward maintenance, they are widely adopted in fields requiring meticulous hole placement and fine detailing. Emerging economies are increasingly investing in precision manufacturing, driving the need for these machines in educational workshops, small-scale fabrication units, and other sectors prioritizing affordable, high-performance tools.

United States Drilling Machines Market was valued at USD 5.74 billion in 2024 and is projected to grow at a CAGR of 4.7% between 2025 and 2034. With the country's continued investment in modern manufacturing practices and adoption of Industry 4.0 technologies, the demand for automated and intelligent drilling machines is growing significantly. The resurgence of domestic production capacity, coupled with expanding renewable energy initiatives and efforts to upgrade outdated infrastructure, is spurring consistent demand for a range of drilling systems. The U.S. also benefits from a robust supply chain, strong R&D investment, and early adoption of new technologies, which supports the integration of sophisticated and innovative equipment across manufacturing, energy, and industrial segments.

Major companies competing in the Drilling Machines Market include Cheto Corporation SA, Soilmec S.p.A., Minitool, Hitachi Construction Machinery Ltd, Mitsubishi Heavy Industries Ltd., Ingersoll Rand, Sandvik AB, Epiroc AB, KURAKI Co Ltd, SMTCL, Beretta S.r.l. P, ERLO Group, Bauer Maschinen GmbH, Robert Bosch GmbH, Caterpillar, Liebherr Group, Dezhou Hongxin Machine Tool Co Ltd, Shenyang Machine Tool Co Ltd, Atlas Copco, and Boart Longyear. To strengthen their market position, leading companies in the drilling machines industry are pursuing strategies such as expanding their product lines with next-generation machines featuring AI integration, IoT connectivity, and automation-friendly designs. Partnerships and joint ventures are being formed to access new regions and enhance distribution capabilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Automation Level

- 2.2.4 Operation

- 2.2.5 Application

- 2.2.6 End use

- 2.2.7 Structure

- 2.2.8 Power Source

- 2.2.9 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Industrial automation and smart manufacturing

- 3.2.1.2 Rising infrastructure and construction projects

- 3.2.1.3 Urbanization and industrialization in emerging economies

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Slow adoption in certain end use industries

- 3.2.2.2 Safety and operational hazards

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation Landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Sensitive drilling machine

- 5.3 Upright drilling machine

- 5.4 Radial drilling machine

- 5.5 Gang drilling machine

- 5.6 Deep hole drilling machine

- 5.7 CNC drilling machine

- 5.8 Multiple spindle drilling machine

- 5.9 Others (magnetic drilling machine)

Chapter 6 Market Estimates & Forecast, By Automation Level, 2021 - 2034, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Semi-Automated

- 6.4 Fully Automated

Chapter 7 Market Estimates & Forecast, By Operation, 2021 - 2034, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Hole drilling

- 7.3 Tapping

- 7.4 Counterboring

- 7.5 Reaming

- 7.6 Spot facing

- 7.7 Others (Boring, Peck, Core)

Chapter 8 Market Estimates & Forecast, By Structure, 2021 - 2034, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Fixed

- 8.3 Portable

Chapter 9 Market Estimates & Forecast, By Power Source, 2021 - 2034, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Battery powered

- 9.3 Corded

Chapter 10 Market Estimates & Forecast, By Application, 2021 - 2034, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Metal drilling

- 10.3 Wood drilling

- 10.4 Fiber & plastic drilling

- 10.5 Composite material drilling

- 10.6 Glass and ceramic drilling

- 10.7 Others (Medical implants & Surgical tools, PCB drilling (Micro drilling), etc.)

Chapter 11 Market Estimates & Forecast, By End Use, 2021 - 2034, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 Aerospace

- 11.3 Heavy equipment

- 11.4 Automotive

- 11.5 Energy industry

- 11.6 Military & defense

- 11.7 Others

Chapter 12 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Billion) (Million Units)

- 12.1 Key trends

- 12.2 Direct

- 12.3 Indirect

Chapter 13 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Million Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 South Korea

- 13.4.5 Australia

- 13.4.6 Indonesia

- 13.4.7 Malaysia

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.6 MEA

- 13.6.1 Saudi Arabia

- 13.6.2 UAE

- 13.6.3 South Africa

Chapter 14 Company Profiles

- 14.1 Atlas Copco

- 14.2 Bauer Maschinen GmbH

- 14.3 Beretta S.r.l. P

- 14.4 Boart Longyear

- 14.5 Caterpillar

- 14.6 Cheto Corporation SA

- 14.7 Dezhou Hongxin Machine Tool Co Ltd

- 14.8 Epiroc AB

- 14.9 ERLO Group

- 14.10 Hitachi Construction Machinery Ltd

- 14.11 Ingersoll Rand

- 14.12 KURAKI Co Ltd

- 14.13 Liebherr Group

- 14.14 Minitool

- 14.15 Mitsubishi Heavy Industries ltd.

- 14.16 Robert Bosch GmbH

- 14.17 Sandvik AB

- 14.18 Shenyang Machine Tool Co Ltd

- 14.19 SMTCL

- 14.20 Soilmec S.p.A.