|

|

市場調査レポート

商品コード

1773259

電動モビリティデバイスの市場機会と促進要因、業界動向分析、2025~2034年予測Powered Mobility Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 電動モビリティデバイスの市場機会と促進要因、業界動向分析、2025~2034年予測 |

|

出版日: 2025年06月24日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

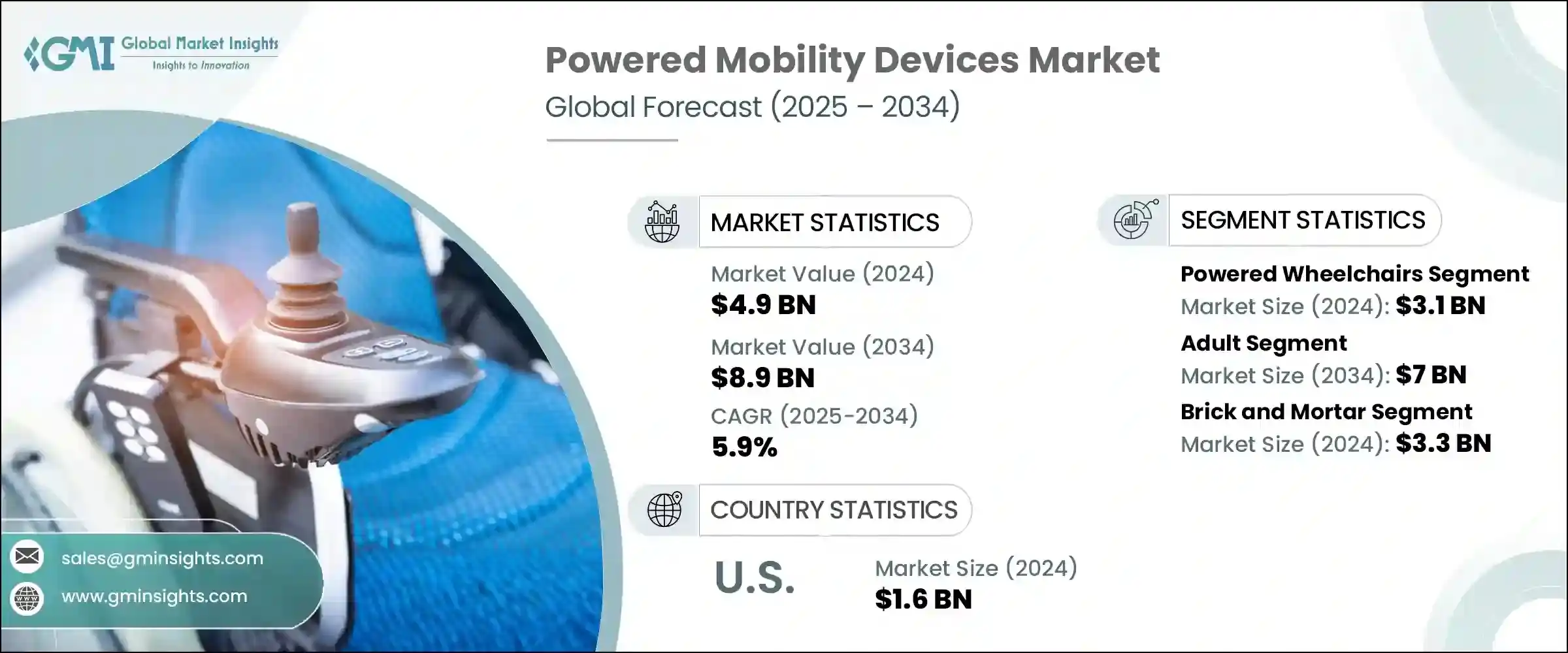

世界の電動モビリティデバイス市場は、2024年には49億米ドルと評価され、CAGR 5.9%で成長し、2034年には89億米ドルに達すると推定されています。

この急増は、世界的な障害率の上昇、神経疾患の有病率の増加、移動補助器具の急速な技術進歩によるものです。バッテリー駆動のモビリティソリューションは、手作業による移動が困難または不可能な場合に自立性を提供し、生活の質を大幅に向上させます。センサーとカメラを搭載したスマート車いすの導入は極めて重要な進歩であり、ユーザー、特に神経学的課題を抱えるユーザーが、リアルタイムのフィードバックで安全に環境を移動できるようにします。こうしたインテリジェントデバイスは、モビリティを向上させるだけでなく、ヘルスケアプロバイダーの貴重な行動洞察もサポートします。アンメットメディカルニーズ、急速な技術進歩、進化する人口統計学的パターンの融合は、電動モビリティデバイスがヘルスケアと個人の自立に不可欠なものとなっている理由を明確に説明しています。

電動モビリティデバイスは、利用者の安全性と自立を最優先する最先端技術を統合することで、移動の障壁を克服する道を切り開きます。先進的なセンサー、直感的なコントロール、AIを搭載したナビゲーションを備え、個々のニーズに合わせた、よりスマートで応答性の高い操作を提供します。自律的な機能は介助者への依存を軽減し、利用者が様々な環境で自信を持って移動できる自由度を高めます。イノベーションと人間工学に基づいたデザインを組み合わせることで、これらのモビリティエイドは身体的なアクセシビリティを高めるだけでなく、社会的包摂と感情的な幸福を育み、全体的な生活の質を向上させます。技術の進化に伴い、電動モビリティデバイスはより適応性が高く、信頼性が高く、ユーザーフレンドリーになってきており、個人に合わせたモビリティサポートの新たな基準を打ち立てています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 49億米ドル |

| 予測金額 | 89億米ドル |

| CAGR | 5.9% |

電動車いすセグメントは、屋内外を問わずシームレスで楽な移動を提供することで、2024年の市場をリードし、31億米ドルに達しました。独立駆動、立ち乗り車いす、ポータブルユニットなどの多様なオプションにより、ユーザーは、調節可能なクッション、人間工学に基づいた背もたれ、高度なチルトインスペース機構などの高度にカスタマイズ可能な機能から恩恵を受け、快適性を向上させるだけでなく、リハビリをサポートし、二次的な健康問題を軽減します。

成人人口セグメントは2034年までに70億米ドルに達すると予想され、特に高齢者が最大のユーザー層を形成します。この人口層における障害の有病率の増加は、大きな成長促進要因です。電動モビリティデバイスは、日常作業の簡素化、ユーザーの自律性の強化、疲労の最小化という重要な役割を担っており、高齢者の40%近くが移動制限に直面しています。

米国の電動モビリティデバイス市場は2024年に16億米ドルと評価され、神経疾患、脊髄損傷、高齢化人口の増加に支えられています。有利な償還政策と可処分所得の増加が相まって、高級電動車いすと移動用スクーターの導入が加速し、市場成長の勢いがさらに強まっています。

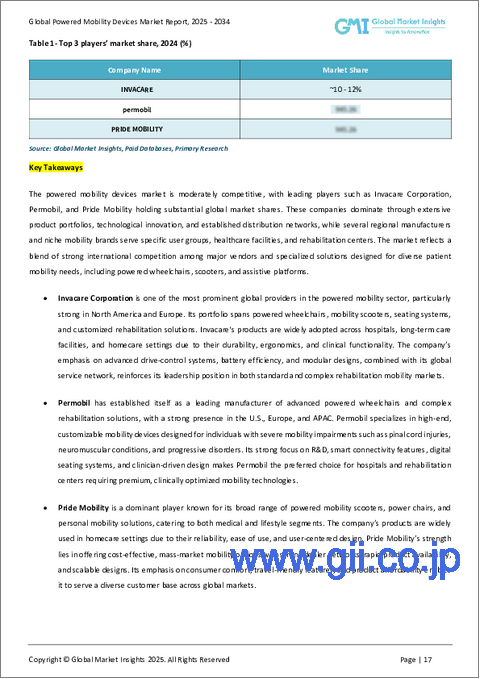

世界の電動モビリティデバイス市場の主要企業には、PRIDE MOBILITY、GOLDEN、Drive DeVilbiss Healthcare、KARMAN、INVACARE、Hoveround Mobility Solutions、Airwheel、Decon Mobility、MEYRA、Permobil、Ottobock、OSTRICH、Merits、LEVO、Fridoなどがあります。これらの企業は、ユーザーの需要に応えるため、技術革新、資金調達、デザインを入れ替えています。大手メーカーは、センサー、IoTコネクティビティ、AI主導型ナビゲーションを統合したインテリジェント機能の研究開発を通じて差別化を図り、より安全でデータが豊富なモビリティソリューションを提供しています。

また、幅広いユーザーや状態に対応できるよう、交換可能な駆動ユニット、調節可能な座席、スタンディング機構といったモジュラー設計でポートフォリオを拡大しています。企業はヘルスケアプロバイダーや支払者とパートナーシップを結び、コストの障壁を減らし、償還経路を改善する一方、高齢者や神経障害のある人をターゲットにしたマーケティングを行っています。ニッチなイノベーターの戦略的買収や合弁事業は、企業が新しい技術や地域市場を開拓するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 神経疾患の有病率の増加

- 電動モビリティ製品の技術的進歩

- 高齢者人口の増加

- 世界における障害率の増加

- 業界の潜在的リスク・課題

- 電動車いすの高コスト

- 厳格な規制枠組み

- 機会

- 軽量で折りたたみ可能な電動車いす

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- 技術・イノベーションの情勢

- 現在の技術動向

- 新興技術

- 製品タイプ別の価格動向

- 将来の市場動向

- 償還シナリオ

- 消費者行動分析

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- その他の地域

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021~2034年

- 主要動向

- 電動車いす

- 後輪式

- 中輪式

- 前輪式

- その他

- 電動車両

- 3輪

- 4輪

- 5輪

- パワーアドオンまたは推進補助ユニット

第6章 市場推計・予測:患者別、2021~2034年

- 主要動向

- 成人

- 小児

第7章 市場推計・予測:流通チャネル別、2021~2034年

- 主要動向

- 実店舗販売

- オンラインチャネル

第8章 市場推計・予測:最終用途別、2021~2034年

- 主要動向

- ホームケア

- リハビリセンター

- 病院

- その他

第9章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Airwheel

- decon

- drive DeVilbiss Healthcare

- Frido

- GOLDEN

- Hoveround Mobility Solutions

- INVACARE

- KARMAN

- LEVO

- merits

- MEYRA

- OSTRICH

- ottobock

- permobil

- PRIDE MOBILITY

The Global Powered Mobility Devices Market was valued at USD 4.9 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 8.9 billion by 2034. This surge is due to rising global disability rates, increased prevalence of neurological conditions, and rapid technological progress in mobility aids. Battery-powered mobility solutions offer independence where manual movement is challenging or impossible, significantly enhancing quality of life. The introduction of smart wheelchairs with sensors and cameras marks a pivotal advancement, enabling users-especially those with neurological challenges-to navigate environments safely with real-time feedback. These intelligent devices not only boost mobility but also support healthcare providers with valuable behavior insights. The convergence of unmet medical needs, rapid technological advancements, and evolving demographic patterns clearly explains why powered mobility devices are becoming indispensable in healthcare and personal independence.

These devices lead the way in overcoming mobility barriers by integrating cutting-edge technology that prioritizes user safety and independence. Equipped with advanced sensors, intuitive controls, and AI-powered navigation, they offer smarter, more responsive operations tailored to individual needs. Autonomous features reduce the reliance on caregivers, allowing users greater freedom to move confidently in various environments. By combining innovation with ergonomic design, these mobility aids not only enhance physical accessibility but also improve overall quality of life, fostering social inclusion and emotional well-being. As technology continues to evolve, powered mobility devices are becoming more adaptive, reliable, and user-friendly, setting new standards in personalized mobility support.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.9 Billion |

| Forecast Value | $8.9 Billion |

| CAGR | 5.9% |

The powered wheelchair segment led the market in 2024, reaching USD 3.1 billion, by providing seamless, effortless movement both indoors and outdoors. With diverse options such as independent drive, standing wheelchairs, and portable units, users benefit from highly customizable features like adjustable cushions, ergonomic backrests, and advanced tilt-in-space mechanisms-enhancements that not only improve comfort but also support rehabilitation and reduce secondary health issues.

The adult population segment is expected to reach USD 7 billion by 2034, especially seniors form the largest base of users. The increasing prevalence of disabilities within this demographic is a significant growth driver. Powered mobility devices play a vital role in simplifying everyday tasks, enhancing user autonomy, and minimizing fatigue-benefits that are crucial for older adults, nearly 40% of whom face mobility limitations.

United States Powered Mobility Devices Market was valued at USD 1.6 billion in 2024, supported by a rise in neurological conditions, spinal cord injuries, and an aging population. Favorable reimbursement policies combined with higher disposable incomes have accelerated the adoption of premium electric wheelchairs and mobility scooters, further strengthening the market's growth momentum.

Leading brands in the Global Powered Mobility Devices Market include PRIDE MOBILITY, GOLDEN, Drive DeVilbiss Healthcare, KARMAN, INVACARE, Hoveround Mobility Solutions, Airwheel, Decon Mobility, MEYRA, Permobil, Ottobock, OSTRICH, Merits, LEVO, and Frido. These companies are reshuffling innovation, funding, and design to meet user demands. Leading manufacturers are differentiating through R&D of intelligent features-integrating sensors, IoT connectivity, and AI-driven navigation-to offer safer, data-enriched mobility solutions..

They are expanding portfolios with modular designs-swappable drive units, adjustable seating, and standing mechanisms-to accommodate a wider range of users and conditions. Firms are forging partnerships with healthcare providers and payers to reduce cost barriers and improve reimbursement pathways, while targeted marketing addresses seniors and individuals with neurological disabilities. Strategic acquisitions of niche innovators, along with joint ventures, help companies tap new technologies and geographic markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Patient

- 2.2.4 Distribution channel

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of neurological diseases

- 3.2.1.2 Technological advancements in powered mobility products

- 3.2.1.3 Rising percentage of geriatric population

- 3.2.1.4 Increasing prevalence of disabilities worldwide

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of powered wheelchairs

- 3.2.2.2 Stringent regulatory framework

- 3.2.3 Opportunities

- 3.2.3.1 Focus on lightweight and foldable electric wheelchairs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends, by product type

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.9 Consumer behaviour analysis

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Rest of the world

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Powered wheelchairs

- 5.2.1 Rear wheel

- 5.2.2 Mid-wheel

- 5.2.3 Front wheel

- 5.2.4 Other types

- 5.3 Power operated vehicles

- 5.3.1 3-wheel devices

- 5.3.2 4-wheel devices

- 5.3.3 5-wheel devices

- 5.4 Power add-on or propulsion-assist units

Chapter 6 Market Estimates and Forecast, By Patient, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Brick and mortar

- 7.3 Online channel

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Home care

- 8.3 Rehabilitation centers

- 8.4 Hospitals

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Airwheel

- 10.2 decon

- 10.3 drive DeVilbiss Healthcare

- 10.4 Frido

- 10.5 GOLDEN

- 10.6 Hoveround Mobility Solutions

- 10.7 INVACARE

- 10.8 KARMAN

- 10.9 LEVO

- 10.10 merits

- 10.11 MEYRA

- 10.12 OSTRICH

- 10.13 ottobock

- 10.14 permobil

- 10.15 PRIDE MOBILITY