|

市場調査レポート

商品コード

1773221

乾式排煙脱硫装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Dry Flue Gas Desulfurization System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 乾式排煙脱硫装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月19日

発行: Global Market Insights Inc.

ページ情報: 英文 142 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

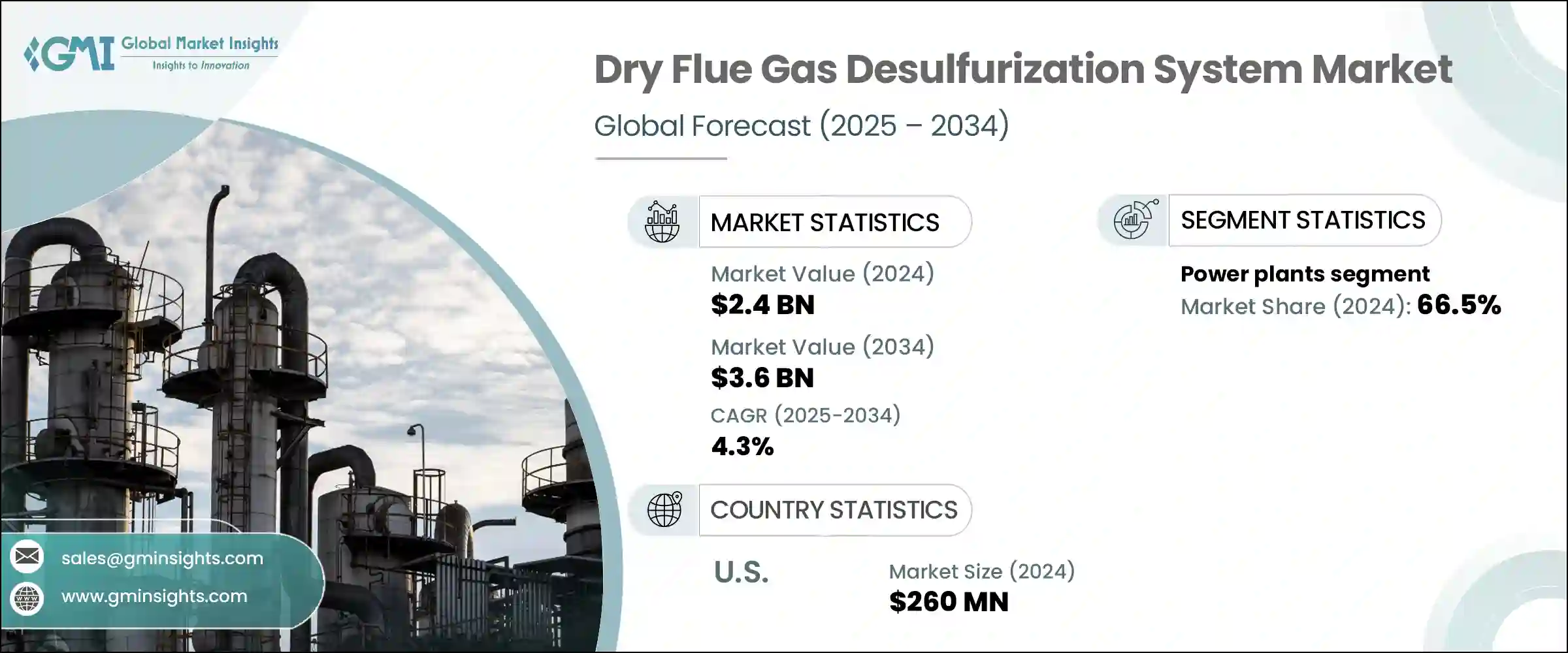

乾式排煙脱硫装置の世界市場規模は、2024年に24億米ドルとなり、CAGR 4.3%で成長し、2034年には36億米ドルに達すると予測されています。

市場成長の原動力となっているのは、環境規制の強化や世界のクリーン生産の推進によって、効率的な二酸化硫黄(SO2)排出抑制に対する産業界の需要が高まっていることです。これらの乾式FGD技術は、水消費量の削減、システムの複雑性の軽減、既存インフラへの統合の簡素化など、いくつかの利点を提供します。発電、化学製造、セメント製造、金属加工などの業界では、コンプライアンスや持続可能性戦略の一環として、こうしたシステムの導入が増加しています。

乾式脱硫システムの性能と信頼性は、技術的なアップグレードによって改善され続けており、生産性を損なうことなく排出量の削減を目指す企業にとって好ましい選択肢となっています。大気汚染削減を求める世論と規制の圧力が高まる中、新興経済諸国の産業界では、乾式脱硫装置に対する需要が高まっています。乾式脱硫技術のコンパクトな設計とモジュール機能により、既存施設の改造は容易になっています。欧州や北米のような地域では、特に規制遵守と環境性能が優先されるため、強力な政策施行とグリーンイニシアティブが普及につながっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 24億米ドル |

| 予測金額 | 36億米ドル |

| CAGR | 4.3% |

用途別では、発電分野が2024年に66.5%の最大市場シェアを占め、2034年までのCAGRは3.6%と予測されます。この成長は主に、古い石炭ベースのプラントを迅速かつコスト効率よく改修する必要がある、積極的な排出義務化によってもたらされます。乾式脱硫システムは、水の使用量を最小限に抑え、設計を合理化し、設置期間を短縮する理想的なシステムです。特に、世界のエネルギー転換が進む中、土木工事やプラントのオーバーホールに多額の投資をすることなく、排出基準を満たすことができます。

米国乾式排煙脱硫装置2024年の市場規模は2億6,000万米ドル。同市場の好調は、厳格なEPA規制と工業プロセスにおける硫黄排出削減の重視に支えられています。乾式脱硫技術は、その節水機能、既存の排ガス流路への設置の容易さ、アップグレード時の運転中断の減少により、この市場で際立っています。環境に関する説明責任が強化される中、これらのシステムは、米国産業が効率的にコンプライアンス要件を満たす上で重要な役割を果たしています。

乾式排煙脱硫装置市場を形成する有力企業には、 Mitsubishi Heavy Industries、GE Vernova、CECO Environmental、Babcock &Wilcox Enterprisesなどがあります。乾式排煙脱硫装置市場の各企業は、エネルギー生産者とのパートナーシップの形成、ターンキーの改造ソリューションの提供、デジタルモニタリングや予知保全ツールを含むサービスポートフォリオの拡大といった戦略的イニシアティブに注力しています。

モジュール式のシステム設計や水効率の高い技術を優先することで、企業は水の乏しい地域で操業する産業の現実的なニーズに対応しています。研究開発への投資は、システム効率の向上、エネルギー消費の削減、SO2回収率の向上を目指しています。メーカーはまた、産業が拡大し、大気質規制が厳しくなっている新興市場をターゲットとして、世界の足跡を広げています。自動化とスマート制御の統合を活用することで、これらの企業は、業界固有の排出規制基準や運用上の制約に沿った、よりカスタマイズされたコンプライアンス対応ソリューションを提供できるようになっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 発電所

- 化学・石油化学

- セメント

- 金属加工・鉱業

- 製造業

- その他

第6章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- チリ

- アルゼンチン

第7章 企業プロファイル

- Babcock &Wilcox Enterprises

- CECO Environmental

- Duconenv

- GE Vernova

- GEA Group Aktiengesellschaft

- Hitachi Zosen Inova AG

- John Cockerill

- KC Cottrell India

- MET

- Mitsubishi Heavy Industries

- Nederman Holding AB

- Thermax Limited.

- Tri-Mer Corporation

- Valmet

- Verantis Environmental Solutions Group

The Global Dry Flue Gas Desulfurization System Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 4.3% to reach USD 3.6 billion by 2034. The market growth is fueled by increasing industrial demand for efficient sulfur dioxide (SO2 ) emission control, driven by tightening environmental regulations and the global push toward cleaner production. These dry FGD technologies provide several advantages, including low water consumption, reduced system complexity, and simplified integration into existing infrastructure. Industries such as power generation, chemical manufacturing, cement production, and metal processing are increasingly installing these systems as part of compliance and sustainability strategies.

Technological upgrades continue to improve the performance and reliability of dry FGD systems, making them a preferred choice for businesses aiming to lower emissions without compromising productivity. As public and regulatory pressure mounts to cut air pollution, industries in fast-developing economies are seeing growing demand for these systems. Retrofitting existing facilities has become easier due to the compact design and modular capabilities of dry FGD technologies. In regions like Europe and North America, strong policy enforcement and green initiatives are leading to widespread adoption, especially where regulatory compliance and environmental performance are prioritized.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 4.3% |

In terms of application, the power generation segment held the largest market share at 66.5% in 2024 and is projected to grow at a CAGR of 3.6% through 2034. This growth is primarily driven by aggressive emission mandates that require older coal-based plants to be retrofitted quickly and cost-effectively. Dry FGD systems remain an ideal fit, offering minimal water usage, streamlined design, and quicker installation timelines. Their scalable, modular nature provides utilities with the flexibility to meet emission standards without heavy investment in civil engineering or plant overhaul, especially amid a broader global energy transition.

United States Dry Flue Gas Desulfurization System Market generated USD 260 million in 2024. The market's strength is supported by rigorous EPA regulations and a strong emphasis on reducing sulfur emissions in industrial processes. Dry FGD technologies stand out in this market for their water-saving features, ease of installation in pre-existing flue gas channels, and reduced operational interruptions during upgrades. As environmental accountability intensifies, these systems are playing a vital role in helping U.S. industries meet compliance requirements with efficiency.

Prominent players shaping the Dry Flue Gas Desulfurization System Market include Mitsubishi Heavy Industries, GE Vernova, CECO Environmental, and Babcock & Wilcox Enterprises. Companies in the dry flue gas desulfurization system market are focusing on strategic initiatives such as forming partnerships with energy producers, offering turnkey retrofit solutions, and expanding service portfolios to include digital monitoring and predictive maintenance tools.

By prioritizing modular system designs and water-efficient technologies, firms are addressing the practical needs of industries operating in water-scarce regions. Investments in R&D aim to enhance system efficiency, reduce energy consumption, and improve SO2 capture rates. Manufacturers are also expanding their global footprints by targeting emerging markets with industrial expansion and strict air quality regulations. Leveraging automation and smart control integration has allowed these companies to deliver more tailored, compliance-ready solutions that align with industry-specific emission control standards and operational constraints.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategy dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034, (USD Billion)

- 5.1 Key trends

- 5.2 Power plants

- 5.3 Chemical & petrochemical

- 5.4 Cement

- 5.5 Metal processing & mining

- 5.6 Manufacturing

- 5.7 Others

Chapter 6 Market Size and Forecast, By Region, 2021 - 2034, (USD Billion)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 UK

- 6.3.3 France

- 6.3.4 Spain

- 6.3.5 Italy

- 6.3.6 Netherlands

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 South Korea

- 6.4.5 Australia

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 UAE

- 6.5.3 South Africa

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Chile

- 6.6.3 Argentina

Chapter 7 Company Profiles

- 7.1 Babcock & Wilcox Enterprises

- 7.2 CECO Environmental

- 7.3 Duconenv

- 7.4 GE Vernova

- 7.5 GEA Group Aktiengesellschaft

- 7.6 Hitachi Zosen Inova AG

- 7.7 John Cockerill

- 7.8 KC Cottrell India

- 7.9 MET

- 7.10 Mitsubishi Heavy Industries

- 7.11 Nederman Holding AB

- 7.12 Thermax Limited.

- 7.13 Tri-Mer Corporation

- 7.14 Valmet

- 7.15 Verantis Environmental Solutions Group