|

市場調査レポート

商品コード

1666924

排煙脱硫装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Flue Gas Desulfurization System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 排煙脱硫装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2024年12月09日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

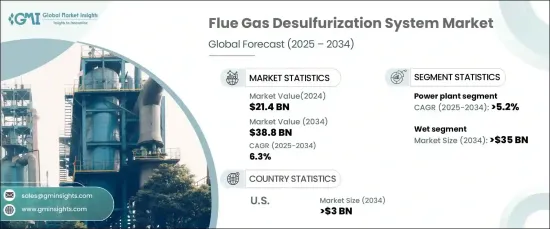

排煙脱硫装置の世界市場は、2024年に214億米ドルとなり、2025年から2034年にかけて6.3%の安定したCAGRで成長すると予測されています。

エネルギー需要の増大は産業排出物の増加を招き、重大な環境課題の一因となっています。発電所や工業施設による大気汚染への懸念が高まる中、世界各国の政府や政策立案者は、より厳格な排出規制対策を重視しています。

新たな製造施設や産業拠点の設立による産業活動の急速な拡大は、強固な環境規制の導入の緊急性をさらに際立たせています。産業活動の激化に伴い、二酸化硫黄(SO2)のような有害汚染物質の排出が増加しており、排煙脱硫装置のような高度な排出制御技術の必要性が浮き彫りになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 214億米ドル |

| 予測金額 | 388億米ドル |

| CAGR | 6.3% |

湿式排煙脱硫装置の市場は、2034年までに350億米ドルを超えると予測されています。これらのシステムは、産業排出物から二酸化硫黄と粒子状物質を削減するのに非常に効率的であるため、進化する環境基準への準拠を目指す産業に人気のある選択肢となっています。大気汚染物質と廃水汚染物質の両方を管理する湿式FGDシステムの有効性は、エネルギー多消費セクターにおける重要なソリューションとして位置づけられています。

FGDシステムは発電用途でも人気を集めており、この分野は2034年までにCAGR5.2%以上の成長が見込まれています。経済開発と工業化によって電力需要が増加し続ける中、排出レベルを抑制するための先進技術の採用が不可欠となっています。排煙脱硫装置は、二酸化硫黄の排出を削減し、発電所における厳しい環境ガイドラインの遵守を確保する上で不可欠です。

米国では、排煙脱硫装置市場は2034年までに30億米ドルを超えると予想されています。政府のイニシアティブと資金援助に支えられた排出抑制技術への投資が、市場の成長を後押ししています。こうした進歩は、高度なシステムの導入コストの低減に役立ち、普及への道を開いています。

アジア太平洋では、エネルギーインフラと排出制御技術の統合に向けた取り組みが、排煙脱硫装置の導入を加速させています。協力的な地域的アプローチと産業拠点への重点的な取り組みが大気汚染削減の進展を促し、同地域での市場の成長を支えています。この戦略により、世界的に排煙脱硫装置の採用がさらに進むと予想されます。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 市場推計・予測パラメータ

- 予測計算

- データソース

- 一次

- 二次

- 有料

- 公的

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム分析

- 規制状況

- 業界への影響要因

- 成長促進要因

- 業界の潜在的リスク・課題

- 成長可能性分析

- ポーター分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- 湿式

- 乾式

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 発電所

- 化学・石油化学

- セメント

- 金属加工・鉱業

- 製造業

- その他

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- インドネシア

- オーストラリア

- ベトナム

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ナイジェリア

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

第8章 企業プロファイル

- Alstom

- Andritz

- Babcock &Wilcox

- Beijing SPC Environment Protection Tech

- Chiyoda

- Doosan Enerbility

- Ducon Infratechnologies

- FLSmidth

- General Electric

- Hamon

- Ljungstrom

- Longking Environmental Protection

- Marsulex Environmental Technologies

- Mitsubishi Heavy Industries

- Thermax

- Valmet

The Global Flue Gas Desulfurization System Market, valued at USD 21.4 billion in 2024, is anticipated to grow at a steady CAGR of 6.3% from 2025 to 2034. The increasing energy demand has led to a rise in industrial emissions, contributing to significant environmental challenges. With growing concerns over air pollution caused by power plants and industrial facilities, governments and policymakers worldwide are emphasizing stricter emission control measures.

The rapid expansion of industrial activities, driven by the establishment of new manufacturing facilities and industrial hubs, has further underscored the urgency of implementing robust environmental regulations. As industrial operations intensify, emissions of harmful pollutants such as sulfur dioxide (SO2) have escalated, highlighting the critical need for advanced emission control technologies like FGD systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.4 Billion |

| Forecast Value | $38.8 Billion |

| CAGR | 6.3% |

The market for wet FGD systems is projected to surpass USD 35 billion by 2034. These systems are highly efficient in reducing sulfur dioxide and particulate matter from industrial emissions, making them a popular choice for industries aiming to comply with evolving environmental standards. The effectiveness of wet FGD systems in managing both air and wastewater pollutants has positioned them as a key solution in energy-intensive sectors.

FGD systems are also gaining traction in power generation applications, with this segment expected to grow at a CAGR of over 5.2% by 2034. As the electricity demand continues to rise, driven by economic development and industrialization, the adoption of advanced technologies to curb emission levels has become essential. FGD systems are vital in reducing sulfur dioxide emissions and ensuring adherence to stringent environmental guidelines in power plants.

In the United States, the FGD system market is expected to exceed USD 3 billion by 2034. Investments in emission control technologies, supported by government initiatives and funding, are driving market growth. These advancements are helping to lower the costs of deploying sophisticated systems, paving the way for widespread adoption.

In the Asia Pacific, efforts to integrate energy infrastructure with emission control technologies are accelerating the deployment of FGD systems. Collaborative regional approaches and a focus on industrial hubs are fostering progress toward reducing air pollution, supporting the market's growth in the region. This strategy is expected to drive further advancements in the adoption of FGD systems globally.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Wet

- 5.3 Dry

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Power Plants

- 6.3 Chemical & petrochemical

- 6.4 Cement

- 6.5 Metal Processing & mining

- 6.6 Manufacturing

- 6.7 Others

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Indonesia

- 7.4.6 Australia

- 7.4.7 Vietnam

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.5.4 Nigeria

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 Alstom

- 8.2 Andritz

- 8.3 Babcock & Wilcox

- 8.4 Beijing SPC Environment Protection Tech

- 8.5 Chiyoda

- 8.6 Doosan Enerbility

- 8.7 Ducon Infratechnologies

- 8.8 FLSmidth

- 8.9 General Electric

- 8.10 Hamon

- 8.11 Ljungstrom

- 8.12 Longking Environmental Protection

- 8.13 Marsulex Environmental Technologies

- 8.14 Mitsubishi Heavy Industries

- 8.15 Thermax

- 8.16 Valmet