|

市場調査レポート

商品コード

1766351

薬物スクリーニングの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Drug Screening Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 薬物スクリーニングの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月04日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

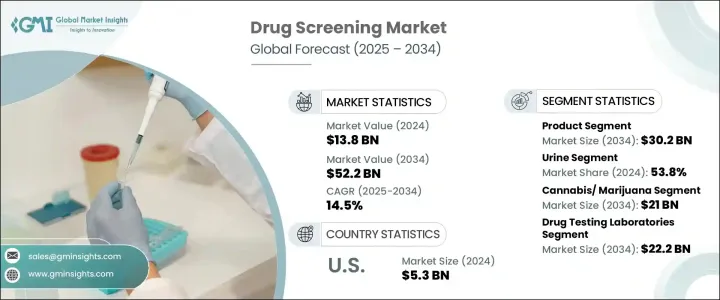

世界の薬物スクリーニング市場は2024年に138億米ドルと評価され、CAGR 14.5%で成長し、2034年には522億米ドルに達すると推定されています。

この成長の背景には、薬物乱用問題への取り組みへの注目の高まり、薬物検査技術の進歩、雇用、スポーツ、ヘルスケアなど様々な分野における政策の厳格化があります。世界各国の政府は薬物乱用撲滅への取り組みを強化しており、これが効果的なスクリーニング・ソリューションに対する市場の需要をさらに促進しています。

液体クロマトグラフィー質量分析(LC-MS)やイムノアッセイのような最先端技術は、薬物スクリーニングプロセスの精度と効率を大幅に向上させています。さらに、迅速スクリーニングキットやオンサイト検査装置へのアクセスが容易になったことで、プロセスがより便利になり、結果に要する時間が短縮されています。これにより、薬物スクリーニングソリューションは、特に「薬物のない職場法(Drug-Free Workplace Act)」のような規制の下で、職場の安全とコンプライアンスに不可欠なものとなり、市場拡大の原動力となっています。

| 市場規模 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 138億米ドル |

| 予測金額 | 522億米ドル |

| CAGR | 14.5% |

薬物スクリーニングでは、血液、尿、毛髪、唾液、汗などの生体サンプルを検査して薬物やその代謝物を検出します。市場には、免疫測定分析装置、クロマトグラフィーシステム、呼気分析装置、経口液検査キット、迅速検査装置などの検査機器を含む、薬物検出用に設計された幅広いツールとサービスが含まれます。検査室でのスクリーニングと現場でのスクリーニングの両方が、この業界で一般的に用いられている方法です。

製品セグメントは市場の最大シェアを占め、2024年の市場規模は81億米ドルでした。このセグメントには、免疫測定分析装置、クロマトグラフィー装置、呼気分析装置など、正確で信頼性の高い結果を出す上で極めて重要なツールが含まれます。迅速検査装置は、その携帯性、使いやすさ、即座に結果を出す能力から特に需要が高く、職場や緊急検査シナリオでの使用に理想的です。サンプル採取キット、キャリブレーション・キット、コントロール・デバイスなどの消耗品も、使用頻度が高く定期的な補充が必要なため、需要が高いです。

尿ベースの薬物検査セグメントは2024年に53.8%の最大シェアを占め、予測期間中にさらなる成長が見込まれます。尿検査は、その費用対効果、信頼性、幅広い物質の検出能力により、依然として最も広く使用されている方法です。代謝物は尿中に排泄されるため、最近の薬物使用を特定するための理想的なサンプルとなります。尿検査は、職場の薬物検査、雇用前スクリーニング、リハビリテーション・プログラムに一般的に使用されています。非侵襲的な採取方法と、カンナビノイド、オピオイド、アンフェタミン、ベンゾジアゼピンなどの物質を検出する能力により、薬物乱用管理プログラムには欠かせないものとなっています。

北米の薬物スクリーニング2024年の市場規模は59億米ドルで、2034年には212億米ドルに達し、CAGR 14%で成長すると予測されています。北米は、厳しい規制要件、技術革新、職場の安全に対する高い意識が市場を牽引しています。米国では、運輸省(DOT)や薬物乱用・精神衛生管理局(SAMHSA)などによる規制の枠組みがあり、運輸、ヘルスケア、政府などさまざまな業界で薬物検査が義務付けられています。

薬物スクリーニング世界市場の主要企業には、アボット、アジレント、ドラッガーワーク、ラボラトリー・コーポレーション・オブ・アメリカ(LabCorp)、クエスト・ダイアグノスティックス、サーモフィッシャーサイエンティフィック、F.ホフマン・ラ・ロシュ、ライフロック・テクノロジーズなどがあります。これらの企業は合計で市場シェアのかなりの部分を占めており、技術革新の推進、規制遵守、効率的な薬物検査技術の開発に貢献しています。市場での地位を高めるため、薬物スクリーニング市場の企業はいくつかの戦略に注力しています。大手企業は研究開発に多額の投資を行い、検査技術の革新と精度・スピードの向上を図っています。また、ヘルスケア、雇用、法執行機関など幅広い業界に対応するため、製品ポートフォリオを拡大しています。研究機関や他の企業との戦略的提携や協力関係も、市場拡大のために形成されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 薬物とアルコールの消費量の増加

- 薬物スクリーニングをサポートする厳格な法律の存在

- 薬物乱用検査のための製品とサービスの入手可能性の増加

- 業界の潜在的リスク&課題

- 職場での薬物検査の禁止

- 訓練を受けた研究室専門家の不足

- 市場機会

- 職場における薬物検査ポリシーの導入増加

- 新興諸国における意識の高まりと政策の施行

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーとイノベーションの情勢

- ギャップ分析

- 薬物スクリーニング製品・サービス別のボリューム分析、2024年

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 製品・サービス別企業シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 拡張計画

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- 製品

- 分析機器

- 免疫測定分析装置

- クロマトグラフィー分析装置

- 呼気分析装置

- 口腔液検査分析装置

- 迅速検査装置

- 消耗品

- 分析機器

- 薬物スクリーニングサービス

第6章 市場推計・予測:サンプルタイプ別、2021年~2034年

- 主要動向

- 尿

- 呼吸

- 経口補水液

- 髪

- その他のサンプルタイプ

第7章 市場推計・予測:薬物タイプ別、2021年~2034年

- 主要動向

- 大麻/マリファナ

- オピオイド

- アルコール

- アンフェタミン

- その他の薬物タイプ

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 薬物検査機関

- 職場

- 病院

- 法執行機関

- その他の用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Abbott

- Agilent

- Alcohol Countermeasure Systems

- Alfa Scientific Designs

- Dragerwerk

- Eurofins Scientific

- F. Hoffmann-La Roche

- Laboratory Corporation of America(LabCorp)

- Lifeloc Technologies

- Omega Laboratories

- OraSure Technologies

- PerkinElmer

- Premier Biotech

- Psychemedics

- Quest Diagnostics

- Shimadzu

- Siemens Healthineers

- Thermo Fisher Scientific

The Global Drug Screening Market was valued at USD 13.8 billion in 2024 and is estimated to grow at a CAGR of 14.5% to reach USD 52.2 billion by 2034. This growth can be attributed to an increasing focus on addressing substance abuse issues, advancements in drug testing technologies, and the rise of stricter policies in various sectors, including employment, sports, and healthcare. Governments worldwide are intensifying efforts to combat drug abuse, which is further spurring market demand for effective screening solutions.

Cutting-edge technologies like liquid chromatography-mass spectrometry (LC-MS) and immunoassays have significantly improved the accuracy and efficiency of drug screening processes. Moreover, the rise in accessibility to rapid screening kits and on-site testing devices is making the process more convenient and reducing the time required for results. This has made drug screening solutions indispensable for workplace safety and compliance, especially under regulations like the Drug-Free Workplace Act, which has become a driving force behind the market's expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.8 Billion |

| Forecast Value | $52.2 Billion |

| CAGR | 14.5% |

Drug screening involves testing biological samples such as blood, urine, hair, saliva, or sweat to detect drugs or their metabolites. The market encompasses a wide range of tools and services designed for drug detection, including testing devices such as immunoassay analyzers, chromatography systems, breath analyzers, oral fluid testing kits, and rapid test devices. Both laboratory and on-site screenings are common methods used in the industry.

The product segment accounted for the largest share of the market, valued at USD 8.1 billion in 2024. This segment includes essential tools such as immunoassay analyzers, chromatographic instruments, and breath analyzers, which are pivotal in delivering accurate and reliable results. Rapid testing devices are particularly in demand due to their portability, ease of use, and ability to provide immediate results, which makes them ideal for use in workplace and emergency testing scenarios. Consumables like sample collection kits, calibration kits, and control devices are also in high demand, as they are used frequently and require regular replenishment.

The urine-based drug testing segment held the largest share of 53.8% in 2024, with further growth anticipated during the forecast period. Urine testing remains the most widely used method due to its cost-effectiveness, reliability, and ability to detect a broad range of substances. Since metabolites are excreted in urine, it serves as an ideal sample for identifying recent drug use. Urine tests are commonly used for workplace drug testing, pre-employment screenings, and rehabilitation programs. Their non-invasive collection method and ability to detect substances like cannabinoids, opioids, amphetamines, and benzodiazepines make them indispensable in substance abuse management programs.

North America Drug Screening Market generated USD 5.9 billion in 2024 and is projected to reach USD 21.2 billion by 2034, growing at a CAGR of 14%. North America leads the market, driven by stringent regulatory requirements, technological innovations, and high awareness of workplace safety. The regulatory framework in the U.S., including mandates by the Department of Transportation (DOT) and the Substance Abuse and Mental Health Services Administration (SAMHSA), requires drug testing in various industries, including transportation, healthcare, and government.

Key players in the Global Drug Screening Market include companies such as Abbott, Agilent, Dragerwerk, Laboratory Corporation of America (LabCorp), Quest Diagnostics, Thermo Fisher Scientific, F. Hoffmann-La Roche, and Lifeloc Technologies. These companies collectively hold a substantial portion of the market share and are instrumental in driving innovation, regulatory compliance, and developing efficient drug testing technologies. To enhance their market position, companies in the drug screening market focus on several strategies. Leading players are heavily investing in research and development to innovate and improve the accuracy and speed of testing technologies. They are also expanding their product portfolios to cater to a wide range of industries, including healthcare, employment, and law enforcement. Strategic partnerships and collaborations with research institutions and other businesses are also being formed to expand their market reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Sample type

- 2.2.4 Drug type

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing drug and alcohol consumption

- 3.2.1.2 Presence of stringent laws to support drug screening

- 3.2.1.3 Growing availability of products and services for drug-of abuse testing

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Prohibition on workplace drug testing

- 3.2.2.2 Dearth of trained laboratory professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Growing adoption of drug testing policies in workplaces

- 3.2.3.2 Rising awareness and policy enforcement in developing countries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology and innovation landscape

- 3.6 Gap analysis

- 3.7 Drug screening volume analysis, by product and service, 2024

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 MEA

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company share analysis, by product and service

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Product

- 5.2.1 Analytical instruments

- 5.2.1.1 Immunoassay analyzers

- 5.2.1.2 Chromatographic analyzers

- 5.2.1.3 Breath analyzers

- 5.2.1.4 Oral fluid testing analyzers

- 5.2.2 Rapid testing devices

- 5.2.3 Consumables

- 5.2.1 Analytical instruments

- 5.3 Drug screening services

Chapter 6 Market Estimates and Forecast, By Sample Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Urine

- 6.3 Breath

- 6.4 Oral fluids

- 6.5 Hair

- 6.6 Other sample types

Chapter 7 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Cannabis/ marijuana

- 7.3 Opiods

- 7.4 Alcohol

- 7.5 Amphetamines

- 7.6 Other drug types

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Drug testing laboratories

- 8.3 Workplace

- 8.4 Hospitals

- 8.5 Law enforcement agencies

- 8.6 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott

- 10.2 Agilent

- 10.3 Alcohol Countermeasure Systems

- 10.4 Alfa Scientific Designs

- 10.5 Dragerwerk

- 10.6 Eurofins Scientific

- 10.7 F. Hoffmann-La Roche

- 10.8 Laboratory Corporation of America (LabCorp)

- 10.9 Lifeloc Technologies

- 10.10 Omega Laboratories

- 10.11 OraSure Technologies

- 10.12 PerkinElmer

- 10.13 Premier Biotech

- 10.14 Psychemedics

- 10.15 Quest Diagnostics

- 10.16 Shimadzu

- 10.17 Siemens Healthineers

- 10.18 Thermo Fisher Scientific