|

市場調査レポート

商品コード

1766312

使い捨て失禁用品の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Disposable Incontinence Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 使い捨て失禁用品の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月03日

発行: Global Market Insights Inc.

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

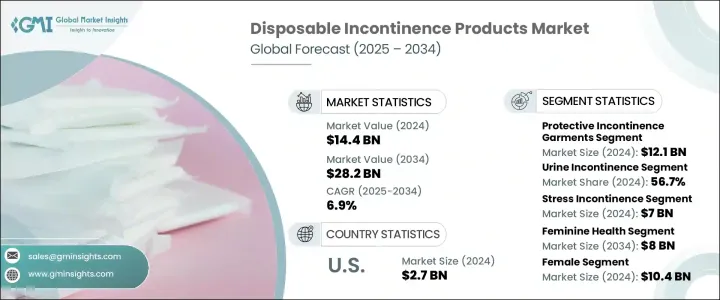

世界の使い捨て失禁用品市場は、2024年に144億米ドルと評価され、CAGR 6.9%で成長し、2034年には282億米ドルに達すると推定されています。

この一貫した市場拡大の背景には、尿失禁を経験する人の増加、治療や管理オプションに関する意識の高まり、メーカーによる継続的な製品の進歩があります。企業は、吸収性や皮膚適合性が高いだけでなく、生分解性もある素材の革新を優先しており、ヘルスケアの有効性と環境への責任の両方に合致しています。さらに、eコマースの発展により購入プロセスが簡素化され、ユーザーは目立たずに製品を入手できるようになりました。このような利便性、機能性、アクセシビリティの組み合わせは、病院から家庭環境まで、さまざまなケア環境での需要を加速させ、市場全体の成長軌道に寄与しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 144億米ドル |

| 予測金額 | 282億米ドル |

| CAGR | 6.9% |

使い捨て失禁ソリューションは、吸収パッド、大人用ブリーフ、保護衣などの製品を通じて、不随意的な膀胱や腸の漏れを管理できるように設計されています。これらの製品は、特に高齢者、術後患者、慢性失禁患者にとって、快適性、尊厳、衛生を高めるものです。使用と廃棄が簡単な設計で、臨床と在宅ケアの両方のニーズに対応し、確実な吸収と最小限の不快感を提供します。

保護用失禁衣服セグメントは市場をリードし、その幅広い採用と使いやすさから、2024年には121億米ドルと評価されました。これらの衣服は、信頼できる性能と快適性により、病院、長期介護センター、家庭で好まれています。吸収性が高く、衛生的で漏れにくい構造は、利用者が活動的で自信に満ちたライフスタイルを維持するのに役立ちます。また、失禁の重症度レベルに対応するため、複数の形態で販売されており、患者と介護者の双方への訴求力を高めています。

尿失禁分野は2024年に56.7%のシェアを占めました。高齢化社会における尿失禁の高い有病率と持続性は、製品需要に大きく寄与しています。長引く尿漏れのエピソードを管理するには効果的なソリューションが必要であり、使い捨て失禁用品は実用的で衛生的なオプションを提供しています。このような健康上の懸念を抱える高齢者の数が増加していることが、このセグメントの市場での存在感を高めています。

米国の使い捨て失禁用品市場は2024年に27億米ドルと評価されました。ストレス性尿失禁の症例が特に高齢女性の間で増加しており、製品需要を押し上げています。更年期、肥満、出産などの要因が骨盤底の合併症の一因となっており、女性が治療を求めるようになっています。高度なヘルスケア施設の利用可能性、骨盤の健康に対する意識の高まり、有利な償還制度が、同国の市場拡大をさらに後押ししています。

使い捨て失禁用品の世界市場における主要企業は、Essity、BD、Coloplast、CardinalHealth、B Braun、Ontex、Attends、FUBURG、UROCARE、MEDLINE、Kimberly-Clark、cobaTec、ABENA、unicharm、Hollisterなどです。使い捨て失禁用品分野の企業は、製品革新、持続可能性、流通拡大に注力することで、市場での地位を高めています。多くの企業が研究開発に投資し、環境に優しい素材、消臭技術、超薄型・高吸収製品を開発することで、ユーザーの快適さと慎重さを高めています。高齢化社会の進化するニーズに対応するため、各社は失禁の程度に合わせた製品ラインを発売しています。ヘルスケアプロバイダーや介護者との戦略的提携は、早期の採用促進に役立っています。さらに各社は、現代の消費者の嗜好に合った定期購入型モデルや目立たない配送サービスを提供するため、オンラインでのプレゼンス拡大を図っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 世界中で失禁の有病率が増加

- 政府による支援的な償還政策

- 慢性疾患の発生率の増加と高齢者人口の増加

- 最近の技術進歩と新製品開発

- 業界の潜在的リスク&課題

- 新興国における認知度と製品の入手性の欠如

- 市場機会

- 在宅ヘルスケアとeコマースの流通チャネルの拡大

- 持続可能性を重視した生分解性と環境に優しいソリューション

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- 世界のその他の地域

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- 償還シナリオ

- 償還政策が市場成長に与える影響

- 消費者行動分析

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 世界

- 北米

- 欧州

- 世界のその他の地域

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 失禁保護用衣類

- 使い捨て防護下着

- 使い捨て大人用おむつ

- 布製大人用おむつ

- 使い捨てパッドとライナー

- 男性用保護用品

- 膀胱コントロールパッド

- 失禁ライナー

- ベルト付きとベルトなしの下着

- 使い捨てアンダーパッド

- 尿道カテーテル

- 留置カテーテル(フォーリーカテーテル)

- 間欠カテーテル

- 外部カテーテル

- 尿バッグ

- 脚用尿バッグ

- ベッドサイド尿バッグ

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 尿失禁

- 便失禁

- 二重失禁

第7章 市場推計・予測:失禁タイプ別、2021年~2034年

- 主要動向

- ストレス

- 混合

- 衝動

- その他の失禁タイプ

第8章 市場推計・予測:病気別、2021年~2034年

- 主要動向

- 女性の健康

- 妊娠と出産

- 閉経

- 子宮摘出術

- その他の女性の健康疾患

- 慢性疾患

- 精神障害

- 良性前立腺肥大症

- 膀胱がん

- その他の病気

第9章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 綿織物

- 超吸収剤

- プラスチック

- ラテックス

- その他の材料

第10章 市場推計・予測:男女別、2021年~2034年

- 主要動向

- 女性

- 男性

第11章 市場推計・予測:年齢別、2021年~2034年

- 主要動向

- 20歳未満

- 20歳~39歳

- 40歳~59歳

- 60歳~79歳

- 80歳以上

第12章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 小売店

- eコマース

第13章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 介護施設

- 長期ケアセンター

- 外来手術センター

- その他の最終用途

第14章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第15章 企業プロファイル

- ABENA

- Attends

- B Braun

- BD

- CardinalHealth

- Coloplast

- convaTec

- essity

- FUBURG

- Hollister

- Kimberly-Clark

- MEDLINE

- Ontex

- unicharm

- UROCARE

The Global Disposable Incontinence Products Market was valued at USD 14.4 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 28.2 billion by 2034.

This consistent market expansion is fueled by the growing number of individuals experiencing urinary incontinence, rising awareness regarding treatment and management options, and continuous product advancements by manufacturers. Companies are prioritizing innovation in materials that are not only highly absorbent and skin-compatible but also biodegradable, aligning with both healthcare efficacy and environmental responsibility. In addition, the growth of e-commerce has simplified purchasing processes, enabling users to obtain products discreetly. This combination of convenience, functionality, and accessibility is accelerating demand across multiple care settings, from hospitals to home environments, contributing to the overall growth trajectory of the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.4 Billion |

| Forecast Value | $28.2 Billion |

| CAGR | 6.9% |

Disposable incontinence solutions are designed to help individuals manage involuntary bladder or bowel leakage through products such as absorbent pads, adult briefs, and protective garments. These items enhance comfort, dignity, and hygiene, especially for elderly users, post-surgical patients, and people with chronic incontinence. Designed for easy use and disposal, they serve both clinical and home care needs, offering reliable absorption and minimal discomfort.

The protective incontinence garments segment led the market and was valued at USD 12.1 billion in 2024, owing to its wide adoption and ease of use. These garments are preferred across hospitals, long-term care centers, and homes due to their reliable performance and comfort. Their absorbent, hygienic, and leak-resistant structure helps users maintain an active and confident lifestyle. They are available in multiple formats to address varying severity levels of incontinence, which enhances their appeal to both patients and caregivers.

Urine incontinence segment held a 56.7% share in 2024. Its high prevalence and persistent nature across aging populations significantly contribute to product demand. Effective solutions are necessary to manage prolonged episodes of urine leakage, with disposable incontinence products offering a practical and hygienic option. The growing number of elderly individuals dealing with such health concerns continues to boost the segment's prominence in the market.

United States Disposable Incontinence Products Market was valued at USD 2.7 billion in 2024. Increasing cases of stress urinary incontinence, especially among aging women, are pushing product demand. Factors such as menopause, obesity, and childbirth have contributed to pelvic floor complications, prompting women to seek treatment. The availability of advanced healthcare facilities, greater pelvic health awareness, and favorable reimbursement systems are further supporting market expansion in the country.

Key players in the Global Disposable Incontinence Products Market include Essity, BD, Coloplast, CardinalHealth, B Braun, Ontex, Attends, FUBURG, UROCARE, MEDLINE, Kimberly-Clark, convaTec, ABENA, unicharm, and Hollister. Companies in the disposable incontinence products space are enhancing their market position by focusing on product innovation, sustainability, and distribution expansion. Many are investing in R&D to develop eco-friendly materials, odor-control technology, and ultra-thin, high-absorption products that increase user comfort and discretion. To meet the evolving needs of aging populations, players are launching tailored product lines catering to different levels of incontinence severity. Strategic collaborations with healthcare providers and caregivers help promote early adoption. Additionally, firms are expanding their online presence to offer subscription-based models and discreet delivery services, which resonate with modern consumer preferences.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 Incontinence type

- 2.2.5 Disease

- 2.2.6 Material

- 2.2.7 Gender

- 2.2.8 Age group

- 2.2.9 Distribution channel

- 2.2.10 End Use

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of incontinence across the globe

- 3.2.1.2 Supportive reimbursement policies by governments

- 3.2.1.3 Increasing incidence of chronic diseases coupled with rising elderly population

- 3.2.1.4 Recent technological advancements and new product developments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of awareness and product availability in emerging countries

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of home healthcare and e-commerce distribution channels

- 3.2.3.2 Sustainability-driven biodegradable and eco-friendly solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Rest of the world

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.8.1 Impact of reimbursement policies on market growth

- 3.9 Consumer behaviour analysis

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Rest of the world

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Protective incontinence garments

- 5.2.1 Disposable protective underwear

- 5.2.2 Disposable adult diaper

- 5.2.3 Cloth adult diaper

- 5.2.4 Disposable pads and liners

- 5.2.4.1 Male guards

- 5.2.4.2 Bladder control pads

- 5.2.4.3 Incontinence liners

- 5.2.4.3.1 Belted and beltless undergarments

- 5.2.4.3.2 Disposable under pads

- 5.3 Urinary catheter

- 5.3.1 Indwelling (foley) catheter

- 5.3.2 Intermittent catheter

- 5.3.3 External catheter

- 5.4 Urine bag

- 5.4.1 Leg urine bag

- 5.4.2 Bedside urine bag

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Urine incontinence

- 6.3 Fecal incontinence

- 6.4 Dual incontinence

Chapter 7 Market Estimates and Forecast, By Incontinence Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Stress

- 7.3 Mixed

- 7.4 Urge

- 7.5 Other incontinence types

Chapter 8 Market Estimates and Forecast, By Disease, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Feminine health

- 8.2.1 Pregnancy and childbirth

- 8.2.2 Menopause

- 8.2.3 Hysterectomy

- 8.2.4 Other feminine health diseases

- 8.3 Chronic disease

- 8.4 Mental disorders

- 8.5 Benign prostatic hyperplasia

- 8.6 Bladder cancer

- 8.7 Other diseases

Chapter 9 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Cotton fabrics

- 9.3 Super absorbents

- 9.4 Plastic

- 9.5 Latex

- 9.6 Other materials

Chapter 10 Market Estimates and Forecast, By Gender, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Female

- 10.3 Male

Chapter 11 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 40 to 59 years

- 11.3 60 to 79 years

- 11.4 20 to 39 years

- 11.5 Below 20 years

- 11.6 80+ years

Chapter 12 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 12.1 Key trends

- 12.2 Retail stores

- 12.3 E-commerce

Chapter 13 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 13.1 Key trends

- 13.2 Hospital

- 13.3 Nursing facilities

- 13.4 Long-term care centers

- 13.5 Ambulatory surgical centers

- 13.6 Other end users

Chapter 14 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 14.1 Key trends

- 14.2 North America

- 14.2.1 U.S.

- 14.2.2 Canada

- 14.3 Europe

- 14.3.1 Germany

- 14.3.2 UK

- 14.3.3 France

- 14.3.4 Spain

- 14.3.5 Italy

- 14.3.6 Netherlands

- 14.4 Asia Pacific

- 14.4.1 China

- 14.4.2 Japan

- 14.4.3 India

- 14.4.4 Australia

- 14.4.5 South Korea

- 14.5 Latin America

- 14.5.1 Brazil

- 14.5.2 Mexico

- 14.5.3 Argentina

- 14.6 Middle East and Africa

- 14.6.1 South Africa

- 14.6.2 Saudi Arabia

- 14.6.3 UAE

Chapter 15 Company Profiles

- 15.1 ABENA

- 15.2 Attends

- 15.3 B Braun

- 15.4 BD

- 15.5 CardinalHealth

- 15.6 Coloplast

- 15.7 convaTec

- 15.8 essity

- 15.9 FUBURG

- 15.10 Hollister

- 15.11 Kimberly-Clark

- 15.12 MEDLINE

- 15.13 Ontex

- 15.14 unicharm

- 15.15 UROCARE